- Sporting Goods & Equipment

- Gaming Accessories Market

Gaming Accessories Market Size, Share, and Growth Forecast 2026 - 2033

Gaming Accessories Market by Product Type (Headsets, Controllers, Keyboards, Mouse, Gaming Chairs, VR Accessories, Others), Platform (PC Gaming, Console Gaming, Mobile Gaming), by Connectivity (Wired, Wireless), Distribution Channel (Online Retail, Specialty Stores, Supermarkets/Hypermarkets, Others), and Regional Analysis, 2026 - 2033

Gaming Accessories Market Size and Trend Analysis

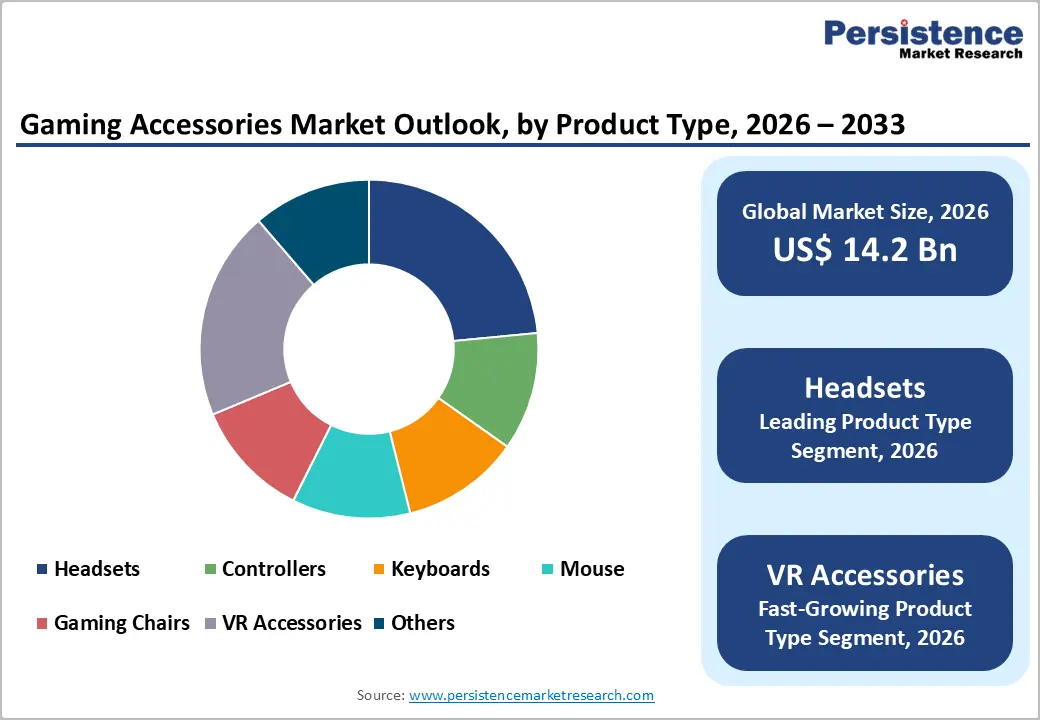

The global gaming accessories market is expected to be valued at US$ 14.2 billion in 2026 and projected to reach US$ 26.1 billion by 2033, expanding at a CAGR of 9.1% between 2026 and 2033.

Growth is propelled by the structural expansion of the global gamer base and the professionalization of competitive play. According to the Entertainment Software Association (ESA), over 190 million Americans play video games, while the International Olympic Committee has formally recognized esports through the inaugural Olympic Esports Games in 2027. Rising disposable income and rapid cloud and mobile gaming penetration from Microsoft, Sony, and Tencent are sustaining strong peripheral upgrade cycles.

Key Industry Highlights:

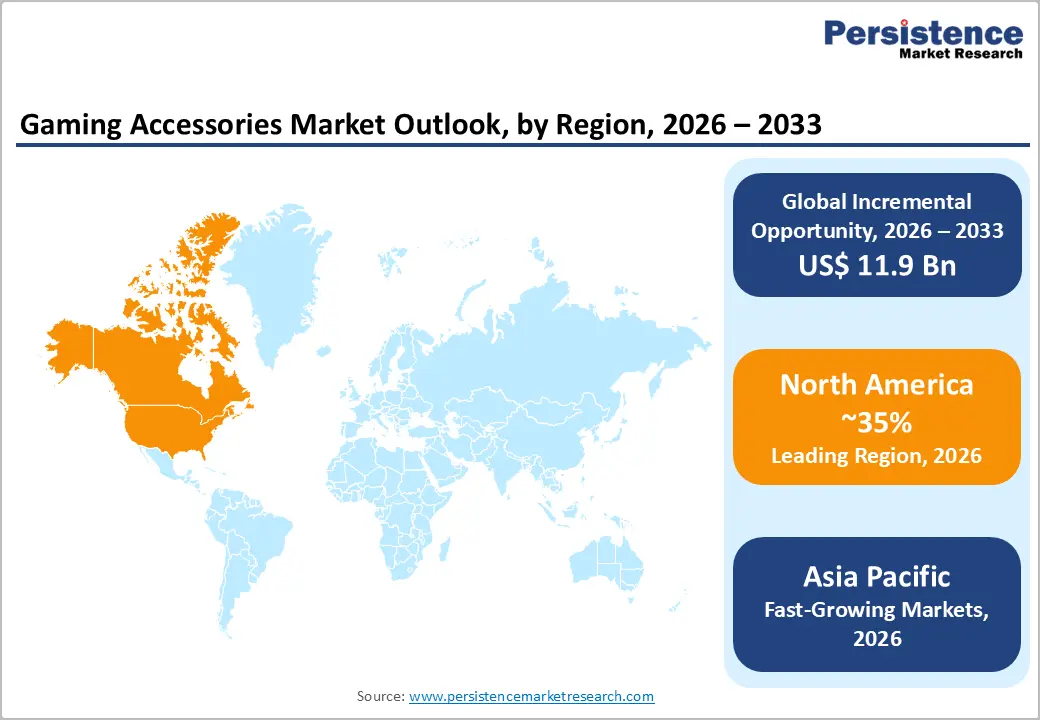

- Leading Region: North America dominates the gaming accessories market with approximately 35% share in 2025, anchored by mature esports infrastructure, high consumer purchasing power, and strong console and PC household penetration.

- Fast-growing Market: Asia Pacific is poised as the fast-growing market driven by mobile-first gaming, rising disposable incomes, and government-backed esports initiatives in China, India, and Southeast Asia.

- Dominant Segment: Headsets lead the product type category with around 28% market share in 2025, fueled by multiplayer voice-chat dependency, content-creator demand, and rapid wireless adoption.

- Fastest Growing Segment: VR Accessories is the fastest-growing product sub-category, supported by next-generation hardware launches from Meta, Sony, and Apple and rising enterprise and consumer mixed-reality use cases.

- Key Opportunity: Sustainable, modular, and right-to-repair compliant peripherals represent a high-value opportunity, particularly across Europe and North America, where regulatory and ESG-led purchasing is accelerating.

Market Dynamics

Drivers - Rising Esports Participation and Prize Pools Are Boosting Premium Peripheral Demand

The maturation of esports into a mainstream entertainment vertical is the single largest tailwind for the gaming accessories category. Tournaments organized by ESL FACEIT Group, Riot Games, and Valve distributed cumulative prize pools exceeding US$ 480 million in 2024, with The International 2024 alone awarding nearly US$ 2.6 million to its winning Dota 2 team. Aspiring competitors are upgrading peripherals to match professional standards.

The professionalization trend extends well beyond elite athletes into amateur and collegiate tiers. With the Asian Games having included esports as a medal event in Hangzhou 2022 featuring eight game titles, and the International Olympic Committee confirming the Olympic Esports Games 2027, structured competitive pathways now exist that directly translate into purchases of low-latency mechanical keyboards, high-DPI sensors, and Hi-Res Audio certified headsets at every skill tier.

Expanding Mobile Gaming Ecosystem Is Driving Accessory Innovation Globally

Mobile gaming has emerged as the largest gaming sub-segment globally, with consumers collectively spending over 4.4 billion hours per week on mobile titles according to industry usage benchmarks tracked by major app distribution platforms. This shift has created an entirely new accessory sub-category. Companies such as Razer, GameSir, and Backbone have launched dedicated mobile-first ranges including controller grips, cooling fans, capacitive triggers, and Bluetooth gamepads.

Demand is reinforced by blockbuster titles such as PUBG Mobile, Genshin Impact, and Call of Duty: Mobile, which collectively command hundreds of millions of monthly active users. The proliferation of cloud gaming services including Xbox Cloud Gaming, NVIDIA GeForce NOW, and PlayStation Plus Premium further amplifies demand for cross-platform peripherals that bridge mobile, PC, and console environments seamlessly within a single user setup.

Restraints - Counterfeit Products and Price Sensitivity Are Eroding Brand Revenue

The proliferation of counterfeit and low-quality imitation accessories on cross-border e-commerce platforms is eroding brand equity and consumer trust across multiple regions. The U.S. Customs and Border Protection (CBP) reported seizing more than 23 million counterfeit consumer-electronics items in fiscal year 2023, with gaming peripherals among the top intercepted categories alongside audio devices and charging accessories sold under spoofed branding.

In price-sensitive markets across Southeast Asia, Latin America, and Africa, unbranded substitutes priced 40-60% below branded equivalents capture significant volume share, suppressing realized revenue for established manufacturers. This dynamic complicates warranty and support frameworks, distorts authorized-dealer pricing, and forces premium brands like Logitech and Razer to invest disproportionately in anti-counterfeit holograms, serial-tracking, and direct-to-consumer authentication portals to safeguard channel margins.

Semiconductor Shortages and Logistics Volatility Are Compressing Manufacturer Margins

The gaming accessories industry remains structurally vulnerable to upstream semiconductor cycles and global logistics disruptions. The U.S. Department of Commerce highlighted persistent shortages of microcontrollers and wireless chipsets through 2023-2024, while shipping disruptions in the Red Sea during 2024 lengthened lead times for Asia-to-Europe routes by an average of 10-14 days according to the International Chamber of Shipping.

These bottlenecks raise input costs for manufacturers of wireless headsets, RGB-lit keyboards, and haptic controllers, compressing margins across the value chain. Component scarcity occasionally forces product launch delays during critical seasonal windows such as Black Friday and the year-end holiday season, when up to 35% of annual peripheral revenue is generated, leaving brands exposed to lost momentum and discount-driven inventory clearance.

Opportunities - Virtual and Mixed Reality Accessories Represent the Fastest-Growing Opportunity

The fastest-growing opportunity lies in VR accessories, where next-generation headset launches are reshaping peripheral demand patterns globally. Meta reported that its Quest platform crossed US$ 1 billion in content and accessory sales by 2024, while Apple Vision Pro and Sony PlayStation VR2 have established a premium-tier market for haptic gloves, eye-tracking modules, body trackers, and specialized facial interfaces purchased separately.

Accessory makers, including Logitech, HTC, and bHaptics, have launched VR-specific stylus pens, full-body haptic suits, and wireless streaming adapters, positioning the category as a high-margin innovation frontier. With AR/VR headset shipments rebounding strongly through 2024 and enterprise training, fitness, and social-VR use cases scaling rapidly, the segment is structurally positioned to outpace the broader peripheral market through 2033 by a wide margin.

Sustainable and Modular Hardware Is Unlocking Premium Consumer Segments

Environmental, social, and governance (ESG) considerations are creating a parallel opportunity in sustainable peripherals across mature markets. The European Commission's Right to Repair Directive, adopted in 2024, mandates extended product lifespans and easy replaceability of parts for consumer electronics sold in the EU, fundamentally reshaping product design priorities for accessory manufacturers serving the 27-member bloc.

Logitech has introduced certified carbon-neutral mice and keyboards using post-consumer recycled plastics, while Razer's "Go Green with Razer" initiative targets 100% recycled or recyclable packaging by 2030. Modular keyboards with hot-swappable switches, replaceable headset ear pads, and user-serviceable batteries on wireless controllers are unlocking a premium consumer segment willing to pay 15-25% more, particularly across Western Europe and North America.

Category-wise Analysis

Product Type Insights

Headsets lead the gaming accessories market with an estimated share of approximately 28% in 2025. Rising consumption of multiplayer titles such as Fortnite, Valorant, and Apex Legends, where voice communication is integral to gameplay. Brands such as SteelSeries, HyperX, Astro Gaming, and Sony have introduced wireless, low-latency models with active noise cancellation and THX Spatial Audio, while Discord-certified voice chat clarity is becoming a standard purchase consideration.

VR Accessories is the fastest-growing product sub-category, propelled by next-generation headset launches and an expanding mixed-reality content library. Meta Quest, Apple Vision Pro, and Sony PlayStation VR2 have established a premium tier where haptic gloves, eye-tracking modules, body trackers, and specialized facial interfaces are sold separately from the core hardware. Accessory makers, including Logitech, HTC, and bHaptics, are launching VR-specific stylus pens, full-body suits, and wireless streaming adapters.

Platform Insights

PC Gaming is the leading segment in the platform category, accounting for an estimated 44% market share in 2025. The Steam platform, owned by Valve, recorded over 132 million monthly active users in 2024, with concurrent player records repeatedly crossing 38 million users. PC gaming supports the broadest peripheral compatibility, including mechanical keyboards, vertical mice, ultrawide-monitor compatible chairs, and stream decks within a single setup, encouraging frequent enthusiast-driven upgrades.

Mobile Gaming is the fastest-growing platform segment, supported by global smartphone penetration and blockbuster franchises like PUBG Mobile, Genshin Impact, and Call of Duty: Mobile. The category is unlocking entirely new accessory formats, including controller grips, capacitive trigger buttons, cooling fans, and Bluetooth gamepads from Razer, GameSir, and Backbone. Cloud gaming services such as Xbox Cloud Gaming and NVIDIA GeForce NOW further accelerate demand for mobile-compatible peripherals.

Connectivity Insights

Wired connectivity historically dominated competitive gaming setups but has been overtaken in unit terms, with Wireless now holding around 58% of market share in 2025. The advancement of low-latency protocols such as Bluetooth LE Audio, Wi-Fi 6E, and proprietary systems including Razer HyperSpeed and Logitech LIGHTSPEED has effectively eliminated the historical latency disadvantage versus wired peripherals, while graphene-coated cells now deliver over 100 hours of continuous flagship use.

Wireless is also the fastest-growing sub-segment, reinforced by the proliferation of clean-desk aesthetics popularized by setup-influencer communities on Instagram, TikTok, and YouTube. Demand is further amplified by growing sales of mobile and hybrid devices, including the Steam Deck, Nintendo Switch 2, and ASUS ROG Ally, where cable-free configurations are not merely preferred but functionally essential, sustaining a structural shift toward Bluetooth and dongle-based peripherals.

Distribution Channel Insights

Online Retail dominates the distribution channel category with approximately 52% market share in 2025. Marketplaces operated by Amazon, Best Buy, Newegg, Flipkart, and JD.com offer extensive SKU breadth, transparent peer reviews, and aggressive holiday discounting that physical formats struggle to match. The U.S. Census Bureau reported that the e-commerce share of total retail trade reached 16.1% in Q4 2024, with electronics consistently ranking among the top-performing categories.

Online retail is also the fastest-growing distribution channel, propelled by direct-to-consumer storefronts from Logitech G, Razer, Corsair, and HyperX that offer exclusive colorways, configurator tools, and bundled software ecosystems. Same-day and next-day delivery infrastructure in major metros has eroded the immediacy advantage previously held by specialty stores, while live-shopping formats on TikTok Shop and Amazon Live are unlocking impulse purchases for accessories priced under US$ 100.

Regional Insights

North America Gaming Accessories Market Trends and Insights

North America is the leading regional market with an estimated 35% share in 2025, supported by high household penetration of consoles and PCs, mature esports infrastructure, and substantial creator-economy spending. Regional trends include strong adoption of premium wireless ecosystems, the rise of streaming-focused peripherals, and an expanding aftermarket for ergonomic gaming furniture. The presence of major publishers, including Microsoft, Activision Blizzard, and Electronic Arts anchors a robust developer-peripheral feedback loop.

- U.S. Gaming Accessories Market Size

The United States accounts for nearly 84% of the North American gaming accessories market in 2025. According to the U.S. Bureau of Labor Statistics Consumer Expenditure Survey, average annual household spending on entertainment electronics has steadily risen, while the NPD Group / Circana confirmed gaming hardware revenue surpassed US$ 6 billion in 2024. Strong franchise releases such as Call of Duty and Madden NFL keep replacement cycles short, particularly across controllers and headsets.

Europe Gaming Accessories Market Trends and Insights

Europe holds the second-largest position globally, propelled by a deep esports culture in countries like Germany, Sweden, and Poland. The Interactive Software Federation of Europe (ISFE) reports more than 125 million European players. Trends include accelerating wireless and ergonomic adoption, sustainability-led purchasing reinforced by EU Ecodesign rules, and rising demand for localized language support across keyboards and controllers.

- Germany Gaming Accessories Market Size

Germany is the largest national market in Europe, contributing nearly 22% of the regional total in 2025. According to game Verband der deutschen Games-Branche, the German games industry generated revenue exceeding €10.6 billion in 2024, with hardware and peripherals representing a sizeable share. Strong PC gaming culture, robust LAN-event circuits, and the country's manufacturing precision heritage uphold demand for premium mechanical keyboards and gaming chairs.

- U.K. Gaming Accessories Market Size

The United Kingdom represents approximately 18% of the European gaming accessories market in 2025. According to Ukie (UK Interactive Entertainment), the UK games market reached around £7.82 billion in 2024, ranking it among the top five globally. Demand drivers include high broadband penetration, a mature streamer community, and strong console attach rates, particularly for PlayStation 5 and Xbox Series X|S controllers and headsets.

- France Gaming Accessories Market Size

France accounts for around 15% of the European market in 2025. The Syndicat des Éditeurs de Logiciels de Loisirs (SELL) reported that the French games sector generated nearly €6.0 billion in 2024, with accessories among the fastest-growing sub-segments. The country's strong creative-tech ecosystem, anchored by domestic publishers such as Ubisoft and a thriving cosplay-and-streaming culture, supports continued peripheral upgrades.

Asia Pacific Gaming Accessories Market Trends and Insights

Asia Pacific is the fastest-growing region during the forecast period, supported by mobile-first consumption and rapid esports expansion. China alone, according to the China Audio-Video and Digital Publishing Association (CADPA), recorded gaming industry revenues exceeding ¥325 billion in 2024. Trends include surging mobile-controller demand, government-backed esports infrastructure, and aggressive penetration of homegrown brands.

- India Gaming Accessories Market Size

India is among the fastest-growing markets within Asia Pacific, contributing roughly 9% of the regional market in 2025. The Ministry of Electronics and Information Technology (MeitY), through its AVGC-XR Task Force, has positioned gaming as a strategic export sector. Smartphone-led gaming, low-cost wireless earbuds doubling as gaming headsets, and rising tournament participation through platforms like Krafton's BGMI are key demand engines.

- Japan Gaming Accessories Market Size

Japan holds an estimated 17% share of the Asia Pacific gaming accessories market in 2025. The Computer Entertainment Supplier's Association (CESA) reports that the domestic gaming industry exceeded ¥2 trillion in revenue in 2024. Strong loyalty toward Nintendo Switch peripherals, fighting-game arcade sticks, and premium audio brands such as Audio-Technica sustains a culturally distinctive accessory landscape with a high willingness to pay.

- Southeast Asia Gaming Accessories Market Size

Southeast Asia collectively represents around 12% of the Asia Pacific gaming accessories market in 2025, led by Indonesia, Vietnam, Thailand, and the Philippines. According to the Singapore Tourism Board, the region hosted multiple regional Mobile Legends: Bang Bang and Free Fire finals, drawing crowds exceeding 15,000 spectators in 2024. Affordable wireless gamepads and mobile-cooling accessories are the dominant entry-level product types.

Competitive Landscape

The gaming accessories market is moderately fragmented, blending a handful of globally scaled peripheral specialists with a long tail of regional brands and category-focused challengers competing primarily on price, design language, and esports credibility. Differentiation hinges on proprietary low-latency wireless technologies, integrated software ecosystems for customization and macros, and high-visibility sponsorship arrangements with leading professional gaming organizations and individual streamers across major titles.

R&D intensity is rising sharply in haptic feedback, AI-tuned spatial audio, biometric sensing, and adaptive ergonomics, with manufacturers racing to embed firmware-upgradable features that extend product relevance. Subscription-linked software updates, modular hardware platforms with user-replaceable components, and creator-economy partnerships are emerging as defensible business models that lock in consumer loyalty beyond the initial hardware purchase cycle.

Key Developments:

- In January 2025, Razer launched the Razer Kitsune all-button optical arcade controller for PlayStation 5, marking a strategic push into the premium fighting-game peripherals segment and reinforcing its position in tournament-grade competitive accessories.

- In September 2024, Logitech G unveiled the G PRO X 2 LIGHTSPEED Superlight 2 wireless mouse featuring the upgraded HERO 2 sensor, targeting professional esports athletes with reduced weight, sharper tracking precision, and extended battery life.

- In May 2024, Sony Interactive Entertainment expanded its official PlayStation accessories portfolio by releasing the PULSE Elite wireless headset and PULSE Explore wireless earbuds, deepening its first-party audio ecosystem and lossless audio experience for PS5 users.

Gaming Accessories Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 8.8 billion |

| Current Market Value (2026) | US$ 14.2 billion |

| Projected Market Value (2033) | US$ 26.1 billion |

| CAGR (2026 - 2033) | 9.1% |

| Leading Region | North America, 35% |

| Dominant Category-1 | Headsets, 28% |

| Top-ranking Category-2 | PC Gaming, 44% |

| Incremental Opportunity | US$ 11.9 billion |

Companies Covered in Gaming Accessories Market

- Logitech International S.A.

- Razer Inc.

- Corsair Gaming, Inc.

- HyperX (HP Inc.)

- SteelSeries (GN Store Nord A/S)

- Sony Interactive Entertainment

- Microsoft Corporation

- Turtle Beach Corporation

- Astro Gaming

- Mad Catz Global Limited

- Cooler Master Co., Ltd.

- ASUSTeK Computer Inc. (ROG)

- Thrustmaster (Guillemot Corporation)

- GameSir

- NACON SA

Frequently Asked Questions

The global gaming accessories market is expected to be valued at US$ 14.2 billion in 2026, advancing toward US$ 26.1 billion by 2033 at a forecast CAGR of 9.1%.

The strongest driver is the global expansion of esports and competitive gaming, supported by professional tournament prize pools exceeding US$ 480 million in 2024 and Olympic recognition through the Olympic Esports Games 2027.

North America is the leading region with approximately 35% market share in 2025, underpinned by mature esports infrastructure, high household console and PC penetration, and a strong creator economy anchored by the United States.

The fastest-emerging opportunity lies in VR accessories and sustainable, modular peripherals, supported by next-generation devices from Meta, Sony, and Apple alongside the EU's Right to Repair Directive adopted in 2024.

Major companies include Logitech, Razer, Corsair, HyperX, SteelSeries, Sony Interactive Entertainment, Microsoft, Turtle Beach, ASUS ROG, and Cooler Master.