- Processed Food

- Ready-to-Eat Food Market

Ready-to-Eat Food Market Size, Share and Growth Forecast, 2026 - 2033

Ready-to-Eat Food Market by Product Type (Ready Meals, Snacks & Savory RTE, Instant Foods, Others), Ingredient Source (Vegetable-Based, Cereal-Based, Meat/Poultry-Based, Others), Packaging Type (Canned, Retort, Others), and Regional Analysis for 2026 - 2033

Ready-to-Eat Food Market Share and Trends Analysis

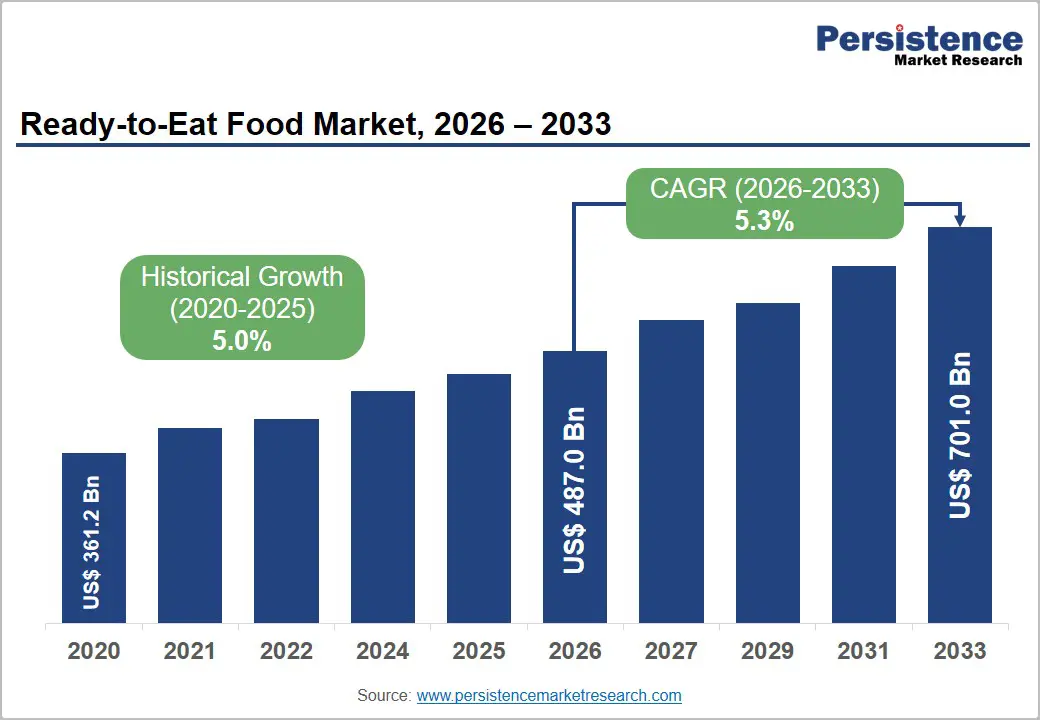

The global ready-to-eat food market size is likely to be valued at US$487.0 billion in 2026 and is projected to reach US$701.0 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026 - 2033, driven by urbanization, rising dual-income households, and growing demand for convenience food industry solutions across both developed and emerging economies.

Advancements in cold-chain logistics and retail infrastructure are improving distribution efficiency and expanding access to packaged, ready meals. Rising health awareness is also driving demand for plant-based ready-to-eat foods, while innovations in retort and frozen packaging are enhancing shelf life and reducing waste. Regulatory oversight from agencies such as the U.S. Food and Drug Administration, European Food Safety Authority, and Food Safety and Standards Authority of India continues to strengthen food safety standards across the market.

Key Industry Highlights:

- Dominant Product Type: Ready meals are set to lead the ready-to-eat food market growth with 30% share in 2026, while plant-based RTE is the fastest growing at 6% CAGR through 2033, driven by rising plant-based ready-to-eat foods demand and health-conscious consumption.

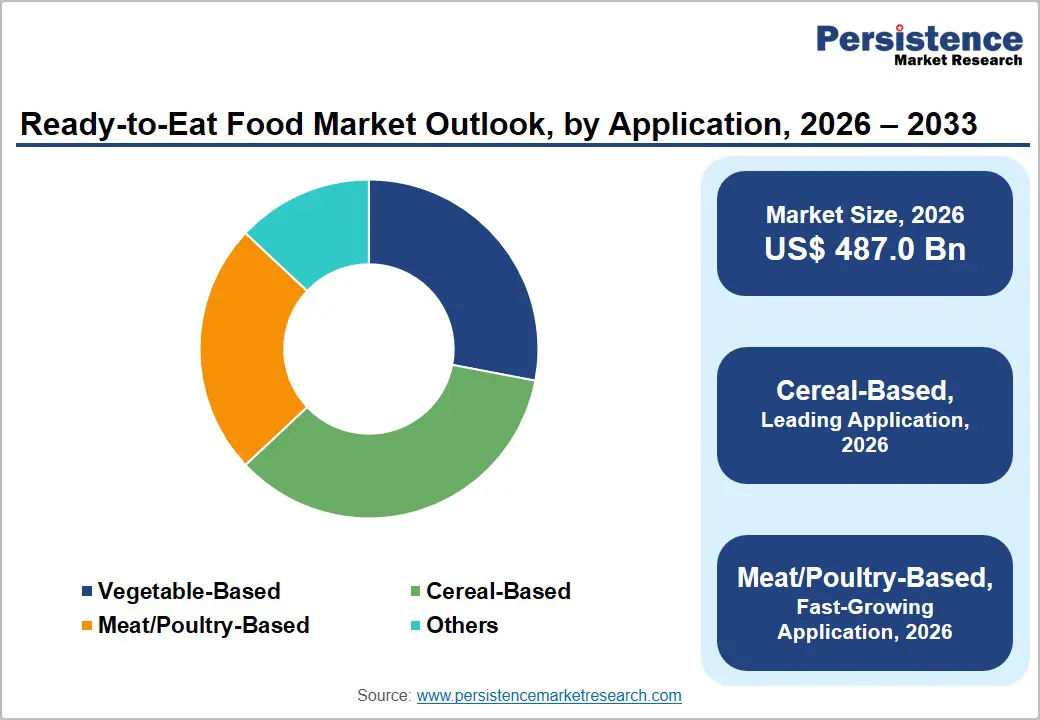

- Ingredient Source Leadership: Cereal-based products will dominate with 35% share in 2026, supported by cost efficiency and widespread use in the instant food market analysis, while meat/poultry-based RTE is the fastest-growing at 6.2% CAGR due to rising protein intake in urban diets.

- Packaging Type Dynamics: Retort packaging is expected to lead with 40% share in 2026, supported by strong shelf stability and retort-packaged food market trends, while frozen/chilled formats are the fastest-growing at 6.5% CAGR, driven by cold-chain expansion and freshness preference.

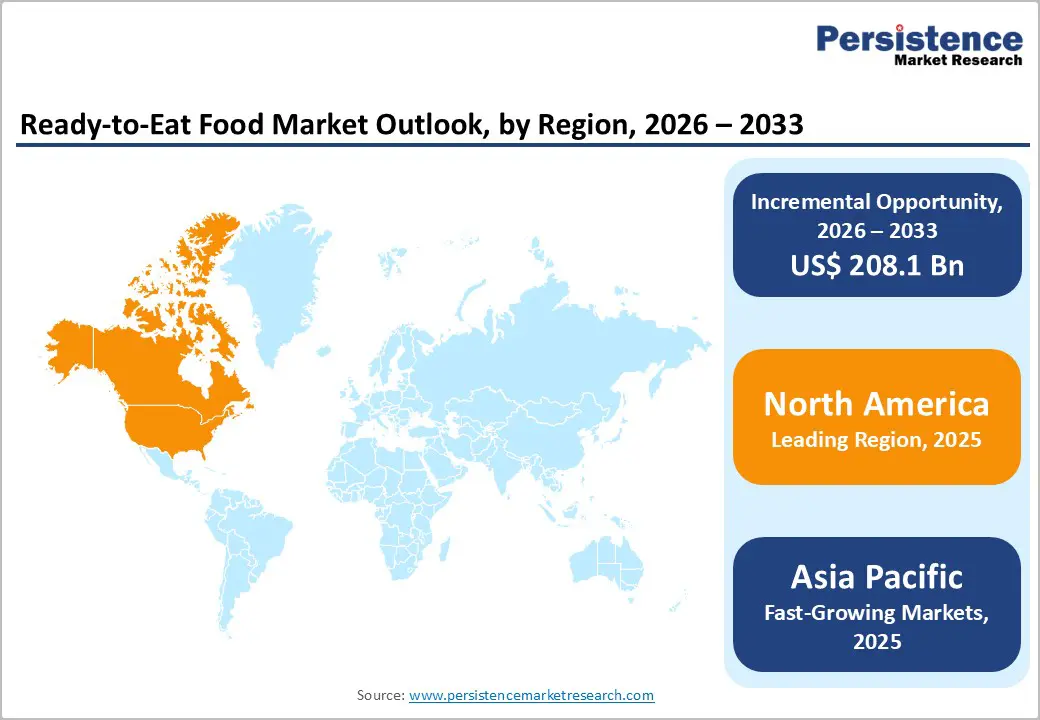

- Regional Leadership: North America is expected to lead with 32% share in 2026, driven by high consumption of packaged meals and strong retail networks, while Asia Pacific is the fastest growing at 6.8% CAGR, supported by urbanization, income growth, and expansion of the convenience food industry.

- Competitive Environment: The market is witnessing consolidation through mergers, capacity expansion, and plant-based product launches, as players compete to strengthen positioning across the global RTE ecosystem.

DRO Analysis

Driver - Urbanization and Demand for Time-Saving Food Consumption Patterns

Rapid urbanization remains the most influential growth driver for the ready-to-eat food market growth trajectory. According to the United Nations Department of Economic and Social Affairs (UN DESA), over 56% of the global population now resides in urban areas, increasing reliance on processed and packaged food formats. Dual-income households, particularly in OECD countries, are driving demand for quick meal solutions such as instant food market analysis products and frozen meals.

The USDA Economic Research Service (ERS) highlights rising consumer expenditure on processed food categories, especially in urban clusters. This structural shift has elevated demand for microwaveable and heat-and-eat formats. As working hours increase and lifestyle patterns evolve, manufacturers are focusing on ready meals innovation with extended shelf life. This trend is significantly strengthening the shelf-stable ready meals industry adoption across supermarkets and online grocery platforms. The result is a sustained, long-term structural uplift in consumption behavior across all major economies.

Restraint - High Processing Costs and Regulatory Compliance Pressure

A key restraint impacting the ready-to-eat food market growth ecosystem is the high cost of processing, preservation, and advanced packaging technologies. Methods such as retort sterilization, freeze-drying, and modified atmosphere packaging significantly raise production expenses. Energy-intensive operations and cold-chain dependency further reduce cost efficiency across value chains. These factors collectively limit scalability, particularly for small and mid-sized manufacturers in price-sensitive markets.

Strict food safety and labeling regulations across major economies add further pressure on manufacturers. Authorities such as the US FDA, EFSA, and FSSAI enforce rigorous hygiene, labeling, and microbial safety standards. This is reinforced by 2025 FDA-led investigations and recalls of ready-to-eat and frozen meals linked to Listeria risks, increasing inspection frequency, and compliance requirements. Additionally, raw material volatility, especially in meat and dairy inputs, heightens operational risk in frozen ready meals market size segments and restricts smooth market expansion.

Opportunity - Expansion of Plant-Based and Sustainable Ready-to-Eat Products

The strongest opportunity lies in the rising demand for plant-based ready-to-eat foods, driven by health awareness, sustainability concerns, and a preference for clean-label convenience meals. Demand is strongest for high-protein plant-based meals and ready-to-heat snacks across urban consumers, aligning with the RTE meals industry trends 2026. This shift is most visible in North America and Europe, where plant-based diets are increasingly replacing traditional meat-based convenience foods.

The industry movements are reinforcing this trend. The American Heart Association’s updated dietary guidance in 2026 encouraged greater reliance on plant-based proteins, strengthening institutional support for meat substitution in daily diets. In addition, major consolidation in the food industry, including Danone’s acquisition of plant-based nutrition brand Huel (2026), reflects rising corporate investment in scalable plant-based RTE solutions. These developments are benefiting global food manufacturers, retail private-label brands, and QSR chains expanding plant-based menus within the convenience food industry.

Category-wise Analysis

Product Type Insights

Ready meals are expected to dominate the ready-to-eat food market growth with 30% share in 2026, driven by rising urban lifestyles and dual-income households. Retail expansion and quick-commerce penetration are improving access to chilled and frozen meal formats across global markets. In 2025, capacity expansions in large European ready-meal production hubs signaled rising industry-scale investment. This is steadily reinforcing volume-led growth across the global convenience food industry.

Plant-based RTE is projected to expand at 6% CAGR, supported by rising health consciousness and sustainability-led consumption shifts. Retailers are steadily increasing plant-based ready meal offerings across mainstream and premium shelves. In 2025-2026, major supermarket expansions of frozen vegan meal lines indicate accelerating mainstream adoption. This is reshaping competitive positioning within the RTE meals industry trends 2026, unlocking strong incremental growth opportunities.

Ingredient Source Insights

Cereal-based RTE is expected to lead with 35% share in 2026, supported by cost-efficiency, long shelf stability, and wide consumer acceptance. Rice, pasta, and grain-based meals continue to anchor mass-market consumption patterns globally. In 2025, the expansion of organic grain-based ready meal portfolios strengthened premium and health-focused retail penetration. This continues to support stable, volume-driven growth in the instant food market analysis.

Meat/poultry-based RTE is anticipated to grow at 6.2% CAGR, driven by rising protein-rich dietary preferences and urban convenience demand. Expansion of chilled and frozen protein meal offerings is improving accessibility across developed and emerging markets. In 2026, new production capacity additions in Asia Pacific for frozen protein snacks and meals are supporting category scaling. This is accelerating momentum in the frozen ready meals market segment.

Packaging Type Insights

Retort packaging is projected to lead with 40% share in 2026, supported by extended shelf life, low refrigeration needs, and strong cost efficiency. It continues to dominate retail, military, and emergency meal applications globally. In 2025, global manufacturers expanded shelf-stable ready meal portfolios to strengthen scalable export networks. This reinforces consistent growth in the retort packaged food market trends, ensuring high distribution efficiency.

Frozen and chilled formats are expected to grow at 6.5% CAGR, driven by cold-chain modernization and rising demand for fresher-tasting convenience meals. Retailers and quick-commerce platforms are rapidly expanding frozen meal assortments in urban markets. In 2025-2026, investments in cold-chain infrastructure across Asia Pacific are improving frozen food accessibility and delivery speed. This is strengthening the shelf-stable ready meals industry, enabling faster premiumization and consumption growth.

Regional Analysis

North America Ready-to-Eat Food Market Trends

North America is estimated to account for 32% of the ready-to-eat food market growth in 2026, supported by high per-capita consumption of convenience meals, strong retail penetration, and advanced cold-chain infrastructure. The region is expected to maintain a stable demand for frozen, chilled, and premium ready meals, driven by established consumption habits and high reliance on processed foods. This continues to support the packaged ready meals market forecast, particularly in urban and suburban households.

U.S. Ready-to-Eat Food Market Trends

The U.S. is estimated to contribute 40% of the regional market in 2026, driven by sustained demand for frozen dinners, meal kits, and ready-to-heat meals. Consumption is expected to remain high due to busy lifestyles and strong retail availability across supermarkets and e-commerce channels. In 2025, Kroger expanded its private-label frozen and ready-to-heat meal range across multiple states, strengthening affordability-driven adoption. This is expected to further reinforce high-volume consumption of convenience meals.

Canada Ready-to-Eat Food Market Trends

Canada is estimated to hold 20% of the regional share in 2026, supported by steady demand for frozen and chilled ready meals among urban households. Consumption is expected to grow gradually due to rising preference for portion-controlled and health-oriented convenience foods. In 2026, Loblaw expanded its President’s Choice ready meal portfolio into high-protein and plant-forward frozen formats, supporting premiumization. This is expected to gradually strengthen the penetration of healthier RTE options.

Europe Ready-to-Eat Food Market Trends

Europe is estimated to contribute 27% of the global market in 2026, driven by strong demand for chilled ready meals, bakery-based convenience foods, and plant-based alternatives. Consumption is expected to remain stable with gradual premiumization, supported by sustainability-focused purchasing behavior. Regulatory frameworks and clean-label preferences are expected to continue shaping the convenience food industry, particularly in Western Europe.

Germany Ready-to-Eat Food Market Trends

Germany is estimated to account for 25% of the European market in 2026, driven by high frozen meal consumption and strong retail penetration. Demand is expected to remain stable, supported by urban working populations and increasing preference for sustainable packaged foods. In 2025-2026, REWE Group expanded its private-label frozen meal range with low-carbon packaging initiatives, aligning with sustainability trends. This is expected to further support eco-friendly product adoption.

U.K. Ready-to-Eat Food Market Trends

The U.K. is estimated to hold 20% of the regional market in 2026, led by strong consumption of chilled ready meals in urban households. Demand is expected to grow steadily, supported by convenience-driven lifestyles and high supermarket dependence. In 2025, Tesco expanded its plant-based chilled ready meal range nationwide, reflecting increasing flexitarian adoption. This is expected to gradually strengthen plant-based penetration in mainstream retail.

Asia Pacific Ready-to-Eat Food Market Trends

Asia Pacific is estimated to be the fastest-growing region in the ready-to-eat food market, supported by rapid urbanization, rising disposable incomes, and evolving dietary preferences. The region is expected to witness strong expansion in instant meals, frozen foods, and affordable convenience products. Growth is further supported by expanding cold-chain infrastructure and digital grocery platforms, strengthening the instant food market analysis outlook.

China Ready-to-Eat Food Market Trends

China is estimated to hold 40% of the regional market in 2026, driven by strong urban demand for packaged and frozen meals. Consumption is expected to grow steadily, supported by busy urban lifestyles and increasing reliance on convenience foods. In 2025, JD.com expanded its cold-chain logistics network for frozen and fresh food delivery across major cities, improving distribution efficiency. This is expected to further strengthen frozen RTE accessibility.

India Ready-to-Eat Food Market Trends

India is estimated to account for 20% of the regional market in 2026, supported by urbanization, rising working populations, and expanding organized retail. Demand for instant meals and frozen snacks is expected to grow rapidly in metro cities. In 2025-2026, Reliance Retail expanded frozen and ready-to-heat private-label meal offerings across its supermarket network, improving affordability and access. This is expected to accelerate mainstream adoption of RTE products in urban households.

Competitive Landscape

The global ready-to-eat food market growth is moderately consolidated, led by players such as Nestlé, Unilever, Conagra Brands, General Mills, and Kraft Heinz. These companies collectively hold a strong share driven by large-scale manufacturing, brand strength, and extensive retail distribution networks. Continuous investment in product innovation, frozen and chilled meal expansion, and premiumization is strengthening their positioning. This reinforces steady dominance across the packaged ready meals market forecast landscape.

Regional and niche players such as McCain Foods, Nomad Foods, ITC, Ajinomoto, and CP Foods are gaining traction through localized offerings and category specialization. Private-label brands are also expanding rapidly, intensifying price competition across retail channels. While high regulatory compliance and cold-chain dependency limit new entrants, e-commerce and digital retail are enabling faster market access. Gradual consolidation is expected through acquisitions and portfolio expansion in the convenience food industry.

Key Industry Developments:

- In March 2026, Unilever’s food business restructuring and merger with McCormick marked a major consolidation move in packaged foods. This strengthened scale efficiencies across seasoning-linked and ready-to-eat categories, reshaping competition in the convenience food industry.

- In May 2025, Chobani acquired Daily Harvest to expand into the ready-to-eat meals segment beyond its core dairy portfolio. This move accelerated its diversification into whole-meal convenience foods, intensifying competition in the ready-to-eat food market growth space.

Companies Covered in Ready-to-Eat Food Market

- Nestlé S.A.

- Unilever PLC

- Kraft Heinz Company

- Conagra Brands Inc.

- General Mills Inc.

- McCain Foods Limited

- Nomad Foods

- Tyson Foods Inc.

- Hormel Foods Corporation

- ITC Limited

- CP Foods

- Ajinomoto Co. Inc.

- Kellogg Company

- BRF S.A.

- Dr. Oetker GmbH

Frequently Asked Questions

The global ready-to-eat food market is expected to reach US$487.0 billion in 2026.

Urban lifestyles, rising dual-income households, and demand for convenience food industry solutions drive market growth.

The ready-to-eat food market grows at a CAGR of 5.3% from 2026 to 2033.

Plant-based innovation, cold-chain expansion, and premium frozen meal demand create strong growth opportunities.

Nestlé, Unilever, Conagra Brands, General Mills, and Kraft Heinz lead the global market.