- Processed Food

- Food Flavors Market

Food Flavors Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Food Flavors Market by Flavor Type (Vanilla, Cocoa, Tea, Coffee, Spices, Herbs & Botanicals, Fruit and Vegetables, Dairy, Wine & Spirits, Others), Nature (Natural, Synthetic), Form (Dry, Liquid, Gel), Application (Beverages, Dairy & Frozen Products, Bakery & Confectionery, Sauces, Dressings & Condiments, Meat & Seafood, Animal & Pet Food, Others), and Regional Analysis, 2026 - 2033

Food Flavors Market Share and Trends Analysis

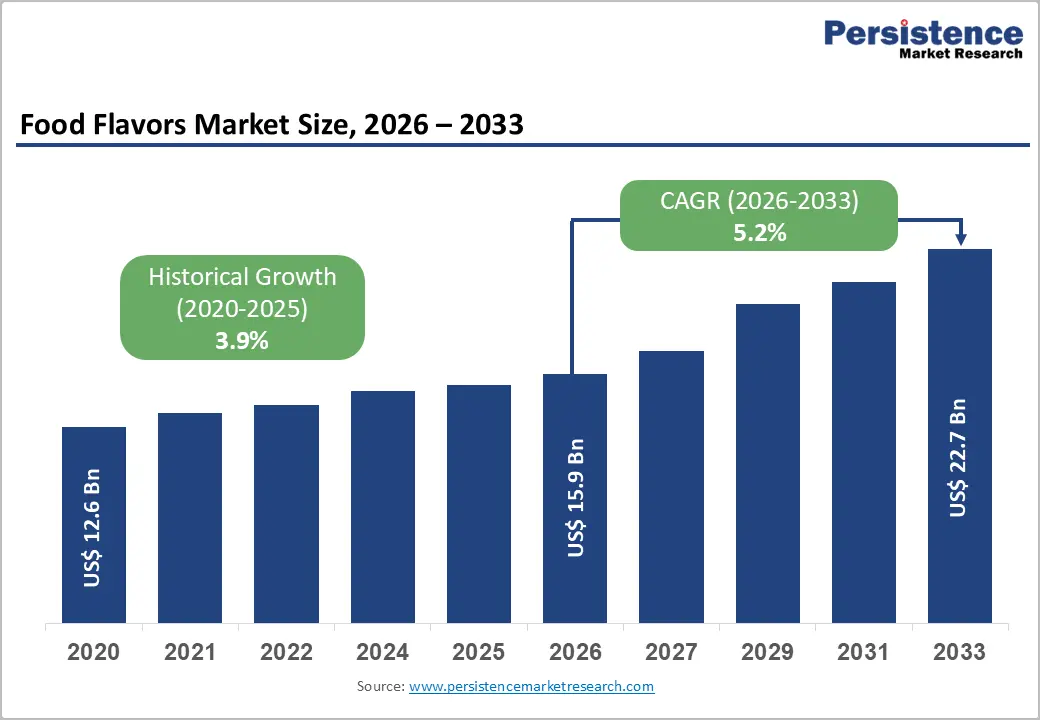

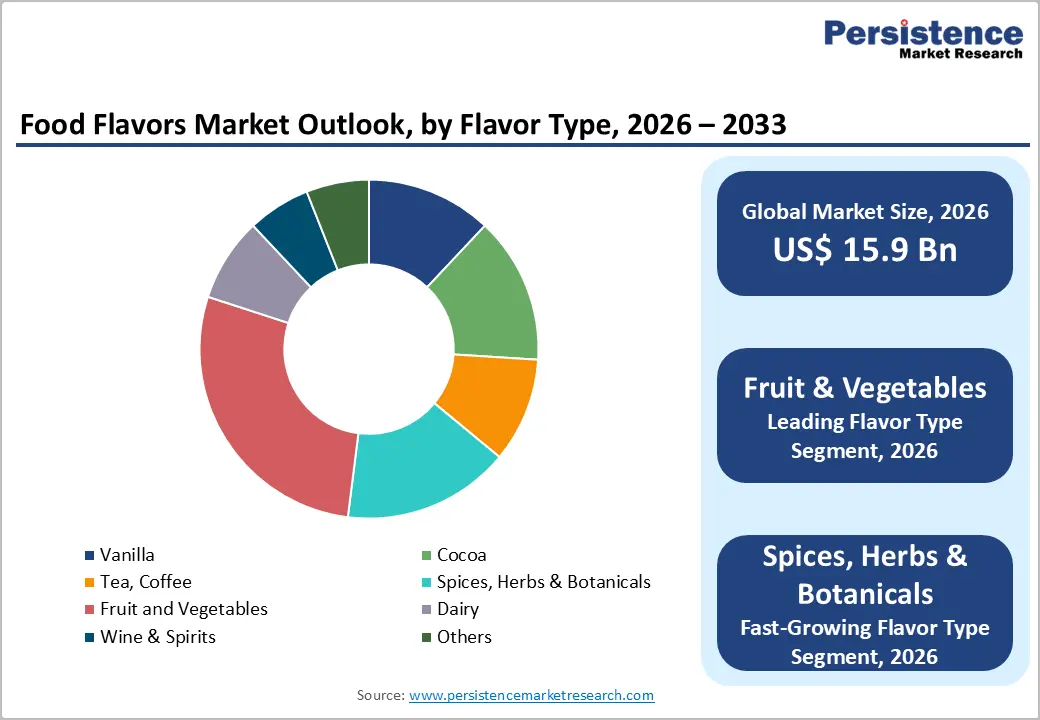

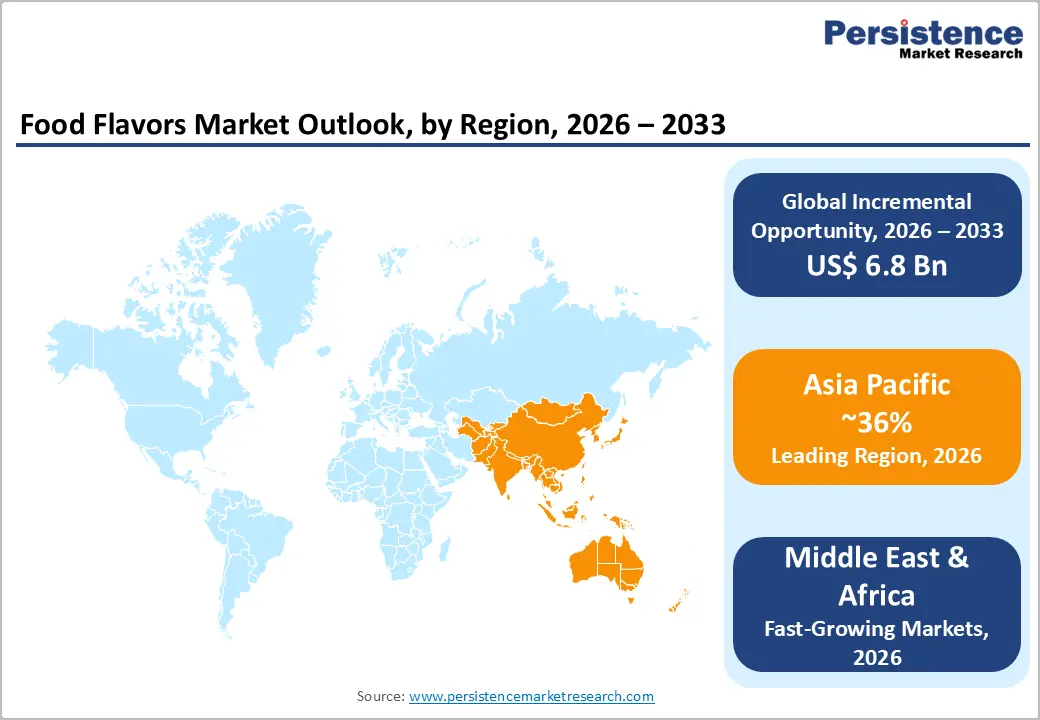

The global food flavors market size is expected to be valued at US$ 15.9 billion in 2026 and projected to reach US$ 22.7 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033. The global market is undergoing transformation shaped by evolving consumer expectations, rapid urbanization, and continuous product innovation. As food consumption patterns shift toward convenience and experiential eating, flavors have become central to product differentiation and brand identity.

Companies are investing heavily in advanced technologies to replicate authentic taste experiences while aligning with clean-label and sustainability demands. The convergence of health awareness, personalization, and global cuisine exposure is pushing flavor development into a more sophisticated, data-driven space. This evolution is redefining how manufacturers approach formulation, positioning flavors as a strategic lever for growth.

Key Industry Highlights:

- Leading Region: Asia Pacific, holding ~36% market share, driven by a large population base, rapid urbanization, and strong demand for diverse and culturally rooted flavor profiles across China and India

- Fastest-Growing Region: Middle East & Africa, fueled by rising disposable incomes, expanding foodservice sector, and increasing demand for processed and convenience foods in Saudi Arabia and South Africa

- Leading Flavor Type Segment: Fruit & Vegetables, driven by strong demand in beverages and dairy applications, with consumer preference for fresh, citrus, and tropical taste profiles associated with health and wellness

- Fastest-Growing Flavor Type Segment: Spices, Herbs & Botanicals, supported by increasing demand for ethnic, functional, and fusion flavors such as turmeric, ginger, and basil aligned with global wellness trends

- Market Drivers: Rising consumption of ready-to-eat and ultra-processed foods, increasing reliance on flavor enhancers to maintain taste, consistency, and sensory appeal in packaged food products

- Opportunities: Growing demand for customized and personalized flavor solutions using data analytics and AI to cater to specific dietary preferences such as low-sugar, keto, and allergen-free formulations

- Consumer Trends: Strong shift toward natural, clean-label, and plant-based flavors, with increasing preference for transparency, sustainability, and minimally processed ingredients

- Key Developments: In March 2026, Unilever PLC and McCormick & Company, Inc. announced plans to combine Unilever’s Foods business with McCormick to strengthen flavor solutions capabilities. In December 2025, dsm-firmenich introduced “Frosted Star Anise” as its Flavor of the Year for 2026, reflecting evolving global taste preferences.

| Key Insights | Details |

|---|---|

|

Global Food Flavors Market Size (2026E) |

US$ 15.9 Bn |

|

Market Value Forecast (2033F) |

US$ 22.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.9% |

Market Dynamics

Driver - Rising Demand for Ready-to-Eat and Convenience Foods

The increasing global preference for ready-to-eat and convenience foods is significantly driving demand in the food flavors market. As modern lifestyles become more fast-paced, consumers are prioritizing quick meal solutions that deliver consistent taste and quality without extensive preparation. This shift has encouraged food manufacturers to invest in advanced flavor technologies that can replicate fresh, homemade, and region-specific taste profiles in packaged formats. As a result, flavor innovation has become a critical tool for differentiation in highly competitive processed food categories.

According to the British Heart Foundation, more than 50% of an average individual’s energy intake in the UK comes from ultra-processed foods, reflecting the scale of convenience food consumption. This growing reliance on packaged products is creating strong demand for flavor enhancers that improve palatability and sensory appeal. Manufacturers are increasingly developing customized flavor solutions to cater to evolving preferences, including indulgent, functional, and health-oriented formulations.

Restraints - High Costs of Raw Material Sourcing and Volatility

The flavor industry is highly susceptible to the erratic pricing of natural raw materials caused by climate change and geopolitical instability. Natural extracts, such as Vanilla from Madagascar or specific Spices, often face supply chain disruptions, leading to significant price hikes. Data from the Food and Agriculture Organization (FAO) indicates that agricultural yield fluctuations directly impact the cost of goods sold for flavor houses. This volatility makes it challenging for smaller players to maintain competitive pricing, especially when synthetic alternatives are significantly cheaper. The transition to sustainable sourcing also adds a layer of logistical complexity and certification costs that can dampen profit margins for companies unable to scale their operations efficiently.

Opportunity - Customization of Flavors for Personalized Nutrition and Preferences

The growing demand for personalized food experiences is creating a strong opportunity in the global food flavors market. Consumers are increasingly seeking products aligned with their health goals, dietary restrictions, and cultural taste preferences. This shift is encouraging manufacturers to develop tailored flavor solutions that cater to specific needs such as low-sugar, keto-friendly, or allergen-free formulations. Advances in data analytics and artificial intelligence are enabling companies to better understand evolving consumption patterns and design targeted flavor profiles that resonate with distinct consumer segments.

Companies such as Symrise are leveraging proprietary tools such as trendscope™ and Symvision AI™ to decode emerging trends and enhance product innovation. These capabilities allow for the creation of highly customized and differentiated offerings. Beyond improving consumer satisfaction, personalized flavors support premiumization strategies and foster brand loyalty, positioning manufacturers to capture higher-value segments and sustain long-term growth in an increasingly competitive and experience-driven market.

Category-wise Analysis

Flavor Type Insights

The Fruit and Vegetables segment stood as the leading flavor type in 2025, commanding a significant 28% market share. This dominance is attributed to the universal appeal of fruity profiles in the Beverages and Dairy sectors. Consumers associate citrus, berry, and tropical flavors with health and freshness, making them the primary choice for product reformulations. Statistics from global trade databases highlight that orange and lemon extracts are among the most traded flavoring commodities. Meanwhile, the Spices, Herbs & Botanicals segment is identified as the fastest-growing category. This is driven by the adventurous palate of modern consumers seeking ethnic and fusion flavors, such as turmeric, ginger, and basil, which also offer perceived medicinal benefits, aligning with the global wellness trend.

Nature Insights

Natural flavors are gaining strong traction in the global food flavors market as consumers increasingly prioritize clean-label, transparent, and health-oriented food choices. Growing awareness regarding the potential drawbacks of synthetic additives is encouraging a shift toward naturally derived ingredients perceived as safer and higher in quality. This transition is closely aligned with broader lifestyle changes focused on wellness, driving demand for minimally processed and organically sourced flavor solutions across food and beverage applications.

Consumer preference data further reinforces this trend, with surveys indicating that a significant portion of buyers consider organic, natural, or non-GMO labeling as a key purchase factor. This evolving demand is prompting manufacturers to reformulate existing products and invest in natural ingredient innovation. As a result, the market is witnessing a surge in new product developments featuring plant-based and naturally sourced flavors, positioning them as a critical pillar for differentiation and long-term growth.

Regional Insights

Asia Pacific Food Flavors Market Trends and Insights

Asia Pacific is the leading regional segment, holding a 36% market share in 2025. This dominance is fueled by the massive populations and rapid urbanization in China, India, and ASEAN countries. The region benefits from significant manufacturing advantages and a vast agricultural base for raw material sourcing. China and Japan are major hubs for both consumption and production of savory and umami flavors, which are central to Asian cuisine. The growth dynamics in India and Southeast Asia are particularly impressive, driven by an expanding middle class with a penchant for westernized snacks and beverages. Local players are increasingly competing with multinationals by offering localized flavor profiles that cater to regional palates, such as durian, matcha, and masala. The rise of the organized retail sector and the proliferation of fast-food chains are creating a consistent demand for high-volume flavoring solutions. Furthermore, the region is becoming a center for cost-effective synthetic biology research, positioning it as a future leader in sustainable flavor production.

Middle East & Africa Food Flavors Market Trends and Insights

Middle East & Africa market is expected to show a CAGR of 6.3% during the forecast period, driven by evolving consumer tastes and increasing demand for processed and packaged foods across urban centers. Rising disposable incomes and a growing young population are accelerating the adoption of convenience foods, which in turn is boosting the need for diverse and regionally adapted flavor solutions. The expanding foodservice sector and international cuisine exposure are further influencing flavor innovation in the region.

A key trend shaping the market is the strong preference for bold, ethnic, and authentic taste profiles inspired by traditional Middle Eastern and African cuisines. Manufacturers are focusing on natural and clean-label flavor formulations to align with shifting consumer expectations toward healthier consumption. Additionally, the rapid growth of retail infrastructure and food manufacturing in countries like Saudi Arabia and South Africa is enhancing product accessibility, supporting steady expansion of the food flavors market across the region.

Competitive Landscape

The global food flavors market exhibits a highly consolidated structure at the top tier, with major players such as Givaudan S.A., IFF, and dsm-firmenich commanding a significant share through strong R&D capabilities and strategic acquisitions. These companies leverage advanced technologies and trend intelligence tools to develop innovative, customized flavor solutions aligned with evolving consumer preferences for natural, vegan, and clean-label products.

Despite this concentration, the market remains dynamic with the presence of regional and niche players specializing in botanical extracts and localized flavor profiles. Competitive differentiation is driven by end-to-end solution offerings, sustainability-focused sourcing, and co-creation models where flavor developers collaborate closely with food manufacturers. Increasing regulatory scrutiny and demand for compliant, safe formulations further shape innovation strategies across the industry.

Key Developments:

- In March 2026, Unilever PLC and McCormick & Company, Inc. announced an agreement to combine Unilever’s Foods business with McCormick, aiming to strengthen their position in the global food ingredients and flavor solutions market.

- In December 2025, dsm-firmenich unveiled “Frosted Star Anise” as its Flavor of the Year for 2026, reflecting emerging consumer preferences for warm, aromatic, and globally inspired taste profiles.

- In March 2025, Takasago International Corporation unveiled Vivid Flavors® Retroma®, an innovative flavor brand crafted using proprietary patented technology.

- In February 2025, MANE introduced a collection of 8 innovative vegan flavors, meticulously crafted to replicate the rich and savory taste of beef, while remaining entirely plant-based and cruelty-free.

Companies Covered in Food Flavors Market

- Givaudan S.A.

- IFF

- Kerry Group plc.

- Symrise

- Takasago International Corporation

- Sensient Technologies Corporation

- McCormick & Company, Inc.

- dsm-firmenich

- ADM

- Döhler GmbH

- Mane Group

- Corbion

- T. Hasegawa Co., Ltd.

- The Edlong Corporation

- Others

Frequently Asked Questions

The global food flavors market is projected to be valued at US$ 15.9 Bn in 2026.

Rising demand for ready-to-eat and convenience foods is a major driver of the global food flavors market.

The global food flavors market is poised to witness a CAGR of 5.2% between 2026 and 2033.

Customization of flavors for personalized nutrition and preferences is a significant opportunity in the food flavors market.

Major players in the global food flavors market include Givaudan S.A., IFF, Kerry Group plc., Symrise, Takasago International Corporation, Sensient Technologies Corporation, McCormick & Company, Inc.T., Hasegawa Co., Ltd. and others.