- Media & Entertainment

- Mobile and Handheld Gaming Market

Mobile and Handheld Gaming Market Size, Share, and Growth Forecast 2026 - 2033

Mobile and Handheld Gaming Market by Game Type (Action, Adventure, Puzzle, Sports, Other), Device Type (Smartphones, Tablets, Handheld Consoles, Other), Operating System (Android, iOS, Other), and Regional Analysis for 2026-2033

Mobile and Handheld Gaming Market Size and Trend Analysis

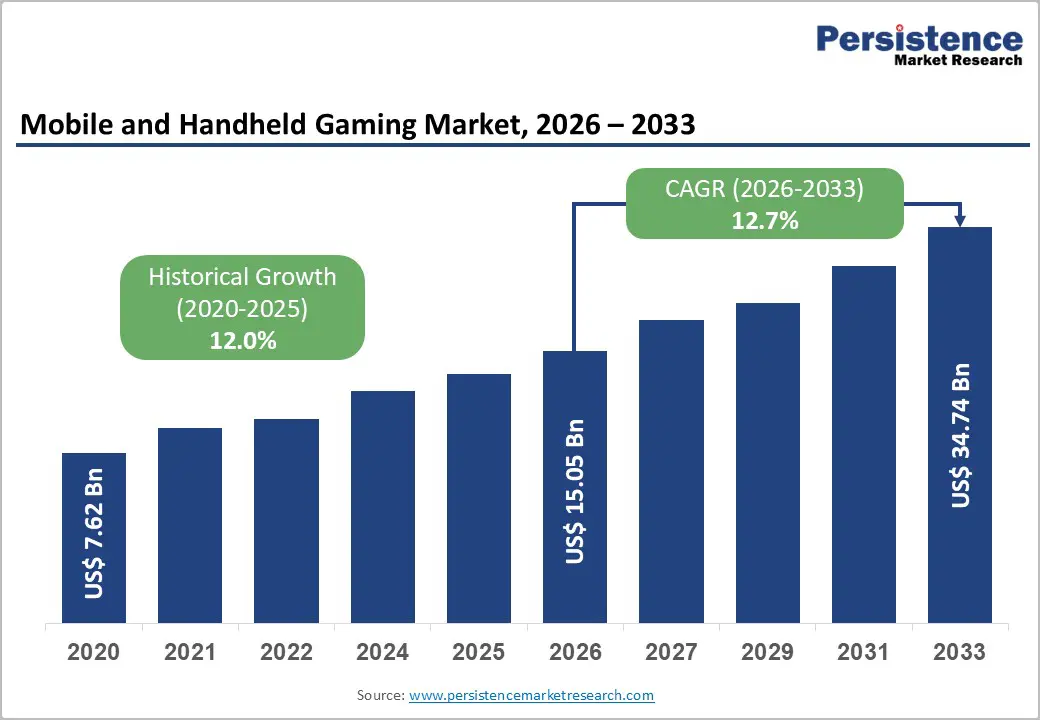

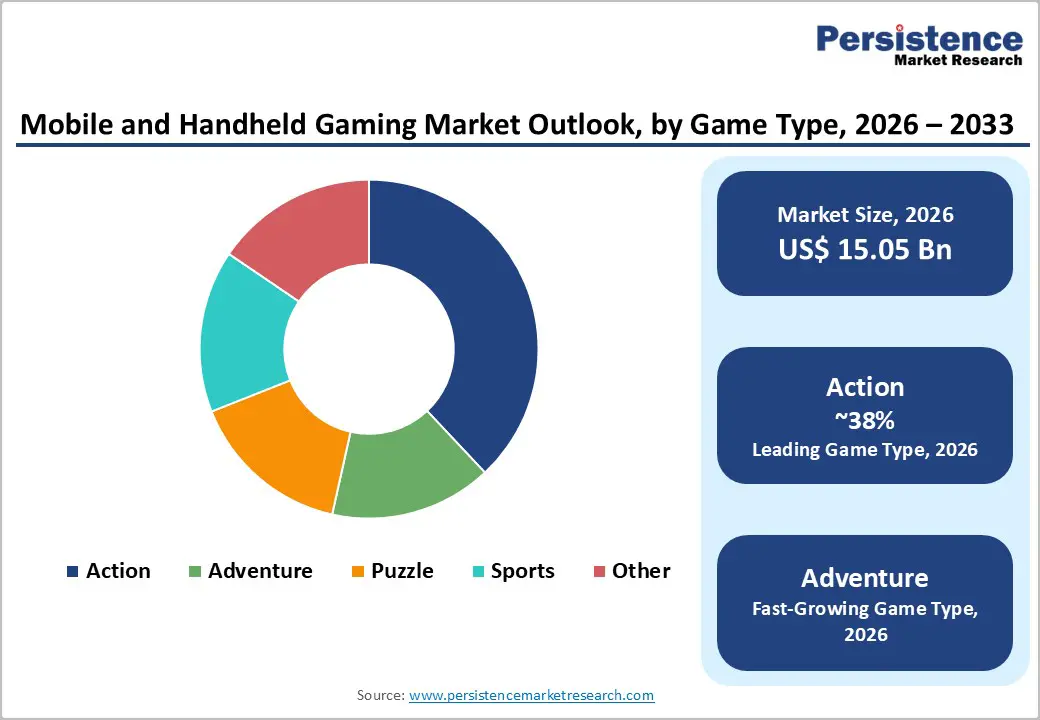

The global mobile and handheld gaming market size is supposed to be valued at US$ 15.0 Bn in 2026 and is projected to reach US$ 34.7 Bn by 2033, growing at a CAGR of 12.7% between 2026 and 2033.

The market expansion is driven by unprecedented smartphone penetration reaching 6.9 billion users globally by 2024, coupled with over 5.3 billion mobile internet users providing an extensive user base for gaming adoption. The proliferation of affordable budget smartphones priced under US$ 150 and data costs below US$ 1/GB in developing economies has democratized gaming access, fueling participation across diverse demographics and geographies.

Key Market Highlights

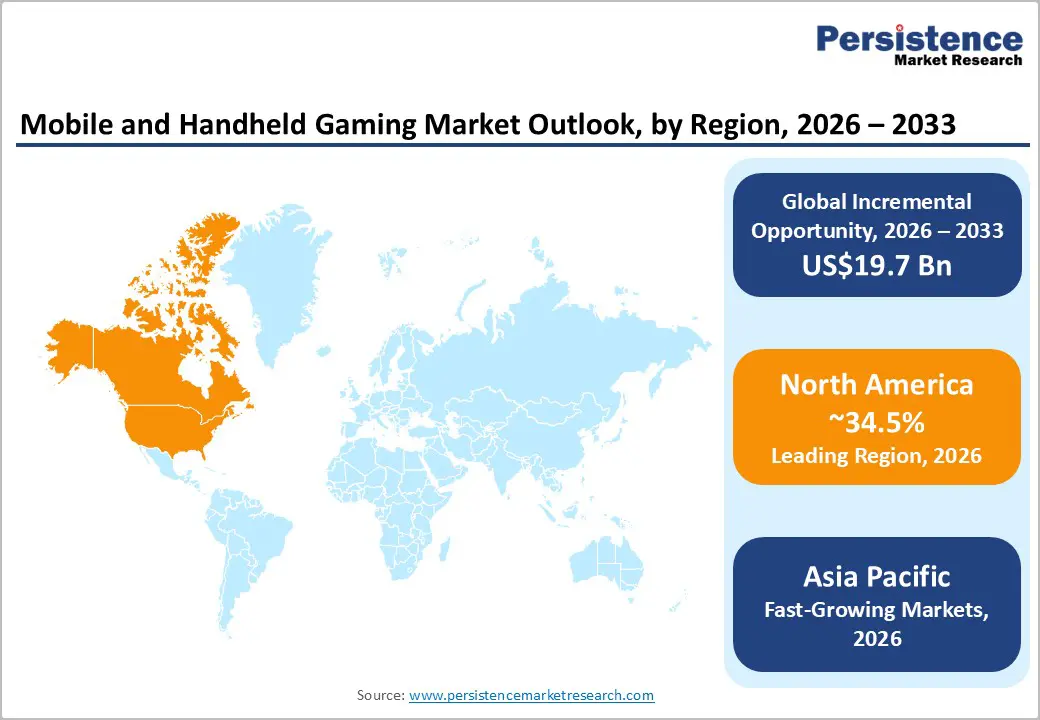

- Leading Region: North America dominates the market, with 34.5% market share, driven by the United States’ advanced digital infrastructure, high smartphone penetration, and a mature ecosystem fostering innovation and premium content adoption.

- Fastest Growing Region: Asia-Pacific demonstrates exceptional growth momentum, driven by massive smartphone adoption exceeding 750 million users in India alone, strong performance from China, Japan, and South Korea.

- Dominant Segment: Smartphones emerge as the dominant device segment, capturing approximately 72% market share, benefiting from the massive installed base of 6.9 billion users worldwide, constant connectivity, dual-purpose functionality eliminating the need for dedicated gaming hardware, and continuous improvements in processing capabilities enabling console-quality experiences.

- Fastest Growing Segment: Action games represent the fastest-growing segment within game type categorization, driven by immersive multiplayer mechanics, integration with mobile esports tournaments, and experiencing substantial expansion.

- Key Market Opportunity: Cloud gaming integration with 5G infrastructure presents the most significant market opportunity, enabling console-quality experiences without hardware limitations, as demonstrated by Deutsche Telekom's 5G+ Gaming offering providing access to 100 premium games, with smartphones projected to account for 60% of U.S. gaming revenues by 2025.

| Key Insights | Details |

|---|---|

| Mobile and Handheld Gaming Market Size (2026E) | US$ 15.0 Bn |

| Market Value Forecast (2033F) | US$ 34.7 Bn |

| Projected Growth CAGR (2026-2033) | 12.7% |

| Historical Market Growth (2020-2025) | 12.0% |

Market Dynamics

Market Growth Drivers

5G Infrastructure Expansion and Cloud Gaming Integration

The global deployment of 5G networks stands as a significant catalyst for the growth of mobile and handheld gaming. According to the Ericsson Mobility Report, 5G subscriptions exceeded 1.7 billion in early 2024 and are projected to reach 5.6 billion by 2029, accounting for 60% of all mobile subscriptions. This advancement in infrastructure allows for latency reductions to below 20 milliseconds, making competitive multiplayer gaming feasible on mobile devices.

The convergence of 5G technology with cloud gaming platforms marks a transformative shift in the industry. In 2024, Xbox Cloud Gaming expanded its beta program to enable direct game purchases via mobile applications. Concurrently, NVIDIA GeForce NOW has integrated with 5G edge computing nodes to facilitate 4K streaming at 60 frames per second on handheld devices. This technological synergy removes hardware limitations, enabling smartphones and tablets to access AAA titles previously reserved for consoles.

Cross-Platform Ecosystem Development and Social Gaming Features

The evolution towards seamless cross-platform ecosystems has significantly transformed player engagement patterns. According to Newzoo's 2023 Global Gamers Study, 79% of gamers are now engaging on mobile devices. Advanced social integration features further enhance this widespread adoption. Remarkably, Tencent's Honor of Kings generated $1.8 billion in revenue in 2024 by incorporating real-time voice chat, live streaming capabilities, and tournament systems that replicate console experiences. This success illustrates that mobile gaming has evolved beyond casual play, with core gamers spending an average of 14.2 minutes per session on iOS devices, comparable to the time spent on traditional consoles.

Furthermore, Nintendo's strategic launch of Nintendo Switch Online services has resulted in subscription revenue of $1.19 billion, reflecting a 19% year-over-year growth. This underscores the effectiveness of the subscription-as-a-service model within handheld ecosystems. The Entertainment Software Association reports that 78% of players in the United States now utilize mobile devices for gaming, representing a remarkable 136% increase over the past decade. This trend indicates that platform agnosticism has emerged as the prevailing consumer expectation, rather than merely a niche preference.

Market Restraints

Regulatory Fragmentation and Data Privacy Compliance

The gaming industry is facing significant challenges related to data protection regulations and privacy compliance across multiple jurisdictions, leading to operational complexities and potential legal liabilities. The U.S. Consumer Financial Protection Bureau (CFPB) estimates that 58% of online game users are under 16, highlighting the need for strict adherence to regulations such as the California Consumer Privacy Act (CCPA) and the Children's Online Privacy Protection Act (COPPA). In 2024, California settled with a SpongeBob game app developer for $500,000 due to allegations of unauthorized collection and sharing of personal information from users under 13.

The mobile gaming sector is experiencing further regulatory headwinds as governments worldwide enact varying data protection frameworks. The European Union's enforcement of the Digital Markets Act (DMA) in 2024 disrupted traditional revenue models, requiring Google to allow third-party payment processors and leading to a 15% reduction in platform fees, which increased churn rates by 8% among European users. Additionally, China's Personal Information Protection Law (PIPL) has forced companies like Tencent to localize data storage, raising annual infrastructure costs by $200 million and restricting cross-border data analytics.

Hardware Limitations and Thermal Throttling in High-Performance Gaming

Despite the advancements in technology, fundamental hardware constraints continue to present significant challenges to achieving console-quality gaming experiences on mobile devices. Particularly, thermal throttling in smartphones can reduce processor performance by 30-40% during prolonged gaming sessions. This limitation restricts sustained gameplay for graphically intensive titles. For instance, AnTuTu benchmarking data indicates that flagship devices experience a 25% performance degradation after just 20 minutes of playing Genshin Impact at maximum settings.

Battery consumption is another critical concern, as premium mobile games can drain approximately 1% of battery life per minute of active play. This factor creates usability challenges, resulting in approximately 35% of users choosing to abandon their gaming sessions prematurely. The handheld console market faces similar struggles, with Nintendo Switch hardware sales declining by 30.3% year-over-year in FY2024, indicative of market saturation and the technological stagnation associated with current-generation chipsets. Although cloud gaming offers potential solutions to some of these issues, gaps in 5G network coverage persist. Data from the FCC indicates that 7% of rural Americans still lack access to 5G, which creates a digital divide and excludes approximately 23 million potential users from accessing high-quality mobile gaming experiences.

Market Opportunities

Emerging Markets Expansion and Localization Strategies

Emerging markets constitute a critical growth frontier for the mobile and handheld gaming sector. In India, 5G subscriptions are expected to rise sharply from 119 million in 2023 to 840 million by 2029, representing 65% of all mobile subscriptions. This rapid infrastructure expansion, combined with 950 million mobile internet users, has created a USD 4.7 billion gaming download market that recorded 6% growth in early 2024. Tencent leveraged this momentum by localizing PUBG Mobile, achieving 50 million daily active users prior to regulatory restrictions.

The Middle East and Africa are projected to grow, driven by Saudi Arabia's gaming population, where 51% of gamers prefer mobile platforms. Nintendo's strategic partnership with Tencent to distribute the Switch in China unlocked 12.62 million units sold in the region, demonstrating that culturally adapted content and distribution partnerships can overcome market entry barriers.

Direct-to-Consumer (D2C) Monetization and Web Shop Integration

The transition to Direct-to-Consumer (D2C) payment models offers a significant opportunity to eliminate platform fees and increase revenue by up to 30% per transaction. Regulatory changes in Europe compelling Apple and Google to permit alternative billing have accelerated this trend, with Ubisoft introducing web shops for Assassin’s Creed mobile titles to bypass app store commissions.

For handheld consoles, D2C subscriptions, such as those for Nintendo Switch Online, could retain an estimated $360 million annually. Microsoft’s 2024 initiative, enabling Xbox purchases directly via mobile apps, validated this approach, driving a 12% rise in conversion rates. Sensor Tower reports hybrid-casual games achieved 37% revenue growth through D2C strategies, while Android ad revenue reached $10 billion in H1 2024. Proprietary digital storefronts leveraging 5G connectivity can further capture the $19 billion digital add-on content market.

Category-wise Insights

Game Type Analysis

Action games hold the dominant position within the mobile and handheld gaming segment, accounting for nearly 38% of market share. This leadership is driven by immersive gameplay, competitive multiplayer modes, and high engagement levels that foster long-term retention. Prominent titles such as PUBG, Call of Duty Mobile, and Honor of Kings exemplify this strength, with the latter sustaining global success despite regulatory challenges in China.

The genre benefits from cross-platform compatibility, frequent content updates, and integration with esports ecosystems, which enhance visibility and participation. Mobile esports tournaments, particularly in Latin America, have experienced notable growth, generating revenue through sponsorships, media rights, and entry fees. Advancements in device processing power further enable console-quality graphics and responsive controls, elevating the mobile action gaming experience.

Device Type Analysis

Smartphones dominate the mobile and handheld gaming market, accounting for nearly 72% of the total share, driven by widespread availability, affordability, and continuous advancements in processing technology. With an installed base of 6.9 billion users globally as of 2024, smartphones offer unmatched reach compared to dedicated handheld consoles. Regional trends reveal Android’s dominance in markets such as India and Brazil, while iOS maintains a strong revenue presence in the United States.

In the handheld segment, Nintendo Switch leads with lifetime sales exceeding 152 million units and 1.39 billion software units, securing 35.5% market share. Steam Deck follows closely at 35.6%, and ASUS ROG Ally holds 11.6%, reflecting growing interest in PC-compatible portable devices. Smartphones remain preferred for their portability, connectivity, and multifunctionality, appealing to casual and mid-core gamers across demographics.

Operating System Analysis

The Android operating system dominates the global mobile gaming market, accounting for over 70% of downloads as of 2025. This leadership is primarily driven by the widespread availability of affordable Android smartphones in emerging economies across Asia, Africa, and Latin America, where cost-sensitive consumers prioritize accessibility over premium features. Android’s open ecosystem supports multiple app stores beyond Google Play, including region-specific platforms such as Samsung Galaxy Store and third-party channels prevalent in China. India exemplifies this dominance with more than 750 million Android users, fueled by budget devices and localized content.

While iOS maintains a smaller user base, it generates disproportionately higher revenues per user, with the United States market demonstrating firm iOS territory preferences and China ranking second globally for iOS gaming downloads and revenue. Data from data.ai confirms that iOS dominates the Chinese market despite Android's global leadership, highlighting regional variations in platform preferences based on economic factors, device availability, and consumer purchasing power.

Regional Insights

North America Mobile and Handheld Gaming Trends

North America retains its leadership in the mobile and handheld gaming market, with 34.5% market share, driven by the United States’ advanced digital infrastructure, high smartphone penetration, and a mature ecosystem fostering innovation and premium content adoption. The region exhibits a strong preference for iOS, with the U.S. ranking as the leading market for Apple gaming revenues, supported by robust monetization through in-app purchases and subscriptions. Consumer trends favor multiplayer experiences, competitive esports, and action-adventure genres that sustain engagement and command premium pricing.

Microsoft’s acquisition of Activision Blizzard for US$68.7 billion in 2022 further strengthened the landscape, boosting Xbox content and services revenue by 50% in fiscal 2024. Additionally, stringent data privacy regulations, venture capital investment, telecom partnerships, and AI-driven personalization underscore the region’s dynamic and innovation-oriented gaming environment.

Europe Mobile and Handheld Gaming Trends

Europe represents a mature and highly regulated mobile gaming market, shaped by harmonized frameworks such as the GDPR and diverse consumer preferences across major economies, including Germany, the United Kingdom, France, and Spain. Germany stands as a leading market, with mobile gaming revenue nearing EUR 10 billion in 2023 and in-game purchases reaching EUR 4.742 billion, reflecting strong demand for premium content.

The U.K. demonstrates robust engagement, driven by high smartphone penetration and growing interest in multiplayer and esports genres. Significant developments include Epic Games’ 2024 relaunch of Fortnite in compliance with the EU Digital Markets Act and Deutsche Telekom’s 5G+ Gaming package offering access to premium titles. Despite regulatory complexities, government support for innovation and mobile services contributing EUR 1.1 trillion to GDP underscores the sector’s economic significance.

Asia Pacific Mobile and Handheld Gaming Trends

Asia Pacific stands as the fastest-growing region in the global mobile and handheld gaming market, driven by large population bases, rising disposable incomes, and widespread mobile device adoption across China, Japan, South Korea, India, and ASEAN nations. China, Japan, and South Korea consistently rank among the top five global markets for mobile gaming revenue, with South Korea generating approximately US$1.4 billion in Q3 2025, marking five-year highs through successful IP-based launches.

India leads regional growth, supported by over 750 million smartphone users and affordable data plans under US$1/GB, enabling gaming access across urban and rural demographics. Despite regulatory challenges, China retains market leadership with titles like Honor of Kings and PUBG. Manufacturing advantages further position Asia Pacific as a hardware hub, while Android dominates downloads and iOS drives premium revenues.

Competitive Landscape

Market Structure Analysis

The mobile and handheld gaming market is highly fragmented, comprising global technology leaders and independent studios, fostering intense competition and continuous innovation. Leading players such as Tencent Holdings, Microsoft, Nintendo, and Supercell pursue diverse strategies, including mergers and acquisitions, strategic partnerships, cross-platform content distribution, and investments in emerging technologies like cloud gaming and artificial intelligence. Key differentiators include proprietary IP development, social feature integration to enhance community engagement, adoption of free-to-play models with advanced monetization, and ecosystem strategies leveraging existing user bases. Emerging trends emphasize subscription services, telecom-bundled cloud gaming, and Web3 integration, enabling player ownership.

Key Market Developments

- June 2025: Tencent Holdings announced the integration of subsidiary Supercell's popular mobile games, beginning with Brawl Stars, as WeChat mini games, expanding monetization opportunities across WeChat's 1.4 billion monthly active users and strengthening the company's gaming ecosystem.

- December 2024: Pokémon Trading Card Game Pocket achieved remarkable commercial success, reaching 60 million downloads and generating US$ 180 million in revenue within six weeks post-launch, demonstrating sustained consumer demand for established intellectual property in mobile gaming formats.

- August 2024: Epic Games successfully relaunched Fortnite on iPhones in the European Union and Android devices worldwide following a four-year absence, leveraging the EU's Digital Markets Act provisions to ensure regulatory compliance and enable broader mobile user access.

Top Companies in Mobile and Handheld Gaming Trends

Tencent Holdings (Shenzhen, China) operates as the world's largest gaming company by revenue, maintaining dominant positions across mobile, PC, and console gaming segments through wholly-owned studios and strategic investments in leading publishers, including majority ownership of Supercell. The company's competitive advantage derives from integration of gaming content within its WeChat ecosystem, reaching 1.4 billion monthly users, demonstrated through the June 2025 launch of Supercell titles as WeChat mini games, alongside ownership of globally successful franchises including Honor of Kings and PUBG Mobile.

Nintendo Co., Ltd. (Kyoto, Japan) maintains market leadership in handheld console gaming with the Nintendo Switch achieving 152.12 million cumulative unit sales and 1.39 billion software sales as of March 2025, commanding 35.5% market share among dedicated handheld devices. The company's brand loyalty, hybrid console design enabling both portable and home gaming, and proprietary intellectual property portfolio, including Mario, Zelda, and Pokémon franchises, establish strong competitive moats and sustained consumer engagement.

Microsoft Corporation (Redmond, U.S.) has substantially strengthened its gaming operations following the US$ 68.7 billion acquisition of Activision Blizzard in 2022, resulting in 50% year-over-year increase in Xbox content and services revenue in fiscal 2024 as major franchises, including Call of Duty, Candy Crush, and Diablo, transitioned to first-party status. The acquisition enhances Microsoft's mobile gaming presence through popular titles, including Candy Crush, while the company pursues agnostic publishing strategies, launching content across PlayStation, Nintendo, and PC platforms to maximize addressable markets.

Companies Covered in Mobile and Handheld Gaming Market

- NVIDIA

- Microsoft

- Ubisoft Entertainment SA

- King Digital Entertainment, Plc

- Supercell Oy

- The Walt Disney Company

- HID Global

- Tencent Holdings

- Nintendo Co., Ltd.

Frequently Asked Questions

The global Mobile and Handheld Gaming Market is projected to reach US$ 34.7 billion by 2033, growing from US$ 15.0 billion in 2026 at a compound annual growth rate of 12.7% during the forecast period, driven by increasing smartphone penetration, expanding internet connectivity, and adoption of free-to-play monetization models across global markets.

The market growth is primarily driven by rapid smartphone adoption reaching 6.9 billion users globally with over 5.3 billion mobile internet users, availability of affordable budget smartphones priced below US$ 150 with data costs under US$ 1/GB in emerging economies, evolution of free-to-play models with in-app purchase monetization generating approximately US$ 92 billion in revenue during 2024, and integration of 5G networks enabling cloud gaming experiences without hardware limitations.

Action games command the leading position, capturing an estimated 38% market share, driven by immersive multiplayer mechanics, competitive gameplay features, high engagement rates sustaining long-term player retention, and the success of flagship titles including PUBG, Call of Duty Mobile, and Honor of Kings

North America dominates the market, with 34.5% market share, driven by the United States’ advanced digital infrastructure, high smartphone penetration, and a mature ecosystem fostering innovation and premium content adoption

Cloud gaming integration with 5G infrastructure presents transformative opportunities, enabling console-quality experiences without hardware limitations, as demonstrated by Deutsche Telekom's 5G+ Gaming offering providing six-month access to 100 premium games.

Leading market players include Tencent Holdings, Nintendo Co., Ltd., Microsoft Corporation, alongside Supercell Oy, King Digital Entertainment, Electronic Arts, Epic Games, and NVIDIA Corporation.