- Processed Food

- Pizza Foodservice Market

Pizza Foodservice Market Size, Share, and Growth Forecast, 2026 – 2033

Pizza Foodservices Market by Service Structure (Chained Outlets, Independent Outlets, others), Service Model (Delivery-Only, Dine-in, Takeout, Catering Services, Food Delivery Apps, Others), and Regional Analysis for 2026–2033

Pizza Foodservice Market Share and Trends Analysis

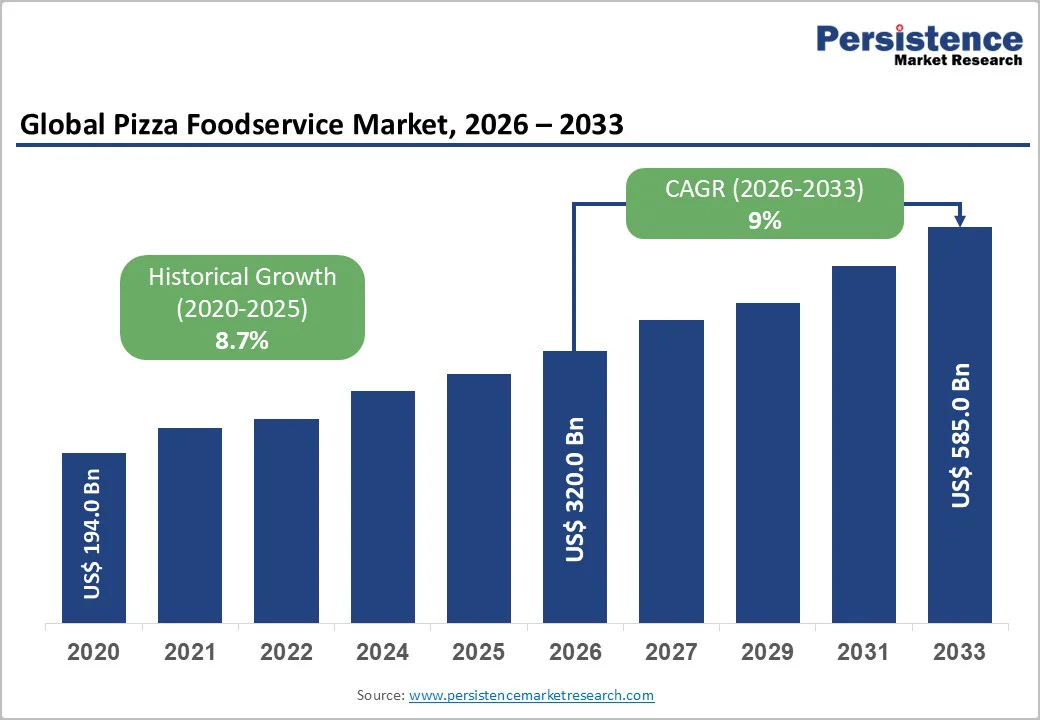

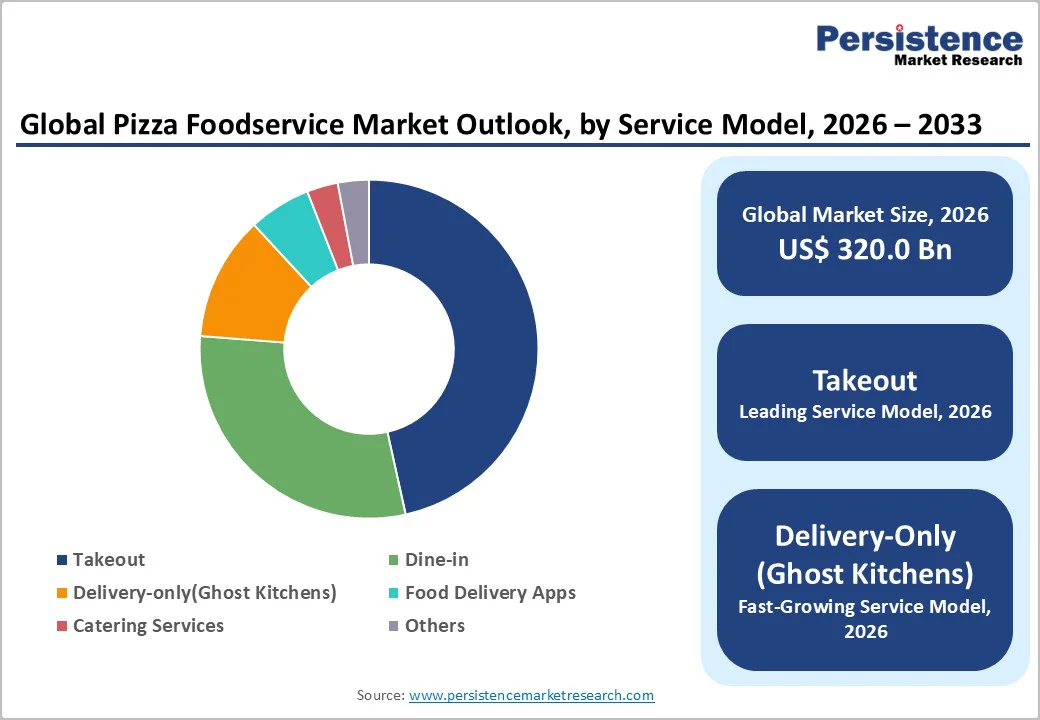

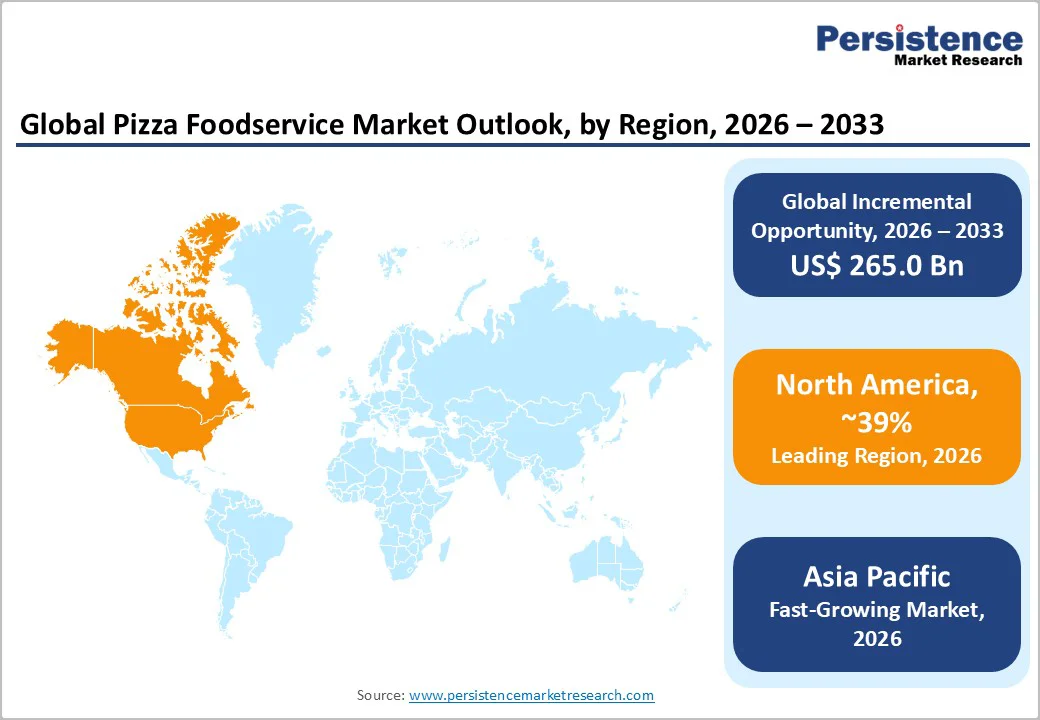

The global pizza food service market size is likely to be valued at US$ 320.0 billion in 2026, and is projected to reach US$ 585.0 billion by 2033, growing at a CAGR of 9% during the forecast period 2026-2033. This growth is underpinned by increasing urbanization, rising disposable incomes, and a strong consumer shift toward convenience through Online Delivery, Digital Ordering, and delivery-oriented business models such as ghost kitchens. At the same time, evolving consumer preferences toward premium offerings, including plant-based pizza and customizable toppings, support market expansion.

Key Industry Highlights

- Service Structure Dominance: Chained outlets are expected to dominate the market with around 70.2% revenue share in 2026, while independent pizzerias are projected to grow the fastest at an estimated 9.6% CAGR through 2033.

- Leading & Fastest-growing Service Model: The takeout format is anticipated to hold the largest share at around 47.2% in 2026, where delivery-only models are expected to grow the fastest at approximately 9.1% CAGR through 2033.

- Regional Leadership: North America is expected to lead the market with a 39% share in 2026, with Asia Pacific registering the highest 2026-2033 CAGR at about 8.56%.

- Key Strategic Developments: Expansion of ghost kitchens, adoption of automation and digital ordering platforms, and rapid menu innovation, including plant-based and premium pizza offerings, are reshaping the competitive landscape.

| Key Insights | Details |

|---|---|

| Pizza Foodservice Market Size (2026E) | US$ 320.0 Bn |

| Market Value Forecast (2033F) | US$ 585.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Urban Lifestyle Shifts and Technology-Enabled Convenience

The pizza foodservice market growth is driven by rapid urbanization, rising dual-income households, and evolving routines that prioritize convenience. As daily schedules tighten, demand for ready-to-eat meals grows, with delivery and takeout capturing a larger share than dine-in. For instance, in India, Jubilant FoodWorks, operator of Domino’s, opened 184 new stores in FY25 and plans 230 more, reflecting strong urban demand for accessible pizza options. This shift broadens the addressable customer base, while the proliferation of quick-service restaurants (QSR), takeaway pizza, online delivery, and digital ordering further reinforces growth momentum. Consumers increasingly prefer quick, reliable, and time-saving options that fit urban lifestyles.

Technological advancements are transforming pizza preparation and delivery. Digital ordering platforms, automated kitchens, AI-driven forecasting, and optimized logistics enhance efficiency for both chained outlets and independent pizzerias. These innovations reduce labor pressures, shorten service times, and support customization trends such as thin crust, premium toppings, and plant-based pizzas. Together, lifestyle and technology trends improve customer experience, boost order frequency, and sustain growth across traditional and delivery-first models.

Rising Health Concerns and Cost-Driven Operational Pressures

Pizza foodservice businesses are facing mounting pressure from shifting consumer expectations and evolving health regulations. Increasing awareness around calories, sodium, processed ingredients, and overall nutritional value is prompting many customers to limit consumption or seek alternatives. At the same time, regulatory standards on food composition continue to tighten, adding compliance requirements that restrict product flexibility. These shifts collectively challenge operators to balance taste, affordability, and transparency while maintaining consumer trust.

Alongside health-driven constraints, cost inflation and supply chain volatility add further strain to market performance. Fluctuations in key raw materials such as cheese, flour, meats, and vegetables can quickly erode margins, particularly for operators working within competitive or thin-profit environments. Securing high-quality, premium, or specialty ingredients also increases sourcing complexity, especially for smaller establishments. When combined with rising operational expenses, these pressures can limit menu innovation, drive pricing decisions, and affect overall profitability across both independent and chain operators.

Expansion through Digital Models and Premium, Localized Offerings

The strong growth potential of the market can be tapped through strategic expansion in emerging economies and the increasing adoption of delivery-first formats. Rising urbanization, higher disposable incomes, and changing food preferences in developing markets create a favorable environment for international and local operators. Digital-native models such as ghost kitchens further strengthen this opportunity by enabling low-cost scalability and efficient market penetration. Their ability to operate with minimal overhead supports rapid geographic reach while catering to the growing preference for delivery and takeout.

Evolving consumer expectations around taste, health, and personalization open the door for premiumization across product lines. For instance, Blackbird Foods launched “Blackbirdie Pizza Minis” in 2025, offering small 5-inch vegan, non-GMO, dairy-free pizzas through retail channels, while Toppers Pizza introduced fully vegan, plant-based variants at its restaurant locations. Offering plant-based options, functional ingredients, gourmet toppings, and customizable crust varieties enables brands to differentiate and command higher margins. Localized menus tailored to cultural preferences help operators connect with diverse consumer groups, enhancing customer loyalty and brand relevance.

Category-wise Insights

Service Structure Insights

Chained outlets are expected to dominate with approximately 60% of the pizza foodservice market revenue share in 2026, supported by strong branding, standardized processes, and efficient supply-chain systems. Their ability to maintain consistent quality across multiple regions enables rapid expansion into mature and emerging markets. In April 2025, for instance, Papa John’s partnered with Google Cloud to implement AI-powered digital ordering, push notifications, and chatbots, enhancing operational efficiency and customer engagement. Large-scale marketing investments further strengthen brand recall and drive higher order volumes. As urban markets grow, these chains benefit from prime locations and broad customer reach. Their operational scale allows seamless integration of digital platforms, loyalty programs, and delivery systems, providing a competitive advantage over smaller competitors.

Independent outlets are set to be the fastest-growing segment, projected to expand at 9.6% CAGR through 2033, fueled by a soaring demand for authenticity and customization. These outlets attract consumers seeking artisanal techniques, regional flavors, and specialty crusts such as thin crust. Flexibility has enabled quick menu innovation, seasonal ingredients, and local adaptations. Lower capital requirements allow easier market entry. As consumer interest in novelty rises, independents are expected to strengthen their niche presence and sustain above-industry growth.

Service Model Insights

The takeout model is projected to lead in 2026, capturing around 47% revenue share, driven by convenience, shorter wait times, and affordability it offers compared to dine-in. Many consumers choose takeout for family meals, office lunches, or on-the-go consumption, making it a stable revenue source. The segment benefits from packaging innovations that maintain food quality and temperature during transit. Its operational simplicity supports predictable demand patterns, and busy lifestyles globally reinforce takeout as a core distribution channel for both chains and independent outlets.

Delivery-only kitchens are poised to grow the fastest, expected to advance at a 9.1% CAGR from 2026 to 2033, owing to the widespread adoption of digital ordering platforms and app-based delivery options. These kitchens operate without dine-in areas, reducing overhead and enabling rapid scaling in dense urban zones. In 2025, Domino’s expanded delivery via third-party platforms such as DoorDash, widening customer access and boosting incremental sales. Flexible structures allow menu testing, virtual brands, and faster expansion. Efficient logistics shorten delivery times and improve satisfaction, making delivery-only models highly cost-effective for growth.

Regional Insights

North America Pizza Foodservice Market Trends

North America is expected to dominate in 2026, estimated to secure 39% of the pizza foodservice market share, powered primarily by the U.S., where quick-service pizza formats and advanced delivery ecosystems are deeply established. High disposable incomes, massive adoption of digital ordering, and growing use of automation across kitchen operations reinforce this leadership. Mature supply-chain networks and strong brand presence among major chains create a highly efficient operating environment. Regulatory standards on food safety and packaging encourage consistency but increase operational costs, prompting continuous innovation. Despite being a saturated market, evolving consumer expectations for faster service and improved convenience sustain long-term relevance. Incremental growth continues as operators enhance menus, streamline delivery, and offer personalized digital experiences.

The regional competitive landscape features a blend of major chains and local independents, the latter gaining traction through gourmet positioning and regional flavor diversity. Technology investments remain central to market expansion, including AI-driven scheduling, automated make-lines, and sustainable last-mile delivery initiatives. Urban and suburban regions continue to attract targeted expansion, particularly in underpenetrated neighborhoods seeking convenient dining options. Menu innovation, including healthier alternatives and premium toppings, helps brands retain consumer interest in a highly competitive environment. The region’s strong purchasing power supports ongoing upgrades in packaging and service efficiency.

Europe Pizza Foodservice Market Trends

Europe stands as one of the major contributors to global pizza demand, supported by Germany, the U.K., France, and Spain, where a mix of traditional pizza culture and rising fast-casual formats drive consistent performance. The regional market benefits from established dining habits, increasing urbanization, and a growing inclination toward convenient meal solutions. Western-style diets continue influencing younger consumers, strengthening demand for quick-service and takeaway formats. Food safety, labeling, and sustainability standards set by the European Union (EU) shape product offerings and encourage higher-quality sourcing. As health consciousness rises, demand grows for plant-based, gluten-free, and environmentally responsible menu options.

Competition in Europe spans large multinational chains and independent artisanal pizzerias, the latter strengthening their position through regional ingredient use and authentic culinary methods. Many operators are investing in modern restaurant formats, digital ordering, and efficient takeaway systems to appeal to on-the-go consumers. Urban centers offer fertile ground for franchising and fast-casual expansion, particularly among younger, value-driven diners. Sustainability trends are influencing packaging, supply chains, and menu innovation across the region. Operators increasingly differentiate through nutrition-focused offerings and premium crust or topping varieties, making the regional market highly dynamic.

Asia Pacific Pizza Foodservice Market Trends

Asia Pacific is likely to be the fastest-growing regional market for pizza foodservice, projected to post a 9.6% CAGR through 2033, propelled by rapid urbanization, rising disposable incomes, and accelerated westernization of diets. Key markets such as China, India, Japan, and Southeast Asia exhibit strong appetite for affordable quick-service dining. Increasing smartphone penetration and widespread use of online food-delivery platforms further elevate demand, especially among younger consumers. Shifting lifestyle patterns in metro cities support frequent ordering and preference for convenience-based dining formats. Operators are leveraging this momentum by expanding delivery fleets, digital storefronts, and value-focused menu options. The region’s large consumer base creates significant long-term scalability.

The competitive landscape combines global chains with fast-growing local brands offering regionally inspired flavors, such as spicy, seafood-based, or fusion-style pizzas. Regulatory standards around food safety, sourcing transparency, and import controls shape supply-chain decisions and influence ingredient availability. Investors are gravitating toward cost-efficient models such as dark kitchens and compact takeaway outlets to reach high-density markets. Partnerships with delivery apps accelerate market penetration and increase brand visibility. Affordability remains crucial, leading operators to develop low-cost menu formats to appeal to price-sensitive consumers while driving high-volume orders. Asia Pacific's demographic scale and evolving consumer habits make it one of the most promising growth hubs for pizza foodservice companies.

Competitive Landscape

The global pizza foodservice market structure is moderately consolidated, dominated by major international chains such as Domino’s, Pizza Hut, Papa John’s, and Little Caesars. These brands benefit from extensive franchising systems that support rapid expansion across diverse geographies. Their leadership is reinforced by advanced digital ordering platforms, AI-based delivery routing, and strong loyalty programs that enhance customer retention. Investments in automated kitchen technologies improve operational efficiency and order consistency. Menu innovation, including plant-based pizza, premium toppings, and customizable thin crust options, further differentiates offerings. Robust supply-chain integration enables competitive pricing and reliable ingredient sourcing.

Independent pizzerias and regional chains compete effectively through authenticity, artisanal preparation, and localized menu differentiation. These operators appeal to consumers seeking unique flavors, handcrafted styles, and community-rooted dining experiences. Their agility allows rapid adaptation to emerging trends, including healthier ingredients and premium customization. The rise of online delivery, food-delivery apps, and ghost kitchens has expanded digital access and lowered barriers to market entry. Many independents leverage flexible pricing and personalized service to build customer loyalty. Cost-efficient expansion models, such as delivery-only formats, allow them to scale without heavy capital investment. Brands balancing innovation, quality, and digital convenience are increasingly competitive in high-growth markets.

Key Industry Developments

- In August 2025, Papa John’s announced plans to re-enter the Indian market after an eight-year absence, starting with a reopening in Bengaluru by October 2025. The company aims to expand to 650 stores over the next decade, targeting under-penetrated urban centers. This move highlights Papa John’s focus on capturing growth in emerging markets with rising urbanization and disposable incomes.

- In March 2025, Domino’s and Uber expanded their partnership so that stores in Australia and New Zealand can use Uber Direct to fulfil orders placed on Domino’s own channels, enabling extended trading hours and better coverage during demand spikes such as major sporting events.

- In January 2025, DPC Dash, Domino’s master-franchisee in China, opened 14 new stores across 13 cities as part of its “go-deeper, go-broader” strategy, expanding into under-penetrated cities such as Shenyang, Chongqing, and Zhengzhou.

Companies Covered in Pizza Foodservice Market

- Domino's Pizza, Inc.

- Pizza Hut

- Papa John's International, Inc.

- Little Caesars

- Sbarro, LLC

- California Pizza Kitchen, Inc.

- MOD Pizza

- Round Table Pizza

- Blaze Pizza

- Papa Murphy’s Holdings, Inc.

- Pizza Capers

- Pizza Ranch

Frequently Asked Questions

The global pizza foodservice market is projected to reach US$ 320.0 billion in 2026.

Urban migration, rising incomes, quick-service and delivery-first preferences, technology adoption, and a strong demand for customizable menus are driving the market.

The market is poised to witness a CAGR 9% from 2026 to 2033.

Opportunities include independent pizzerias, ghost kitchen expansion, digital ordering adoption, plant-based and premium menu offerings, and urban growth markets.

Some of the key players in the market include Domino’s, Pizza Hut, Papa John’s, and Little Caesars.