- Media & Entertainment

- Online Gaming Market

Online Gaming Market Size, Growth, Share, Trends, and Forecast, 2025 - 2032

Online Gaming Market by Gaming Platform (Mobile Games, PC Games, Console Games, Others), Revenue Model (Free-To-Play (F2P), Pay-To-Play/Premium, Others), Gaming Type (First-Person Shooter Game (FPS), Others), and Regional Analysis for 2025 - 2032

Online Gaming Market Share and Trends Analysis

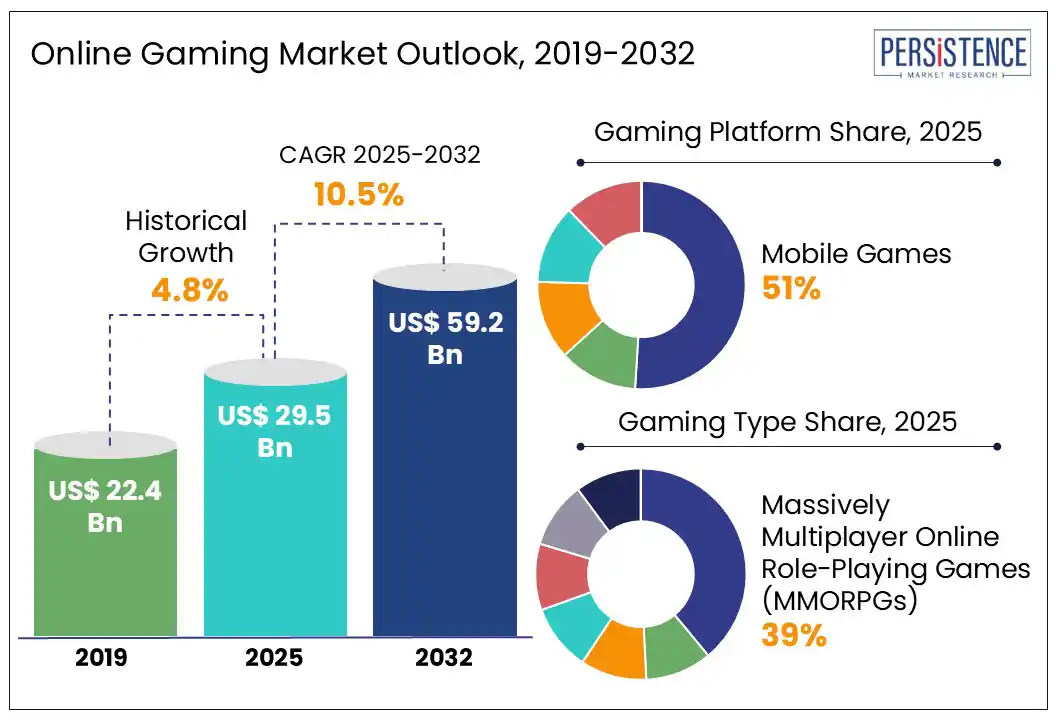

The global online gaming market size is likely to be valued at US$ 29.5 Bn in 2025 and is estimated to reach US$ 59.2 Bn in 2032, growing at a CAGR of 10.5% during the forecast period 2025 - 2032.

Online gaming refers to the act of playing video games over the internet, either with or against other players. The ability to connect players across different locations, anytime and anywhere with an internet connection, provides a highly interactive and immersive experience. They can be played on numerous devices including dedicated video games consoles such as PlayStations, Xboxes, and Nintendo Switches, and PCs, laptops and mobile phones.

The online gaming market growth is driven by increasing internet and smartphone penetration, technological advancements and awareness, higher disposable incomes, rising popularity of multiplayer and mobile games, and growth of esports and streaming.

Online gaming has opened up new opportunities for revenue generation and player engagement with Pokemon Go released in 2016, which showcased the immense potential of mobile and AR gaming. The rise of esports turned competitive gaming into a professional industry, with titles including League of Legends and Call of Duty leading. Twitch transformed live streaming and game watching into mainstream entertainment.

Key Industry Highlights

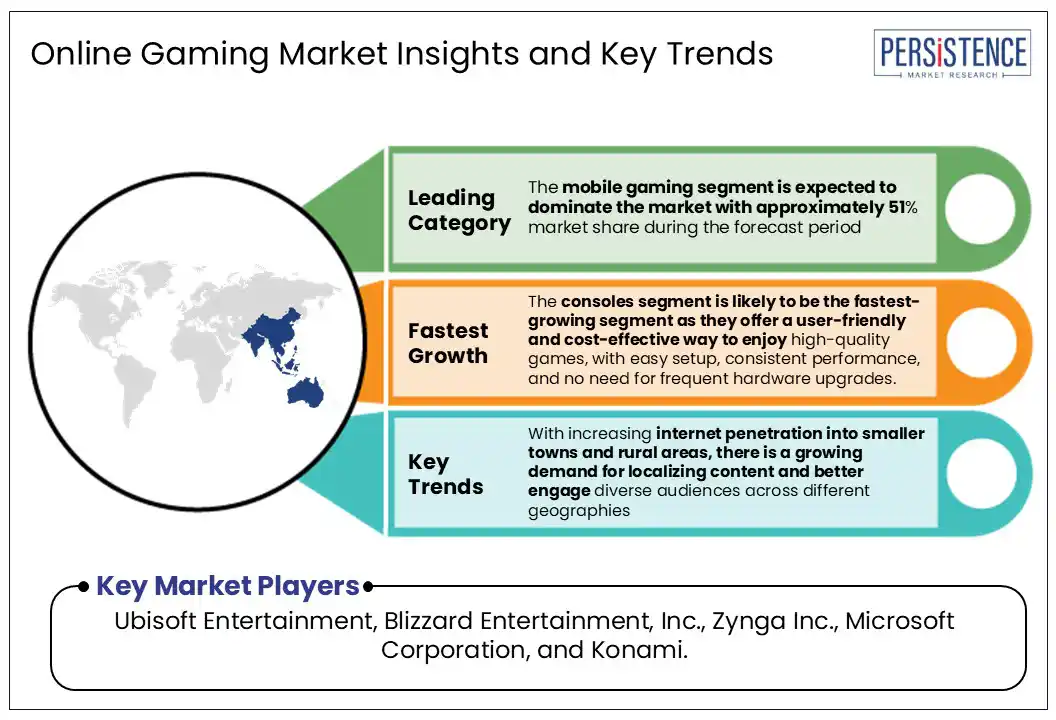

- The mobile gaming segment is expected to dominate the market with approximately 51% market share during the forecast period.

- By game type, the Massively Multiplayer Online Role-Playing Games (MMORPGs) segment is expected to dominate the market in 2025.

- Market growth is driven by increasing internet and smartphone penetration, technological advancements and awareness, higher disposable incomes, rising popularity of multiplayer and mobile games, growth of esports, and streaming.

- The consoles segment is likely to be the fastest-growing segment as they offer a user-friendly and cost-effective way to enjoy high-quality games, with easy setup, consistent performance, without frequent hardware upgrades.

- Asia Pacific is likely to dominate the market, accounting for a market share of 55% over the forecast period.

- With increasing internet penetration into smaller towns and rural areas, there is a growing demand for localizing content and for better engagement with diverse audiences across different geographies.

- China is likely to be the fastest-growing within Asia Pacific over the forecast period.

|

Global Market Attribute |

Key Insights |

|

Online Gaming Market Size (2025E) |

US$ 29.5 Bn |

|

Market Value Forecast (2032F) |

US$ 59.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

10.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Dynamics

Driver - Increasing Mobile Accessibility and Internet Adoption

The high adoption of smartphones has augmented mobile gaming. Mobile gaming accounts for over 50% of the gaming market revenue, with global smartphone users reaching about 6.8 billion in 2024, covering roughly 85% of the world’s population. The rapid growth of affordable smartphones with brands such as Xiaomi, Realme, and IQOO (a Vivo sub-brand targeting gamers with high refresh rates, fast charging, and gaming modes), along with the expansion of high-speed internet networks such as 4G and 5G, has made online gaming highly popular. By 2024, 5G connections surpassed 2.5 billion, with mobile gaming traffic on 5G networks growing three times faster than on 4G.

The migration of popular PC and console titles such as League of Legends (LoL Wild Rift), Call of Duty Mobile, Diablo Immortal, PUBG, Minecraft, FIFA, and Fortnite to mobile platforms has attracted diverse gaming audiences. Cloud gaming platforms such as Xbox Cloud Gaming, and NVIDIA GeForce Now reduce hardware barriers by streaming games over fast internet connections. Localized content and monetization models tailored to regional audiences (Tencent’s Arabic version of PUBG Mobile catering to Middle Eastern gamers) are driving growth. Partnerships between game developers and telecom operators offering bundled gaming subscriptions or zero-rated data plans are boosting gaming in emerging markets including India, Southeast Asia, and Africa. Brands such as Xiaomi’s Black Shark provide dedicated gaming phones.

Restraint - Cybersecurity and Data Privacy Issues

Online gaming offers entertainment and promotes social connection, but also makes players, especially young individuals, vulnerable to cyber-attacks and personal safety risks. Gamers can unknowingly download malware, spyware, or phishing links when accessing games or cheat codes from untrusted sources. Identity theft and account takeovers are common, especially when players reuse passwords or share sensitive information through in-game chats. Serious threats include doxing (publishing private information) and swatting (triggering emergency responses to a player’s home). Kaspersky's report reveals over 19 million malicious attempts targeting Gen Z through GTA and Minecraft.

Cyberbullying and online grooming pose immense dangers, particularly for younger players. Technical threats such as cross-site scripting, large-scale data breaches (the Zynga hack affecting over 200 million accounts), and distributed denial-of-service (DDoS) attacks such as those that disrupted Blizzard Entertainment’s tournaments in 2020 and again in April 2025, highlight the dangers in online gaming infrastructure. Call of Duty has been used to spread spyware under the guise of cheats. Features such as loot boxes and skin betting have raised concerns about encouraging gambling-like behavior.

Opportunity - Innovative Uses and Advanced Applications

Online gaming has evolved with user-generated content on platforms such as Roblox and Minecraft, and Dreams, empowering players to create, share, and monetize their own games and experiences, making gaming more participatory. Through M&A, many major players are acquiring mobile studios and integrating advanced technologies such as facial recognition and in-game advertising. Cloud gaming and cross-platform ecosystems are eliminating hardware barriers, while localized content, hybrid monetization models (battle-pass lite and rewarded ads), and affordable 5G smartphones are witnessing high growth in emerging markets such as Southeast Asia and the Middle East. Gaming is at the threshold of metaverse development, presenting virtual events and social experiences. Gaming has also started exploring blockchain-based play-to-earn models, offering possibilities for player rewards and digital ownership.

The rise of esports leagues and gaming influencers is fueling revenue streams through brand endorsements, live streaming, and large-scale digital tournaments. At the same time, Augmented Reality (AR) and Virtual Reality (VR) technologies are becoming more accessible, enabling developers to offer interactive gameplay experiences, particularly in mobile gaming. Although still evolving, blockchain-based games such as Axie Infinity and Gods Unchained familiarized play-to-earn models and digital asset ownership, indicating a shift in how games may integrate virtual economies. Games such as Beat Saber, Half-Life: Alyx, and Pokémon GO have become game-changers.

Category-wise Analysis

Gaming Platform Insights

By gaming platform, the mobile gaming segment is expected to dominate the market with approximately 51% market share during the forecast period. Unlike consoles or PCs, smartphones are widely available across all income groups and geographies, allowing anyone with a mobile device and internet connection to play games anytime and anywhere. Casual game formats, free-to-play models, and social features (multiplayer and chat) further boost its mass appeal. Modern smartphones offer high refresh rates, advanced GPUs, and vapor cooling systems. Devices such as ASUS ROG Phone 8, Xiaomi Black Shark, and iQOO Neo series are built specifically for gamers. Xbox Cloud Gaming and NVIDIA GeForce Now enable console-quality experiences on mobiles.

The consoles segment is likely to be the fastest-growing segment over the forecast period. Gaming consoles offer easy setup and consistent performance sans frequent hardware upgrades, supporting seamless multiplayer experiences, both online and offline. Consoles also double as entertainment hubs, allowing users to stream movies, music, and more from a single device. Wireless controllers, motion-based gameplay, and features including parental controls, consoles provide an accessible and immersive gaming experience for players. Microsoft & ASUS introduced the ROG Xbox Ally series, a Windows 11-powered handheld blending Xbox, Steam, and Epic libraries in a sleek console-like form factor, transitioning toward platform-centric gaming. Valve’s Steam Deck (including OLED updates) enables handheld PC gaming, enabling streaming of AAA titles at 1440p/60fps.

Gamer Type Insights

By game type, the Massively Multiplayer Online Role-Playing Games (MMORPGs) segment is expected to dominate the market in 2025, accounting for around 39% of the market share. These games are popular for their immersive worlds, strong social communities, and long-term player engagement. Popular titles include World of Warcraft, Final Fantasy XIV, Black Desert Online, Guild Wars 2, The Elder Scrolls Online, Old School RuneScape, and Lost Ark. They are highly popular as they always receive continuous content updates, expansive storylines, and the ability to form social bonds through guilds, raids, and PvP modes. These are free-to-play models, but monetized through microtransactions, and localized for pricing. Key players include Blizzard Entertainment, Square Enix, NCSoft, Nexon, Pearl Abyss, and ZeniMax Online.

The Multiplayer Online Battle Arena (MOBA) games segment is projected to be the fastest-growing. MOBA games are known for their fast-paced and team-based gameplay that blends strategy, action, and real-time coordination. Major titles in this genre include League of Legends (LoL) by Riot Games, Dota 2 by Valve, Mobile Legends: Bang (MLBB) by Moonton, Arena of Valor by Tencent, Smite by Hi-Rez Studios, and Heroes of the Storm by Blizzard. They are popular due to their competitive nature, global esports appeal, and free-to-play models supported by in-game purchases. Their compatibility with PCs and mobile platforms (MLBB and Arena of Valor) has helped hold ground in regions including Southeast Asia, China, and Latin America.

Regional Insights

Asia Pacific Online Gaming Market Trends

Asia Pacific is likely to dominate the market, accounting for a market share of 55% in 2025. China, India, South Korea, and Japan have a robust gaming base. High smartphone penetration and expanding 4G and 5G networks have made mobile gaming popular and accessible. The region’s popular online games include Mobile Legends: Bang, PUBG Mobile, Genshin Impact, Honor of Kings, League of Legends, and Dota 2. The International (Dota 2) held annually features top teams worldwide, with many from Asia-Pacific regions including China, Southeast Asia, and India. Regulations in the Asia Pacific online gaming market vary by country but generally focus on content control and player protection. India focuses on data privacy, age verification, and taking down illegal gambling and unlicensed games.

China is likely to be the fastest-growing within Asia Pacific over the forecast period. Key trends shaping the market include the expansion of cloud gaming, fueled by widespread 5G adoption, which enables high-quality game streaming without any high-end hardware. Major companies including Tencent and NetEase are heavily investing in this infrastructure. Esports continues to be a mainstream attraction in China, with millions of viewers, substantial investments, and government-backed esports arena construction. Regulatory measures by the government focus on managing gaming content and screen time, especially for minors, aiming to promote healthier gaming habits and cultural alignment.

North America Online Gaming Market Trends

North America is likely to witness significant growth. The widespread smartphone adoption and 5G connectivity and the rise of cloud gaming services that allow high-quality streaming without high-end hardware are major drivers. Microsoft’s acquisition of Activision Blizzard highlights the strategic initiatives undertaken to expand the market. There are guidelines to ensure player safety and fair play, with organizations such as the ESRB providing game ratings. Popular games in the region include Fortnite, Call of Duty, and Apex Legends. The esports scene is thriving, with major tournaments such as the Fortnite World Cup, Call of Duty League, and League of Legends Championship Series. Key players in the market include Microsoft, Sony, Epic Games, and Activision Blizzard.

The U.S. is likely to be the fastest-growing country in North America over the forecast period. Its large gamer base, high disposable incomes, advanced digital infrastructure, thriving esports ecosystem, and numerous leading game developers and publishers headquartered in the U.S. make it strong. Regulatory frameworks in the U.S. are relatively favorable for innovation, and is primarily focused on data privacy (Children’s Online Privacy Protection Act - COPPA) and consumer protection, rather than stringent restrictions on game content or monetization models.

Europe Online Gaming Market Trends

Europe is likely to experience steady growth over the forecast period. This moderate expansion is influenced by stringent regulations, a preference for traditional gaming experiences, and focus on data privacy and consumer protection. The EU’s Digital Markets Act (DMA) promotes fair competition and consumer choice by regulating "gatekeepers" including Apple and Google, impacting app distribution and in-app purchases. Ubisoft, CD Projekt, Electronic Arts, Activision Blizzard, and Epic Games lead the market. The General Data Protection Regulation (GDPR) enforces strict standards on how player data is collected, stored, and processed, with heavy fines for non-compliance.

The UK online gaming market is likely to witness significant growth as physical game sales continue to shrink, and digital downloads, in-game purchases, and subscriptions are highly popular. Streaming platforms and esports events are booming around titles such as FIFA, Call of Duty, and Fortnite. The UK’s Online Safety Act and Digital Market reforms require games to implement stronger consumer protections, age verification, clear subscription interfaces, and guard against dark patterns and loot-box mechanics.

Competitive Landscape

The global online gaming market is highly competitive and is dominated by giants such as Tencent, Sony, Microsoft (with Activision Blizzard), Nintendo, EA, and Ubisoft, who collectively hold 40-60% of revenues leveraging console, mobile, cloud, and live-service ecosystems. Companies are investing in R&D and adopting growth strategies such as product innovations, strategic partnerships, and acquisitions.

Key Industry Developments

- In June 2025, Epic Games launched Squid Game-themed cosmetics and a Reload map into Unreal Editor for Fortnite and Fortnite Creative, empowering creators to design and customize their own unique versions of this globally popular franchise’s immersive environment.

- In June 2025, RubyPlay partnered with BetMGM to expand its footprint in New Jersey, bringing a diverse portfolio of games, including Gummy Giga Match, Diamond Explosion Patriots, Mad Hit Wild Alice, Go High Panda, and Immortal Ways Sweet Coin, live on BetMGM’s online casino platform.

Companies Covered in Online Gaming Market

- Ubisoft Entertainment

- Blizzard Entertainment, Inc.

- Zynga Inc.

- Microsoft Corporation

- Konami

- Sega

- Sony Corp.

- Tencent

- Wargaming Airy Technology

- Electronic Arts

Frequently Asked Questions

The global market is projected to be valued at US$ 29.5 Bn in 2025.

Market growth is driven by increasing internet and smartphone penetration, technological advancements and awareness, higher disposable incomes, rising popularity of multiplayer and mobile games, growth of esports and streaming.

The market is poised to witness a CAGR of 10.5% from 2025 to 2032.

With increasing internet penetration into smaller towns and rural areas, there is a growing demand for localizing content and for better engagement with diverse audiences across different geographies.

Major players in the Global Online Gaming Market include Ubisoft Entertainment, Blizzard Entertainment, Inc., Zynga Inc., Microsoft Corporation, and Konami.