- Pharmaceuticals

- Diabetic Nephropathy Market

Diabetic Nephropathy Market Size, Share, and Growth Forecast, 2026 - 2033

Diabetic Nephropathy Market by Drug Class (ACE Inhibitors, Angiotensin Receptor Blockers, SGLT2 Inhibitors, Others), Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, Others), and Regional Analysis for 2026 - 2033

Diabetic Nephropathy Market Size and Trends Analysis

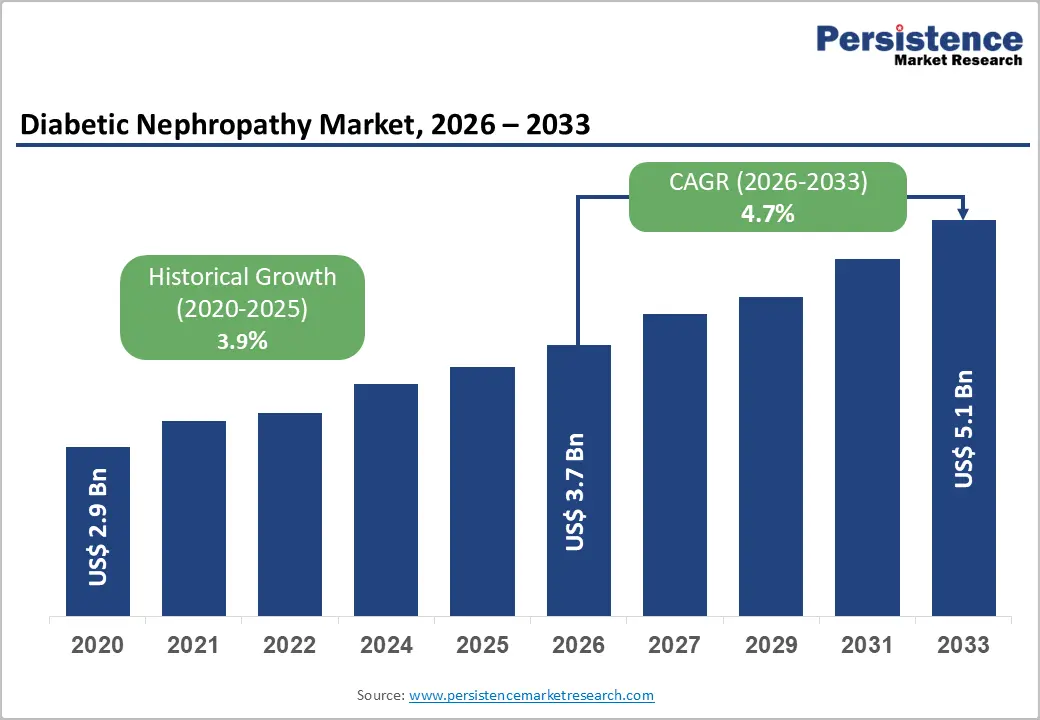

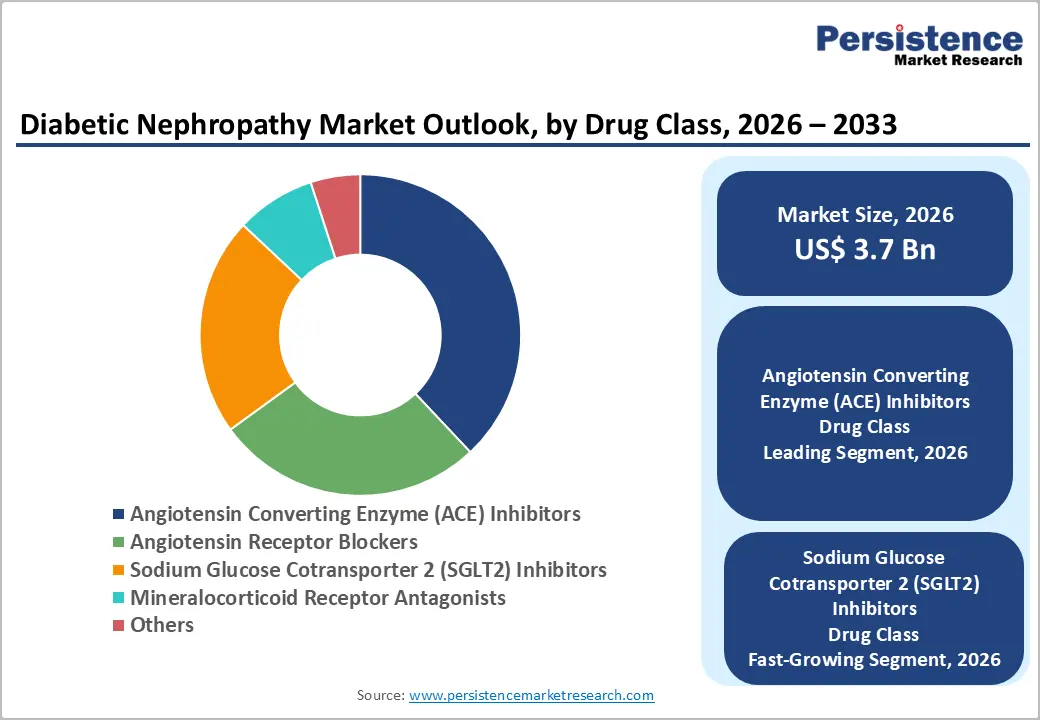

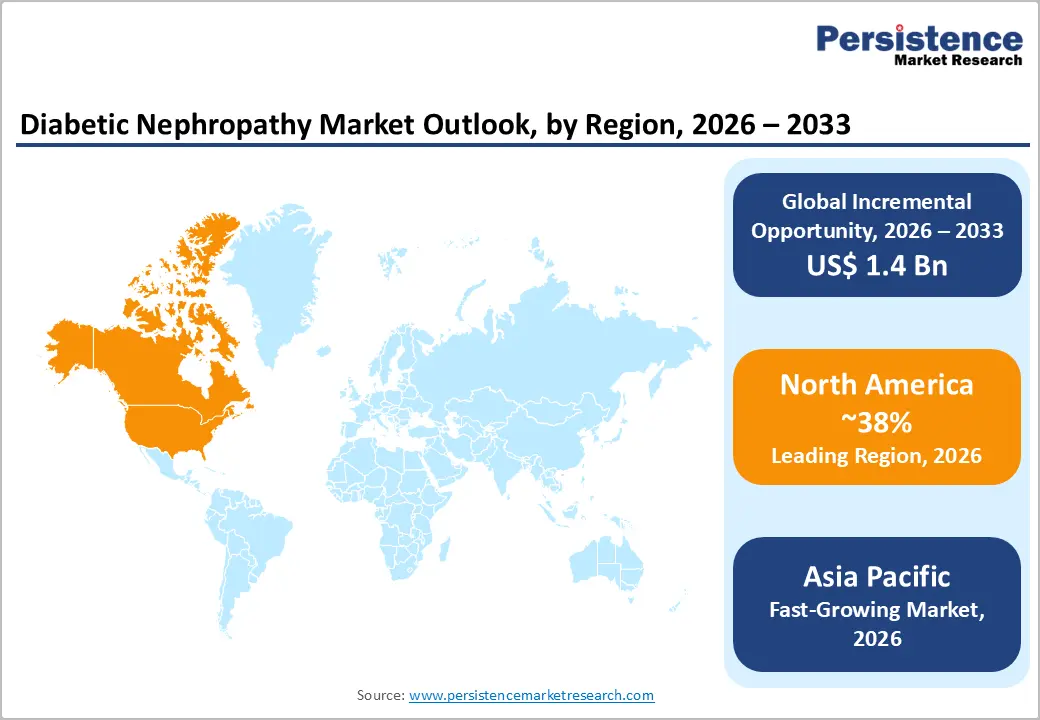

The global diabetic nephropathy market size is likely to be valued at US$3.7 billion in 2026, and is expected to reach US$5.1 billion by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by the rising global prevalence of diabetes, especially type 2 diabetes, which significantly increases the risk of kidney-related complications.

Growing awareness of early kidney disease diagnosis, increasing adoption of advanced therapies such as SGLT2 inhibitors and GLP-1 receptor agonists, and rising healthcare expenditure are further accelerating market growth.

Key Industry Highlights:

- Dominant Region: North America is expected to dominate, commanding 38% of the total revenue in 2026, propelled by high pharmaceutical spending, favorable reimbursement policies, and strong clinical development activity for innovative DN therapies, led by the U.S. market.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, due to the rising diabetic population, improving healthcare infrastructure, increasing awareness, and expanding access to advanced kidney disease therapies.

- Leading Drug Class: ACE inhibitors are expected to dominate, holding 38% of the share in 2026, due to strong long-term clinical evidence supporting their use as first-line renoprotective therapy in diabetic kidney disease.

- Dominant Distribution Channel: Hospital pharmacies are expected to dominate with approximately 55% of share in 2026, driven by specialist-led management of moderate-to-severe CKD patients through integrated hospital-based nephrology and diabetes care systems.

DRO Analysis

Driver - Surging Global Diabetes Prevalence and the Rising Burden of Diabetic Kidney Disease

The single most powerful driver of the market is the relentless global expansion of diabetes mellitus prevalence, which directly determines the addressable patient population for DN therapeutics. The International Diabetes Federation (IDF) Diabetes Atlas (10th Edition, 2021) estimated that 537 million adults aged 20-79 years were living with diabetes globally in 2021, a figure projected to rise to 643 million by 2030 and 783 million by 2045, representing an increase over approximately 25 years.

In the U.S., the Centers for Disease Control and Prevention (CDC) reports that approximately 38.4 million Americans (11.6% of the total population) have diabetes, with an additional 97.6 million adults classified as prediabetic, a reservoir of future diabetic kidney disease incidence. The National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK) estimates that diabetic kidney disease affects approximately 1 in 3 adults with diabetes in the U.S.

Restraint - Generic Erosion of Established Drug Classes and Pricing Pressure

The market’s most commercially established drug classes, ACE inhibitors and angiotensin receptor blockers (ARBs), have undergone extensive genericization, with branded originator drugs largely replaced by low-cost generic alternatives priced at under US$0.10 per tablet in highly competitive markets.

Although this widespread availability has improved affordability and expanded patient access, it has also substantially compressed manufacturer revenues and profit margins. As a result, future market expansion is expected to rely increasingly on the adoption of newer patented therapies, including SGLT2 inhibitors and mineralocorticoid receptor antagonists (MRAs), which provide stronger commercial potential and higher revenue generation opportunities.

Payer pushback against the pricing of SGLT2 inhibitors and finerenone represents an additional barrier to market growth. Despite strong clinical evidence from outcome trials, formulary placement and reimbursement access for these agents in the context of diabetic nephropathy, specifically as opposed to their overlapping cardiac and diabetes indications, vary significantly across insurance and national health systems.

Opportunity - Novel Therapeutic Pipeline and Combination Therapy Approaches

The diabetic nephropathy treatment pipeline remains one of the most active across nephrology therapeutic areas, with several Phase 2 and Phase 3 candidates targeting disease pathways beyond traditional renin-angiotensin system (RAS) blockade and SGLT2 inhibition. Prominent pipeline segments include endothelin-A receptor antagonists, selective aldosterone synthase inhibitors, soluble guanylate cyclase stimulators, and advanced glycation end-product (AGE) inhibitors.

In addition, combination therapies involving SGLT2 inhibitors and finerenone are being evaluated in the CONFIDENCE trial, where preliminary findings indicate greater albuminuria reduction compared to either therapy alone. This additive therapeutic effect could increase per-patient prescribing volumes and further expand the addressable diabetic nephropathy drug market.

The GLP-1 receptor agonist category, led by semaglutide from Novo Nordisk and dulaglutide from Eli Lilly and Company, has also shown meaningful reductions in albuminuria along with potential renoprotective benefits in major cardiovascular outcome studies, including the LEADER, SUSTAIN-6, and REWIND trials. Furthermore, dedicated kidney outcome studies such as the FLOW trial evaluating semaglutide in chronic kidney disease are producing findings that are significantly influencing the future direction of nephroprotective therapies.

Category-wise Analysis

Drug Class Insights

ACE inhibitors are projected to maintain market leadership, contributing approximately 38% of total revenue in 2026. Their dominance is supported by decades of clinical evidence demonstrating the effectiveness of ACE inhibitors such as ramipril, lisinopril, enalapril, and perindopril as first-line renoprotective therapies for patients with diabetic kidney disease, irrespective of hypertension status. Widely prescribed products in this category include ramipril, marketed by Pfizer under the Altace brand, and lisinopril, commercialized by AstraZeneca as Zestril, both recognized for their role in slowing the progression of diabetic kidney disease.

SGLT2 inhibitors are anticipated to register the fastest growth during the forecast period. Leading originator therapies, including dapagliflozin, canagliflozin, empagliflozin, and ertugliflozin, have secured approvals from the FDA and EMA for chronic kidney disease (CKD) indications and are increasingly being integrated into both specialist and primary care treatment protocols worldwide following updated recommendations from the ADA, KDIGO, and global nephrology associations. AstraZeneca obtained FDA approval for Farxiga (dapagliflozin) in CKD treatment, while Eli Lilly and Company, in collaboration with Boehringer Ingelheim, expanded the use of Jardiance (empagliflozin) in CKD management, accelerating the adoption of SGLT2 inhibitors in diabetic nephropathy care.

Distribution Channel Insights

Hospital pharmacies are likely to dominate, accounting for approximately 55% of global market revenue in 2026. This dominance reflects the specialist-driven prescribing dynamics of DN management: patients with moderate-to-severe CKD (eGFR below 45 mL/min/1.73m²) are predominantly managed within hospital-based nephrology, diabetology, and internal medicine outpatient clinics where prescriptions are dispensed through integrated hospital pharmacy systems. Mayo Clinic manages diabetic nephropathy patients through hospital-based nephrology programs, where drugs such as Farxiga (dapagliflozin) from AstraZeneca are dispensed via integrated hospital pharmacy systems.

Drug stores and retail pharmacies represent the fastest-growing distribution channel. This growth is driven by the progressive migration of stable, well-controlled DN patients from specialist hospital care to primary care physician management, a shift actively promoted by health systems to relieve specialist capacity constraints. CVS Health expanded retail pharmacy services for diabetes and kidney care patients, supporting the shift of stable diabetic nephropathy management from hospitals to primary care settings.

Regional Insights

North America Diabetic Nephropathy Market Trends

North America is projected to lead the market, accounting for approximately 38% of the total revenue in 2026, with the U.S. contributing more than 88% of the regional demand. The strong position of the U.S. market is supported by the world’s highest per-capita pharmaceutical expenditure, a highly favorable reimbursement framework for innovative therapies for diabetic nephropathy, and extensive clinical trial activity that continues to support label expansions for both existing and emerging treatments for diabetic nephropathy.

U.S. Diabetic Nephropathy Market Insights

The U.S. diabetic nephropathy market is driven by the high prevalence of diabetes and chronic kidney disease, strong adoption of advanced therapies such as SGLT2 inhibitors and non-steroidal MRAs, and favorable reimbursement systems. Increasing focus on early diagnosis, growing healthcare expenditure, and ongoing clinical research are further supporting market growth in the country.

Canada Diabetic Nephropathy Market Insights

The Canada market is growing due to the rising burden of diabetes and increasing prevalence of chronic kidney disease among the aging population. Government-supported access to healthcare, growing awareness of early kidney disease management, and the adoption of advanced therapies such as SGLT2 inhibitors are supporting market expansion.

Europe Diabetic Nephropathy Market Trends

Market growth in Europe is fueled by universal healthcare coverage, well-established nephrology specialty infrastructure, and comprehensive guideline-driven prescribing across EU member states.

Germany Diabetic Nephropathy Market Trends

Germany is the dominant European market, reflecting the country’s strong specialty pharmaceutical prescribing culture, significant diabetic CKD patient burden (approximately 8.7% of the German population has Type 2 diabetes, per the German Diabetes Society), and Bayer AG’s domestic commercial infrastructure for finerenone (Kerendia), which received its first global commercial launch in Germany following CHMP recommendation.

U.K. Diabetic Nephropathy Market Trends

The U.K. NHS presents a highly formulary-managed prescribing environment for DN therapeutics. NICE has published technology appraisals recommending dapagliflozin for CKD (TA775, 2022), establishing a reimbursement-backed prescribing pathway that NHS commissioners are progressively implementing across CCG/ICB territories.

Asia Pacific Diabetic Nephropathy Market Trends

Asia Pacific is likely to be the fastest-growing regional market, witnessing rapid growth, due to the rising diabetic population, improving healthcare infrastructure, and increasing awareness of early kidney disease treatment. Expanding access to advanced therapies and growing healthcare investments in countries such as China, India, and Japan are further driving market demand.

China Diabetic Nephropathy Market Trends

China is the region’s dominant market and carries the world’s largest absolute burden of diabetic kidney disease, with an estimated 30-40 million Chinese patients with CKD attributable to diabetes. The National Medical Products Administration (NMPA) has approved dapagliflozin, empagliflozin, and canagliflozin for their diabetes and cardiovascular indications in China, and their nephroprotective benefits are incorporated into the Chinese Diabetes Society (CDS) guidelines, creating a growing prescribing base.

India Diabetic Nephropathy Market Trends

India represents the Asia Pacific region’s highest-growth individual country market for DN therapeutics, driven by the enormous and rapidly expanding diabetic CKD patient population, growing tertiary nephrology infrastructure, and the emergence of quality-conscious generic drug manufacturers capable of producing affordable DN medications. Indian pharmaceutical companies, including Aurobindo Pharma, Sun Pharmaceutical, and Cipla, dominate the ACE inhibitor and ARB generic segment in India and export to global markets, while simultaneously developing SGLT2 inhibitor generic pipelines targeting patent expiry windows.

Competitive Landscape

The global diabetic nephropathy market is highly competitive, with a mix of large pharmaceutical companies developing innovative patented therapies and generic drug manufacturers competing mainly in the ACE inhibitor and ARB segments through lower pricing. Companies from India, Israel, and the U.S. play a major role in the generics market. AstraZeneca and Janssen Pharmaceuticals are among the leading players in the fast-growing SGLT2 inhibitor segment, with Farxiga and Invokana generating significant revenues from chronic kidney disease (CKD) and diabetic nephropathy treatments worldwide.

Sanofi and Novartis are also strengthening their presence in the diabetic kidney disease space through ongoing research and pipeline development. Sanofi is working with Regeneron Pharmaceuticals on anti-inflammatory therapies, while Novartis is investing in kidney-targeted drug delivery technologies. These efforts highlight their long-term interest in expanding into the diabetic nephropathy treatment market.

Key Industry Developments:

- In November 2023, ProKidney Corp. obtained approval from the U.K. Medicines and Healthcare Products Regulatory Agency (MHRA) for proact 1 (REGEN-006) and received scientific advice from the EMA regarding phase 3 protocols for REACT in diabetic chronic kidney disease.

- In July 2021, the FDA approved Bayer AG’s Kerendia (finerenone) tablets to reduce the risk of decreasing kidney function, kidney failure, non-fatal heart attacks, cardiovascular death, and hospitalization due to heart failure in adults with chronic kidney disease associated with type 2 diabetes.

Companies Covered in Diabetic Nephropathy Market

- Janssen Pharmaceuticals, Inc.

- AstraZeneca

- Aurobindo Pharma Limited

- Teva Pharmaceutical Industries Ltd

- Sanofi

- Novartis AG

- Sun Pharmaceutical Industries Ltd.

- Bayer AG

- Par Pharmaceuticals

Frequently Asked Questions

The global diabetic nephropathy market is projected to reach US$3.7 billion in 2026.

The diabetic nephropathy market is primarily driven by the rising global diabetes population and strong clinical trial evidence supporting SGLT2 inhibitors and non-steroidal MRAs as standard treatments for diabetic kidney disease.

The diabetic nephropathy market is poised to witness a CAGR of 4.7% from 2026 to 2033.

Key opportunities include novel GLP-1 therapies, growing combination treatments, wider access to generic SGLT2 inhibitors, and rising diabetic nephropathy treatment demand in emerging Asian markets.

Key players include AstraZeneca PLC, Janssen Pharmaceuticals (J&J), Bayer AG, Novartis AG, Sanofi S.A., Teva Pharmaceutical Industries, Aurobindo Pharma Limited, Sun Pharmaceutical Industries, and Par Pharmaceuticals.