- Food Ingredients & Additives

- Herbs Flavor Market

Herbs Flavor Market Size, Share, and Growth Forecast, 2026 – 2033

Herbs Flavor Market by Product Type (Natural, Organic, Synthetic), Form (Liquid, Powder, Paste), Application (Food & Beverages, Pharmaceuticals, Nutraceuticals, Cosmetics & Personal Care), and Regional Analysis for 2026-2033

Herbs Flavor Market Share and Trends Analysis

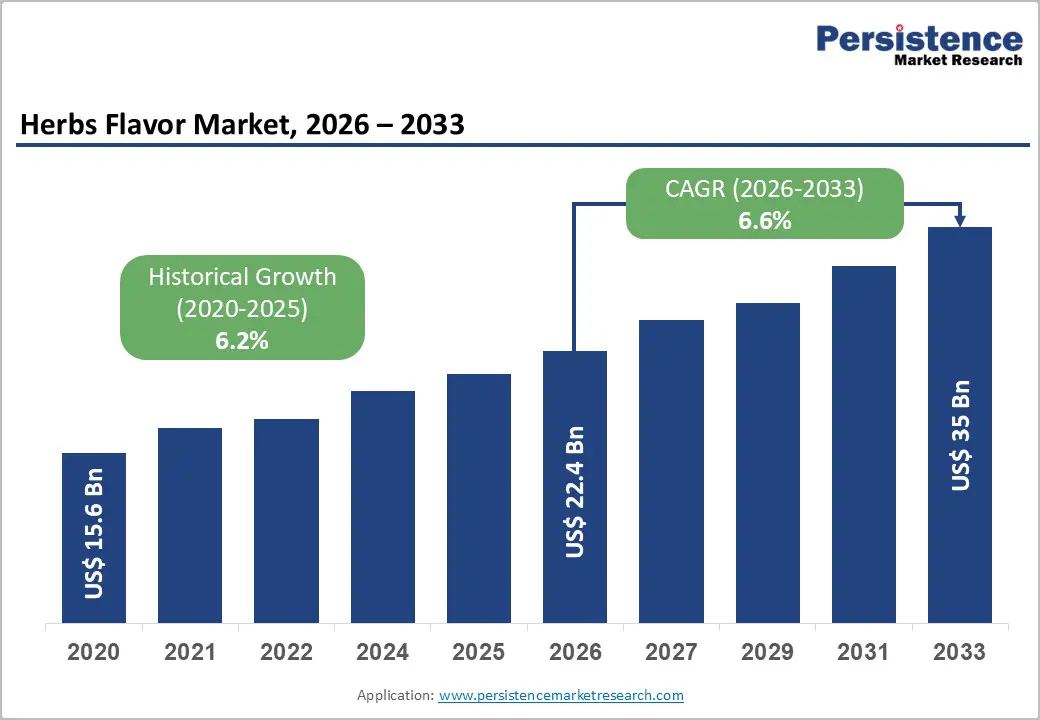

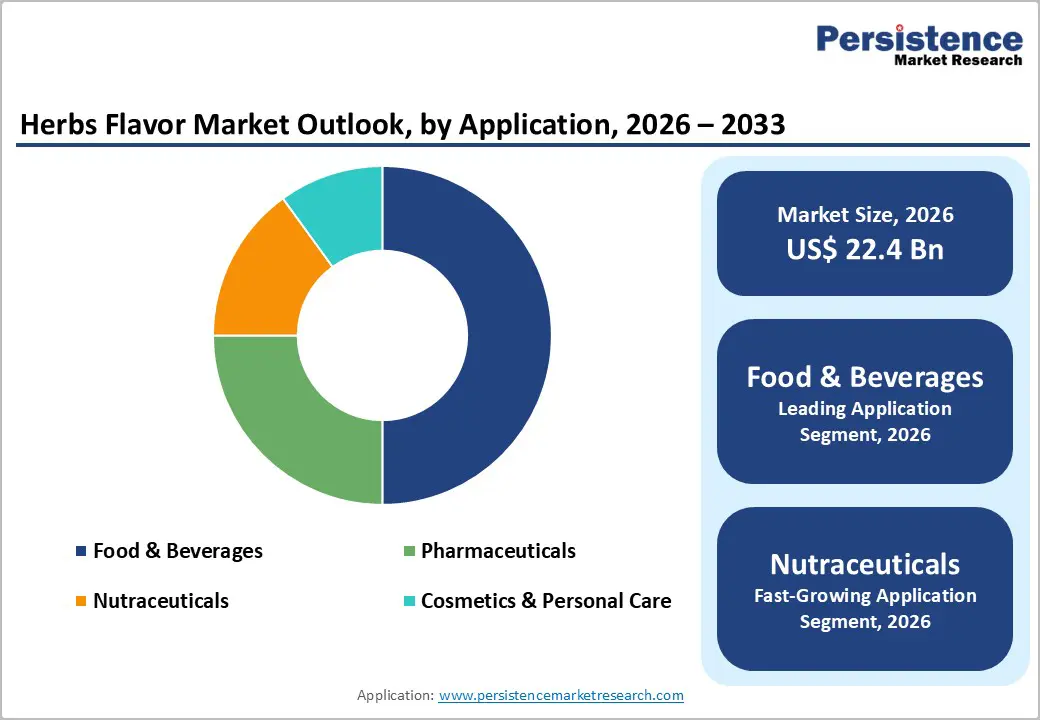

The global herbs flavor market size is likely to be valued at US$ 22.4 billion in 2026, and is projected to reach US$ 35 billion by 2033, growing at a CAGR of 6.6% during the forecast period 2026−2033. Market expansion is driven by increasing consumer preference for natural ingredients, stimulating demand for herbs flavors through health-conscious consumption patterns and awareness initiatives led by regulatory agencies. Advancements in extraction technologies and flavor formulation support efficient, stable, and versatile product development, enabling wider application across food, beverages, and personal care categories. Rising demand within pharmaceutical and nutraceutical sectors emerges from the integration of herb-derived bioactives into functional and preventive health products. Regulatory alignment with food safety and labeling standards strengthens adoption across industrial and commercial segments by improving compliance confidence and product transparency. Expansion of global distribution networks and e-commerce platforms enhances accessibility and cost efficiency, supporting broader market penetration across emerging and developed economies.

Key Industry Highlights

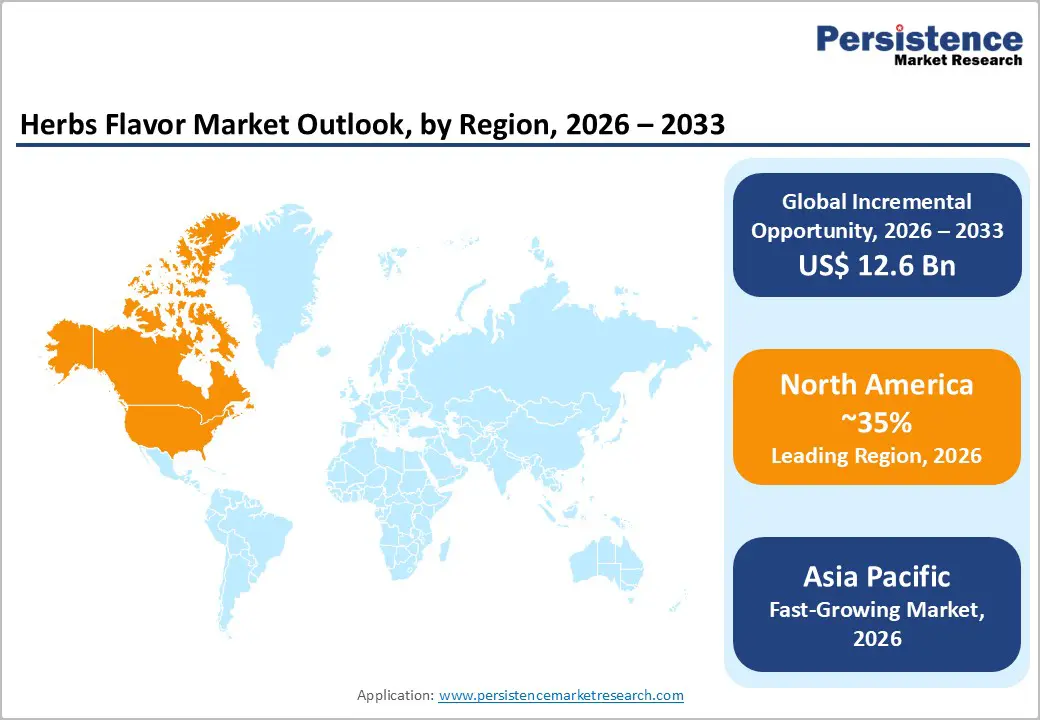

- Dominant Region: North America is projected to lead with a 35% market share in 2026, supported by widespread adoption of herb-based flavors and clean-label trends.

- Fastest-growing Market: Asia Pacific is set to be the fastest-growing market from 2026 to 2033, driven by expanding retail and e-commerce access for innovative natural ingredients across food, beverages, and personal care.

- Leading Application: The food & beverages segment is expected to capture 50% market share in 2026, aided by regulatory compliance, supply chain efficiency, and consumer demand for natural flavors.

- Fastest-growing Application: The nutraceuticals segment is projected as the fastest-growing from 2026 to 2033, propelled by herbal extract integration, digital delivery, regulatory incentives, and preventive health trends.

- September 2025: Fresh Express launched its Mediterranean Herb Chopped Salad Kit, featuring kale, green/red cabbage, carrots, green leaf lettuce, crispy chickpeas, feta cheese, and zesty lemon-oregano vinaigrette.

| Key Insights | Details |

|---|---|

|

Herbs Flavor Market Size (2026E) |

US$ 22.4 Bn |

|

Market Value Forecast (2033F) |

US$ 35 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Consumer Preference for Natural Ingredients

Consumer inclination for natural ingredients is gaining swift traction worldwide, fueled by an evolving trend toward transparency, ingredient familiarity, and perceived wellness alignment. Buyers increasingly evaluate product formulations through clean-label criteria, favoring plant-based flavor sources over synthetic alternatives. Herbs-derived inputs align with expectations related to authenticity, traditional usage, and traceability, which strengthens brand credibility across food, beverage, and personal care portfolios. Urbanization, rising disposable income, and exposure to global wellness trends reinforce demand for formulations perceived as minimally processed and culturally rooted. Retail positioning strategies emphasize natural sourcing narratives, reinforcing purchasing decisions at the point of sale.

Health awareness campaigns and regulatory guidance influence purchasing behavior by linking natural ingredients with long-term dietary balance and preventive lifestyle choices. Herbs-origin flavoring agents benefit from historical association with culinary practices and botanical remedies, supporting acceptance across diverse demographic groups. Innovation teams prioritize natural flavor systems to align with reformulation goals, sugar reduction strategies, and artificial additive replacement initiatives. Product developers leverage herbs-based profiles to differentiate offerings in competitive categories while maintaining sensory consistency. Institutional buyers and private-label operators increasingly specify natural inputs within sourcing frameworks to meet compliance benchmarks and sustainability objectives.

Risk of Contamination and Adulteration

Contamination and adulteration risks represent a key restraint for the herbs flavor market growth owing to structural vulnerabilities across agricultural sourcing and primary processing stages. Herb cultivation often occurs in fragmented farming systems with varying agronomic practices, creating inconsistent control over soil quality, irrigation water, pesticide residues, and post-harvest handling. Exposure to microbial pathogens, heavy metals, and foreign matter arises from open-field cultivation and manual harvesting methods. Adulteration risk increases through intentional dilution with low-cost fillers, synthetic aroma compounds, or non-declared plant materials to stabilize margins under price pressure. Limited traceability in multi-tier supply chains weakens verification of botanical origin and purity, reducing confidence among large-scale buyers.

Quality assurance challenges intensify during extraction, blending, and cross-border trade activities. Inconsistent adherence to Good Manufacturing Practices creates gaps in sanitation control, solvent management, and batch segregation. Regulatory frameworks differ widely across producing and importing economies, leading to uneven enforcement of contaminant thresholds and authenticity standards. Laboratory testing for botanical identity, pesticide residues, and microbial load involves high cost and specialized expertise, limiting routine verification for small and mid-sized processors. Reputational exposure linked to contamination incidents elevates compliance risk for food, beverage, pharmaceutical, and personal care manufacturers, resulting in cautious procurement strategies.

Innovation in Clean-Label Products

An exciting opportunity for companies operating in the market for herb flavors is developing clean-label products as consumer decision-making increasingly prioritizes ingredient transparency, simplified formulations, and recognizable sources. Clean-label positioning aligns with evolving dietary expectations shaped by wellness-focused lifestyles, preventive health awareness, and skepticism toward synthetic additives. Herbs-based flavors naturally support these expectations through plant-derived origins, minimal processing perception, and compatibility with organic and natural product positioning. Food and beverage manufacturers seek differentiation through labels that communicate authenticity, traceability, and functional value, strengthening demand for innovative formulations derived from herbs.

Advances in formulation science enable clean-label innovation without compromising taste stability, shelf life, or sensory consistency, addressing earlier technical limitations associated with natural ingredients. Encapsulation, cold extraction, and solvent-free processing improve flavor performance while maintaining compliance with clean-label standards. This capability expands adoption across categories such as ready-to-eat foods, beverages, dietary supplements, and personal care products where ingredient scrutiny remains high. Regulatory emphasis on transparent labeling frameworks further reinforces this opportunity by encouraging reformulation toward simpler ingredient decks. Clean-label innovation supports alignment with private-label strategies, export readiness, and cross-category application flexibility.

Category-wise Analysis

Product Type Insights

Natural herb flavors are poised to lead with a forecasted 45% share in 2026, owing to consumer preference for unprocessed, recognizable ingredients. Natural variants are incorporated across food, beverage, and nutraceutical formulations due to perceived health benefits and regulatory acceptance. Supply chain optimization and scalable extraction methods enhance product availability. Acceptance by food technologists and product developers facilitates integration into diverse formulations. Increased retail adoption and clear labeling support consumer confidence. Strategic sourcing partnerships enable stable procurement and supply reliability. Innovations in preservation and encapsulation improve flavor stability and sensory quality, reinforcing adoption across commercial and industrial applications.

Organic herb flavors are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by expanding awareness of sustainable agriculture and non-synthetic products. Growth is supported by premium positioning, regulatory incentives, and alignment with health-oriented consumption trends. Consumer trust and brand differentiation reinforce adoption in high-value markets. Product development integrates herb varieties with documented functional benefits. Enhanced traceability and certification frameworks support scalability and cross-border commercialization. Market penetration benefits from partnerships with certified organic suppliers and investment in sustainable farming infrastructure. Digital commerce and subscription models provide direct-to-consumer access, expanding commercial reach. Increased inclusion in functional foods and beverages, nutraceuticals, and personal care applications positions organic variants as a strategic growth avenue.

Form Insights

Liquid forms are likely to be the leading segment with a projected 40% of the herbs flavor market revenue share in 2026, due to versatility in application and ease of integration into food, beverage, and personal care formulations. Liquid flavors facilitate consistent dosing, homogenization, and stability in complex product matrices. Adoption in industrial-scale production enables efficient process integration and cost-effective operations. Retail and foodservice channels benefit from ready-to-use formats. Regulatory alignment and standardized testing protocols enhance reliability and market acceptance. Consumer trust in familiar, easy-to-use forms supports penetration across mass and premium segments.

Powder forms are expected to witness the fastest growth between 2026 and 2033, powered by flexibility in portion control, storage, and integration into dry mixes, supplements, and functional products. Powdered forms support digital commerce and direct-to-consumer distribution due to lightweight packaging and longer shelf stability. Consumer cultural acceptance and increasing adoption of DIY formulations in food and beverage preparation drive demand. Technological advancements in granulation, solubility, and encapsulation enhance flavor release and product quality. Expansion in nutraceutical and cosmetic applications reinforces commercial scalability. Partnerships with contract manufacturers facilitate rapid production scale-up.

Application Insights

The food & beverages segment is slated to hold a dominant position, with an anticipated 50% of the herbs flavor market share in 2026, driven by integration into snacks, beverages, and processed foods for flavor enhancement and functional benefits. Regulatory compliance, safety standards, and consistent sensory quality support widespread adoption. Supply chain integration and retail distribution ensure market accessibility. Consumer preference for natural and healthy ingredients reinforces incorporation into mainstream products. Strategic partnerships with food manufacturers enable product co-development and market alignment. Technological innovation in flavor retention, stability, and encapsulation ensures performance across diverse food matrices. Brand differentiation through authentic and traceable ingredients enhances consumer trust.

The nutraceuticals segment is forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by increased integration of herbal extracts with functional and therapeutic properties. Digital platforms facilitate personalized nutrition delivery, including powdered or liquid forms of herb-based supplements. Clinical validation and provider endorsements support adoption in health-focused consumer segments. Regulatory incentives for preventive health and functional products enhance market receptivity. Supply chain improvements and scalable extraction technologies ensure consistent product quality. Partnerships with healthcare providers and wellness platforms expand consumer engagement. The trend toward preventive and self-directed health management strengthens demand and commercial potential for nutraceutical formulations.

Regional Insights

North America Herbs Flavor Market Trends

North America is expected to dominate with an estimated 35% share of the herbs flavor market in 2026, driven by widespread adoption of herb-based flavor systems across processed foods, beverages, dietary supplements, and personal care formulations. Demand is concentrated in high-value product categories where natural flavor differentiation directly impacts purchasing decisions and brand positioning. Increasing consumer preference for clean-label and plant-derived ingredients has accelerated reformulation initiatives, encouraging manufacturers to integrate herbs for both sensory appeal and functional associations. Early adoption of advanced flavor technologies, including stabilization, encapsulation, and extraction methods, ensures consistent performance across diverse product matrices.

Structural and operational factors reinforce North America’s market leadership. Investment in flavor science, process automation, and research-driven product development enables reliable scalability and high-quality output across extended shelf-life products. Collaborative networks connecting flavor suppliers, contract manufacturers, and brand owners enhance formulation customization and accelerate market entry. Efficient supply chains, integrated cold storage, and advanced logistics reduce cost volatility and ensure consistent availability of raw herbs and flavor concentrates. Distribution through organized retail, digital grocery platforms, and foodservice channels broadens accessibility, while adoption in pharmaceutical and nutraceutical formulations for taste masking and functional benefits diversifies applications beyond traditional food use.

Europe Herbs Flavor Market Trends

The Europe market is anticipated to demonstrate steady throughout the 2026-2033 forecast period, supported by high consumer awareness of health, wellness, and clean-label products. Demand is concentrated in processed foods, beverages, dietary supplements, and premium personal care categories, where natural and plant-derived flavors support product differentiation and sensory appeal. Established food manufacturing infrastructure and advanced processing capabilities enable large-scale adoption of herb-derived flavors, ensuring consistent quality and stability across diverse product formats. Consumer preference for organic, minimally processed, and functional ingredients encourages manufacturers to integrate herb flavors into reformulated offerings, enhancing both taste and perceived health benefits. High purchasing power and trend-conscious consumers facilitate premium product positioning, stimulating innovation in flavor combinations, extraction methods, and formulation techniques.

Commercial growth is reinforced by technological advancements in extraction, encapsulation, and solvent-free processing, which improve flavor performance while maintaining compliance with clean-label and natural ingredient standards. Strong regulatory frameworks for ingredient safety, labeling, and traceability support widespread adoption by reducing compliance risk and facilitating faster product development cycles. Collaboration between flavor houses, contract manufacturers, and consumer brands enables customization tailored to sensory preferences and functional requirements. Increasing integration of herb-derived flavors in nutraceuticals and dietary supplements for taste masking and functional enhancement diversifies applications beyond conventional food and beverage categories. Expansion of organized retail, specialty stores, and digital commerce accelerates distribution efficiency, ensuring broad accessibility and market penetration.

Asia Pacific Herbs Flavor Market Trends

Asia Pacific is forecasted to be the fastest-growing market for herbs flavors between 2026 and 2033, stimulated by rapid urbanization, increasing disposable incomes, and a growing preference for natural, plant-based, and clean-label ingredients. Expansion of organized retail, modern food processing infrastructure, and e-commerce platforms accelerates access to innovative formulations, supporting broader adoption across processed foods, beverages, functional nutrition, and personal care categories. Strong culinary traditions emphasizing herbs and botanicals create high consumer receptivity, enabling rapid introduction of new flavors tailored to local taste preferences. Rising demand for ready-to-eat meals, flavored beverages, and functional snacks drives volume growth while promoting the integration of scalable, stable, and versatile herb flavor solutions.

Technological and industrial developments reinforce market momentum by improving extraction, encapsulation, and solvent-free processing, which enhance flavor stability, potency, and shelf life. Partnerships between global flavor manufacturers and local food companies enable product customization aligned with regional taste and health trends, strengthening adoption across diverse commercial applications. Regulatory clarity on natural ingredients and labeling standards reduces compliance barriers and encourages reformulation toward transparent, clean-label profiles. Expansion into dietary supplements and nutraceutical products, particularly where taste masking or functional enhancement is required, further diversifies demand beyond conventional food and beverage applications.

Competitive Landscape

The global herbs flavor market exhibits a moderately fragmented structure, with leading players collectively capturing an estimated 40% of total revenue, highlighting significant opportunities for both established companies and specialized producers. Key players such as Givaudan, McCormick & Company, Inc., Symrise, and International Flavors & Fragrances Inc. leverage strong research and development capabilities to create innovative, herb-based flavor solutions that address evolving consumer demands for clean-label, natural, and functional products. These companies maintain competitive advantage through investment in advanced extraction, encapsulation, and formulation technologies, ensuring consistency, stability, and versatility of flavors across processed foods, beverages, dietary supplements, and personal care products.

Strategic positioning within the market emphasizes sustainable sourcing, regulatory compliance, and product differentiation, enabling companies to respond effectively to environmental, health, and safety expectations. Multinational players focus on integrating herb-derived flavors into global supply chains, optimizing production scalability while maintaining high-quality standards. Collaboration with contract manufacturers, ingredient suppliers, and consumer brands accelerates product development and market penetration, supporting rapid commercialization of new flavor profiles. Companies also adopt sustainability practices such as responsible herb cultivation, ethical sourcing, and environmentally friendly processing methods to enhance brand reputation and meet regulatory requirements.

Key Industry Developments

- In November 2025, McCormick® unveiled a major redesign of its Gourmet Collection, featuring premium packaging for 72 global flavors, including Mediterranean Saffron and Saigon Cinnamon Sticks, sourced from origin regions for superior quality.

- In July 2025, Chull Wali Chai launched three new herbal tea flavors – Calm Code ChamoMint, Clarity Charge Blue Voltage, and Ageless Aura Hibiscus – featuring vibrant, quirky packaging aimed at blending wellness with bold sensory appeal.

- In May 2025, Rocket Farms introduced its new Organic Living Herbs lineup featuring rooted culinary herbs such as basil, mint, oregano, parsley, rosemary, sage, and more in recyclable packaging to extend freshness, preserve bold flavor and reduce food waste.

Companies Covered in Herbs Flavor Market

- Givaudan

- McCormick & Company, Inc.

- Symrise

- International Flavors & Fragrances Inc.

- dsm-firmenich.

- Döhler GmbH

- Takasago International Corporation

- Kerry Group plc.

Frequently Asked Questions

The global herbs flavor market is projected to reach US$ 22.4 billion in 2026.

Rising consumer preference for natural, clean-label ingredients and growing demand across food, beverage, nutraceutical, and personal care applications drive the market.

The market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Innovation in clean-label and functional products, along with expansion into beverages, nutraceuticals, and premium food applications, presents key market opportunities.

Some of the key market players include Givaudan, McCormick & Company, Inc., Symrise, and International Flavors & Fragrances Inc.