- Technology

- Human Capital Management (HCM) Market

Human Capital Management (HCM) Market Size, Share, and Growth Forecast 2026 - 2033

Human Capital Management (HCM) by Component (HCM Software - Integrated HCM Suite, Recruitment Management, Workforce Management, Employee Engagement; HCM Services - Professional Services), Deployment (Cloud, On-premise), Enterprise Size (Large Enterprises, Small & Medium Enterprises), Industry (IT & Telecom, BFSI, Retail, Healthcare, Government, Manufacturing, Education, Others), by Regional Analysis, 2026 - 2033

Human Capital Management Market Size and Trend Analysis

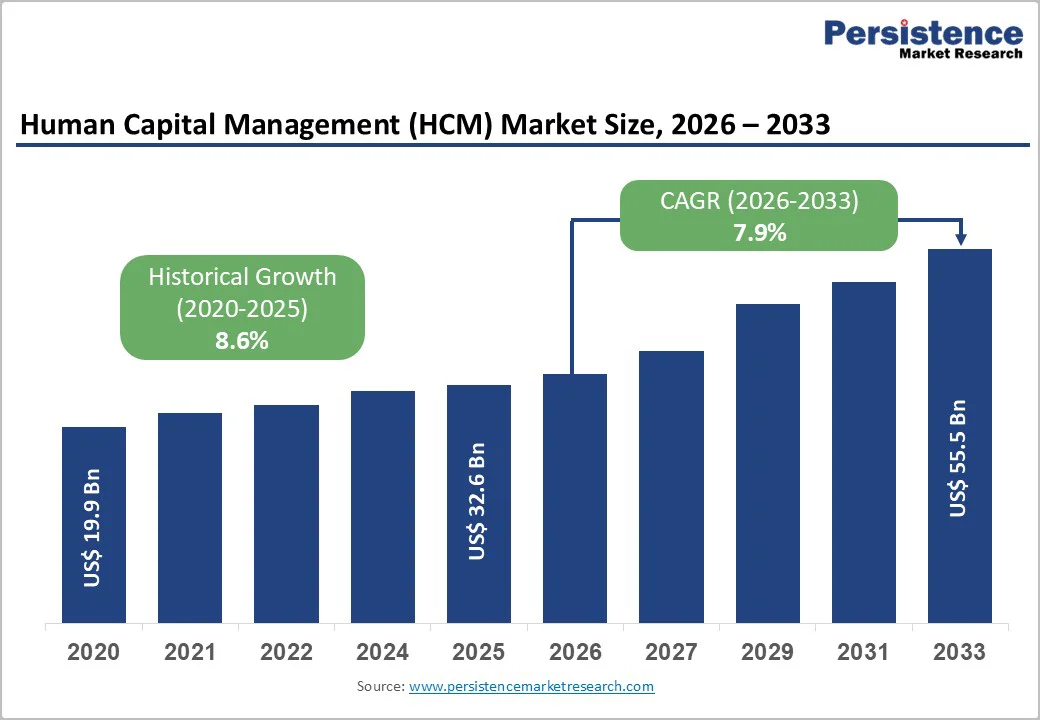

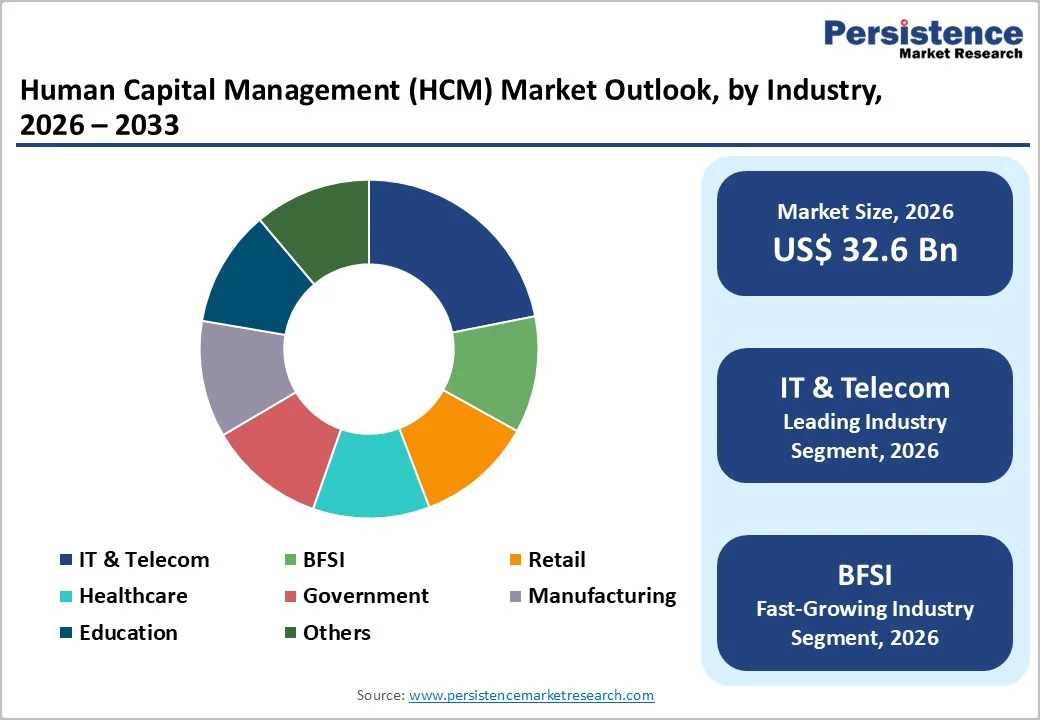

The global human capital management market size is likely to be valued at US$ 32.6 billion in 2026 and projected to reach US$ 55.5 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

The HCM market experiences accelerated expansion driven by convergence of three transformative trends: enterprise-wide digital modernization replacing legacy on-premise systems with cloud-native architectures, integration of artificial intelligence and machine learning into core HR processes improving decision-making and operational efficiency, and fundamental shifts in workforce dynamics necessitating flexible, scalable HCM solutions addressing remote and hybrid work arrangements.

Key Market Highlights

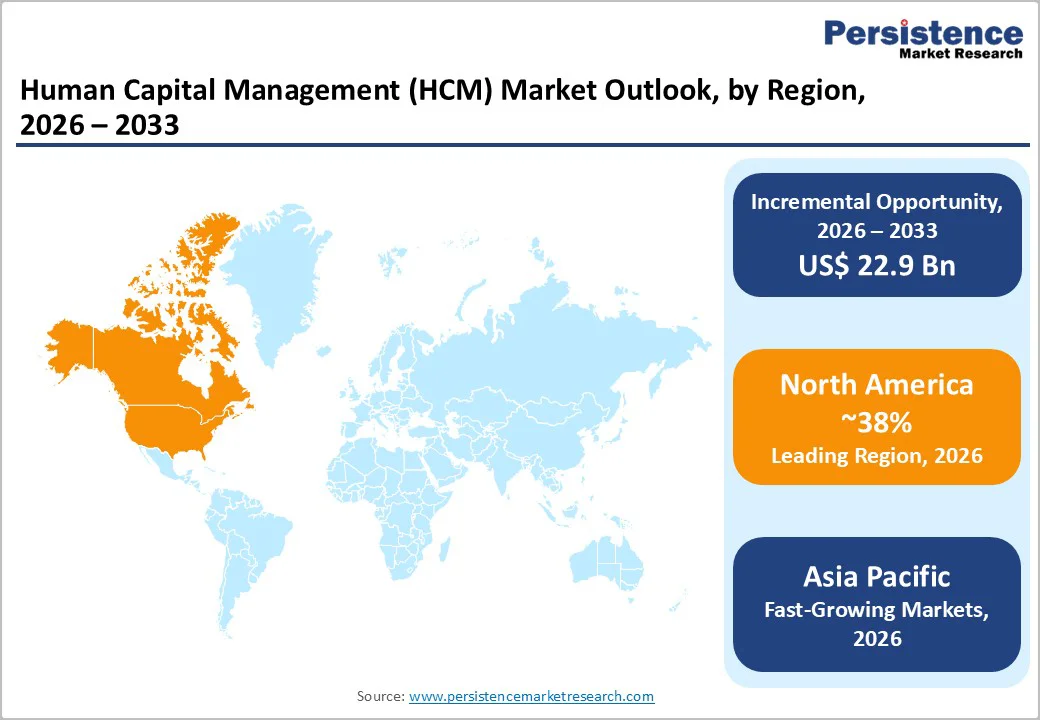

- Leading Region: North America leads the global HCM market with about 38% share in 2025, supported by advanced technology adoption, strong IT spending, and innovation-driven HR modernization.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with 11.2% CAGR through 2032, fueled by rapid digital transformation, SME adoption, and expanding enterprise operations across major economies.

- Dominating Segment: Integrated HCM suites dominate the market with 58% share in 2025 as organizations favor unified platforms covering end-to-end workforce management functions.

- Fastest-Growing Segment: Cloud deployment is the fastest-growing segment at 7.5% CAGR through 2032, driven by strong SME demand, modern workforce needs, and cloud’s 76% revenue share in 2024.

- Key Opportunity: AI and ML adoption offer the strongest opportunity by enabling HR automation, predictive analytics, and personalized workforce support, with Gartner projecting 33% of enterprise apps using agentic AI by 2028.

| Key Insights | Details |

|---|---|

| Human Capital Management Market Size (2026E) | US$ 32.6 billion |

| Market Value Forecast (2033F) | US$ 55.5 billion |

| Projected Growth CAGR (2026 - 2033) | 7.9% |

| Historical Market Growth (2020 - 2025) | 8.6% |

Market Dynamics

Drivers - Cloud Migration Acceleration and Enterprise Digital Transformation

Cloud-based HCM adoption represents the dominant growth catalyst, with cloud solutions accounting for 76% of total HCM revenue in 2024 and expected to reach 99% CAGR through 2030, fundamentally reshaping enterprise HR infrastructure investment patterns. Organizations are transitioning from legacy on-premise systems to modern cloud suites to achieve operational efficiency through centralized payroll processing, simplified workforce management across multiple regions, enhanced regulatory compliance automation, and actionable insights derived from unified data platforms. The shift toward cloud deployment delivers substantial economic benefits through reduced total cost of ownership, faster implementation cycles, scalable user licensing models supporting organizational growth, and eliminated infrastructure maintenance burdens. Enterprise HCM buying decisions increasingly prioritize outcome-based metrics including employee growth, talent agility, skills management, and worker experience rather than traditional feature-based comparisons, creating a preference for comprehensive cloud platforms enabling integrated workforce strategies across recruitment, performance management, learning, and compensation functions.

Artificial Intelligence and Predictive Analytics Integration

Artificial intelligence and machine learning capabilities are transforming HCM platforms from reactive administrative systems to proactive talent optimization engines, enabling recruitment automation, performance prediction, and workforce planning with unprecedented analytical sophistication. Generative AI integration enables automation of routine inquiries, provide personalized employee support, deliver tailored learning recommendations, and generate actionable insights from workforce data supporting strategic decision-making at organizational levels. AI-powered recruitment systems demonstrate capability to scan resumes, analyze job descriptions, and match candidates based on skills, experience, and cultural fit with significantly improved speed and reduced bias compared to manual processes, while predictive analytics detect patterns in employee behavior including early disengagement signals enabling proactive retention interventions. Organizations are leveraging AI-enabled workforce analytics to anticipate future talent needs through predictive modeling of employee attrition, skills demand identification, and organizational restructuring requirements, establishing competitive advantages through strategic workforce planning replacing reactive hiring approaches.

Restraints - Implementation Complexity and User Adoption Challenges

HCM cloud implementations encounter substantial technical and organizational obstacles that compress implementation timelines, escalate project costs, and compromise realization of expected business benefits and return on investment. Data migration complexities represent the most critical implementation barrier, with enterprises underestimating effort requirements for legacy data extraction, cleansing, validation, and integration into modern cloud environments accommodating different data structures and business logic frameworks. Integration difficulties arise from legacy systems incompatibility, third-party application connectivity requirements, and organizational silos requiring configuration of complex middleware solutions elevating implementation costs by 15-30% above initial budgets. Critical user adoption and training deficiencies represent the most significant implementation success factor, with organizations frequently allocating insufficient resources toward comprehensive change management, process redesign education, and end-user skill development necessary to transform behavioral patterns and maximize platform utilization.

Multi-System Integration and Compliance Complexity

Organizations operating across multiple jurisdictions and industry verticals confront escalating compliance requirements demanding sophisticated HCM platform capabilities accommodating diverse regulatory frameworks, labor standards, tax codes, and data protection mandates creating implementation barriers particularly for mid-market enterprises. GDPR data residency requirements restrict personal data movement across geographies, imposing penalties of up to 4% of global annual turnover or €20 million whichever is higher for non-compliance, necessitating HCM solutions supporting regional data segregation, encryption, and access controls meeting stringent European regulatory standards. Industry-specific compliance obligations in healthcare, financial services, and government sectors demand HCM platforms supporting specialized audit trails, segregation of duties, compensation transparency requirements, and employment verification protocols exceeding general enterprise capabilities and elevating implementation complexity for multi-industry organizations.

Opportunities - Rapid Enterprise Adoption of Employee Experience and Wellness Solutions

Employee experience optimization represents the fastest-growing opportunity segment within HCM markets, driven by escalating competitive talent markets, generational workforce preferences emphasizing work-life balance and purpose-driven employment, and measurable productivity correlations with engagement levels. Organizations increasingly recognize that engaged employees demonstrate 18% greater productivity and 23% higher profitability compared to disengaged counterparts, creating strong economic justification for investments in comprehensive employee experience platforms encompassing wellness programs, career development tools, feedback mechanisms, and recognition systems. Digital workplace market projected to grow from US$ 26.4 billion in 2024 to US$ 135.1 billion by 2031 at a 23.83% CAGR, with SMEs representing the fastest-growing segment at 20.7% CAGR, reflecting rapid adoption among cost-conscious organizations discovering competitive advantages through flexible work arrangements and cloud-based collaborative tools. HCM platforms enabling personalized employee journeys through AI-driven career path recommendations, skills development tracking, compensation transparency, and mentorship program matching position providers to capture premium pricing and expand market share among organizations pursuing talent retention strategies.

SME Market Expansion and Cost-Effective Cloud Solutions

Small and Medium Enterprises (SMEs) represent the highest-growth market opportunity within HCM segments, with 97% of businesses in the APEC region classified as SMEs and employment representing 60-80% of the regional workforce, establishing enormous addressable market with underpenetrated technology adoption. SME HCM adoption accelerates through cost-effective cloud solutions eliminating prohibitive on-premise infrastructure investments, offering straightforward pricing models, and delivering automation capabilities vital for resource-constrained HR teams managing increased compliance complexity and administrative burdens without proportional staffing expansion.

Emerging regional HCM providers from India, including Darwin Box, People Strong, Zing HR, and Hono HR establish competitive positions through purpose-built SME solutions offering superior affordability, cultural relevance, compliance with local regulatory frameworks, and localized support, contrasting with enterprise-focused platforms designed for large organization complexity. The emerging market opportunity encompasses an estimated US$ 200+ million incremental HCM demand through 2032 from metro expansion and regional economic growth in Asia Pacific urban centers, supporting competitive positioning for providers developing localized solutions addressing SME operational constraints.

Category-wise Analysis

Component Insights

The integrated human capital management suite segment dominates the HCM component market with approximately 58% market share in 2025, reflecting organizational preference for unified platforms providing comprehensive HR functionality across recruitment, payroll, performance management, learning and development, and employee engagement from single technology vendors. Integrated HCM suites deliver competitive advantages through seamless data flow across HR functions, unified employee records eliminating duplicate data entry, simplified system administration and governance requirements, and superior total cost of ownership compared to point solution architectures requiring multiple vendor relationships and complex integration frameworks.

Leading vendors including Oracle Fusion Cloud HCM, Workday, SAP SuccessFactors, and Microsoft Dynamics 365 Human Resources maintain market dominance through continuous innovation in suite capabilities, AI integration, user experience enhancement, and geographic expansion supporting evolving organizational requirements. Organizations increasingly recognize that integrated platforms reduce implementation complexity, accelerate time-to-value, and enable superior analytics compared to fragmented technology stacks, supporting premium pricing and market share consolidation among major providers.

Deployment Insights

The cloud deployment model commands clear market leadership with approximately 76% of total HCM market share in 2025, reflecting structural preference for software-as-service delivery models offering scalability, flexibility, and reduced capital intensity compared to on-premise alternatives. Cloud HCM solutions eliminate substantial infrastructure investment requirements, enable rapid feature updates and capability enhancements through centralized vendor management, support seamless user accessibility across geographies and devices, and facilitate compliance automation through built-in regulatory framework integrations addressing labor law complexity across jurisdictions. The cloud segment is anticipated to expand at approximately 7.5% CAGR through 2032, driven by accelerating migration of legacy systems, increased adoption among SMEs discovering cost-effectiveness and operational agility advantages, and enterprise demand for AI-native cloud platforms supporting emerging talent management requirements. Cloud HCM deployment delivers particular advantages for organizations managing distributed and hybrid workforces requiring seamless collaboration infrastructure, real-time data visibility, and mobile-first user interfaces supporting flexible work arrangements becoming standard across professional services, technology, and financial services sectors.

Enterprise Size Insights

The large enterprises segment maintains market dominance with approximately 62% HCM market share in 2025, driven by substantial technology investment budgets, complex organizational structures requiring sophisticated workforce management capabilities, and prioritization of integrated talent management supporting thousands of employees across global operations. Large enterprises deploy comprehensive HCM suites supporting specialized requirements including multi-entity payroll consolidation, complex benefits administration, international workforce management across diverse regulatory jurisdictions, and advanced analytics supporting workforce optimization and strategic planning. The large enterprise segment demonstrates steady 6.8% CAGR expansion through 2032, supported by continuous technology upgrades, enterprise expansion into emerging markets, and integration of acquired organizations necessitating enhanced HCM capabilities supporting post-merger workforce integration and cultural alignment.

Industry Insights

The IT & Telecom sector leads HCM industry adoption with approximately 21% market share in 2025, driven by severe skilled talent competition, rapid workforce expansion supporting innovation cycles, and critical dependence on effective recruitment and retention capabilities supporting competitive positioning in dynamic technology markets. IT and telecom companies prioritize HCM solutions enabling talent acquisition acceleration, continuous workforce upskilling supporting technological change, and sophisticated talent analytics identifying high-potential employees and succession pipeline development.

The BFSI (Banking, Financial Services, and Insurance) sector represents the fastest-growing industry vertical with anticipated 8.9% CAGR through 2032, driven by regulatory compliance intensification, digital transformation acceleration, and expanded investment in customer-facing talent attracting consumer preference and competitive differentiation. Financial services organizations increasingly adopt AI-powered HCM capabilities supporting regulatory reporting, anti-money laundering compliance, customer onboarding acceleration, and talent optimization in highly competitive compensation environments.

Regional Insights

North America Human Capital Management Trends

North America maintains global HCM market leadership with approximately 38% market share in 2025, established through advanced technology adoption, substantial enterprise IT budgets, and innovation-driven HR practices influencing global standards. The region benefits from early adoption of cloud technologies by leading technology companies and financial institutions, establishing reference customers validating HCM solution capabilities and supporting technology vendor marketing efforts.

North America demonstrates advanced HCM adoption patterns emphasizing employee experience optimization, diversity and inclusion management, and workforce analytics supporting strategic talent management. Organizations across professional services, technology, financial services, and healthcare sectors compete intensively for skilled talent, justifying premium HCM platform investments and sophisticated onboarding programs supporting new hire productivity acceleration. Remote and hybrid work expansion following pandemic disruption accelerates regional HCM adoption as organizations seek sophisticated platforms managing distributed teams, enabling seamless collaboration, and supporting flexible arrangement administration.

Europe Human Capital Management Trends

Europe represents the second-largest HCM market with approximately 28% global market share in 2025, characterized by stringent data protection regulations, emphasis on employee rights and protections, and regulatory harmonization efforts across diverse national jurisdictions. Organizations across Germany, United Kingdom, France, and Spain prioritize HCM solutions providing localized payroll processing, benefits administration, and employment contract management accommodating diverse national labor laws and collective bargaining arrangements.

European HCM market exhibits particular emphasis on employee wellness, work-life balance, and rights protection reflecting cultural values and regulatory mandates establishing higher standards for employment practices compared to North American markets. Organizations increasingly adopt HCM solutions supporting flexible work arrangements, leave management, and employee engagement recognizing competitive talent market requirements and workforce expectations prioritizing organizational values alignment and personal development opportunities.

Asia Pacific Human Capital Management Trends

Asia Pacific emerges as the highest-growth HCM region with anticipated 11.2% CAGR through 2032, driven by rapid digital transformation acceleration, expanding business operations across China, Japan, India, and Southeast Asian markets, and accelerating SME technology adoption addressing competitive pressures and regulatory compliance requirements. The region experiences unprecedented workforce expansion, urbanization, and rising labor cost pressures incentivizing organizations to invest in HCM technology enabling workforce optimization, automation of administrative functions, and data-driven talent management.

India represents the fastest-growing Asia Pacific market, with accelerating enterprise digital transformation across manufacturing, IT services, and financial services sectors establishing significant HCM opportunity. China and Japan maintain mature HCM adoption patterns with emphasis on workforce planning supporting aging population challenges, skills development addressing technology transformation requirements, and retention initiatives addressing generational workforce dynamics. Southeast Asian markets including Indonesia, Vietnam, Philippines, and Thailand experience rapid HCM adoption growth driven by manufacturing expansion, business process outsourcing acceleration, and SME digital transformation initiatives.

Competitive Landscape

The global HCM market is moderately consolidated, with major vendors controlling over two-third of total revenue and more than 50 regional or niche providers competing in specific geographies and industry verticals. Market structure is shaped by platform breadth, integration depth, and the ability to deliver unified HCM ecosystems that scale across large enterprise environments. Leading vendors strengthen their position through investments in AI-native architectures, configuration intelligence, and automation tools that reduce deployment timelines and enhance user adoption. Competitive strategies increasingly revolve around improving implementation efficiency, expanding partner ecosystems, and offering modular cloud-based services that lower total cost of ownership. Regional challengers differentiate through pricing advantages, localized compliance support, and mobile-first design targeting SMEs with lighter, flexible deployments. As agentic AI and predictive analytics become central to HCM strategy, vendors prioritize autonomous decision support, seamless multi-system integration, and outcome-based service models to build long-term recurring revenue streams and sustain competitive advantage.

Key Market Developments

- February 2025: Workday announces its new Agent System of Record and AI-agent marketplace enabling organizations to deploy and manage AI agents for HR, payroll, contracts, auditing and policy tasks alongside human staff.

- September 2024: Oracle Cloud HCM 24B update brings enhanced data-loader automation for bulk data operations, improved HR “Journeys” workflows including new survey and electronic-signature options, and modernized UI for core HR and succession-management modules.

- October 2024: SAP announces expanded integration and AI enhancements in SAP SuccessFactors, enabling unified HR data flow, skills-based workforce planning, and streamlined cross-system workflows across HR, payroll and core business suites.

Companies Covered in Human Capital Management (HCM) Market

- Oracle Corporation

- Workday, Inc.

- SAP SE

- Microsoft Corporation

- Darwin Box

- People Strong

- Zing HR

- Hono HR

- Ramco Systems Limited

- BambooHR

- MenaTech

- EmiratesHR

- GulfHR

- SumTotal Systems, Inc.

- DataOn

- Hitachi Vantara

- Kronos Workforce

- ADP Global

- Cornerstone OnDemand

- Paychex

Frequently Asked Questions

The HCM market is expected to reach US$ 55.5 billion by 2033, driven by cloud adoption, remote work expansion, AI integration, and rising compliance needs.

Enterprises adopt HCM for digital HR transformation, regulatory compliance automation, better employee experience, and remote workforce management, supported by proven productivity and profitability gains.

Integrated HCM suites lead with about 58% share in 2025 due to unified HR data, lower ownership costs, simplified administration, and seamless functionality across all HR processes.

North America leads with roughly 38% share, while Asia Pacific grows fastest at 11.2% CAGR, supported by rapid digitalization and large SME-driven adoption.

AI and machine learning offer the strongest opportunity, enabling automation, predictive analytics, and personalized workforce management, creating a US$ 200+ million annual revenue stream by 2032.

The market is led by major suite providers Oracle Corporation, Workday, Inc., SAP SE, and Microsoft Corporation.