- Processed Food

- Frozen Seafood Market

Frozen Seafood Market Size, Share, and Growth Forecast, 2026 – 2033

Frozen Seafood Market by Product Type (Shrimp & Prawns, Fish Fillets, Crab & Lobster, Squid & Octopus, Scallops, Others), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Retail, Foodservice, Others), End-User (Household, Foodservice Sector), and Regional Analysis for 2026-2033

Frozen Seafood Market Share and Trends Analysis

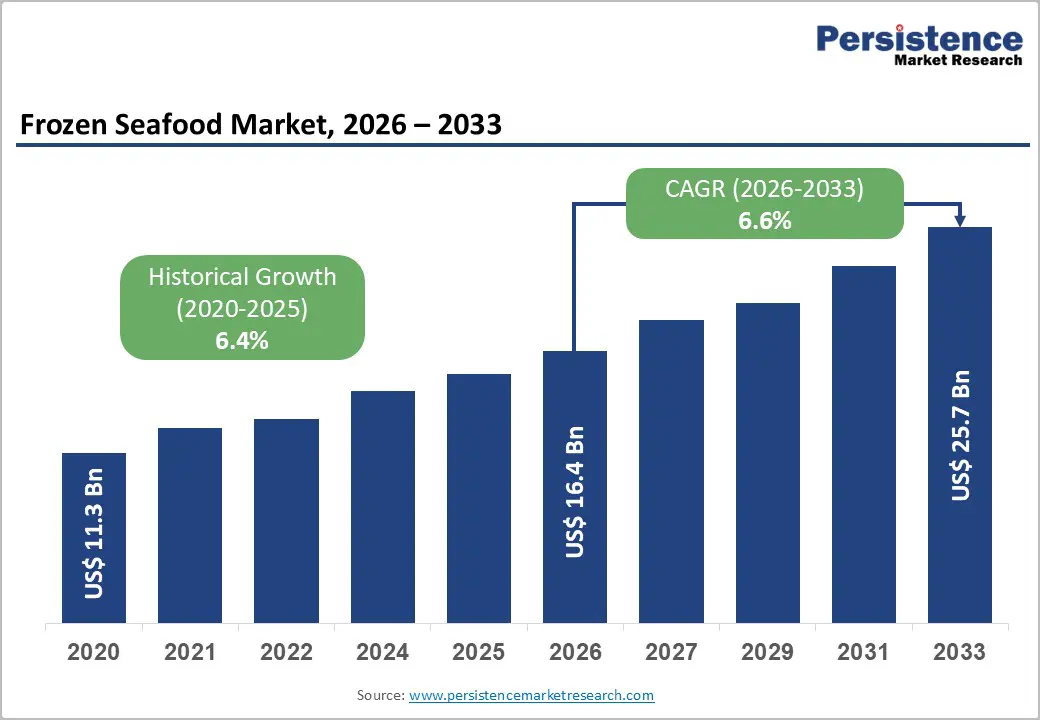

The global frozen seafood market size is likely to be valued at US$ 16.4 billion in 2026, and is projected to reach US$ 25.7 billion by 2033, growing at a CAGR of 6.6% during the forecast period 2026−2033. Market expansion reflects sustained structural shifts in food consumption toward protein security, supply stability, and convenience-driven nutrition. Accelerating urbanization, rising workforce participation, and time-constrained lifestyles increase reliance on frozen protein formats that balance extended shelf life with nutritional integrity.

Population aging and heightened chronic disease awareness elevate preference for lean protein sources, positioning seafood as a clinically accepted dietary component. Institutional endorsement from food safety authorities reinforces confidence in frozen preservation as a method that maintains micronutrient quality while reducing spoilage risk. Concurrent technological integration across cold-chain logistics, rapid freezing processes, and advanced packaging innovations enhances texture retention, flavor stability, and product traceability, translating into broader consumer acceptance across income segments.

Key Industry Highlights

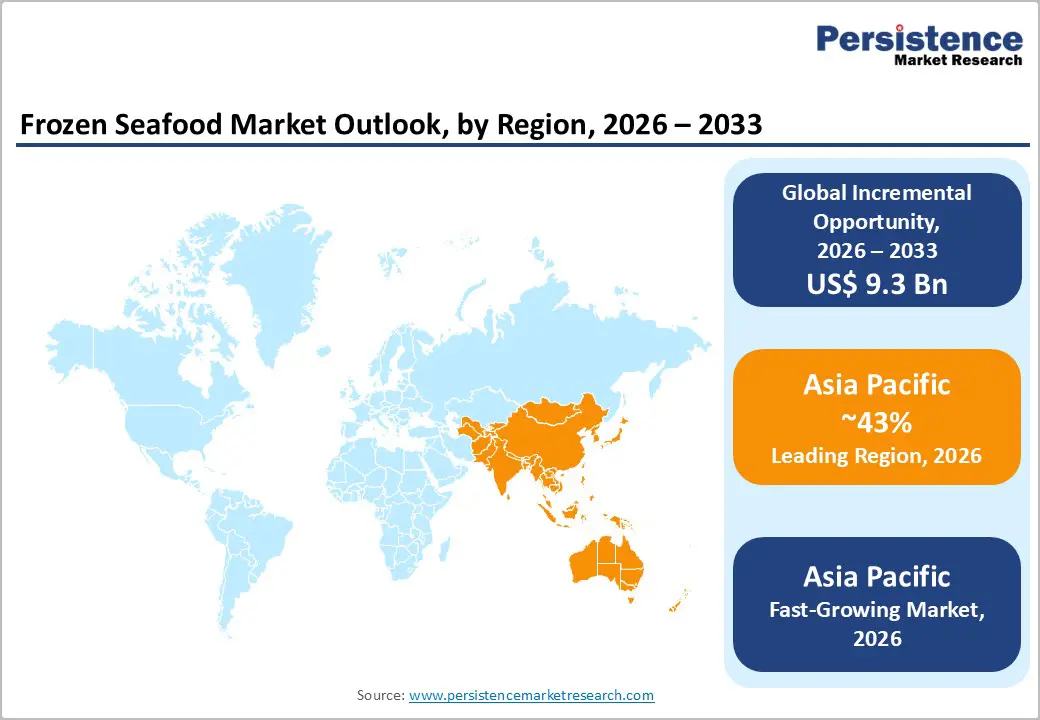

- Dominant Region: Asia Pacific is projected to dominate in 2026 with around 43% market share, driven by a well-routinized seafood consumption culture.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market between 2026 and 2033, fueled by foodservice expansion, export-focused processing upgrades, and government-led cold-chain development.

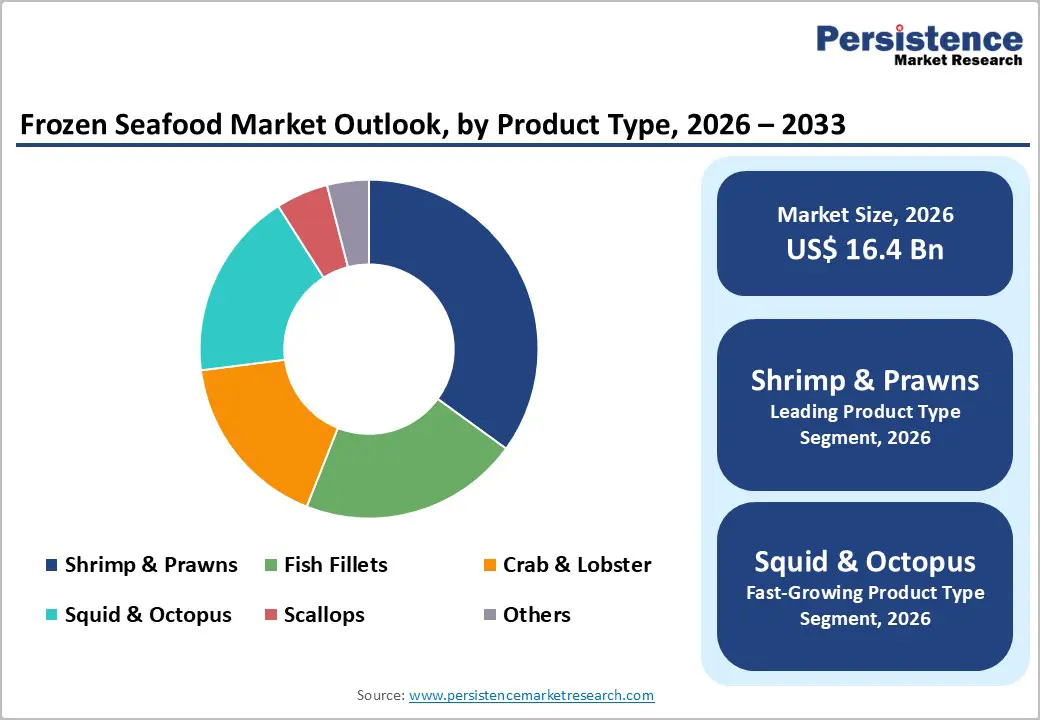

- Leading Product Type: Shrimp and prawns are expected to hold about 35% revenue share in 2026 due to wide culinary acceptance, reliable aquaculture supply, and favorable nutritional profile.

- Fastest-growing Product Type: Squid and octopus are expected to be the fastest-growing segment during 2026–2033, supported by premium menu positioning and advances in freezing and tenderization.

- January 2026: Nissui announced plans to launch three new microwave-ready frozen fish dishes across Japan that can be heated directly for home meals, targeting time-pressed consumers.

| Key Insights | Details |

|---|---|

| Frozen Seafood Market Size (2026E) | US$ 16.4 Bn |

| Market Value Forecast (2033F) | US$ 25.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Cold-Chain Infrastructure and Food Safety Regulation Alignment

Infrastructure-led transformation underpins demand growth by converting frozen distribution from a risk-managed activity into a standardized, scalable food system. Public investment in temperature-controlled storage, refrigerated transport, and monitoring nodes reduces quality volatility across harvest cycles and long-distance trade routes. This structural reliability supports year-round availability, stabilizes pricing, and limits physical degradation that historically constrained consumer trust. India government disclosures confirm that 291 integrated cold-chain projects were operational by mid-2025, creating 25.52 lakh metric tonnes of preservation capacity, reflecting sustained public commitment to national cold logistics under formal policy frameworks. Such scale embeds cold handling as a default requirement rather than a premium feature, enabling processors and distributors to plan volumes with predictable loss profiles and higher asset utilization.

Regulatory alignment magnifies infrastructure impact by converting technical capacity into commercial legitimacy. Food safety authorities mandate documented temperature integrity, hygiene protocols, and traceability records across storage and transit stages, which narrows execution gaps across regions and operators. Uniform compliance standards reduce enforcement ambiguity, improve audit efficiency, and lower transaction friction for institutional buyers, export channels, and organized retail. Regulatory certainty encourages capital allocation toward compliant facilities, digital temperature logging, and certified transport fleets, strengthening operational discipline across the value chain. Consistent enforcement elevates confidence among healthcare professionals, public procurement agencies, and urban consumers who prioritize nutritional integrity and contamination control.

Dietary Protein Transition and Preventive Nutrition Awareness

Dietary protein transition reflects a strategic recalibration of nutrition priorities toward long-term health preservation and risk mitigation. Preventive nutrition frameworks promoted by government health authorities emphasize adequate intake of high-quality protein to support metabolic balance, functional mobility, and immune resilience across age groups. National dietary guidance released in 2025 by a federal authority positions seafood within recommended dietary patterns due to favorable nutrient density and alignment with chronic disease prevention objectives. Policy narratives increasingly link protein quality with healthy aging, workforce productivity, and reduction of nutrition-related public health strain. This institutional framing elevates protein selection from preference-driven choice to outcome-oriented nutrition planning, reinforcing demand for reliable, standardized protein sources that align with official guidance and food safety protocols.

Preventive nutrition awareness influences purchasing behavior toward formats that support consistency, safety, and nutritional assurance under modern consumption constraints. Frozen preservation aligns with government-endorsed food safety practices, reinforcing confidence in nutrient retention, portion accuracy, and contamination control across distribution channels. Public sector emphasis on balanced protein intake supports integration of seafood into routine diets, while frozen formats enable accessibility across urban and semi-urban populations facing time constraints and supply variability. Structured endorsement from dietary authorities strengthens perception of frozen seafood as a practical solution within preventive nutrition strategies rather than a secondary alternative to fresh options.

Mounting Quality Degradation Concerns

The inherent susceptibility of frozen seafood to sensory and compositional changes during storage and handling presents tangible challenges for value chain operators and buyers. Ice crystals that form during freezing can disrupt the microscopic architecture of muscle tissues, leading to moisture loss and weakened texture upon thawing. Oxidative reactions affecting lipids and proteins continue at low temperatures, which degrades flavor profiles and diminishes levels of health-related nutrients such as omega-3 fatty acids. Inconsistent temperature control during distribution amplifies these changes, creating variability in quality that complicates inventory management and undermines shelf-life projections.

Government oversight activity in 2025 illustrates how quality concerns extend into compliance and enforcement risk. In a sampling and testing assignment conducted between 2022 and 2024, the U.S. Food and Drug Administration (FDA) found that 36% of frozen seafood product samples tested violated net weight declaration standards due to unacceptable inclusion of water glaze as part of declared weight, a practice that misrepresents edible yield and falls short of regulatory requirements. This regulatory finding underscores challenges in maintaining accurate product specification, reinforces scrutiny on handling protocols, and contributes to procurement caution among institutional and commercial buyers.

High Energy and Storage Costs

High energy and storage costs act as a critical restraint due to the inherently energy-intensive nature of frozen food preservation across the value chain. Continuous refrigeration is required from processing and blast freezing through warehousing, transportation, and retail display, with no tolerance for temperature deviation. Electricity dependency remains persistent and non-discretionary, converting energy expenditure into a fixed operating cost rather than a variable one. Exposure to power tariff revisions, fuel price movements for backup generation, and grid instability elevates cost volatility and limits margin flexibility. Storage operators face compounding pressure as energy efficiency gains often demand upfront capital investment in advanced compressors, insulation systems, and monitoring technologies, extending payback periods and constraining return profiles.

Storage infrastructure further amplifies cost pressure through capital intensity and operational rigidity. Facilities must be designed for precise temperature control, redundancy, and regulatory compliance, resulting in higher construction, maintenance, and compliance expenses compared to ambient food storage. Utilization risk remains material, as under-occupied cold storage capacity still incurs full energy and maintenance costs. Smaller processors and distributors encounter barriers to scale participation due to limited access to capital and financing for energy-efficient upgrades. Cost escalation ultimately transmits downstream, influencing pricing decisions and limiting affordability across price-sensitive consumer segments.

Rising Demand from Foodservice and Hospitality Sectors

Rising demand from foodservice and hospitality sectors creating an opportunity is reflected in sustained growth across full-service restaurants, limited-service outlets, hotels, and institutional dining channels, which require standardized, high-quality protein inputs that ensure reliability in sourcing, storage, and preparation. Government data shows that total spending at foodservice outlets in the United States reached USD 1.52 trillion in 2024, representing a record high share of consumer food expenditures on food prepared away from home. Frozen seafood aligns with these operational priorities through extended shelf stability, consistent portion control, and reduced waste, supporting margin protection in high-volume kitchens. Menu planning benefits from the ability to offer diverse seafood options without exposure to freshness volatility or supply seasonality, strengthening long-term procurement alignment with hospitality operators.

Large foodservice and hospitality groups emphasize supply chain efficiency, predictable quality, and scalability to manage fluctuating demand patterns. Frozen seafood formats leverage advanced freezing technologies and integrated cold-chain systems that preserve texture and micronutrient integrity, meeting quality benchmarks across premium and value-oriented dining formats. Institutional buyers including hotels, resorts, corporate cafeterias, and healthcare facilities continue to integrate seafood into meal programs based on nutritional suitability and operational convenience.

Technological Advancements in Freezing and Packaging

Rapid improvement in freezing and packaging stands out as a core opportunity because it directly supports product integrity, regulatory compliance, and supply chain resilience in line with public sector preservation guidelines. Government-level food safety frameworks emphasize that proper low-temperature preservation paired with protective packaging slows microbial activity and enzymatic degradation while maintaining texture and nutrient profile throughout distribution, storage, and retail display. High-quality freezing methods significantly reduce the risk of spoilage and food safety incidents, supporting adherence to internationally recognized standards such as those outlined by the United Nations Food and Agriculture Organization (FAO) and national food safety authorities. These improvements build buyer and retailer confidence by aligning product handling with documented safety protocols and critical control point management practices promoted by regulators.

Investment in advanced freezing systems and innovative packaging solutions yields business value by enhancing consistency and reducing operational losses across the value chain. Rapid and uniform freezing minimizes structural damage at the cellular level, preserving sensory attributes that influence repeat purchase decisions, while modern packaging materials with superior barrier properties protect against oxygen and moisture ingress that accelerates quality decline. Integration of traceability and temperature monitoring technologies strengthens cold chain visibility and supports compliance with government guidelines for controlled environment logistics. Enhanced preservation performance reduces supply chain waste and strengthens access to distribution channels that demand documented handling standards.

Category-wise Analysis

Product Type Insights

Shrimp and prawns are anticipated to secure around 35% of the frozen seafood market revenue share in 2026, reflecting broad culinary acceptance, consistent aquaculture supply, and compatibility with multiple cuisines. This leadership is reinforced by strong clinical acceptance linked to high protein density, low saturated fat content, and favorable amino acid composition, aligning with preventive nutrition trends. Treatment effectiveness is supported by rapid freezing methods that stabilize muscle fibers, preserve flavor compounds, and maintain visual appeal across storage cycles. Provider preference within foodservice operations centers on predictable portion sizing, fast cooking times, and adaptability across fried, grilled, and prepared meal formats. Accessibility benefits from extensive cold-chain penetration in retail and institutional channels, while adherence strengthens through low preparation complexity.

Squid and octopus are expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by diversification of consumer diets and rising interest in premium seafood experiences. Growth momentum is supported by expanding culinary exposure through international cuisines and chef-driven menu innovation that positions cephalopods as high-value offerings. Foodservice adoption accelerates as operators pursue differentiation through texture-rich and visually distinctive dishes. Advances in freezing and tenderization techniques address historical challenges related to toughness, improving consistency and consumer acceptance. Export-oriented processors increase capacity and invest in quality control systems to meet stringent international standards.

End-User Insights

Household are likely to be the leading segment with a projected 60% of the frozen seafood market share in 2026 due to convenience-driven consumption and cost efficiency relative to fresh seafood. Demand strength is supported by lifestyle shifts toward planned home cooking, reduced shopping frequency, and preference for products with predictable quality and extended usability. Clinical credibility associated with frozen preservation reinforces trust in nutritional retention and food safety for routine family consumption. Portion flexibility and reduced preparation time align with time-constrained households and dual-income demographics. Digital retail integration enhances accessibility through app-based grocery platforms, subscription models, and home delivery services, enabling consistent availability across urban and semi-urban areas.

Foodservice sector is anticipated to be the fastest-growing segment from 2026 to 2033, fueled by standardized quality requirements, waste reduction priorities, and technology-enabled inventory management. Growth is reinforced by rising demand for menu consistency across multi-outlet restaurant chains, institutional catering, and hospitality groups. Frozen formats support centralized procurement models by ensuring uniform portioning, stable input costs, and predictable cooking outcomes. Waste minimization aligns with margin optimization strategies, as frozen products reduce spoilage and over-preparation risks. Integration of digital inventory systems and demand forecasting tools strengthens stock control and procurement planning.

Regional Insights

North America Frozen Seafood Market Trends

North America demonstrates a structurally mature yet resilient frozen seafood landscape shaped by advanced cold-chain penetration, high regulatory stringency, and premiumization of protein consumption. Consumption patterns emphasize portion control, food safety assurance, and nutritional transparency, aligning strongly with frozen formats that offer consistency and extended usability. Large-scale retail chains and warehouse clubs play a central role by leveraging centralized distribution centers, enabling high inventory turnover and stable pricing. Strong demand for certified, traceable seafood supports uptake of individually quick frozen products with clear origin labeling. Clinical and dietary guidance promoting lean protein intake reinforces household reliance on frozen seafood as a routine meal component rather than an occasional purchase. Processing specialization in value-added formats such as breaded fillets, seasoned portions, and ready-to-cook meal kits differentiates demand from commodity-driven markets.

Growth dynamics are shaped less by volume expansion and more by value optimization and channel diversification. Foodservice recovery and expansion of quick-service and casual dining formats increase demand for frozen inputs that ensure menu consistency and labor efficiency. Sustainability-driven procurement policies elevate preference for responsibly sourced and certified frozen seafood, encouraging suppliers to invest in advanced freezing, glazing control, and digital traceability systems. E-commerce grocery penetration reshapes buying behavior by normalizing bulk frozen purchases supported by reliable last-mile cold delivery. Innovation focuses on packaging formats that extend freezer life while improving convenience, including resealable and microwave-ready solutions.

Europe Frozen Seafood Market Trends

Europe represents a strategically mature and value-focused market shaped by regulatory discipline, consumption sophistication, and premium positioning within frozen protein categories. Demand strength is anchored in high per capita seafood consumption combined with strict food safety and traceability frameworks enforced by public authorities, which favor frozen formats for compliance reliability. Advanced cold-chain penetration across retail and logistics networks supports consistent quality from port to point of sale. Consumer purchasing behavior emphasizes portion control, waste minimization, and certified sourcing, aligning strongly with frozen seafood attributes. Retail private labels play a central role by offering competitively priced, high-quality frozen assortments, reinforcing household adoption. Species specialization such as cod, salmon, haddock, and shellfish supports category stability, while sustainability certifications enhance trust and justify premium pricing.

Growth momentum across Europe is increasingly driven by structural shifts in foodservice and sustainability-led consumption models rather than volume expansion alone. Institutional catering, healthcare facilities, and education systems prioritize frozen seafood to meet nutritional standards while managing cost predictability and inventory control. Restaurant operators rely on frozen inputs to stabilize supply amid tightening wild-catch quotas and seasonal variability. Product innovation focuses on value-added formats including pre-marinated, ready-to-bake, and portioned fillets that reduce labor intensity and preparation time. Sustainability regulation accelerates adoption of frozen formats by extending shelf life and lowering food waste, aligning with circular economy objectives. Expansion of plant-forward diets does not displace seafood demand, as frozen fish remains positioned as a low-impact animal protein.

Asia Pacific Frozen Seafood Market Trends

Asia Pacific is projected to dominate in 2026, commanding approximately 43% of the frozen seafood market share, supported by unmatched production specialization and consumption integration across multiple economies. The area hosts the world’s largest aquaculture production hubs, with countries such as China, India, Vietnam, and Indonesia operating vertically coordinated shrimp and fish farming systems that stabilize supply and pricing. Proximity between farms, processing plants, and export ports shortens freezing cycles, preserving quality while reducing operating costs. Cultural dietary patterns favor seafood as a daily protein rather than an occasional purchase, sustaining baseline demand even during economic fluctuations. Large-scale seafood processing parks equipped with blast freezing and individual quick freezing lines enable high-volume standardized output, supporting both domestic retail and international trade.

Asia Pacific is poised to emerge as the fastest-growing regional market for frozen seafood between 2026 and 2033 due to rapid structural transformation in consumption behavior and distribution capability. Urban expansion and rising female workforce participation increase demand for ready-to-cook proteins that reduce preparation time without compromising nutritional value. Digital grocery platforms in China and Southeast Asia normalize frozen seafood purchases through same-day delivery and subscription models, expanding penetration beyond metropolitan cores. Foodservice chains scale aggressively across emerging cities, relying on frozen inputs to maintain menu consistency and cost control. Export-oriented processors increasingly invest in advanced freezing, glazing, and traceability systems to meet stringent international quality benchmarks, enabling access to higher-value markets. Government-backed cold-chain expansion programs and port modernization accelerate inland distribution efficiency.

Competitive Landscape

The global frozen seafood market exhibits a moderately fragmented structure, shaped by diversity in species sourcing, geographic production bases, and end-use channels rather than concentration around a single dominant supplier. Competitive balance is maintained by the need for multi-origin raw material access, compliance with region-specific food safety regulations, and capital-intensive cold-chain infrastructure. Leading participants such as Thai Union Group PCL, Maruha Nichiro Corporation, Mowi, Nomad Foods, and High Liner Foods Inc hold strong positions within selected categories and geographies, yet global supply remains distributed across numerous regional and mid-sized processors.

Competitive positioning depends heavily on sourcing scale, processing efficiency, and brand presence across retail and foodservice channels. Thai Union Group PCL and Maruha Nichiro Corporation benefit from diversified species portfolios and vertically integrated processing networks that stabilize input availability. Mowi leverages controlled aquaculture systems to ensure consistency and traceability in premium frozen fish segments. Nomad Foods and High Liner Foods Inc strengthen market standing through brand-led strategies, private label partnerships, and value-added product innovation tailored to consumer convenience trends. Investment focus centers on freezing technology upgrades, yield optimization, and packaging formats that support portion control and shelf stability. Absence of a single dominant global supplier sustains competitive intensity, encourages regional specialization, and supports continuous innovation.

Key Industry Developments

- In January 2026, High Liner Foodservice introduced a new line of fully cooked frozen seafood products designed to simplify kitchen operations and meet growing demand for convenient, high-quality menu solutions. The launch expands the company’s frozen seafood portfolio and supports foodservice operators with ready-to-serve options that enhance speed of service and consistency.

- In September 2025, Birds Eye expanded its frozen food range with new prawn products and a selection of “fakeaway” items that offer convenient, take-away-style meals for consumers. The launch is aimed at broadening the brand’s appeal in the frozen category while responding to demand for accessible, meal-solution options.

- In September 2025, Tesco introduced 15 new own-brand and several branded frozen seafood products across its UK stores as part of a major frozen food refresh designed to enhance convenience and meet rising consumer demand for quality frozen seafood options.

Companies Covered in Frozen Seafood Market

- Thai Union Group PCL.

- Maruha Nichiro Corporation

- Mowi

- Nomad Foods

- High Liner Foods, Inc.

- Trident Seafoods

- PESCANOVA

- Dongwon Group

- Clearwater Seafoods

- Lerøy.

- Avanti Feeds Limited.

- Cooke Aquaculture

Frequently Asked Questions

The global frozen seafood market is projected to reach US$ 16.4 billion in 2026.

Rising demand for convenient, long-shelf-life protein, expanding cold-chain infrastructure, urban lifestyle shifts, and increasing confidence in frozen preservation for nutritional quality and food safety are driving the market.

The market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Increasing adoption of advanced freezing and packaging technologies, expansion of cold-chain logistics, growth of digital grocery platforms, and surging demand for value-added seafood formats are creating key market opportunities.

Some of the key market players include Thai Union Group PCL, Maruha Nichiro Corporation, Mowi, Nomad Foods, High Liner Foods Inc., and Trident Seafoods.