- Retail

- Gaming Laptop Market

Gaming Laptop Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Gaming Laptop Market by Display Resolution (Full HD, QHD, 4K, Other), Display Size (13-inch, 15-inch, 17-inch, Other), Processor (i5, i7, i11, Other), RAM (8 GB, 16GB, 32 GB, Other), and Regional Analysis for 2026 - 2033

Gaming Laptop Market Size and Trend Analysis

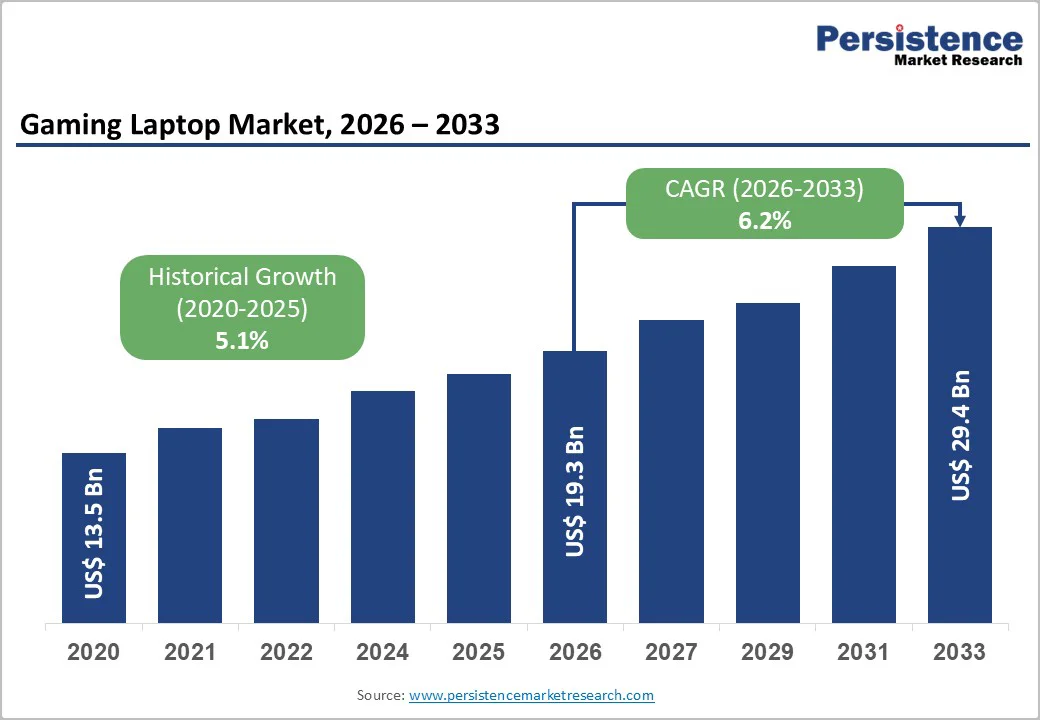

The global gaming laptop market size is likely to be valued at US$19.3 billion in 2026 and is projected to reach US$29.4 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The market expansion stems primarily from surging demand for high-performance portable gaming devices amid esports proliferation and hardware innovations. Esports viewership reached over 500 million globally in 2024, boosting the need for powerful laptops, while advancements like NVIDIA RTX 50-series GPUs enable ray tracing and higher frame rates on portable systems. The integration of artificial intelligence capabilities for performance optimization, coupled with advancements in display technologies such as OLED panels and high refresh rates (144Hz, 240Hz, 360Hz), continues to attract both casual gamers and professional streamers who demand versatile machines capable of simultaneous gaming and content creation.

Key Market highlights

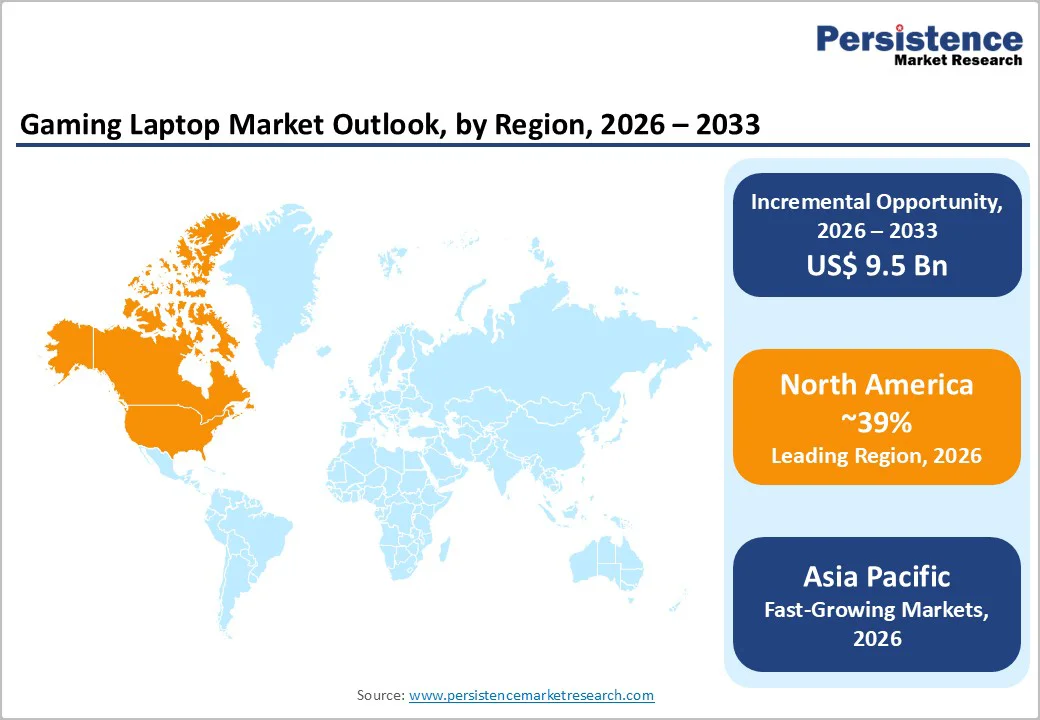

- Regional Leader: North America leads the gaming laptop market, with 39% of the global market share, due to the robust esports infrastructure and consumer spending power.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, fueled by manufacturing hubs and rising gamers in India, China.

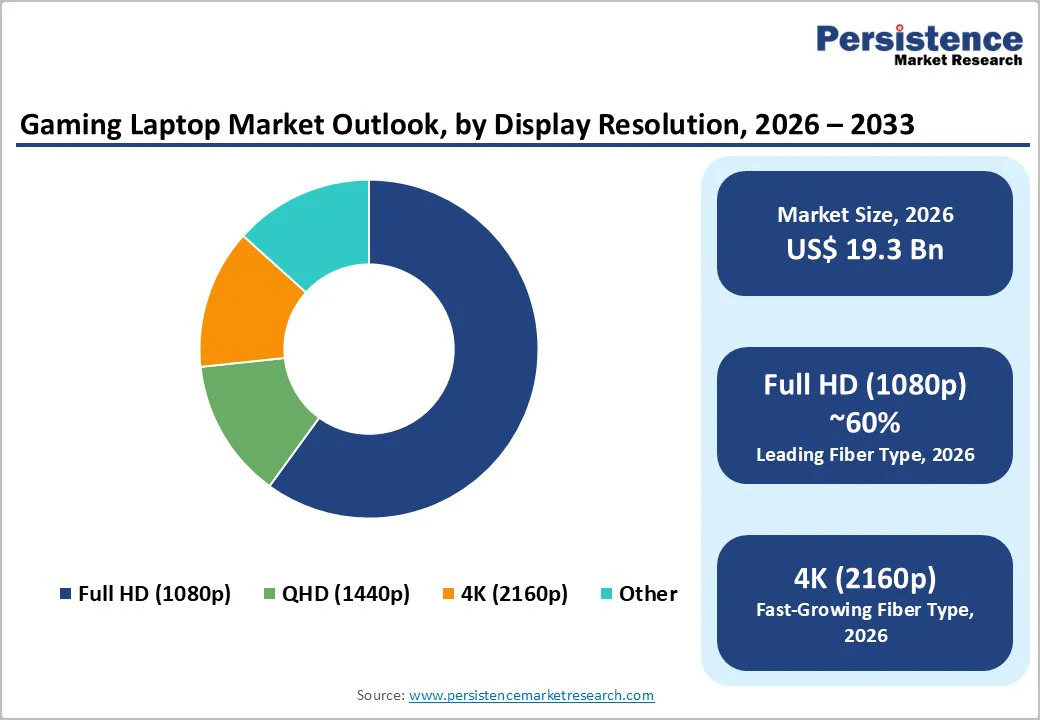

- Leading Segment: Full HD (1080p) display resolution dominates the market, with 60% of the market share, due to its optimal performance-cost balance in esports.

- Fastest Growing Segment: 32GB DDR5 RAM configurations represent the fastest-growing memory segment, driven by professional streaming and content creation demand for simultaneous multi-application workloads, including live streaming, video editing, and real-time audio processing.

- Growth Opportunities: Emerging markets offer key opportunities via affordable models and online gaming integration.

| Key Insights | Details |

|---|---|

| Gaming Laptop Market Size (2026E) | US$19.3 Bn |

| Market Value Forecast (2033F) | US$29.4 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Rising Esports and Streaming Popularity

The rapid rise of esports and live streaming has increased demand for high-performance gaming laptops among both professional and amateur gamers. These users require specialized hardware with top specifications, premium displays, and advanced cooling for competitive play and content creation. Platforms like Twitch and YouTube Gaming allow creators to monetize their gameplay, further driving the need for laptops that can handle demanding games and broadcasting software like OBS Studio seamlessly.

Global esports audience hit 640 million in 2025, up from prior years, with the international events drawing millions and requiring devices with 240Hz displays and RTX GPUs for a competitive edge. This trend integrates with the online gaming market, where seamless transitions between play and streaming demand robust cooling and battery tech, fostering market uplift.

Technological Advancements in Hardware

Innovations in processors, GPUs, and displays have made gaming laptops more capable and accessible, driving adoption among enthusiasts. Intel Core Ultra and AMD Ryzen AI series deliver AI-enhanced performance, while 165Hz OLED panels offer superior visuals without desktop bulk. NVIDIA's latest GeForce RTX laptops deliver up to 175W total performance power with capabilities for 4K gaming and ray tracing, while AMD's Ryzen 9 HX 370 processors incorporate dedicated AI accelerators for intelligent performance management and enhanced battery efficiency. The adoption of DDR5 memory, now available in 60% of premium gaming laptops, offers bandwidth advantages crucial for demanding applications. These upgrades, coupled with improved thermal management like Coldfront Hyper, enable sustained high-frame rates in AAA titles, convincing consumers of laptops' viability over PCs.

Restraints - Premium Pricing and Economic Accessibility Barriers

Elevated prices due to specialized components like discrete GPUs and high-refresh displays limit accessibility for budget gamers, particularly in emerging regions. Entry-level gaming laptops with RTX 5050 graphics are above US$1,000, while mid-range configurations with RTX 5070 GPUs have compressed pricing to approximately between US$1,800 and 2,000. This pricing structure creates accessibility challenges for casual gamers and students who represent substantial portions of the potential customer base but possess limited purchasing power.

Economic fluctuations and inflationary pressures have exacerbated these concerns, as component shortages and supply chain disruptions periodically drive prices higher, further distancing products from mainstream affordability. The rapid pace of technological obsolescence in the gaming sector compounds this challenge, as consumers increasingly delay purchases, anticipating next-generation releases or more competitive pricing.

Thermal Management and Performance Sustainability Challenges

Despite engineering advances, thermal constraints remain a key limitation for gaming laptops, affecting both performance and longevity. Their compact design creates conflicts between maximizing performance and managing heat dissipation, often leading to thermal throttling, where processors reduce clock speeds to prevent overheating. This can negatively impact the user experience during demanding applications and long gaming sessions.

Intense gaming sessions generate excessive heat and drain batteries rapidly, hindering portability. Despite cooling innovations, sustained loads often throttle performance, with battery life averaging under 2 hours for demanding titles. The push for more powerful graphics cards and processors has intensified these challenges, as manufacturers work to balance performance with thermal efficiency within limited chassis space.

Opportunity - Expansion of Content Creation and Streaming Market Segments

The explosive growth of Twitch, YouTube, and emerging platforms has created a distinct market segment of professional and semi-professional streamers requiring specialized hardware configurations. Content creators demand laptops with 32GB minimum RAM, dual-GPU configurations or high-performance mobile workstation variants, and superior audio-visual capture capabilities. Platforms enabling secondary monitor connectivity and streaming optimization present differentiation opportunities.

Rapid gaming adoption in India, Brazil, and ASEAN presents lucrative growth for manufacturers via affordable mid-range laptops. 640 million global esports fans include rising numbers from these areas, with India's player base surpassing 500 million. Manufacturers partnering with streaming platforms, gaming communities, and professional esports organizations to bundle software licenses and optimization tools can capture disproportionate share growth in this expanding segment.

Integration with Cloud Gaming and AI Features

The rise of cloud gaming infrastructure offers gaming laptop manufacturers the chance to rethink their product positioning and reach new customer segments. By shifting computational loads to remote servers, cloud gaming reduces the need for high-end local hardware, allowing laptops with moderate specifications to deliver premium streaming experiences. This shift enables the creation of more affordable gaming laptops, attracting budget-conscious consumers previously deterred by high hardware requirements.

As 5G networks expand and latency decreases, the relationship between cloud gaming and portable hardware will strengthen, making gaming laptops versatile rather than hardware-dependent. Services like GeForce Now minimize hardware needs, while AI upscaling enhances older titles. With the growing cloud gaming market, laptops featuring RTX AI cores are becoming ideal for virtual reality (VR), augmented reality (AR), and streaming. A commitment to using recyclable materials also aligns with sustainability trends and appeals to eco-conscious consumers.

Category-wise Analysis

Display Resolution Insights

Full HD (1080p) commands 60% market share in gaming laptops, favored for balancing performance and affordability in esports and streaming. According to Steam Hardware Survey data from December 2024, 1920x1080 resolution captures the largest user base, with gamers leveraging this resolution across 13-15 inch display configurations to achieve competitive advantages through higher frame rates, particularly critical in esports titles where 240+ FPS separates victory from defeat. The segment benefits from established supply chains and manufacturing maturity that enable competitive pricing, making it an accessible entry point for budget-conscious consumers and students.

While QHD (1440p) and 4K (2160p) displays offer superior visual fidelity, adoption remains concentrated among enthusiasts and professionals willing to invest in premium graphics hardware capable of driving higher resolutions without compromising frame rates. The prevalence of Full HD content across streaming platforms and gaming titles further reinforces the practical advantages of 1080p displays, as users avoid unnecessary upscaling or downscaling processes that can introduce visual artifacts.

Display Size Insights

15-inch screens hold a 55% share, ideal for portability and immersion in competitive play. This screen size has emerged as the industry standard by successfully balancing portability requirements with immersive visual experiences, making it suitable for diverse usage scenarios, including competitive gaming, content creation, and professional applications. The 15-inch form factor enables manufacturers to incorporate high-performance components, including dedicated graphics processors and robust thermal management systems, without excessive weight penalties, typically maintaining overall system weights between 2.0 kg and 2.5 kg.

While content creators, streamers, and competitive esports teams are increasingly adopting 17-inch configurations for superior 1440p and 4K gaming experiences and 13-inch variants prioritize ultra-portability, the 15-inch category's versatility and market maturity ensure continued dominance throughout the forecast period.

Processor Insights

i7 processors lead with 42% share, offering optimal multi-core power for gaming and multitasking. Intel Core i7 excels in GPU-paired loads, powering 40% of top-selling units per sales rankings. The latest Intel Core Ultra 9 275HX processors deliver 24 cores/32 threads with a base power consumption of 45W, enabling efficient thermal management while providing exceptional gaming responsiveness. Intel's architectural advantages in x86 optimization, combined with mature driver ecosystems and gaming engine integrations, continue to attract OEM manufacturers and gaming enthusiasts despite competitive pressure from AMD.

The processor family's dominance stems from architectural advantages, including high clock speeds, efficient multi-threading capabilities, and robust support for demanding gaming workloads and content creation tasks. The processor tier strikes an effective balance by delivering performance that satisfies enthusiast requirements without the premium pricing associated with flagship i9 or i11 processors, making it accessible to broader consumer segments

RAM Insights

The 16 GB RAM capacity holds a dominant 50% market share, making it a sufficient choice for modern gaming and streaming without incurring high costs. It effectively handles 4K textures and multitasking, which has become standard in mid-range to high-end models, according to Amazon trends. Many contemporary gaming titles and multitasking workflows, such as simultaneous gaming, streaming, and communication applications, have established 16 GB as the minimum viable specification for mainstream gaming experiences. Lower RAM capacities often lead to performance bottlenecks and system instability.

While 32 GB RAM configurations appeal to professional content creators and enthusiast users requiring extensive multitasking capabilities, their premium pricing limits adoption to specialized segments. The emergence of faster memory technologies, including DDR5, is enhancing 16 GB configuration performance without capacity increases, further solidifying the segment's market position and extending its relevance throughout the forecast period.

Regional Insights

North America Gaming Laptop Market Trends

North America represents the global center of gaming and esports culture, with established professional gaming infrastructure generating sustained demand for high-performance gaming laptops. The region benefits from high disposable income among target demographics, early adoption of emerging technologies, and concentration of major esports organizations headquartered in metropolitan areas, including Los Angeles, New York, and Seattle.

The U.S. market demonstrates particularly strong preferences for premium configurations featuring cutting-edge graphics processors, high-refresh-rate displays, and advanced cooling solutions, reflecting consumer willingness to invest in top-tier performance. The proliferation of gaming-focused retail channels, including specialized boutiques and online platforms, has enhanced product accessibility, while the integration of gaming laptops into educational technology initiatives at universities and colleges expands the addressable market beyond traditional gaming demographics.

Europe Gaming Laptop Market Trends

Europe represents a sophisticated gaming laptop market characterized by diverse consumer preferences across member states, strong regulatory harmonization, and increasing emphasis on sustainability. Key markets, including Germany, the U.K., France, and Spain, drive regional demand, with Germany emerging as the innovation leader due to its engineering heritage and strong technology sector.

The region's robust eSports infrastructure, including professional leagues and gaming arenas across major cities, sustains demand for performance-oriented configurations among competitive players. Distinctive market characteristics include stronger preferences for sleek industrial design aesthetics and quieter thermal solutions compared to other regions, reflecting European emphasis on sophisticated product experiences beyond raw performance specifications.

Asia Pacific Gaming Laptop Market Trends

Asia Pacific has emerged as both the fastest-growing consumer market and the dominant manufacturing hub for gaming laptops, with China, Japan, India, and ASEAN nations driving expansion. China dominates global gaming laptop production, with Guangdong Province serving as the primary industrial cluster, where Shenzhen alone houses over 70% of major manufacturers due to its mature electronics ecosystem and integrated supply chains. The region's manufacturing advantages include immediate access to critical components, including graphics processing units, display panels, and cooling systems, enabling rapid production scaling and competitive pricing.

Japan market maintains distinct characteristics reflecting premium positioning and technological sophistication, with above-average adoption of cutting-edge AI features, OLED displays, and advanced thermal management technologies. Consumer market dynamics across the Asia Pacific reveal strong growth trajectories fueled by expanding middle-class populations, increasing internet penetration, and rising popularity of mobile eSports competitions.

Competitive Landscape

The gaming laptop market exhibits moderate consolidation, with established technology giants controlling significant market shares while specialized gaming-focused brands maintain strong positioning through differentiated product portfolios. Leading manufacturers pursue multi-brand strategies to address diverse consumer segments, from budget-conscious students to professional gamers and content creators requiring premium specifications. Key strategic initiatives include expansion into emerging markets through localized manufacturing partnerships, development of hybrid cloud-gaming capable systems, and integration of sustainable materials responding to environmental consciousness.

Key Market Developments:

- September 2025: Acer Inc. introduced Predator Helios 18P AI featuring Intel Core Ultra 9 285HX processors, RTX 5090 graphics, 18-inch mini-LED 4K display with 120Hz refresh rate, and up to 192GB ECC memory, representing the flagship convergence of gaming and professional workstation capabilities targeting serious content creators and professional gamers.

- May 2025: AMD unveiled Radeon RX 9060 XT graphics cards featuring RDNA 4 architecture with FSR 4 ML-enhanced upscaling capabilities, delivering competitive 1440p gaming performance and ray tracing capabilities challenging NVIDIA's RTX 50 Series dominance.

- July 2025: Dell Technologies introduced Alienware 16 Aurora in India, featuring Intel Core Series 2 processors, RTX 50 Series GPUs, Cryo-Chamber thermal architecture with dual fans and copper heat pipes, and a 16-inch WQXGA 120Hz display, establishing Dell's commitment to emerging market expansion.

Top Companies in the Gaming Laptop Market

- ASUSTeK Computer Inc. (Taiwan): ASUS maintains market leadership through its diversified gaming laptop portfolio, including the premium ROG (Republic of Gamers) brand and mainstream TUF Gaming series, addressing segments from enthusiast gamers to budget-conscious consumers. ASUS distinguishes itself through innovative form factors including dual-screen designs and gaming tablets, combined with aggressive pricing strategies and strong distribution networks across global markets.

- Lenovo Group Ltd. (China): Lenovo leverages its position as a global PC market leader to maintain a strong gaming laptop presence through its Legion and LOQ product lines spanning premium and value segments. The company's recent LOQ series launch with RTX 50 Series graphics demonstrates a commitment to accessibility through competitive pricing and promotional incentives. Lenovo's manufacturing scale and distribution reach across 150 markets provide competitive advantages in supply chain efficiency and market penetration, while innovative designs, including dual-display systems, showcase continued product innovation.

- Dell Technologies Inc. (USA): Dell's gaming laptop business centers on the iconic Alienware brand, synonymous with premium gaming performance and distinctive industrial design. The company's reintroduction of the Area 51 branding and commitment to cutting-edge graphics and processor integration reinforce its positioning in the enthusiast market segment.

Companies Covered in Gaming Laptop Market

- ASUSTeK Computer Inc.

- Dell Technologies Inc.

- Acer Inc.

- Lenovo Group Ltd.

- Samsung Electronics Co., Ltd

- ORIGIN PC Corp.

- AORUS Pte. Ltd.

- Clevo Corporation

- EVGA Corporation

- The Hewlett-Packard Company

- Giga-byte Technology Co., Ltd.

- MSI Inc.

- Razer Inc.

Frequently Asked Questions

The global gaming laptop market is projected to reach US$27.7 Bn by 2033, growing from US$18.2 Bn in 2026 at a compound annual growth rate of 6.2% during the forecast period.

The gaming laptops market is primarily driven by the explosive growth of eSports and professional gaming ecosystems, combined with advancements in display technology, including 240Hz and 360Hz refresh rate panels and OLED integration.

Full HD (1080p) resolution maintains market dominance with approximately 60% share, driven by competitive gamer preference for maximum frame rates and system responsiveness.

North America maintains market leadership with approximately 39% of global revenue share, driven by robust eSports infrastructure, high disposable incomes, and strong gaming culture, particularly in the U.S.

Cloud gaming integration represents the most significant opportunity, enabling manufacturers to develop affordable variants that leverage remote server processing for premium experiences, potentially expanding addressable markets while creating recurring revenue through bundled subscription models.

Leading companies include ASUSTeK Computer Inc., Dell Technologies Inc., Lenovo Group Ltd., Acer Inc., The Hewlett-Packard Company, MSI, Razer Inc., Samsung Electronics Co., Ltd, and other specialized gaming hardware manufacturers.