- Medical Devices

- Human Augmentation Market

Human Augmentation Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Human Augmentation Market by Product Type (Wearable Devices, Augmented Reality (AR) Devices, Biometric Systems, Intelligent Virtual Assistants, Others), Functionality (Body Worn, Non-body Worn), Technology (Wearable, Virtual Reality, Augmented Reality, Exoskeleton, Intelligent Virtual Assistants), End User (Consumer, Commercial, Medical, Defense, Industrial, Others), and Regional Analysis from 2026 to 2033.

Human Augmentation Market Size and Trend Analysis

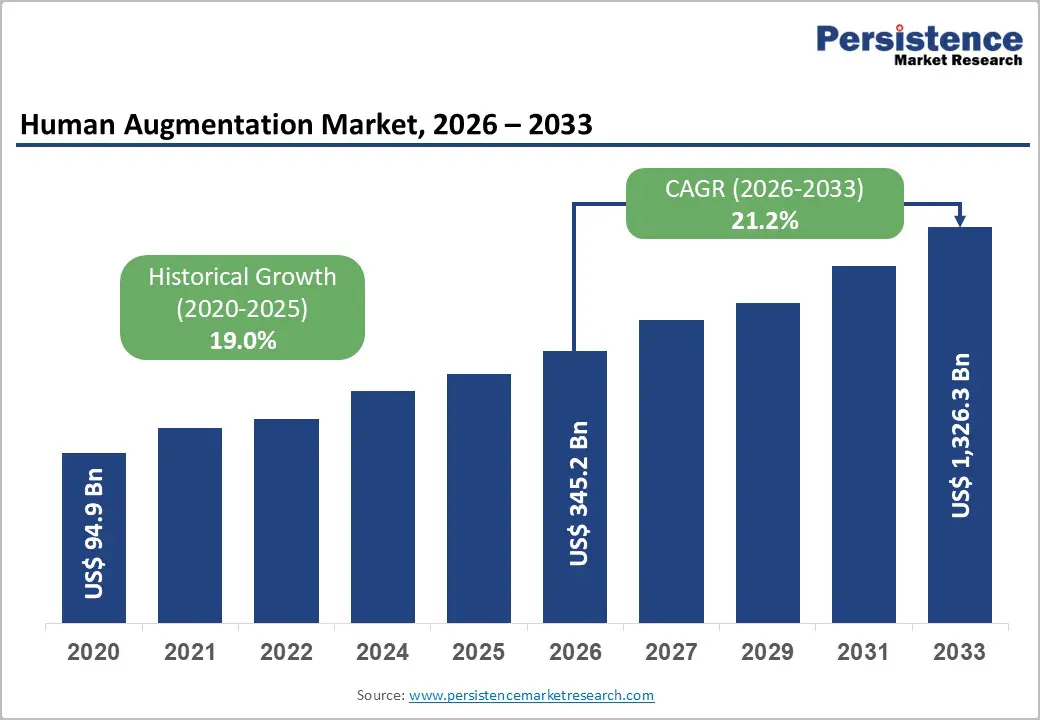

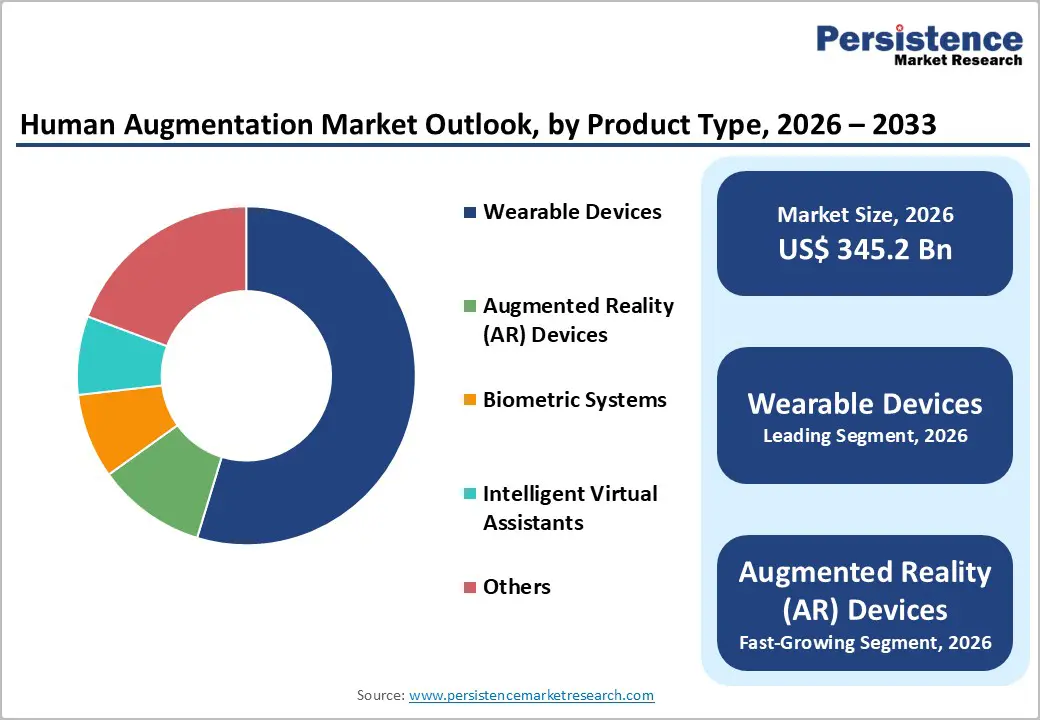

The global human augmentation market is estimated to grow from US$ 345.2 Bn in 2026 to US$ 1,326.3 Bn by 2033. The market is projected to record a CAGR of 21.2% during the forecast period from 2026 to 2033.

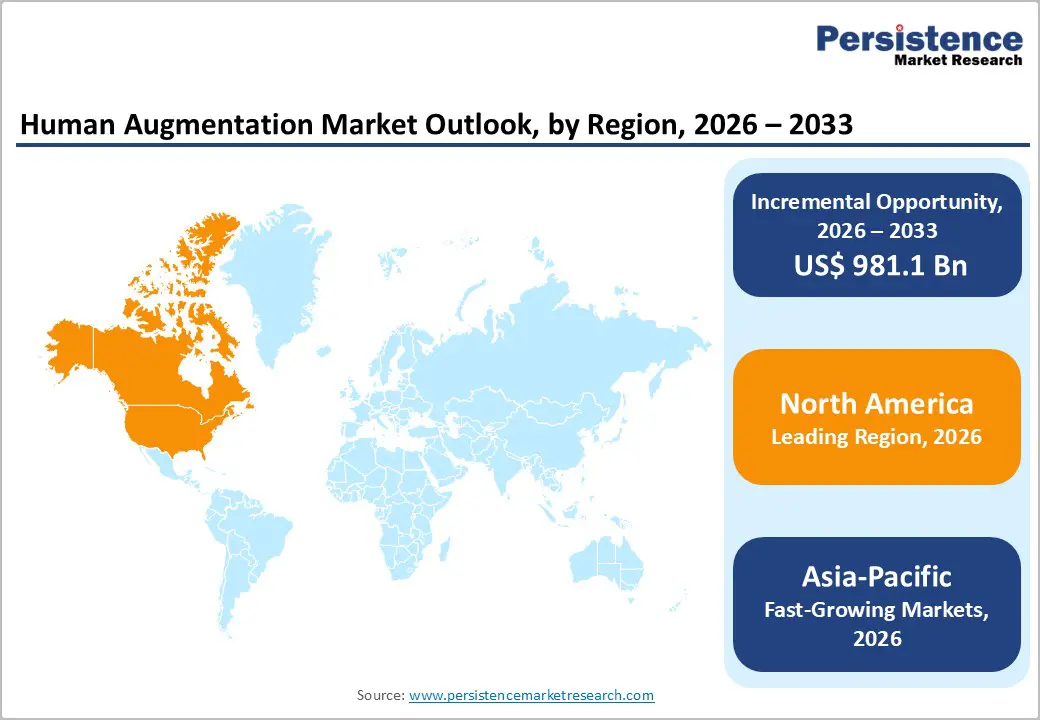

The global human augmentation market is expanding steadily, driven by aging populations, workforce productivity needs, rehabilitation demand, and advances in wearables, exoskeletons, and neurotechnology. North America leads due to strong healthcare infrastructure, defense spending, and rapid adoption, while Asia-Pacific is the fastest-growing, supported by manufacturing scale, rising investments, expanding healthcare access, and favorable government initiatives.

Key Industry Highlights

- Dominant Segment: Wearable devices account for 54.7% share in 2025, driven by widespread adoption of exoskeletons, smart prosthetics, AR wearables, and sensor-based augmentation systems across healthcare, industrial, defense, and rehabilitation settings due to their practicality, mobility support, and real-time performance enhancement.

- Dominant Region: North America leads the market in 2025 with 40.3% share, supported by advanced healthcare infrastructure, strong defense and military investments, high R&D spending, and early adoption of augmentation technologies. Asia-Pacific is the fastest-growing region due to rapid industrialization, expanding healthcare access, rising geriatric population, and government-backed innovation programs.

- Market Drivers: Growth is driven by aging populations, rising disability and rehabilitation needs, demand for workforce productivity and injury reduction, technological advancements in AI, robotics, and neurointerfaces, and increasing use of augmentation solutions in defense, manufacturing, and healthcare.

- Market Opportunity: Key opportunities include expansion of powered exoskeletons in rehabilitation and elderly care, integration of AI and IoT in wearable augmentation systems, growth in industrial and defense applications, cost-effective solutions for emerging economies, and advancements in brain–computer interfaces and human–machine collaboration.

| Global Market Attributes | Key Insights |

|---|---|

| Global Human Augmentation Market Size (2026E) | US$ 345.2 Bn |

| Market Value Forecast (2033F) | US$ 1,326.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 21.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 19.0% |

Market Dynamics

Driver: Increasing adoption of human augmentation in defense, military, and industrial sectors to enhance strength, endurance, and worker safety

The defense and military sectors are increasingly exploring human augmentation technologies, particularly wearable robotics and exoskeletons, to enhance soldier performance, endurance, and injury mitigation. Historically, programs like DARPA-funded exoskeleton research such as the Berkeley Lower Extremity Exoskeleton (BLEEX) demonstrated early efforts to augment load-carrying capacity for warfighters. Contemporary military testing includes passive assist suits evaluated by more than 100 U.S. Army personnel to reduce physical demands and mitigate low back injuries, which historically resulted in over one million lost duty days annually among soldiers. While widespread deployment remains limited, numerous global defense R&D efforts and trials indicate strategic interest in augmentation systems to support physical tasks and force readiness.

Industrial adoption of human augmentation technologies, especially exoskeletons, is driven by the need to reduce musculoskeletal strain and improve workplace safety in sectors with high injury risk. Scientific literature acknowledges that wearable exoskeletons can potentially contribute to occupational health by redistributing biomechanical stress during manual tasks, and industry reports show growing use of passive and active wearables to assist lifting and repetitive motions that cause workplace injuries.

Restraints: High cost of advanced augmentation systems

One of the principal restraints on the human augmentation market is the high cost of advanced devices, which restricts adoption among patients, healthcare providers, and other end users. For example, advanced prosthetic limbs in the United States can cost between USD 15,000 and USD 90,000 depending on complexity, with many high-end myoelectric or bionic models exceeding USD 30,000; reimbursement often covers only a fraction of this cost. Similarly, powered exoskeletons used in rehabilitation and mobility enhancement frequently range from USD 40,000 to USD 120,000 per unit, making them prohibitively expensive without significant insurance or subsidy support.

These elevated price points not only limit individual access but also inhibit broader integration of augmentation technologies across sectors. Healthcare facilities, especially smaller clinics and hospitals in emerging regions, face financial barriers to procuring medical-grade exoskeletons and robotic prosthetics due to limited budgets and inconsistent reimbursement policies. Even in developed markets, insurers often restrict coverage to basic devices, leaving patients to finance advanced systems out-of-pocket. The cumulative effect is a market penetration gap in both low- and middle-income countries and among underinsured populations, suppressing growth potential despite clear clinical and productivity benefits promised by human augmentation.

Opportunity: Rising demand for cost-effective and lightweight exoskeletons in rehabilitation

Demand for cost-effective and lightweight exoskeletons in rehabilitation is increasing as healthcare systems seek efficient patient recovery solutions. Wearable robotic exoskeletons have demonstrated significant clinical benefits, such as improving gait rehabilitation for patients with neurological and musculoskeletal impairments by enabling repetitive, task-specific training and reducing therapist workload, as summarized in peer-reviewed medical literature. Rehabilitation centers and hospitals are integrating these devices to enhance mobility outcomes for stroke and spinal cord injury patients, with global healthcare utilization rising; healthcare accounted for over 50% of exoskeleton demand in 2023, highlighting strong clinical adoption.

Researchers funded by major U.S. agencies like the National Institutes of Health (NIH) are actively developing exoskeleton systems that reduce metabolic effort and improve walking performance in real-world conditions, indicating strong institutional support for affordable, practical rehabilitation technologies. Such devices have increased walking speed while reducing energy expenditure by up to 17% compared with unassisted walking, demonstrating measurable therapeutic benefits. Lightweight and adaptable exoskeletons that use wearable sensors and streamlined control systems are being prioritized in academic research to overcome traditional barriers related to cost and usability, expanding their applicability in clinical and outpatient rehabilitation settings.

Category-wise Analysis

By Product Type, Wearable Devices Dominates the Human Augmentation Market

Monitors occupies 45.6% share of the global market in 2025, because they are widely adopted, non-invasive, and deeply integrated into everyday life. According to International Data Corporation (IDC), global shipments of wearable devices, including smartwatches, fitness trackers, and hearables surpassed 537.9 million units in 2024 and continue to grow, reflecting strong consumer adoption worldwide. Additionally, studies show that a substantial portion of the U.S. population owns wearables, with ownership rates approaching 44.5 % in some surveys, underscoring their penetration among diverse demographic groups. Wearables’ ability to provide continuous health data (heart rate, activity, sleep) and real-time feedback has cemented their role in augmentation, making them practical tools for health management, rehabilitation support, and performance tracking without surgical or complex installations.

By Functionality, Body-worn human augmentation dominates due to widespread wearable adoption, non-invasive use, and proven benefits in mobility, safety, and health monitoring

By functionality, body-worn systems dominate the human augmentation market because they deliver direct, tangible enhancement of physical performance, health monitoring, and mobility support without invasive procedures. A substantial portion of adults use body-worn health devices: a U.S. National Health Interview Survey found that over 30 % of adults regularly use wearable health trackers to monitor activity or physiological signals, demonstrating widespread acceptance of body-worn augmentation for health management. Body-worn devices also include powered and passive exosuits, prosthetics, and supportive orthoses that assist mobility; NIH-funded studies have shown body-worn exoskeletons can increase walking speed and reduce metabolic cost in rehabilitation settings, highlighting clinical benefit. This combination of broad consumer use and clinical efficacy underpins dominance of body-worn augmentation functionality.

Regional Insights

North America Human Augmentation Market Trends

North America dominates the human augmentation market with 40.3% share in 2025, because of strong public research investment, advanced technology infrastructure, and widespread clinical adoption. The United States conducts nearly half of global biomedical research in the life sciences, giving it a scientific lead in developing prosthetics, neural interfaces, and wearable augmentation systems. Government healthcare data also highlight significant clinical demand: the Centers for Disease Control and Prevention (CDC) reports that approximately 13.7?percent of U.S. adults (over 20?million people) have a mobility disability, many of whom benefit from assistive and robotic augmentation devices.

Federal funding mechanisms such as NIH rehabilitation research grants and Department of Veterans Affairs prosthetics programs support continued innovation and deployment, while established regulatory pathways (e.g., FDA approvals) and robust healthcare infrastructure enable rapid integration of augmentation technologies in medical, industrial, and defense settings.

Europe Human Augmentation Market Trends

Europe is an important region in the human augmentation market due to its advanced healthcare systems, strong regulatory frameworks, and significant research investment in assistive technologies. European Union programs like Horizon Europe and the Digital Europe Programme allocate substantial funding toward robotics, AI integration, and assistive device development, supporting both clinical and industrial augmentation solutions. For example, EU disability strategies and national healthcare policies in countries such as Germany and France expand reimbursement and access for assistive technologies, including wearable robotics and exoskeletons. Additionally, Europe’s aging population, where over 21.3% of residents were aged 65 and over in 2023 according to Eurostat drives demand for mobility support and rehabilitation devices. This combination of policy support, demographic need, and innovation infrastructure positions Europe as a key regional market for human augmentation technologies.

Asia-Pacific Human Augmentation Market Trends

Asia Pacific is the fastest?growing region in the human augmentation market because of rapid demographic shifts, rising healthcare needs, and strong technological uptake. The region’s population is aging quickly; by 2050, about one in four people in Asia Pacific will be aged 60 or older, significantly increasing demand for mobility support and assistive technologies that enhance quality of life. Aging populations in countries such as Japan, China, and South Korea are already driving adoption of wearable robotics and assistive devices to support eldercare and rehabilitation.

In parallel, economic growth and expanding digital infrastructure are enabling broader integration of augmentation technologies in healthcare and industrial applications. Increasing chronic disease burdens and limited healthcare workforce availability further compel governments and providers to adopt automation and augmentation solutions, supporting both clinical needs and workforce augmentation.

Market Competitive Landscape

The human augmentation market is highly competitive, led by global and regional players offering wearable, portable, and stationary systems. Competition is fueled by innovations in AI, connectivity, and non-invasive devices, alongside focus on accuracy, safety, and regulatory compliance. Strategic collaborations, R&D investments, and regional expansion further drive differentiation and market intensity worldwide.

Key Industry Developments:

- In December 2025, Google announced that it had partnered with eyewear brands, including Warby Parker, to develop AI?powered smart glasses that were expected to launch in 2026. The collaboration was unveiled at an Android XR event, marking Google’s renewed push into wearable AI after earlier smart glasses efforts.

- In January 2024, Sony Corporation had announced development of a spatial content creation system featuring a high?quality XR head?mounted display and dedicated controllers for intuitive interaction with three?dimensional objects.

Companies Covered in Human Augmentation Market

- Google LLC (Alphabet Inc.)

- ReWalk Robotics Ltd.

- Sony Corporation

- Touch Bionics Inc. (Össur)

- Ekso Bionics Holdings, Inc.

- Microsoft Corporation

- Cyberdyne Inc.

- Huawei Technologies Co., Ltd.

- B-Temia Inc.

- Samsung Electronics Co., Ltd.

- Wandercraft

- Hocoma AG (DIH Technologies)

- Rex Bionics Ltd.

- Wearable Robotics SRL

- Facebook Reality Labs (Meta Platforms, Inc.)

Frequently Asked Questions

The global human augmentation market is projected to be valued at US$ 345.2 Bn in 2026.

Aging populations, healthcare needs, industrial and defense applications, technological advancements, and wearable device adoption drive growth.

The global human augmentation market is poised to witness a CAGR of 21.2% between 2026 and 2033.

Opportunities include affordable exoskeletons, AI integration, industrial adoption, elderly care, rehabilitation, and brain computer interfaces.

Google LLC (Alphabet Inc.), ReWalk Robotics Ltd., Sony Corporation, Touch Bionics Inc. (Össur), Ekso Bionics Holdings, Inc., Microsoft Corporation.