- Hardware & Software IT Services

- VR Gaming Accessories Market

VR Gaming Accessories Market Size, Share, and Growth Forecast 2026 - 2033

VR Gaming Accessories Market by Product Type (Headsets, Motion Controllers, Haptic Feedback Devices, Tracking Devices, VR Treadmills, Other), Platform (PC-based, Console-based, Smartphone-based, Other), Application (Gaming, Simulation & Training, Education, Entertainment, Other), Distribution Channel (Online, Specialty Store, Supermarket/Hypermarket, Other), and Regional Analysis for 2026 - 2033

VR Gaming Accessories Market Size and Trend Analysis

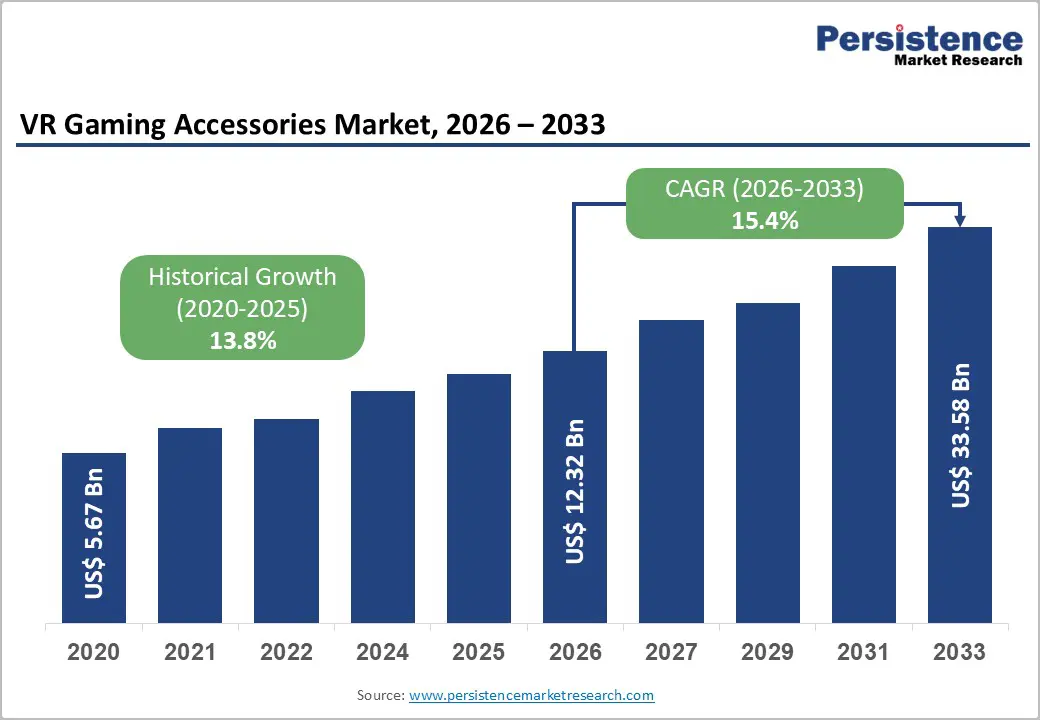

The global VR gaming accessories market size is likely to be valued at US$ 12.3 billion in 2026 and is projected to reach US$ 33.6 billion by 2033, growing at a CAGR of 15.4% between 2026 and 2033.

This robust expansion is driven by the increasing affordability of VR headsets, making immersive gaming experiences accessible to broader consumer segments, coupled with technological advancements in motion tracking, haptic feedback systems, and ergonomic design enhancements. The growing adoption of VR technology across gaming platforms and the rising consumer demand for interactive entertainment experiences are accelerating market penetration, particularly as major technology companies such as Meta, Sony Corporation, and HTC Corporation continue to invest heavily in product innovation and ecosystem development.

Key Market highlights

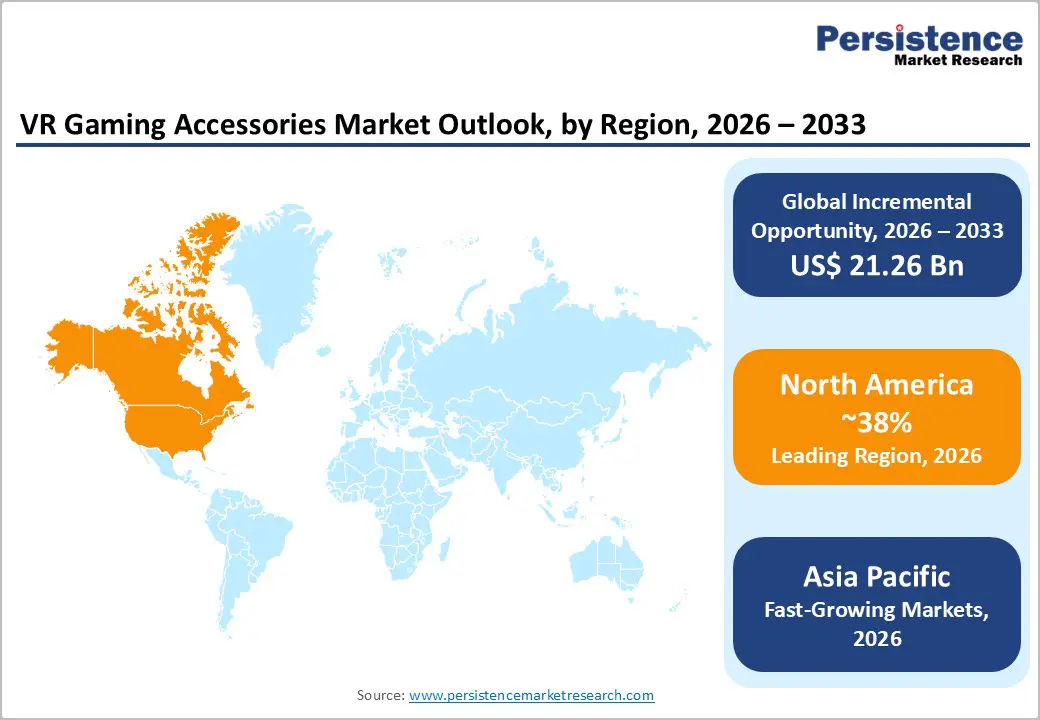

- Regional Leader: North America leads the VR Gaming Accessories Market, with 38% market share, due to robust innovation hubs, high spending, and Meta-Valve dominance shaping global trends.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, propelled by manufacturing in China-India, youth demographics, and policy support for digital gaming surge.

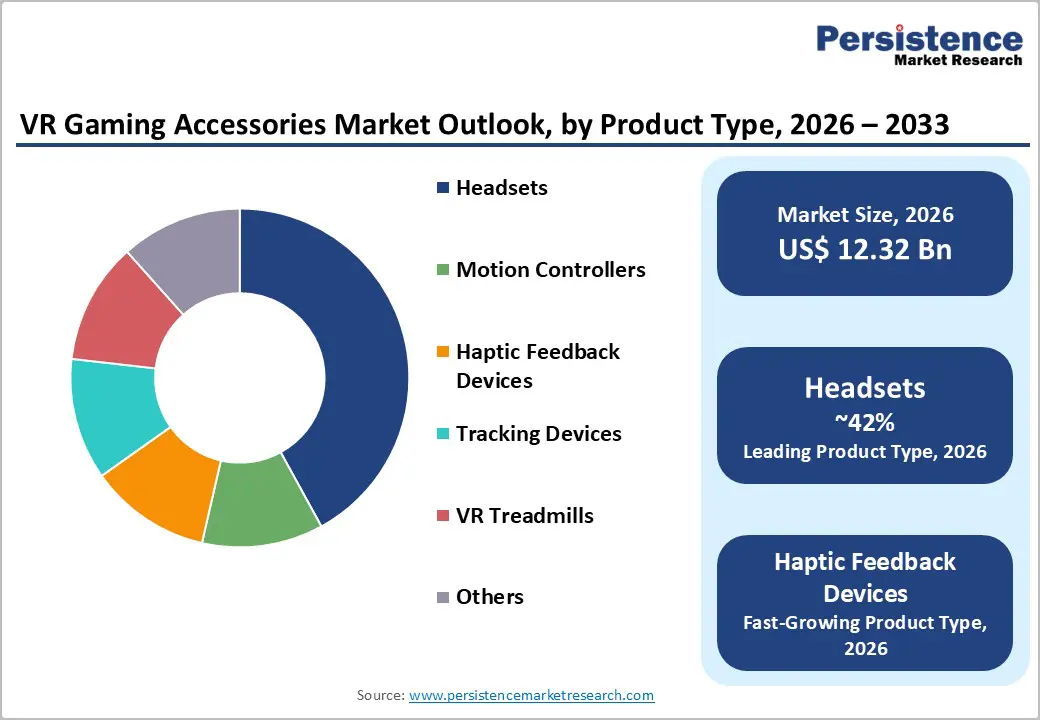

- Dominant Segment: Headsets dominate product segments with 42% share, essential for core immersion and compatible with all platforms per industry benchmarks.

- Fastest Growing Segment: Haptic Feedback Devices grow fastest in products, fueled by consumer demand for deeper immersion and sensory realism.

- Key Market Opportunity: Integration of AI-powered adaptive accessories, cross-platform compatibility solutions, and expansion into enterprise training and simulation applications beyond entertainment represent transformative opportunities for market participants to differentiate products, capture premium segments, and diversify revenue streams.

| Key Insights | Details |

|---|---|

| VR Gaming Accessories Market Size (2026E) | US$ 12.3 Bn |

| Market Value Forecast (2033F) | US$ 33.6 Bn |

| Projected Growth CAGR (2026 - 2033) | 15.4% |

| Historical Market Growth (2020 - 2025) | 13.8% |

Market Dynamics

Drivers - Advancements in Immersive VR Technologies

Rapid advancements in virtual reality (VR) hardware, including enhanced tracking precision, sophisticated haptic feedback, and standalone headsets, are significantly driving the growth of the market. These innovations deliver highly immersive environments, attracting gamers seeking deeper engagement beyond conventional screens. For example, features such as pancake lenses and refresh rates up to 120 Hz in devices like Meta Quest 3 have improved user satisfaction, with over 70% of gamers reporting enhanced immersion. This progress also stimulates demand for complementary accessories within the broader gaming accessories market.

Furthermore, gaming and entertainment applications drive strong demand for controllers, gloves, vests, and full-body haptic suits that provide vibration, force feedback, and texture simulation, allowing players to feel in-game actions and virtual environments physically. This technological evolution is complemented by improvements in motion tracking accuracy, eye-tracking capabilities, and depth-correct mixed reality features as demonstrated by HTC VIVE's Focus Vision headset, launched in September 2024, which incorporates built-in eye-tracking, stereo color passthrough cameras, and infrared sensors for enhanced hand tracking in low-light conditions.

Expanding Consumer Base Through Hardware Affordability and Platform Diversification

The growing affordability of VR hardware across PC-based, console-based, and smartphone-based platforms is democratizing access to immersive gaming experiences and expanding market penetration among diverse consumer segments. According to the Entertainment Software Association (ESA), global VR headset sales exceeded 11.2 million units in 2021, while U.S. consumers spent $57.2 billion on the video game industry in 2022, with a significant share allocated to hardware and accessories. Valve’s hardware survey reported that active VR headset usage among Steam users reached 2.13% in December 2024, reflecting strong adoption despite economic challenges.

Market growth is further propelled by the rise of e-sports and the increasing popularity of social and multiplayer VR gaming, which require accessories enabling seamless interaction. This broadening consumer base is supported by continuous product innovation from major manufacturers, with approximately 9.6 million VR headsets shipped globally in 2024, indicating sustained market momentum. Continuous product innovation and diversified distribution channels, including online platforms and specialty stores, reinforce sustained momentum in the global gaming ecosystem.

Restraints - High Initial Investment Costs and Economic Barriers to Adoption

The substantial initial investment required for premium VR gaming systems and accessories remains a significant barrier to widespread market adoption, particularly in price-sensitive markets and emerging economies. Despite gradual price reductions, complete VR gaming setups, including headsets, motion controllers, haptic devices, and tracking systems, can cost several hundred to over a thousand dollars, which limits accessibility for middle-income consumers. This economic constraint is exemplified by Sony's decision to raise the price of its PlayStation VR2 headset to 89,980 yen ($622) in September 2024, representing a 20% increase that further restricts market penetration.

The high cost structure is compounded by the need for additional peripheral investments such as upgraded gaming PCs or console systems capable of supporting VR experiences, creating a cumulative financial burden that deters potential buyers. Market data indicates that Sony's PS VR2 experienced a 25% year-over-year decline in annual shipments for 2024 despite efforts to integrate with PC platforms, highlighting how pricing challenges negatively impact demand even for established brands.

Motion Sickness and Technical Limitations

Technical challenges, including motion sickness, limited battery life, computational requirements, and ergonomic discomfort, continue to pose significant restraints on market growth and user retention. Motion sickness affects a considerable portion of VR users, particularly during extended gaming sessions or with content featuring rapid movement, which limits the appeal of VR gaming accessories to mainstream audiences. Battery life constraints in standalone and wireless VR systems necessitate frequent recharging or the purchase of additional hot-swappable batteries, disrupting the immersive gaming experience and adding to ownership costs.

The requirement for significant computing power to render high-quality VR graphics at acceptable frame rates creates hardware bottlenecks that restrict the addressable market to consumers with high-performance gaming systems. Ergonomic issues such as headset weight, pressure points, and heat accumulation during prolonged use have prompted manufacturers like HTC to introduce improved face gaskets, deluxe straps, and enhanced cooling systems, indicating that comfort remains an unresolved challenge affecting user satisfaction and repeat purchases.

Market Opportunities

Integration of Artificial Intelligence and Cross-Platform Compatibility Solutions

The integration of AI-powered adaptive accessories, IoT-enabled peripherals, and cross-platform compatibility solutions presents a significant opportunity for market differentiation and premium positioning. AI-driven capabilities such as automatic calibration, personalized haptic feedback, predictive motion tracking, and adaptive difficulty enhance user engagement by tailoring experiences to individual preferences. Developing accessories compatible with multiple platforms, including Meta Quest, PlayStation VR2, HTC Vive, and PC VR systems, addresses consumer demand for versatility and minimizes platform-specific investments.

Furthermore, the convergence of VR gaming with enterprise training, simulation, and education enables manufacturers to diversify revenue streams beyond entertainment. HTC VIVE’s Focus Vision headset exemplifies the viability of dual-purpose solutions for professional and gaming applications. Emerging mixed reality trends further necessitate advanced accessories featuring improved passthrough cameras, spatial computing, and environmental sensors, supported by innovations in lightweight materials, extended battery life, and modular ecosystems.

Expansion into Emerging Platforms and Regions

Standalone and hybrid AR/VR platforms present significant growth opportunities, particularly within the Asia Pacific’s rapidly expanding gaming market. Strategic collaborations among leading technology firms such as Google, Samsung, and Qualcomm highlight untapped potential for affordable, mobile-integrated accessories. The region is projected to achieve 20 million headset units, supported by strong manufacturing capabilities and a youthful demographic driving adoption.

China’s gaming community demonstrates high demand for immersive experiences, reinforced by substantial investments in VR content development. Rising internet penetration, cost reductions, and local manufacturing in China and India further enhance accessibility. Asia Pacific’s robust esports ecosystem and the presence of key players in hardware and content creation accelerate market expansion. Government initiatives promoting digital infrastructure and VR innovation, alongside policies supporting entertainment technologies, strengthen market fundamentals and create opportunities for accessories such as treadmills and trackers.

Category-wise Analysis

Product Type Insights

Headsets dominate the VR Gaming Accessories market with an estimated market share of approximately 42%, driven by continuous technological advancements and their fundamental role as the primary interface for immersive gaming experiences. The segment's leadership is supported by declining prices that make VR headsets accessible to broader consumer demographics while maintaining premium product lines for enthusiasts demanding cutting-edge features. Product innovation from major manufacturers, including Meta's Quest 3 and Quest 3S, Sony's PlayStation VR2, and HTC's Focus Vision, continues to enhance display resolution, field of view, refresh rates, and comfort features, maintaining consumer interest and upgrade cycles.

The increasing adoption of standalone VR headsets that do not require external computing devices is particularly significant, as these systems lower entry barriers and expand the addressable market beyond dedicated gaming enthusiasts to casual users. The integration of mixed reality capabilities, eye-tracking technologies, and improved ergonomics in next-generation headsets further strengthens market fundamentals by delivering enhanced user experiences that justify premium pricing and encourage ecosystem investments in complementary Gaming Accessories Market products.

Platform Insights

PC-based VR gaming accessories account for nearly 38% of the market, underscoring the platform’s ability to deliver superior graphical fidelity, processing power, and customization options sought by professional users and hardcore gamers. These systems support demanding gaming titles, simulation applications, and enterprise training programs that exceed the capabilities of consoles and smartphones. The platform benefits from a mature ecosystem of accessories, including precision motion controllers, full-body tracking systems, haptic feedback devices, and VR treadmills, all leveraging PC performance for immersive experiences.

Steam’s hardware survey reported 2.13% active VR headset usage in December 2024, reflecting sustained engagement. Beyond gaming, compatibility with applications such as architectural visualization, medical training, and industrial simulation diversifies demand. Leading manufacturers like HTC and Valve continue to innovate with products offering DisplayPort connectivity and refresh rates up to 120 Hz, reinforcing PC VR’s premium positioning.

Application Insights

Gaming applications represent approximately 65% of the VR gaming accessories market, driven by consumers’ primary motivation to purchase VR systems for entertainment and interactive experiences. This dominance is supported by ESA data indicating global VR headset sales of 11.2 million units in 2021, with most buyers prioritizing gaming. The immersive nature of VR, offering 360-degree environments, realistic interactions, and social multiplayer features, creates strong demand for high-quality accessories such as precision motion controllers, haptic feedback devices, and spatial audio systems.

While Simulation & Training is a fast-growing niche, the volume of consumer-grade accessory sales is overwhelmingly driven by the entertainment sector, where the immersive nature of VR is a key selling point for action and adventure genres. Competitive VR esports, social platforms, and multiplayer experiences further expand applications beyond solo entertainment, fostering community-driven engagement and increased accessory utilization.

Distribution Channel Insights

Online distribution channels account for approximately 45% of the VR gaming accessories market, driven by convenience, price transparency, and extensive product availability offered by e-commerce platforms. Leading platforms such as Amazon, manufacturer websites like Meta.com, and HTC Vive’s online store, and specialized gaming retailers provide detailed product information, customer reviews, and competitive pricing, enabling informed purchase decisions. These channels allow manufacturers to maintain direct consumer relationships, gather usage insights, and offer subscription services or bundled accessories to enhance customer lifetime value.

Their efficiency in inventory management, logistics, and global reach eliminates the need for extensive physical retail infrastructure. The COVID-19 pandemic accelerated digital commerce adoption, establishing lasting online purchasing behaviors. Additionally, pre-order campaigns, such as HTC’s Focus Vision headset promotion with complimentary accessories, demonstrate how online platforms create marketing momentum and drive demand.

Regional Insights

North America VR Gaming Accessories Market Trends

North America leads the VR gaming accessories market, supported by advanced technological infrastructure, high disposable incomes, and a strong gaming culture that encourages premium product adoption. The U.S. dominates the region, with video game industry spending reaching $57.2 billion in 2022, underscoring significant commercial scale and purchasing power. The presence of major VR technology companies such as Meta, Microsoft, and Valve fosters continuous innovation in hardware, software, and accessory ecosystems. Favorable regulatory frameworks in the U.S. and Canada further promote technology development while ensuring consumer protection.

North America’s innovation ecosystem, driven by venture capital, research institutions, and technology clusters in hubs like Silicon Valley and Seattle, accelerates product development and market introduction. Sustained engagement, reflected by 2.13% active VR headset usage on Steam in December 2024, positions the region as a global trendsetter influencing adoption patterns worldwide.

Europe VR Gaming Accessories Market Trends

Europe is a key market for VR gaming accessories, led by Germany, the U.K., France, and Spain, driven by advanced technology infrastructure, expanding gaming communities, and growing localization of VR content. Harmonized regulations under European Union frameworks create standardized conditions that simplify cross-border commerce and reduce compliance complexity. Germany’s position as the region’s largest economy and its engineering expertise support strong adoption of premium, technically advanced products, while the U.K.’s vibrant gaming culture sustains demand for high-performance peripherals.

France and Spain contribute through rising gaming populations, improved broadband penetration, and broader acceptance of VR beyond early adopters. European consumers prioritize quality, sustainability, and product longevity, creating opportunities for manufacturers offering durable, modular designs. Regional diversity necessitates localized content and partnerships, while trade shows and conventions enhance brand visibility and consumer engagement under strict data privacy and safety standards.

Asia Pacific VR Gaming Accessories Market Trends

Asia Pacific is witnessing the fastest growth in the VR gaming accessories market, projected to expand at a CAGR exceeding 23% from 2025 to 2030. This surge is driven by dynamic gaming ecosystems and favorable demographics across China, Japan, India, and ASEAN nations. China leads the region with its vast consumer base, supportive government policies, and significant investments in VR content and hardware manufacturing, leveraging its position as a global production hub for cost efficiency.

Japan contributes through advanced technology development and a strong gaming culture, while India’s large youth population, rising smartphone penetration, and increasing disposable incomes fuel mobile VR adoption. ASEAN countries, including Vietnam, Thailand, Indonesia, and the Philippines, show strong potential due to growing middle classes and improved digital infrastructure. Diverse market conditions necessitate tailored strategies addressing income levels, infrastructure maturity, and cultural preferences.

Competitive Landscape

The VR gaming accessories market is moderately consolidated, with major technology players such as Meta, Sony Corporation, Microsoft Corporation, and HTC Corporation holding significant market shares, while niche segments attract specialized and emerging manufacturers. Leading companies adopt strategies focused on ecosystem integration, exclusive content partnerships, and continuous technological innovation to sustain competitive advantages. Expansion efforts emphasize geographic diversification, particularly in high-growth Asia Pacific markets, alongside vertical integration across hardware, software, and content development to maximize value chain margins. Differentiators include proprietary tracking systems, ergonomic design, platform-specific optimization, and developer support programs. Emerging business models feature subscription-based content access, enterprise accessory rentals, and modular designs enabling component upgrades without full system replacement.

Key Market Developments

- September 2024: HTC VIVE launched the Focus Vision XR headset featuring built-in eye-tracking, stereo color passthrough cameras for depth-correct mixed reality, infrared sensors for enhanced hand tracking, and DisplayPort mode support for visually lossless PCVR experiences, with pre-orders receiving complimentary wired streaming kits valued at USD $149.

- June 2024: HTC announced the Vive XR Elite Deluxe Pack, including four free accessories, an improved face gasket, mixed reality face gasket, deluxe strap for better weight distribution, and temple clips, available to new and existing customers to enhance headset ergonomics and user comfort.

- October 2024: Meta officially launched the Quest 3S, a budget-friendly mixed reality headset priced at US$ 299, significantly driving demand for compatible entry-level accessories.

Top Companies in the VR Gaming Accessories Market

- Meta (Menlo Park, U.S.) dominates the consumer VR market through its Quest product line, leveraging extensive resources for research and development, aggressive pricing strategies, and comprehensive content ecosystems that drive accessories adoption. The company's vertical integration across hardware, software platforms, and content creation enables seamless user experiences and strong customer retention. Meta's continuous product iteration, including Quest 3 and Quest 3S, maintains market leadership while expanding addressable markets through standalone functionality that eliminates PC dependency.

- Sony Corporation (Tokyo, Japan) leverages its PlayStation gaming ecosystem and consumer electronics expertise to deliver integrated VR solutions for console gamers. The company's strength lies in exclusive gaming content, established distribution networks, and brand recognition among gaming enthusiasts. Sony's focus on high-fidelity graphics, proprietary haptic feedback technologies, and seamless PlayStation console integration differentiates its accessories offerings in the premium gaming segment.

- HTC Corporation (Taoyuan, Taiwan) positions itself as a premium VR technology provider serving both consumer and enterprise markets with products like the Vive Focus Vision and Vive XR Elite that emphasize technical specifications, professional applications, and PC VR capabilities. The company's strategy focuses on high-end segments, enterprise training and simulation use cases, and location-based entertainment venues where performance specifications justify premium pricing. HTC's commitment to continuous innovation, comprehensive accessory ecosystems including tracking devices and haptic peripherals, and strong developer relationships maintain competitive relevance.

Companies Covered in VR Gaming Accessories Market

- Meta

- Sony Corporation

- HTC Corporation

- Valve Corporation

- Microsoft Corporation

- Google LLC

- Shenzhen Youban Zhihui Technology Co., Ltd

- KIWI design

- Samsung Electronics Co., Ltd.

- Turtle Beach Corporation

- Logitech International S.A.

Frequently Asked Questions

The global VR gaming accessories market is projected to reach a value of US$ 33.6 Bn by 2033, expanding significantly from US$ 12.3 Bn in 2026.

Key drivers include the rapid technological advancements in haptic feedback systems and the increasing affordability and adoption of standalone VR headsets like the Meta Quest series.

The Headsets segment dominates the market, accounting for the 42% revenue share as the essential primary hardware required for virtual reality experiences.

North America is expected to remain the leading region, driven by a mature gaming ecosystem, high consumer spending power, and the presence of key technology innovators.

A significant opportunity lies in the fitness and wellness sector, where there is growing demand for accessories that support "Exergaming" and biometric tracking for health-conscious users.

Major players include Meta, Sony Corporation, HTC Corporation, Valve Corporation, Microsoft Corporation, Samsung Electronics, and Logitech International.