- Food Ingredients & Additives

- Malted Barley Flour Market

Malted Barley Flour Market Size, Share, and Growth Forecast, 2026 - 2033

Malted Barley Flour Market by Product Type (Diastatic Flour, Non-Diastatic Flour), Application (Bakery, Beverages, Cereals, Nutraceutical), Nature (Conventional, Organic) and Regional Analysis for 2026-2033

Malted Barley Flour Market Share and Trends Analysis

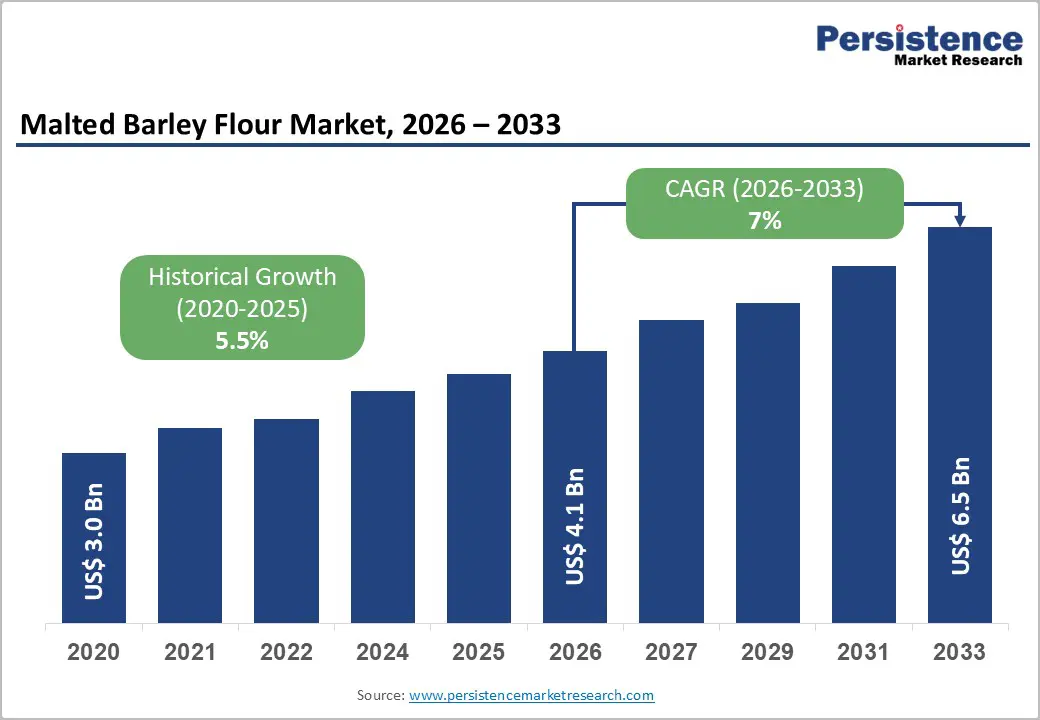

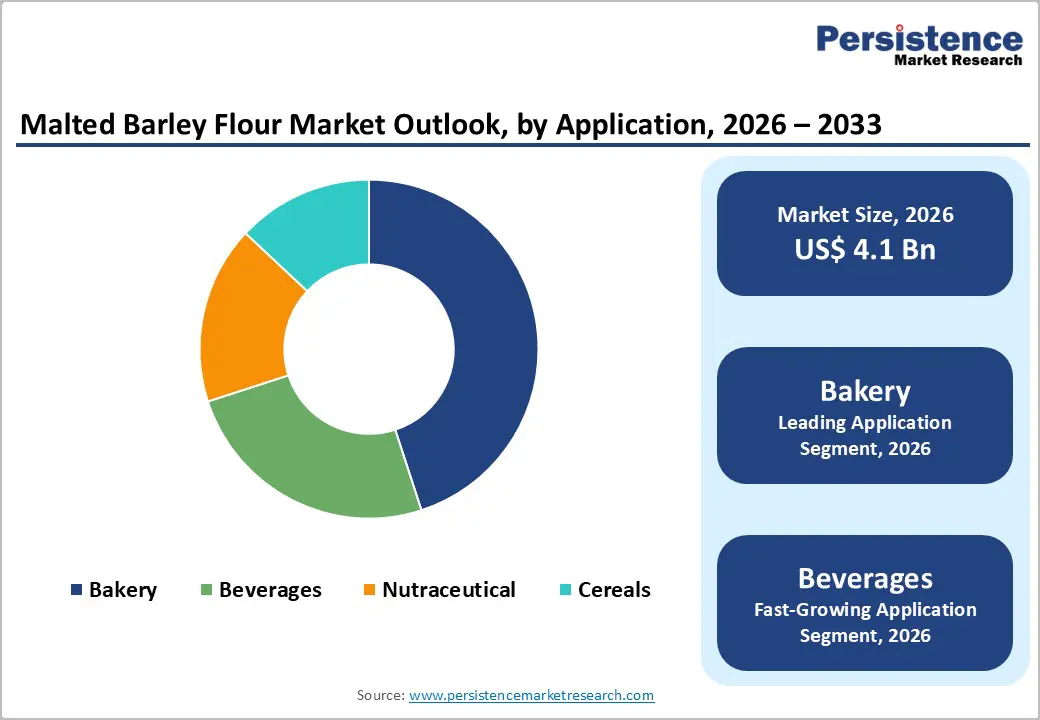

The global malted barley flour market size is likely to be valued at US$ 4.1 billion in 2026, and is projected to reach US$ 6.5 billion by 2033, growing at a CAGR of 7% during the forecast period 2026−2033. Market growth is being supported by increasing consumer preference for clean-label food products that emphasize simple ingredient lists and functional nutrition.

Malted barley flour is providing enzymatic activity that enhances dough performance, improves texture, and supports natural sweetness development without synthetic additives. Food manufacturers are incorporating this ingredient to improve fermentation efficiency and product consistency in baked goods. Rising demand for fortified and nutritionally enriched formulations is further strengthening adoption across industrial and artisanal baking segments. Growing awareness of digestive health benefits associated with enzyme-rich grain ingredients is encouraging broader use across bakery, confectionery, and selected beverage applications. Diastatic enzymes present in malted barley flour are supporting starch breakdown, which contributes to improved fermentation and potential digestive advantages. At the same time, consumer interest in organic and non-genetically modified organism (non-GMO) ingredients is expanding premium product categories. Developed markets are witnessing strong demand for certified organic malted barley flour variants, particularly within specialty bread and craft baking segments.

Key Industry Highlights

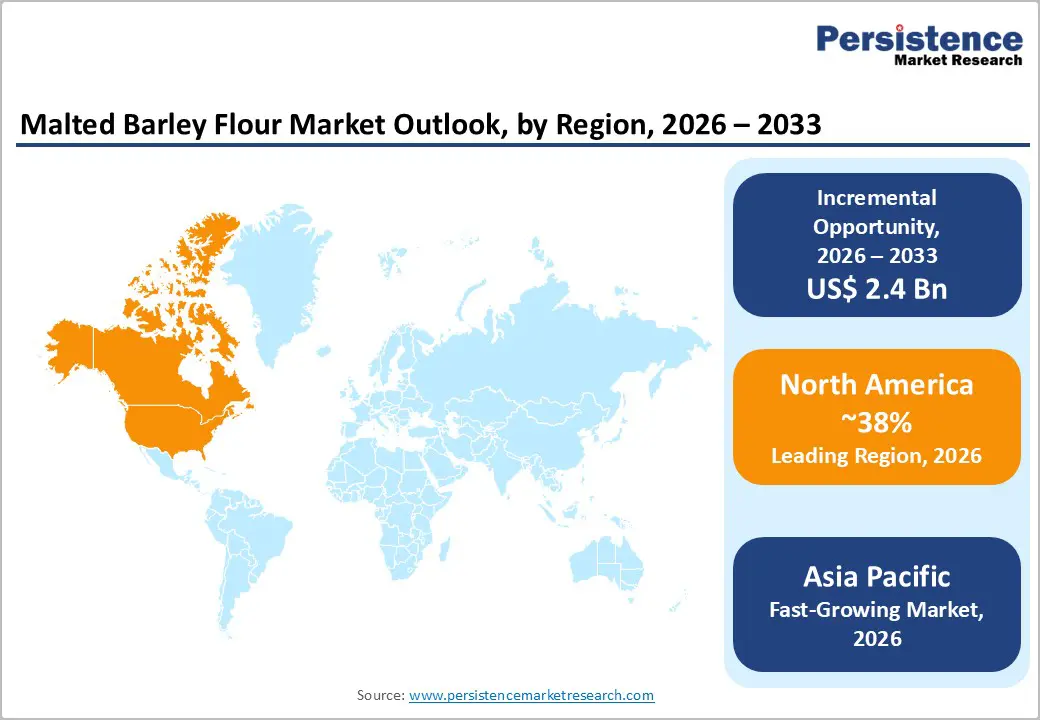

- Dominant Region: North America is expected to command about 38% of the market share in 2026, boosted by its advanced artisan bakery infrastructure and mature craft brewing sector.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing through 2033, due to the rapid westernization of dietary patterns and an expanding middle-class consumer base.

- Leading & Fastest-growing Product Type: Diastatic flour is likely to dominate with approximately 62% revenue share, whereas non-diastatic flour is slated to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing Application: Bakery is poised to lead by capturing an estimated 58% revenue share in 2026, while beverages are expected to be the fastest-growing segment over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

| Malted Barley Flour Market Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 6.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Health and Wellness Consciousness

Consumers are increasingly prioritizing functional food ingredients that provide measurable nutritional benefits. Malted barley flour is gaining attention because it contains naturally occurring enzymes such as alpha-amylase and beta-amylase, which support starch breakdown during digestion and improve dough fermentation performance. These enzymatic properties are contributing to improved digestibility and more stable glycemic responses when compared with highly refined wheat flour. As health awareness rises, food manufacturers are incorporating malted barley flour into formulations that appeal to consumers seeking natural alternatives to synthetic improvers. The Whole Grains Council reports that sustained consumer interest in products that contain malted and whole grains, particularly among buyers who associate these ingredients with enhanced nutrition and transparency.

Regulatory validation is further strengthening market positioning. The European Food Safety Authority (EFSA) has recognized beta-glucans derived from barley for their role in supporting cardiovascular health, which provides a credible scientific foundation for product claims. Manufacturers are leveraging this endorsement by integrating malted barley flour into premium bread varieties, artisanal baked goods, and breakfast cereals. This approach aligns with clean-label demand while addressing performance needs within industrial baking processes. Businesses should interpret this alignment between nutritional science, regulatory support, and consumer preference as a strategic inflection point. Reformulating mainstream portfolios with enzyme-rich and fiber-enhanced ingredients is creating opportunities to capture higher-margin segments while strengthening long-term brand credibility.

Competition from Alternative Functional Flours

The functional flour space is becoming increasingly competitive, creating pressure for malted barley flour across key application areas. Suppliers of alternative grains and specialty flours are actively promoting ancient grains, pulse-based formulations, and enzyme-enhanced wheat derivatives to address similar functional needs. Ingredients such as chickpea flour, almond flour, and quinoa flour are attracting strong consumer interest through clean-label positioning and health-focused marketing narratives. These substitutes are appealing to buyers who prioritize plant-based nutrition and perceived natural purity. As a result, malted barley flour manufacturers are encountering intensified competition in bakery products, beverage formulations, and fortified nutrition segments. To remain relevant, producers are refining value propositions and emphasizing distinctive functional performance attributes.

Competing flours benefit from established distribution networks and strong brand visibility across retail and foodservice channels. Malted barley flour suppliers are therefore differentiating through measurable technical performance, cost optimization, and application-specific customization. Demonstrating superior fermentation support, improved texture development, and enhanced flavor profiles is becoming critical for securing long-term contracts with industrial bakers. Business leaders are shifting from generalized marketing toward targeted solution development tailored to premium bread, craft brewing, and health-oriented cereal segments. By integrating data-backed performance claims with competitive pricing frameworks, suppliers are strengthening positioning while identifying portfolio gaps that require innovation investment. This disciplined approach is enabling malted barley flour producers to navigate fragmentation and sustain growth in a highly dynamic functional ingredient landscape.

Innovation in Plant-Based and Functional Food Applications

The global plant-based food sector is creating meaningful growth avenues for malted barley flour as a multifunctional ingredient. Producers are incorporating it into meat alternatives, dairy substitutes, and protein-fortified snack products to address structural and sensory formulation challenges. The natural enzymatic activity within malted barley flour is improving texture stability, enhancing flavor development, and supporting protein utilization during processing. These properties are helping manufacturers overcome common consumer concerns related to mouthfeel, aftertaste, and product consistency in plant-based formulations. As demand for clean-label and minimally processed ingredients is increasing, malted barley flour is offering a functional solution that aligns with natural positioning strategies.

Food technology firms are collaborating with malt processors to refine fermentation processes for plant-derived proteins. Enzymes present in malted barley flour are accelerating fermentation cycles and improving aroma and taste profiles, which are critical for consumer acceptance. Beyond plant-based meat and dairy, the sports nutrition segment is presenting additional opportunity. Performance supplements, recovery beverages, and high-protein bars are incorporating enzyme-rich grain ingredients to enhance digestibility and nutrient absorption. During intensive physical activity, digestive comfort and efficient nutrient delivery are becoming key product attributes. Companies that are targeting these high-growth categories are positioning themselves strategically within functional nutrition ecosystems.

Category-wise Analysis

Product Type Insights

The diastatic segment is poised to lead in 2026, holding approximately 62% of the malted barley market revenue share due to its essential function in commercial baking. This flour category contains active enzymes that convert complex starches into simple sugars, thereby improving yeast activity and fermentation efficiency. Enhanced sugar availability is supporting stronger dough rise, improved crust coloration, and increased loaf volume. Industrial bakeries are depending on these predictable enzymatic properties to maintain uniform product quality and production consistency. Artisan producers are also valuing batch reliability and controlled fermentation performance. Specialty baking facilities are optimizing throughput by leveraging improved dough handling characteristics and texture development. Demand is remaining stable across professional baking environments where precision and repeatability are central to operational success.

Non-diastatic malted barley flour is projected to be the fastest-growing segment from 2026 to 2033. In this flour type, enzymes are deactivated through high-temperature processing, leaving primarily flavor and color enhancement properties. It is widely used in products such as bagels, pretzels, and specialty breads where distinctive malt flavor and darker crust tones are desirable without active fermentation effects. Rising consumer interest in artisanal and craft bakery items is increasing demand for flavor-focused ingredients. Application expansion is also occurring in breakfast cereals, malt-flavored beverages, and confectionery formulations where enzymatic activity is not required. As premium product lines emphasize authentic taste profiles and sensory differentiation, non-diastatic malted barley flour is capturing incremental growth across diverse food categories.

Application Insights

The bakery segment is projected to account for an estimated 58% of the malted barley flour market share in 2026, making it the top application area. Manufacturers are incorporating malted barley flour into a broad range of products such as bread, rolls, bagels, pizza dough, and specialty baked items. Its enzymatic properties are improving dough elasticity, fermentation stability, and finished product consistency across both industrial and artisanal operations. Large-scale bakeries are relying on predictable performance to standardize output and maintain uniform quality benchmarks. Artisan producers are achieving enhanced crumb structure and flavor development through controlled enzymatic activity. Reduced processing time and improved shelf stability are delivering measurable operational cost benefits, reinforcing bakery dominance within the overall application landscape.

The beverages segment is expected to record the fastest growth between 2026 and 2033. Expansion in craft brewing, development of malt-based functional drinks, and innovation in non-alcoholic alternatives are driving this upward trajectory. Health-focused consumers are showing increased interest in malt-infused beverages that combine flavor complexity with perceived nutritional advantages. Plant-based milk alternatives incorporating malted barley flour for taste enhancement and nutrient fortification are emerging as a promising niche. The broader food and confectionery category, including breakfast cereals, snack bars, and malt-based dairy beverages, is also benefiting from clean-label demand and interest in minimally processed ingredients. As product developers continue diversifying applications beyond traditional baking, beverage-led innovation is expected to capture incremental market share during the forecast period.

Nature Insights

Conventional malted barley flour is likely to command around 73% of market revenues in 2026. Manufacturers are favoring conventional variants for cost-sensitive applications such as commercial baking, industrial food processing, and mainstream beverage production. Established agricultural supply chains are ensuring consistent raw material availability and stable pricing structures. These efficiencies are supporting large-scale manufacturing requirements and predictable procurement planning. High-volume buyers are prioritizing affordability and functional reliability when sourcing ingredients for mass-market food products. Conventional malted barley flour is meeting these operational demands while maintaining required enzymatic performance standards. As a result, it is continuing to anchor the bulk of volume-driven demand across industrial applications.

The organic variety of this flour is expected to register the fastest growth between 2026 and 2033. Rising awareness of health, sustainability, and traceability is increasing consumer preference for certified organic ingredients. Buyers are associating organic products with higher purity and improved nutritional integrity. Clean-label purchasing behavior is strengthening momentum within specialty bakery, health-oriented cereals, and premium beverage categories. Distribution expansion across modern retail and foodservice channels is improving accessibility. Producers are responding by expanding certified organic acreage and strengthening traceability systems. Premium pricing is supporting margin expansion while aligning with consumer expectations for transparency and responsible sourcing. This convergence of wellness demand and certification credibility is driving sustained growth in high-value organic segments.

Regional Insights

North America Malted Barley Flour Market Trends

North America is anticipated to dominate with roughly 38% of the malted barley flour market value in 2026, reflecting strong regional demand and established processing infrastructure. The United States spearheads regional market performance due to its developed artisan bakery network and mature craft brewing industry. Consumers are increasingly preferring clean-label grain ingredients in premium bread, specialty baked goods, and craft beverages. Canada is contributing through expanding organic farming capacity and rising demand for health-oriented food products. The U.S. Food and Drug Administration (FDA) is maintaining defined regulatory standards for grain-based ingredients, which are supporting product innovation and facilitating faster commercialization of new formulations. Regulatory clarity is providing confidence to manufacturers seeking to introduce enzyme-optimized or specialty malted flour variants.

Advanced milling technologies and efficient logistics systems are reinforcing regional competitiveness. High per capita consumption of premium bakery products and craft beverages is sustaining consistent ingredient demand across industrial and artisanal channels. Leading producers are investing in organic certification programs and supply chain traceability systems to capture value within higher-margin segments. Export strategies are increasingly targeting Latin America and parts of Asia where functional baking ingredients are gaining traction. Although overall market maturity is moderating volume growth, premiumization and niche applications are generating incremental expansion opportunities. Strategic emphasis on differentiated, value-added formulations is supporting continued regional leadership within the global malted barley flour market.

Europe Malted Barley Flour Market Trends

Europe holds a strong position in the global market for malted barley flour, supported by established consumption patterns and a long-standing baking tradition. Germany is leading the region due to high per capita bread consumption and a dense network of traditional bakeries that prioritize craftsmanship and fermentation quality. The United Kingdom is driving additional momentum through premium retail bakery expansion and growth in craft beverage production. France and Spain are contributing through deep-rooted artisanal baking culture and rising consumer focus on balanced nutrition. The European Union (EU) is harmonizing regulatory oversight through the Novel Foods Regulation and guidance issued by the EFSA, which is ensuring product safety and facilitating smoother cross-border trade within member states. This coordinated regulatory structure is providing operational clarity for manufacturers and supporting consistent quality benchmarks across the region.

Centuries of malting expertise are reinforcing competitive strength across European producers. Consumers are demonstrating strong appreciation for heritage grains and authentic production methods in premium food categories. Agricultural support mechanisms under the Common Agricultural Policy (CAP) are promoting organic cultivation through structured subsidies, thereby strengthening supply continuity. Manufacturers are investing in sustainability certifications, regenerative agriculture partnerships, and specialized enzyme formulations tailored for distinct baking applications. Companies are also expanding export channels to markets in the Middle East and Asia where demand for functional baking ingredients is increasing. Strategic consolidation is addressing fragmentation within local markets, while premium positioning is sustaining profitability despite varied national consumption preferences.

Asia Pacific Malted Barley Flour Market Trends

The market for malted barley flour in Asia Pacific is expected to register the fastest growth during the 2026-2033 forecast period, aided by dietary transition, urban expansion, and rising disposable incomes. China is accelerating demand as western-style bakery consumption is increasing across urban centers and middle-class households are expanding packaged food purchases. Japan is contributing through a well-developed bakery ecosystem and a premium beverage industry that values standardized malting quality. India is strengthening regional momentum through growth in organized retail bakeries, rising foreign direct investment in food processing, and public initiatives aimed at nutritional improvement. Member states of the ASEAN are demonstrating strong consumption potential as urbanization and modern retail penetration continue progressing.

Producers are leveraging cost-efficient manufacturing infrastructure and proximity to high-growth consumer bases to enhance supply responsiveness. Improvements in barley cultivation practices are increasing yield efficiency and strengthening regional raw material availability. Governments across China, India, and ASEAN markets are modernizing food safety frameworks, which are facilitating smoother entry for both imported and locally produced malted ingredients. Companies are expanding domestic production facilities while forming technical partnerships with European and North American milling specialists to enhance formulation capabilities. Distribution strategies are increasingly focusing on organized retail chains, foodservice expansion, and premium product categories where income growth is supporting ingredient upgrades. Strategic alignment with these structural growth drivers is positioning Asia Pacific for sustained long-term expansion within the malted barley flour industry.

Competitive Landscape

The global malted barley flour market structure is moderately consolidated. Major producers such as Axéréal Group, Simpsons Malt Limited, Malt Products Corporation, GrainCorp Limited, and Briess Malt & Ingredients Co. collectively accounting for approximately 40–45% of total market share in 2026. These companies are benefiting from established malting infrastructure, long-term supplier relationships, and diversified customer portfolios across bakery and beverage industries. Market structure reflects a balance between large-scale integrated operators and regional specialists serving niche applications. Scale advantages in sourcing, processing efficiency, and quality assurance systems are enabling leading firms to maintain stable supply and consistent performance standards.

Competitive intensity is remaining high as both established companies and emerging players are pursuing innovation and market expansion. Producers are investing in research and development to introduce specialized enzyme profiles and application-specific formulations that address evolving customer requirements. Portfolio diversification is targeting premium bakery, craft brewing, and health-oriented food segments. Distribution network enhancements are improving geographic coverage and supply reliability. Capacity expansions are supporting volume growth in high-demand regions, while customer-centric product customization is strengthening long-term contracts. This dynamic competitive environment is encouraging continuous operational refinement and creating opportunities for suppliers that can differentiate through technical performance, supply chain resilience, and strategic responsiveness to changing food industry trends.

Key Industry Developments

- In January 2026, Warburtons, the U.K.'s largest bakery brand, launched its Fibre Fix range a 500g seeded wholemeal loaf, featuring a blend of seeds (brown linseed, chia, sunflower, pumpkin, hemp, sesame), grains (red lentil, millet), wheat bran, and malted barley flour, plus added calcium for digestive support.

- In December 2025, Hindustan Unilever Ltd (HUL) introduced an upgraded Horlicks in Tamil Nadu and Kerala, featuring a superfoods blend of malted barley, almonds, oats, and millets enhanced by proprietary NutriMax technology to boost nutrient absorption, reduce anti-nutrients such as phytates, and support children's growth, cognitive development, immunity, and gut health while preserving the classic taste.

- In October 2025, Hovis forayed into the sourdough market with a new range of pre-sliced cob loaves that combine traditional sourdough characteristics with the convenience of sliced bread. The launch expands Hovis’s product lineup into artisanal-style offerings while aiming to meet growing consumer demand for sourdough and craft-inspired baked goods.

Companies Covered in Malted Barley Flour Market

- Malteurop Group

- Crisp Malting Group

- Axéréal Group

- Simpsons Malt

- Malt Products Corporation

- GrainCorp Malt

- Briess Malt & Ingredients

- Muntons PLC

- Viking Malt

- Imperial Malts Limited

- Bairds Malt

- Rahr Corporation

- Holland Malt

- Canada Malting Company

Frequently Asked Questions

The global malted barley flour market is projected to reach US$ 4.1 billion in 2026.

The market is driven by rising demand for clean-label bakery ingredients, craft brewing expansion, and health-conscious consumer preferences.

The market is poised to witness a CAGR of 7% from 2026 to 2033.

Plant-based food formulations, organic premium segments, and Asia Pacific manufacturing expansion present the strongest growth potential.

Axéréal Group, Simpsons Malt, Malt Products Corporation, GrainCorp Malt and Briess Malt & Ingredients are some of the key players in the market.