- Pharmaceuticals

- Diabetic Gastroparesis Market

Diabetic Gastroparesis Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Diabetic Gastroparesis Market by Treatment Type (Pharmaceutical Drugs, Endoscopic Treatments (G-POEM), Gastric Electrical Stimulation, and Others), Disease Type (Compensated Gastroparesis, and Gastric Failure), End-user (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

Diabetic Gastroparesis Market Share and Trends Analysis

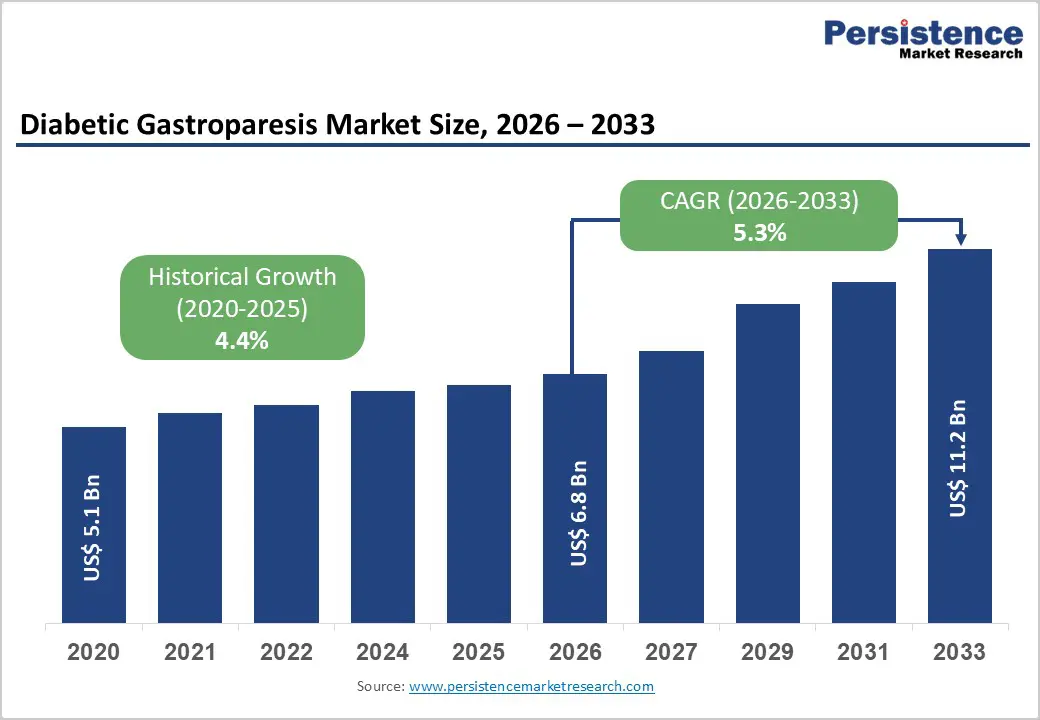

The global diabetic gastroparesis market size is likely to be valued US$ 6.8 billion in 2026 to US$ 11.2 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for diabetic gastroparesis treatments is rising steadily, driven by the growing global prevalence of diabetes, increasing disease awareness, and improved diagnosis of gastrointestinal motility disorders. Hospitals and specialty gastroenterology clinics are witnessing higher patient volumes as diabetic gastroparesis is increasingly recognized as a chronic complication requiring long-term management. The rise of pharmacological therapies, alongside the expanding adoption of advanced endoscopic and device-based interventions, is supporting sustained market growth across developed and emerging economies.

Growing investments in healthcare infrastructure, expansion of specialty care centers, and improved access to gastroenterology services are further accelerating treatment uptake. Continuous advancements in drug formulations, symptom-targeted therapies, and minimally invasive procedures are improving clinical outcomes and patient quality of life. In addition, increasing clinician awareness, expanding clinical guidelines, and a growing body of real-world evidence supporting early intervention and structured disease management continue to reinforce long-term growth in the global diabetic gastroparesis market.

Key Industry Highlights:

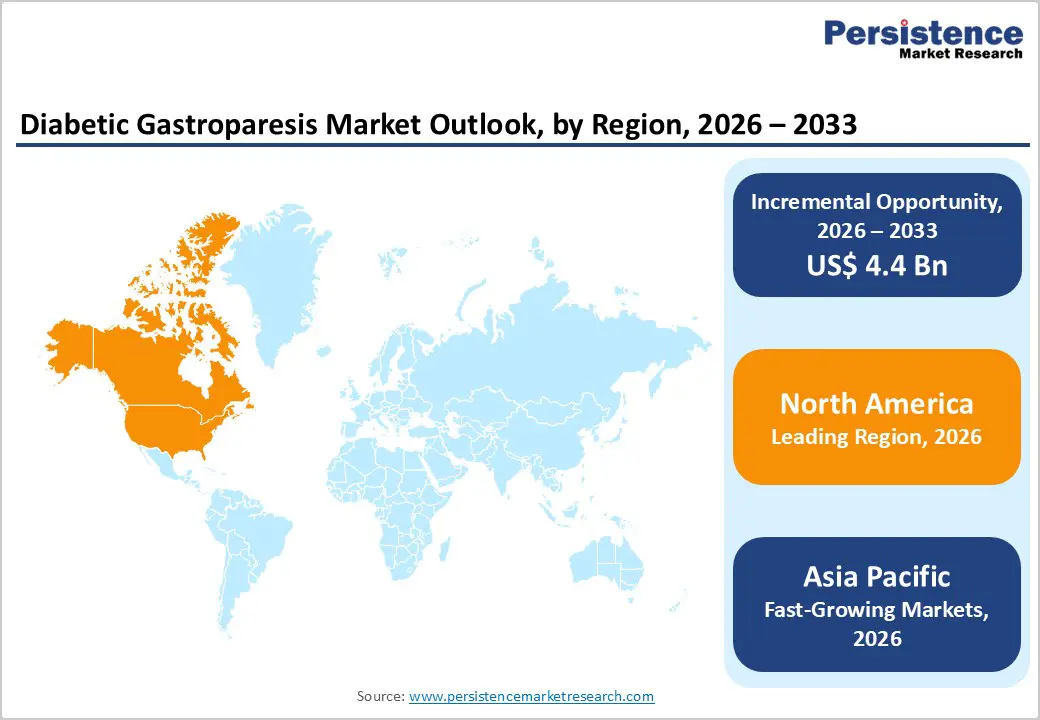

- Leading Region: North America holds the largest share at 47.5%, supported by high diabetes prevalence, advanced gastroenterology care infrastructure, strong healthcare expenditure, and early access to FDA-approved therapies and interventional treatment options.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace, driven by a large and underserved diabetic population, improving diagnosis rates, rapid expansion of specialty hospitals, growing medical tourism, and increasing investment in chronic disease management.

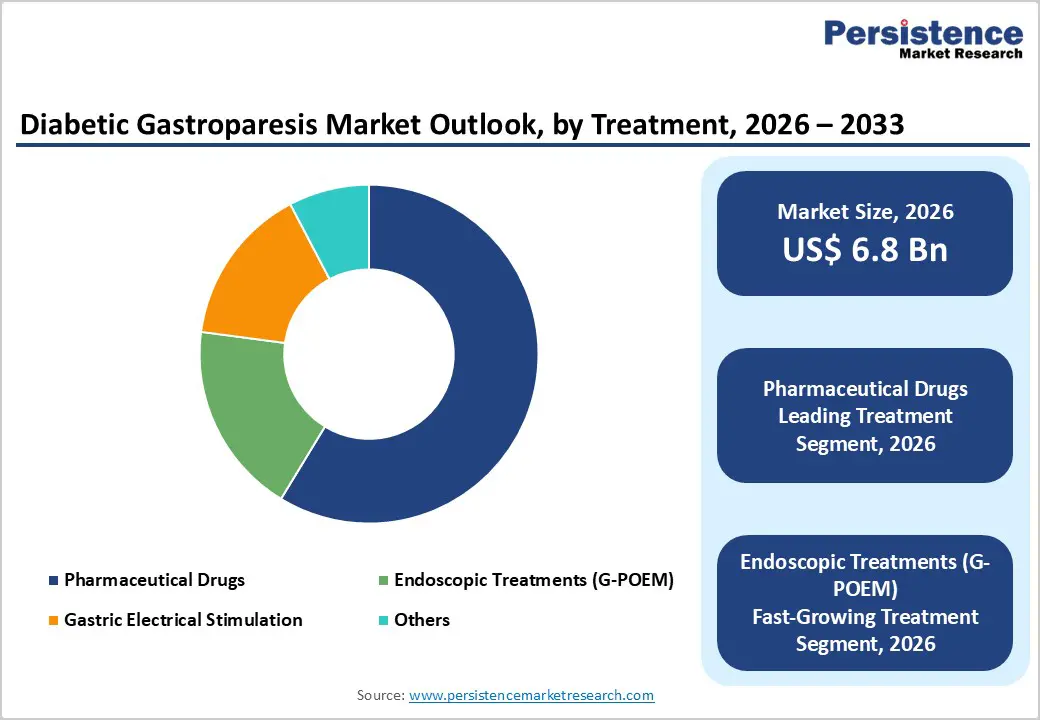

- Leading Treatment Type Segment: Pharmaceutical drugs dominate the market due to their widespread use as first-line therapy for symptom control, ease of administration, long-term patient dependence, and strong physician familiarity across disease stages.

- Fastest-Growing Treatment Type Segment: Endoscopic treatments (G-POEM) are witnessing rapid growth as clinical adoption increases for refractory patients, supported by favorable outcomes, minimally invasive profiles, and growing availability of trained specialists.

- Leading Disease Type Segment: Compensated gastroparesis remains the leading segment, driven by a larger diagnosed patient pool requiring long-term pharmacological management, dietary modification, and routine clinical monitoring.

- Fastest-Growing Disease Type Segment: Gastric failure is growing rapidly due to increasing recognition of severe disease forms, rising demand for advanced interventions, and expanding use of device-based and endoscopic therapies in tertiary care settings.

| Key Insights | Details |

|---|---|

| Diabetic Gastroparesis Market Size (2026E) | US$ 6.8 Bn |

| Market Value Forecast (2033F) | US$ 11.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver - Rising Diabetes Burden and Improved Diagnostic Awareness

The global prevalence of diabetes continues to rise at a significant pace, creating a steadily expanding at-risk population for diabetic gastroparesis. Both type 1 and type 2 diabetes patients, particularly those with long disease duration, suboptimal glycemic control, and diabetes-related neuropathy, are increasingly susceptible to delayed gastric emptying and associated gastrointestinal complications. For instance, according to the International Diabetes Federation (IDF), 2024, approximately 589 million adults aged 20-79 years are currently living with diabetes worldwide. As diabetes prevalence grows across both developed and emerging economies, the absolute number of patients progressing to gastroparesis is increasing, directly expanding the addressable treatment population. Aging populations, lifestyle-related risk factors, and limited access to early diabetes management in certain regions further exacerbate this trend, strengthening long-term demand for gastroparesis therapies.

Furthermore, the rising disease awareness among healthcare professionals and improvements in diagnostic protocols are significantly improving detection rates of diabetic gastroparesis. Enhanced clinical guidelines, greater use of gastric emptying studies, and increased differentiation from overlapping gastrointestinal disorders are enabling earlier and more accurate diagnosis. Growing education initiatives, specialist referrals, and improved access to gastroenterology services are translating into higher treatment initiation rates. Together, expanding diabetes prevalence and improved diagnostic recognition are accelerating patient identification, treatment uptake, and sustained growth in the global diabetic gastroparesis market.

Restraints - Clinical and Economic Barriers Limiting Market Adoption

The market continues to face significant clinical and economic constraints that limit broader treatment adoption. Currently available pharmacological therapies often demonstrate variable efficacy across patient populations, with many patients experiencing only partial or temporary symptom relief. In addition, safety concerns related to long-term drug use, including neurological, cardiovascular, and gastrointestinal adverse effects, reduce treatment adherence and lead to frequent therapy discontinuation. These limitations highlight the lack of highly effective, well-tolerated medications, particularly for chronic disease management, and contribute to persistent unmet clinical needs.

Moreover, the high cost of advanced treatment options presents a substantial barrier, especially in cost-sensitive and emerging markets. Endoscopic interventions such as G-POEM and device-based therapies like gastric electrical stimulation require specialized infrastructure, skilled clinicians, and expensive equipment, restricting widespread adoption. Furthermore, underdiagnosis remains a critical challenge, as gastroparesis symptoms often overlap with other gastrointestinal disorders, delaying accurate diagnosis and treatment initiation. Together, these clinical, economic, and diagnostic barriers continue to restrain market growth despite rising disease prevalence.

Opportunity - Advancements in Targeted Therapies and Minimally Invasive Interventions

The development of novel targeted therapies represents a significant growth opportunity in the diabetic gastroparesis market, as current treatment options fail to adequately address the complex and multifactorial nature of the disease. Innovation in next-generation prokinetic agents, neuromodulators, and symptom-specific drugs is gaining momentum, with several candidates aiming to improve gastric motility while minimizing systemic side effects. Advances in molecular targeting, improved drug delivery mechanisms, and better understanding of gut-brain signaling pathways are enabling the development of therapies with enhanced efficacy and safety profiles, potentially transforming long-term disease management and improving patient adherence.

Furthermore, the expanding adoption of minimally invasive interventions is opening new revenue streams across hospital and specialty care settings. Procedures such as gastric peroral endoscopic myotomy (G-POEM) and next-generation gastric electrical stimulation devices are gaining clinical acceptance for patients with refractory symptoms who do not respond to pharmacological therapy. Improved procedural outcomes, shorter recovery times, and growing specialist expertise are supporting wider adoption. As training programs expand and clinical evidence strengthens, these minimally invasive solutions are expected to play an increasingly important role in the future treatment landscape.

Category-wise Analysis

By Treatment Type, Pharmaceutical Drugs Dominate Globally Owing to High Clinical Utilization and First-Line Therapy Preference

The pharmaceutical drugs segment is projected to dominate the global diabetic gastroparesis market in 2026, accounting for a revenue share of 58.7%. This dominance is primarily driven by the widespread use of drug therapy as the first-line treatment option for managing symptoms such as nausea, vomiting, bloating, and delayed gastric emptying in diabetic patients. Prokinetic agents, antiemetics, and symptom-modulating drugs are routinely prescribed across mild to moderate disease stages, ensuring consistent and recurring demand.

High patient dependence on long-term medication, ease of administration, broader physician familiarity, and availability of approved therapies across major markets further support segment leadership. Additionally, ongoing clinical development of novel oral formulations and improved safety profiles continues to reinforce the strong utilization of pharmaceutical drugs in routine diabetic gastroparesis management.

By Disease Type, Compensated Gastroparesis Dominates Globally Owing to a Larger Diagnosed Population and Long-Term Disease Management

The compensated gastroparesis segment is projected to dominate the global diabetic gastroparesis market in 2026, accounting for a significant revenue share of 64.2%. This leadership is attributed to the larger diagnosed patient population experiencing manageable symptoms that can be controlled through dietary modification, pharmacological therapy, and routine clinical monitoring. Most diabetic gastroparesis patients fall within this category, enabling sustained treatment continuity and higher cumulative healthcare spending.

Patients with compensated gastroparesis typically require long-term symptom control rather than acute intervention, driving repeated physician visits and prolonged drug utilization. Improved diagnostic awareness, earlier disease detection, and structured disease management protocols further contribute to higher treatment volumes.

By End-user, Hospitals Dominate Globally Due to High Patient Volumes and Chairside Imaging Adoption

The hospitals segment is expected to dominate the global diabetic gastroparesis market in 2026, capturing a revenue share of 54.8%. Hospitals serve as the primary care setting for diagnosis, treatment initiation, and management of moderate to severe diabetic gastroparesis cases, particularly those requiring multidisciplinary evaluation and advanced therapeutic interventions. High patient inflow, access to specialist gastroenterologists, and availability of diagnostic modalities such as gastric emptying studies support strong utilization.

Additionally, hospitals are the leading adopters of advanced treatment options, including gastric electrical stimulation and endoscopic procedures for refractory patients. Integrated care models, better reimbursement coverage, and the ability to manage complications associated with diabetes continue to reinforce hospitals as the dominant end-user segment in the global diabetic gastroparesis market.

Region-wise Insights

North America Diabetic Gastroparesis Market Trends

North America is expected to maintain its dominance in the global diabetic gastroparesis market, accounting for an estimated 47.5% market share, supported by a high and growing prevalence of diabetes, strong disease awareness among clinicians and patients, and a well-developed gastroenterology care infrastructure. The U.S. remains the primary contributor due to higher diagnosis rates, widespread availability of FDA-approved pharmacological therapies, and early adoption of advanced treatment options such as gastric electrical stimulation and endoscopic procedures for refractory diabetic gastroparesis cases.

The region also benefits from favorable reimbursement policies, strong penetration of specialty gastroenterology clinics, and extensive clinical research activity focused on gastrointestinal motility disorders. Increasing investment in drug development, improved diagnostic pathways, and expanding use of minimally invasive interventions continue to enhance treatment accessibility and outcomes, reinforcing North America’s long-term leadership position in the global diabetic gastroparesis market.

Europe Diabetic Gastroparesis Market Trends

Europe demonstrates steady and mature growth in the diabetic gastroparesis market, supported by well-established public healthcare systems, strong regulatory frameworks, and widespread access to specialty gastrointestinal care across countries such as Germany, the U.K., France, Italy, Spain, and the Nordic region. Rising diabetes prevalence, improved disease recognition, and consistent demand for pharmacological management of chronic gastroparesis symptoms are key factors sustaining market expansion.

European healthcare systems place strong emphasis on clinical efficacy, safety, and cost-effectiveness, driving sustained utilization of approved drug therapies while gradually increasing adoption of advanced endoscopic treatments for severe and treatment-resistant cases. Ongoing efforts to standardize diagnostic protocols, improve early intervention, and enhance cross-border healthcare access, particularly in Central and Eastern Europe continue to support moderate market growth despite reimbursement constraints and pricing pressures in certain countries.

Asia Pacific Diabetic Gastroparesis Market Trends

Asia Pacific is projected to be the fastest-growing region, registering a CAGR of approximately 7.2%, driven by rapidly rising diabetes prevalence, expanding healthcare infrastructure, and improving awareness of diabetic complications affecting gastrointestinal function. Key markets including China, India, Japan, South Korea, and Southeast Asian countries are experiencing increasing diagnosis rates as access to specialist care and advanced diagnostic capabilities improves across both urban and semi-urban settings.

Government initiatives aimed at strengthening chronic disease management, growth of private hospitals and specialty clinics, and increasing affordability of pharmacological therapies are significantly accelerating market growth. In parallel, rising investments in advanced endoscopic procedures, expanding medical tourism, and improving regulatory clarity are positioning Asia Pacific as a critical growth engine for global diabetic gastroparesis drug developers and treatment solution providers.

Competitive Landscape

The global diabetic gastroparesis market is moderately to highly competitive, with key participants including EVOKE PHARMA®, Theravance Biopharma, Vanda Pharmaceuticals Inc., Renexxion Ireland Limited, Dr. Falk Pharma GmbH, and other emerging biopharmaceutical developers focused on gastrointestinal motility disorders. These companies strengthen their market positions through differentiated drug pipelines, proprietary formulations, targeted mechanisms of action, and established commercialization capabilities across hospital and specialty care settings.

Market participants are increasingly prioritizing the development of novel prokinetic agents, symptom-targeted therapies, and combination approaches to address significant unmet clinical needs. Strategic focus areas include late-stage clinical development, regulatory approvals in major markets, lifecycle management of approved drugs, geographic expansion into emerging economies, and partnerships with research institutions and specialty gastroenterology networks to accelerate adoption and sustain long-term growth.

Key Industry Developments:

- In May 2025, Renexxion Ireland Limited, in collaboration with Dr. Falk Pharma GmbH, announced the successful completion of patient enrollment for the global Phase 2b MOVE-IT study (NCT05621811) evaluating naronapride for gastroparesis. The trial reached its target enrollment of 320 patients, with topline results expected in the second half of 2025.

- In December 2024, Evoke Pharma reaffirmed its commitment to gastroparesis care following the FDA’s update on domperidone supply, highlighting GIMOTI® (metoclopramide) nasal spray as a critical treatment option. As the only FDA-approved nasal spray for acute and recurrent diabetic gastroparesis in adults, GIMOTI® offers a non-oral alternative that helps address treatment gaps and supports consistent symptom management when other therapies are limited.

- In December 2023, Vanda Pharmaceuticals Inc. (NASDAQ: VNDA) announced that the U.S. Food and Drug Administration (FDA) accepted the filing of its New Drug Application (NDA) for tradipitant for the treatment of gastroparesis symptoms.

Companies Covered in Diabetic Gastroparesis Market

- EVOKE PHARMA®

- Theravance Biopharma.

- Vanda Pharmaceuticals Inc.

- Renexxion Ireland Limited

- Dr. Falk Pharma GmbH

- Healio

- AdvaCare Pharma®

- AbbVie Inc.

- Bausch Health Companies Inc.

- AstraZeneca

- Neurogastrx, Inc.

- Processa Pharmaceuticals, Inc.

- Takeda Pharmaceutical Company Limited.

- Altos Therapeutics LLC

- Others

Frequently Asked Questions

The global diabetic gastroparesis market is projected to be valued at US$ 6.8 Bn in 2026.

Rising global diabetes prevalence and aging populations, plus increasing diagnosis rates and substantial unmet need for effective prokinetic therapies and minimally-invasive device options are driving growth of the global diabetic gastroparesis market.

The global diabetic gastroparesis market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Commercialize novel targeted prokinetics and minimally-invasive interventions (G-POEM, next-gen GES), while expanding into emerging markets and improved diagnostic/ care pathways.

EVOKE PHARMA®, Theravance Biopharma, Vanda Pharmaceuticals Inc., Renexxion Ireland Limited, Dr. Falk Pharma GmbH, and Healio are some of the key players in the diabetic gastroparesis market.