- Food Ingredients & Additives

- Food Grade Cellulose Market

Food Grade Cellulose Market Size, Share, and Growth Forecast 2026 - 2033

Food Grade Cellulose Market by Product Type (Microcrystalline Cellulose (MCC), Carboxymethyl Cellulose (CMC), Hydroxypropyl Methylcellulose (HPMC), Methylcellulose (MC), others), by Species/End Use (Food & Beverages, Pharmaceuticals & Nutraceuticals, Food Processing, others), by Regional Analysis, 2026-2033

Food Grade Cellulose Market Size and Trend Analysis

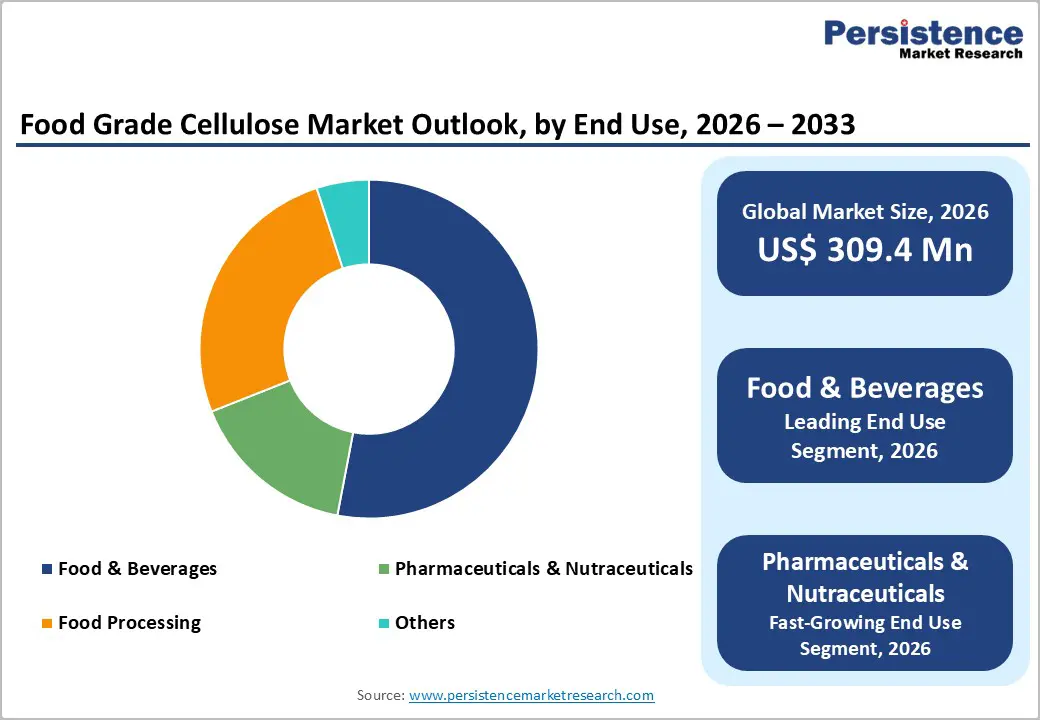

The global Food Grade Cellulose market size is expected to be valued at US$ 309.4 million in 2026 and projected to reach US$ 421.1 million by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

The market's upward trajectory is primarily driven by the increasing consumer pivot toward high-fiber, clean-label diets and the expanding utility of cellulose derivatives in plant-based food formulations. As global regulatory bodies like the European Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA) emphasize the safety and nutritional benefits of dietary fiber, manufacturers are integrating these derivatives to enhance texture and stability. Furthermore, the rising demand for low-fat and gluten-free products in developed regions reinforces the market’s stability, as these additives provide essential structural properties without adding caloric value.

Key Industry Highlights

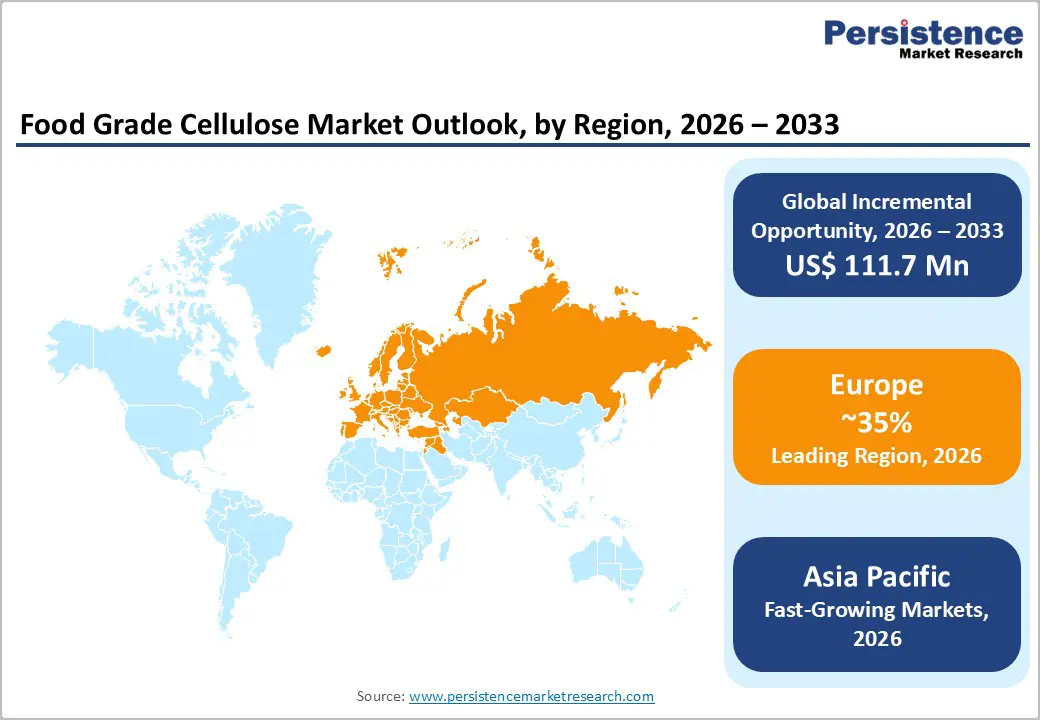

- Leading Region: Europe, holding around 35% market share, supported by strict EFSA regulations, early clean-label adoption, and strong demand for functional, plant-based foods across bakery, dairy, and beverage applications.

- Fastest-Growing Region: Asia Pacific, driven by rapid urbanization, expansion of processed food consumption, and surging pharmaceutical manufacturing in China and India, particularly for MCC-based excipients.

- Fastest-Growing Product Type Segment: Microcrystalline Cellulose (MCC), fueled by its dual role as a food texturizer and the gold-standard excipient for tablets, capsules, and nutraceutical delivery systems.

- Market Drivers: Rising demand for clean-label, fiber-enriched formulations positions cellulose as a preferred plant-based stabilizer, thickener, and bulking agent across food, beverage, and health-focused products.

- Opportunities: Expansion of pharmaceutical-grade and nutraceutical cellulose grades, supported by tightening excipient safety guidelines and growing supplement consumption among aging and health-conscious populations.

- Key Developments: In October 2025, Ashland appointed Tilley Distribution as its exclusive U.S. partner for food and beverage ingredients, strengthening domestic reach. In May 2025, Oji Holdings acquired a stake in India-based Chemfield Cellulose, reinforcing its position in high-growth MCC manufacturing.

| Global Market Attributes | Key Insights |

|---|---|

| Global Food Grade Cellulose Market Size (2026E) | US$ 309.4 Mn |

| Market Value Forecast (2033F) | US$ 421.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver – Growing Demand for Clean-Label and Health-Conscious Food Formulations

The global shift toward "clean-label" products is a definitive driver for the Food Grade Cellulose Market. Modern consumers increasingly scrutinize ingredient lists, seeking recognizable, plant-based additives over synthetic alternatives. Cellulose, being a naturally occurring polymer found in plant cell walls, aligns perfectly with this trend. It serves as a multi-functional ingredient—acting as a thickener, stabilizer, and anti-caking agent—which allows manufacturers to simplify their labels. According to the World Health Organization (WHO), increasing dietary fiber intake is critical for combating non-communicable diseases, leading to a surge in fiber-fortified breads and snacks. Companies such as IFF and Roquette Frères are capitalizing on this by offering high-purity cellulose powders that meet the stringent requirements of health-conscious demographics.

Restraints – Competition from Synthetic Hydrocolloids and Alternative Fibers

While cellulose is a natural powerhouse, it faces stiff competition from other hydrocolloids such as xanthan gum, guar gum, and modified starches, which may offer superior cost-efficiency in specific applications. In the dairy and beverage industries, some synthetic stabilizers provide better clarity and suspension properties at lower inclusion rates. Furthermore, the rising popularity of other dietary fibers, such as chicory root inulin or oat fiber, challenges the market share of Microcrystalline Cellulose (MCC) in the nutraceutical sector. Manufacturers must constantly innovate to demonstrate the unique functional advantages of cellulose such as its superior heat stability and inertness to prevent substitution by these evolving alternative ingredient technologies.

Opportunity – Expansion of Pharmaceutical-Grade Excipients and Nutraceutical Delivery Systems

The Pharmaceuticals & Nutraceuticals segment represents the fastest-growing end-use category, offering immense potential for high-margin expansion. Food-grade cellulose, particularly MCC, is the "gold standard" binder and disintegrant in tablet manufacturing due to its exceptional compressibility and chemical purity. As the global geriatric population increases and the demand for daily supplements surges in Asia Pacific, pharmaceutical giants are seeking high-purity excipients that ensure consistent drug release. The European Medicines Agency (EMA) has updated several guidelines regarding excipient safety, favoring the bio-inert properties of cellulose. Companies like Sigachi Industries and Shin-Etsu Chemical Co., Ltd. are investing in specialized production lines to meet these pharmaceutical-grade standards, positioning themselves to capture this high-value demand.

Category-wise Analysis

Product Type Analysis

The Microcrystalline Cellulose (MCC) segment currently leads the market, accounting for a dominant share due to its ubiquitous presence in both the food and pharmaceutical industries. MCC is prized for its ability to act as a fat replacer and texture enhancer in dairy products and bakery goods without affecting flavor profiles. Its physical properties high porosity and surface area make it an ideal carrier for flavors and active nutrients. In 2025, this segment held a commanding position because it serves as a bridge between basic food stabilization and advanced medicinal delivery. The justification for its leadership lies in its diverse functionality; it can provide creaminess to low-fat dressings while simultaneously serving as a flow aid in powdered seasoning mixes. The reliability of MCC has made it a staple in the formulations of global food leaders like Nestlé and Kraft Heinz.

End Use Analysis

The Food & Beverages segment is the leading end-use category, holding a 53% market share in 2025. This dominance is fueled by the widespread application of cellulose in dairy alternatives, frozen desserts, and processed meats. In the dairy sector, cellulose is essential for preventing ice crystal formation and maintaining a smooth mouthfeel. Furthermore, in the bakery industry, it is used to manage moisture and improve the structural integrity of gluten-free breads. The segment's leadership is reinforced by the massive scale of the global processed food industry, which consumes thousands of tons of CMC and MCC annually to ensure product consistency during long-distance shipping and extended shelf storage. As convenience food consumption rises in urban centers, the demand for these stabilizers remains the primary engine of the market's value.

Region-wise Insights

North America Food Grade Cellulose Market Trends and Insights

North America remains a critical hub for innovation and consumption in the Food Grade Cellulose Market. The United States leads the region, driven by a highly mature food processing industry and a robust regulatory framework overseen by the FDA. A key trend in this region is the rapid adoption of cellulose in "keto-friendly" and "low-carb" products, where it serves as a non-caloric bulking agent to replace flour or sugar. The innovation ecosystem in North America is characterized by heavy investment in biotechnology; for example, companies like IFF are developing enzymatic processes to produce high-purity cellulose from non-traditional plant sources.

Furthermore, the U.S. market is seeing a significant shift toward pharmaceutical-grade cellulose as domestic drug manufacturing increases. The presence of major nutraceutical brands and a health-conscious population that prioritizes high-fiber diets ensures a steady demand for MCC and HPMC. The regional dynamics are also influenced by the growing demand for sustainable food systems, leading to the integration of cellulose-based materials in biodegradable food service ware and secondary packaging, aligning with both corporate sustainability goals and consumer preferences.

Europe Food Grade Cellulose Market Trends and Insights

Europe is the leading regional market, holding a 35% market share in 2025. This leadership is a result of the region's early and aggressive adoption of clean-label standards and strict regulatory oversight by the EFSA. Countries like Germany, France, and the United Kingdom have some of the world's highest per-capita consumption rates of functional and plant-based foods. European manufacturers are at the forefront of "regulatory harmonization," ensuring that cellulose derivatives meet the highest safety benchmarks for "E-number" additives (E460 to E466).

The European market is also characterized by a strong emphasis on sustainability and the "farm-to-fork" strategy. Major players like Roquette Frères and Lamberti S.p.A. are focusing on reducing the environmental footprint of cellulose production by sourcing raw materials from certified sustainable forests. The demand for CMC in the European dairy and beverage sectors is particularly high, where it is used to stabilize acidified milk drinks and protein-fortified plant milks. This focus on premium quality and ethical sourcing maintains Europe's status as the most valuable region in the global market.

Asia Pacific Food Grade Cellulose Market Trends and Insights

Asia Pacific is the fastest-growing region in the market, with growth fueled by rapid urbanization and the expansion of the middle class in China, India, and the ASEAN countries. As dietary habits in these nations shift toward Western-style processed foods and "on-the-go" snacks, the demand for food stabilizers and texturizers is skyrocketing. China has emerged as a manufacturing powerhouse for cellulose derivatives, leveraging its vast agricultural base and advanced chemical processing capabilities to meet both domestic and international demand.

The growth dynamics in Asia Pacific are further supported by a burgeoning pharmaceutical sector. India, often referred to as the "pharmacy of the world," is a major consumer of MCC for generic drug production. Local companies like Sigachi Industries are expanding their capacities to cater to the global export market. Additionally, the increasing health awareness among Asian consumers has led to a surge in the consumption of functional beverages and fiber-enriched noodles, providing a significant volume boost to the market.

Market Competitive Landscape

The Food Grade Cellulose Market is characterized by a consolidated structure, where a small group of multinational corporations controls the majority of the market share. These leaders, including IFF, Ashland, and Shin-Etsu, leverage their extensive R&D capabilities and global distribution networks to maintain dominance. Competitive strategies are currently focused on "product differentiation" creating specialized cellulose grades with unique viscosities or solubility profiles for niche applications like high-protein beverages or low-fat bakery fillings. Emerging business models are increasingly prioritizing vertical integration, with companies acquiring pulp suppliers to ensure raw material security. Furthermore, there is a clear trend toward "sustainability-linked branding," where market leaders use their environmental credentials as a key differentiator to win contracts with eco-conscious global food brands.

Key Developments:

- In October 2025, Ashland appointed Tilley Distribution as its exclusive distribution partner for food and beverage ingredients in the United States, strengthening its domestic market reach.

- In May 2025, Oji Holdings Corporation announces that it has acquired shares in Chemfield Cellulose Private Limited, a premier manufacturer of microcrystalline cellulose (MCC) based in India.

- In March 2025, IFF Pharma Solutions highlighted its advanced excipient technologies at CPHI Japan 2025, reinforcing its focus on innovation in pharmaceutical formulation solutions.

- In March 2025, Asahi Kasei Receives Prestigious Okochi Memorial Prize for its Microcrystalline Cellulose (MCC) Ceolus™ UF Grade

Companies Covered in Food Grade Cellulose Market

- IFF

- Ashland

- Lamberti S.p.A.

- Roquette Frères

- Asahi Kasei Corporation

- Kima Chemical Co., Ltd.

- Celotech Chemical Co., Ltd.

- Sigachi Industries

- Shin-Etsu Chemical Co., Ltd.

- Ataman Chemicals

- Others

Frequently Asked Questions

The global market is expected to reach a valuation of US$ 309.4 million by 2026, following a steady recovery and growth in the demand for plant-based stabilizers.

The leading driver is the global consumer shift toward Clean-Label and high-fiber products, which has prompted food manufacturers to utilize natural cellulose as a replacement for synthetic additives.

Europe currently leads the market with a 35% share in 2025, owing to its advanced food processing sector and stringent health and safety regulations.

The expansion into Pharmaceutical-Grade Excipients and the development of Sustainable Packaging are the most promising avenues for generating high-value revenue.

The market is led by global ingredient specialists including IFF, Ashland, Roquette Frères, Shin-Etsu Chemical, and Asahi Kasei Corporation.