- Processed Food

- Frozen Vegetables Market

Frozen Vegetables Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Frozen Vegetables Market by Product Type (Mixed Vegetables, Beans, Peas, Corn and Baby Corn, Tomato, Carrot, Spinach, Others), Nature (Organic, Conventional), Distribution Channel (B2B, B2C), and Regional Analysis, 2026 - 2033

Frozen Vegetables Market Share and Trends Analysis

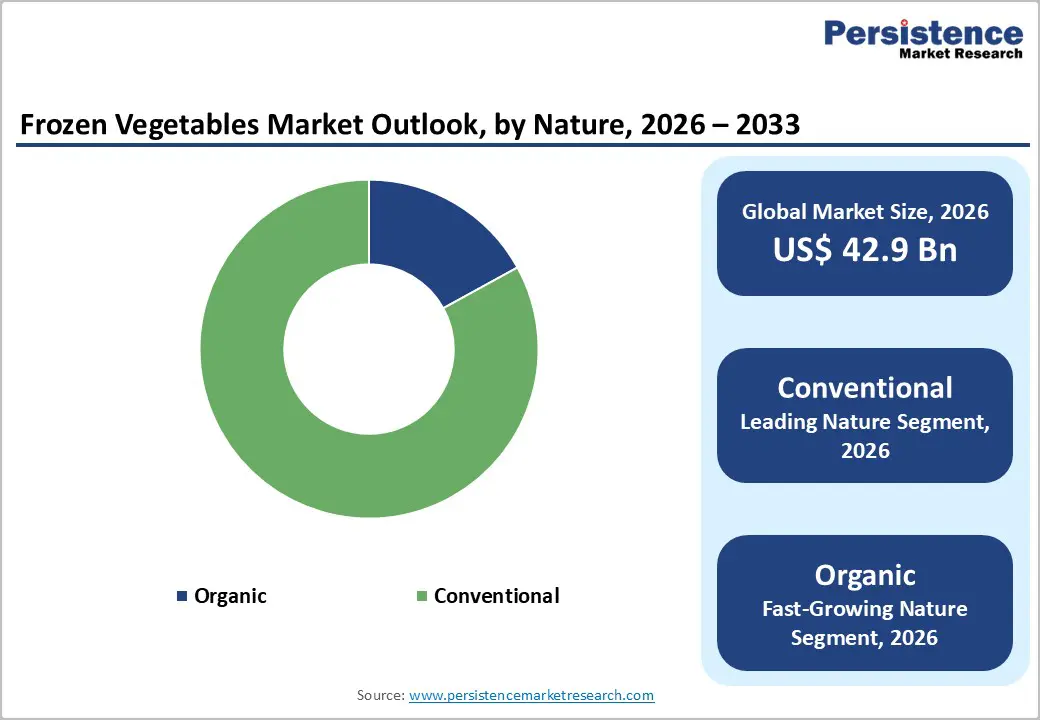

The global frozen vegetables market size is expected to be valued at US$ 42.9 billion in 2026 and projected to reach US$ 61.6 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

The market is undergoing a structural shift from basic preservation to value-added, convenience-driven nutrition solutions. What was once a storage solution is now a strategic category aligned with modern consumption patterns: health, speed, and minimal waste. Technological advancements such as IQF and improvements in cold-chain logistics are redefining quality benchmarks, enabling frozen vegetables to closely compete with fresh produce. At the same time, evolving retail ecosystems and rising urbanization are accelerating accessibility across both developed and emerging markets.

Key Industry Highlights:

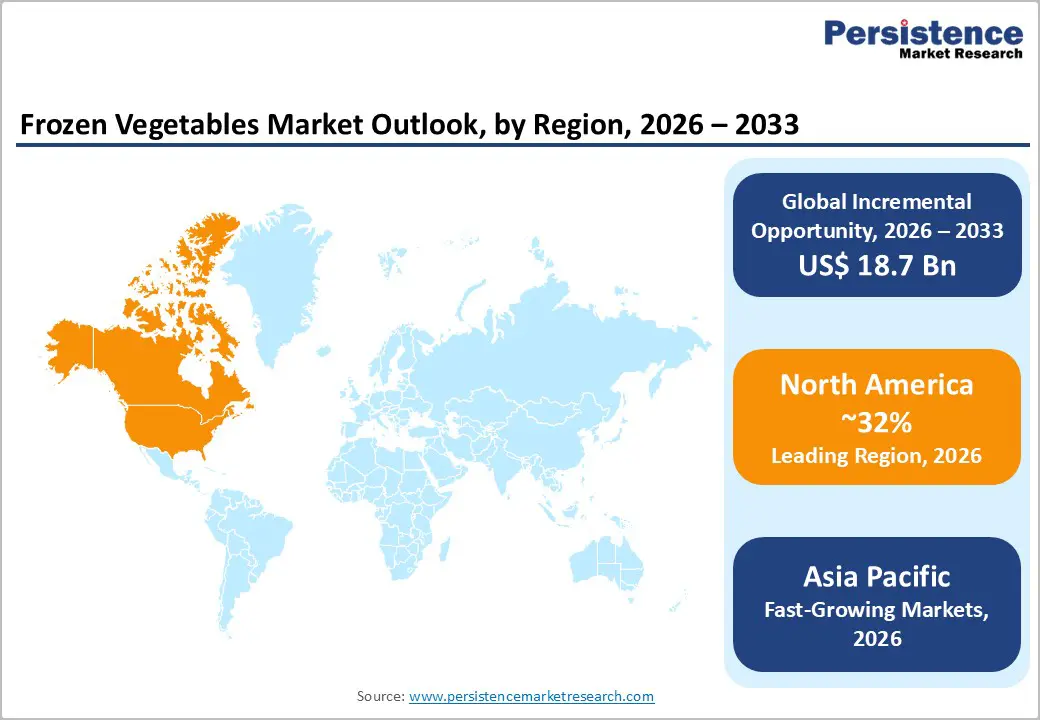

- Leading Region: North America, holding ~32% market share, driven by advanced cold-chain infrastructure, high convenience demand, and strong consumer trust in food safety standards

- Fastest-Growing Market: Asia Pacific, fueled by urbanization, rising middle-class income, expanding retail infrastructure, and increasing adoption of Western-style convenience diets

- Fastest-Growing Nature Segment: Organic, driven by rising demand for clean-label, pesticide-free, and sustainably sourced frozen food products

- Fastest-Growing Distribution Channel: Online Retail, driven by rapid improvements in cold-chain last-mile delivery and growing digital grocery adoption

- Market Drivers: Increasing demand for convenient, ready-to-cook, and time-saving food solutions among urban and working populations

- Opportunities: Expanding demand for organic and clean-label frozen vegetables aligned with health, sustainability, and premium consumption trends

- Consumer Trends: Rising preference for healthy convenience, with consumers seeking nutrient-retained, minimally processed, and easy-to-prepare vegetable options for everyday meals

- Key Developments: In February 2026, Seneca Foods Corp. acquired Green Giant’s U.S. frozen vegetable business from B&G Foods, strengthening its market position. In October 2025, Apetit Plc acquired Foodhills AB, expanding its footprint in the European frozen foods sector.

| Key Insights | Details |

|---|---|

|

Frozen Vegetables Market Size (2026E) |

US$ 42.9 Bn |

|

Market Value Forecast (2033F) |

US$ 61.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Dynamics

Driver - Rising Demand for Convenience Foods and Ready-to-Cook Ingredients

The growing demand for convenient and time-efficient food solutions is a major driver for the frozen vegetables market, particularly among urban consumers and the expanding global workforce. Busy lifestyles, longer working hours, and the rise in dual-income households are pushing consumers toward products that minimize preparation time without compromising on nutrition. Frozen vegetables address this need by eliminating time-consuming steps like washing, peeling, and chopping, making them highly attractive for quick meal preparation. This convenience factor aligns strongly with the preferences of younger consumers, especially millennials, who seek a balance between health and ease of use in their daily diets.

Additionally, rising disposable incomes and rapid urbanization are reinforcing the shift toward processed and ready-to-use food products. Retailers are responding by expanding frozen food assortments, including regionally inspired and value-added vegetable blends. Continuous improvements in freezing technologies, such as IQF (Individually Quick Frozen), help retain nutrients and texture, further enhancing product appeal. As consumers increasingly prioritize both convenience and quality, frozen vegetables are gaining steady traction across retail and foodservice channels globally.

Restraints - High Energy Dependency and Cold Chain Logistical Constraints

The frozen vegetables market is significantly constrained by its heavy reliance on energy-intensive processing and cold chain infrastructure. From rapid-freezing technologies such as IQF to refrigerated storage and transportation, maintaining consistent low temperatures throughout the supply chain is critical to preserving product quality and safety. This dependence on a continuous energy supply increases operational costs, particularly in regions with volatile electricity prices or underdeveloped infrastructure. Additionally, cold chain disruptions during transit or storage can lead to product spoilage, financial losses, and reduced shelf life. Emerging markets face greater challenges due to limited refrigerated logistics networks and higher capital investment requirements. As sustainability concerns rise, the sector also faces pressure to reduce energy consumption and carbon emissions, pushing companies to invest in energy-efficient technologies and optimized distribution systems.

Opportunity - Surging Demand for Organic and Clean-Label Frozen Produce

The rising consumer shift toward organic and clean-label food products is creating a strong growth opportunity for the global frozen vegetables market. Increasing awareness around pesticide residues, food safety, and long-term health impacts is encouraging consumers to opt for certified organic produce with minimal processing. Frozen vegetables positioned as clean-label, free from additives, preservatives, and artificial ingredients are gaining traction, particularly among health-conscious urban populations. This trend is further supported by regulatory bodies promoting transparency in food labeling and sustainable agricultural practices.

At the same time, advancements in freezing technologies are enabling manufacturers to preserve the nutritional integrity of organic vegetables without compromising quality. Retailers are expanding premium organic frozen ranges, while private labels are entering the segment with competitively priced offerings. The growing popularity of plant-based diets and sustainable consumption patterns is also reinforcing demand, positioning organic frozen vegetables as a high-value, future-ready category within the broader frozen foods market.

Category-wise Analysis

Nature Insights

The conventional segment continues to dominate the global frozen vegetables market, accounting for approximately 83% share in 2025. Its strong position is primarily driven by affordability, consistent supply, and widespread availability across supermarkets and mass retail channels. Conventional frozen vegetables are widely preferred by price-sensitive consumers, institutional buyers, and foodservice operators due to their cost efficiency and scalability. Their compatibility with large-scale processing and established supply chains further strengthens their role as the backbone of volume-driven market growth.

Furthermore, the organic segment is emerging as the fastest-growing category, driven by rising consumer awareness of food safety and chemical-free agriculture. Organic frozen vegetables are gaining traction among health-conscious consumers seeking clean-label and sustainably sourced products. Market trends indicate rising investments in certified organic farming and premium product positioning. Opportunities are expanding through private labels, specialty retail, and export markets, as brands focus on transparency, traceability, and eco-friendly packaging to capture higher-value segments globally.

Form Insights

Supermarkets and hypermarkets dominate the distribution landscape for frozen vegetables, supported by extensive freezer infrastructure, strong brand visibility, and high consumer footfall. These outlets offer a wide assortment of international brands alongside competitive private-label options, enabling price differentiation and broad consumer reach. Their ability to maintain consistent product quality and availability makes them the preferred channel for everyday household purchases across developed and emerging markets.

At the same time, the B2B channel remains a significant contributor to volume, driven by demand from foodservice operators, quick-service restaurants, and institutional catering. Online retail is emerging as the fastest-growing segment, supported by advancements in cold-chain logistics and last-mile delivery solutions. Specialty stores are also gaining traction by focusing on organic, premium, and niche product ranges. Globally, opportunities are expanding across these channels as companies invest in digital platforms, bulk supply agreements, and differentiated product offerings to capture evolving consumption patterns.

Regional Insights

North America Frozen Vegetables Market Trends and Insights

North America is the globally leading region accounted for a 32% share in 2025. The region's leadership is underpinned by a highly mature cold-chain infrastructure and a massive consumer base in the United States and Canada that prioritizes convenience and food safety. The U.S. Food and Drug Administration (FDA) maintains rigorous safety standards, which has fostered high consumer trust in frozen brands like Conagra Brands Inc. and J.R. Simplot Co.

Innovation is currently focused on value-added frozen vegetables, such as pre-seasoned stir-fry kits and steam-in-bag technology. There is a notable trend toward the snackification of vegetables, with products like frozen edamame and corn bits gaining traction. Furthermore, the strong presence of major market players ensures a high level of research and development in sustainable packaging. The high disposable income and the established habit of bulk-buying at club stores such as Costco maintain North America as the primary engine for global market value and technological breakthroughs.

Asia Pacific Frozen Vegetables Market Trends and Insights

Asia Pacific is identified as the fastest-growing segment for the frozen vegetables market through 2033. This rapid expansion is primarily driven by the burgeoning middle class in China, India, and ASEAN countries, who are increasingly adopting Western-style convenience diets. The rising awareness of food hygiene and the modernization of the retail sector are major trends in the region. China is a major global player, not only as a massive consumer but also as a leading exporter of frozen Corn and Carrots.

The region also benefits from significant manufacturing advantages and lower raw-material costs. In India, the government's focus on reducing post-harvest losses has led to the establishment of Mega Food Parks with integrated cold storage facilities, significantly boosting the capacity of local players such as ITC Limited. The rapid expansion of modern retail and the massive reach of e-commerce platforms like Alibaba and BigBasket have made premium frozen vegetable brands more accessible to a wider demographic. As Asian diets incorporate more frozen ingredients into traditional stir-fries and curries, the Asia Pacific region is poised to become the global hub for both production and consumption.

Competitive Landscape

The frozen vegetables market reflects a moderately consolidated competitive structure, where global food conglomerates and specialized processors maintain strong control over supply chains and distribution networks. Leading players leverage vertical integration spanning farm sourcing, processing, and global logistics to ensure consistent quality and cost efficiency. Competitive strategies are centered on geographic expansion, advancements in freezing technologies such as IQF, and acquisitions to strengthen raw material access in key agricultural regions. At the same time, regional markets remain dynamic, supported by private-label brands and niche organic producers targeting premium and health-focused consumers. Product quality consistency, rapid freezing capabilities, and compliance with food safety and sustainability certifications are key differentiators. Increasing emphasis on traceability, farm-to-fork transparency, and flexible supply partnerships is reshaping competition as companies adapt to evolving consumer expectations.

Key Developments:

- In February 2026, Seneca Foods Corp. acquired the Green Giant U.S. frozen vegetable business from B&G Foods, strengthening its position in the frozen foods segment.

- In October 2025, Apetit Plc acquired 100% shares of Foodhills AB, expanding its footprint in the European frozen foods market.

- In October 2025, Farmton Foods signed an MoU with the Government of Gujarat during Vibrant Gujarat to invest INR580 crore in a greenfield frozen potato processing facility.

Companies Covered in Frozen Vegetables Market

- Conagra Brands Inc.

- Ajinomoto Co., Inc.

- General Mills Inc.

- ITC Limited

- Uren Food Group Limited

- Greenyard NV

- J.R. Simplot Co.

- The Kraft Heinz Company

- Nature’s Garden

- Ardo

- Goya Foods Inc.

- Others

Frequently Asked Questions

The global Frozen Vegetables market is projected to be valued at US$ 42.9 Bn in 2026.

Rising Demand for Convenience Foods and Ready-to-Cook Ingredients is a major factor driving the global Frozen Vegetables market.

The Global Frozen Vegetables market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Surging Demand for Organic and Clean-Label Frozen Produce is a significant opportunity in the Frozen Vegetables market.

Major players in the Global Frozen Vegetables market include Conagra Brands Inc., Ajinomoto Co., Inc., General Mills Inc., ITC Limited, Uren Food Group Limited, and others.