- Medical Devices

- Diabetic Markers Market

Diabetic Markers Market Size, Share, and Growth Forecast, 2026 – 2033

Diabetic Markers Market by Biomarker (Traditional, Novel, Inflammatory), Diabetes Type (Type 2 Diabetes, Type 1 Diabetes, Gestational Diabetes), End-user (Hospitals & Clinics, Diagnostic Laboratories, Home Care & Point-of-Care), and Regional Analysis 2026 – 2033

Diabetic Markers Market Size and Trends Analysis

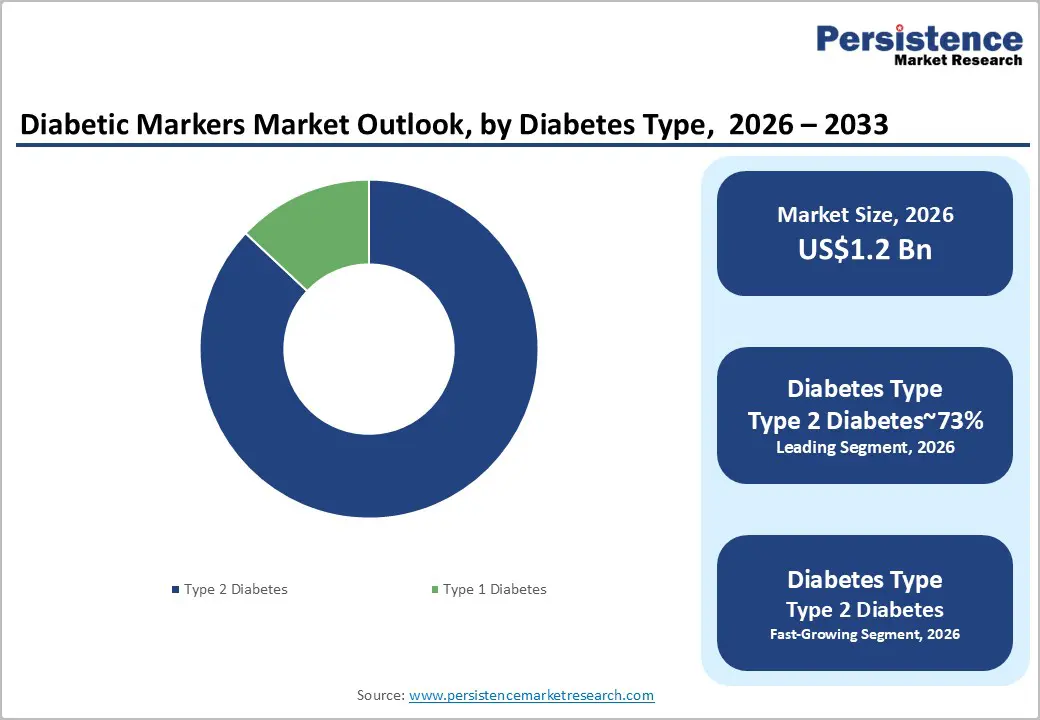

The global diabetic markers market size is likely to be valued at US$ 1.2 billion in 2026 and is expected to reach US$2.3 billion by 2033, growing at a CAGR of 10.3% during the forecast period from 2026 to 2033, driven by the escalating global prevalence of diabetes and a structural shift toward personalized medicine and predictive diagnostics.

As clinical guidelines increasingly emphasize early intervention, the demand for high-accuracy biomarkers has surged. Innovations in continuous monitoring and the integration of artificial intelligence (AI) into diagnostic panels are further catalyzing growth by enhancing the predictive value of traditional testing methods.

Key Industry Highlights:

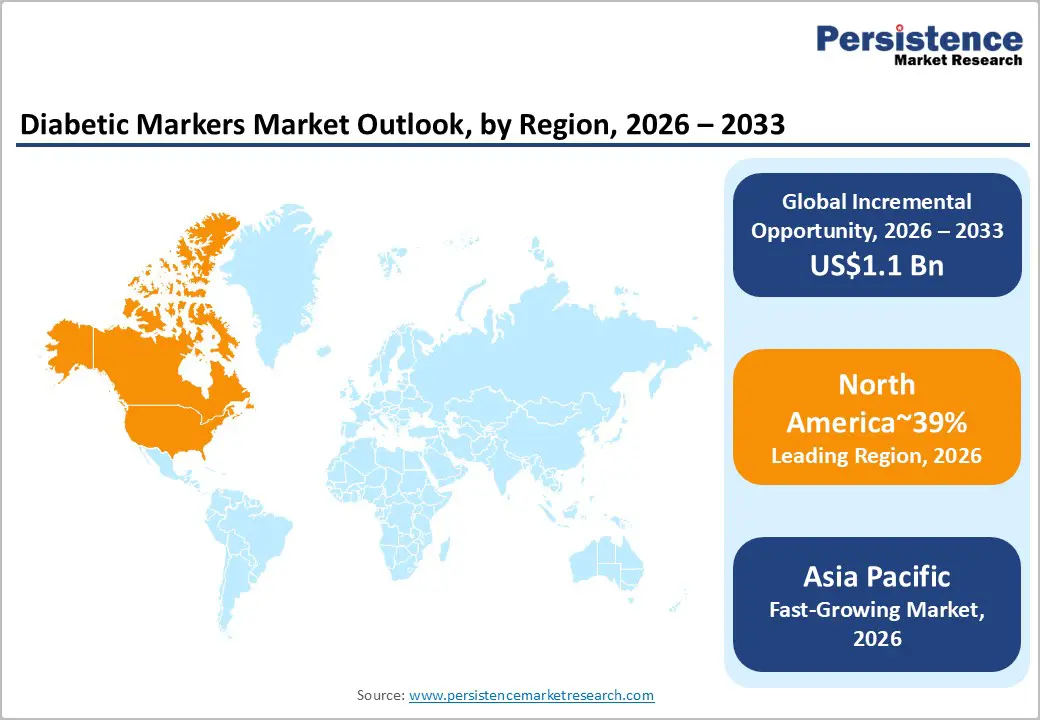

- Leading Region: North America is projected to lead due to strong reimbursement alignment, advanced diagnostic infrastructure, and integrated continuous glucose monitoring ecosystems, accounting for approximately 39% share in 2026, supported by high technology adoption and established laboratory networks anchored by players such as Abbott Laboratories and Dexcom.

- Fastest-Growing Region: Asia Pacific is anticipated to grow fastest due to expanding diagnostic penetration in China and India, supportive public screening programs, domestic manufacturing expansion under the National Medical Products Administration and Central Drugs Standard Control Organization, and rising adoption of digital health platforms across decentralized care settings.

- Leading Diabetes Type Segment: Type 2 diabetes is anticipated to dominate the market, accounting for 87% of the share, due to its overwhelming global patient prevalence and the need for continuous biochemical monitoring for lifelong glycemic management across healthcare systems.

- Leading End-user Segment: Hospitals & clinics are projected to dominate for operational simplicity, centralized infrastructure, established reimbursement pathways, and functional use across acute and chronic diabetes management, holding approximately 45% share in 2026.

| Key Insights | Details |

|---|---|

| Diabetic Markers Market Size (2026E) | US$1.2 Bn |

| Market Value Forecast (2033F) | US$2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Escalating Global Diabetes Prevalence and Expanding Diagnostic Screening Demand

The diabetic markers market is structurally driven by accelerating global diabetes prevalence across aging and urbanized populations. Epidemiological assessments from the International Diabetes Federation indicate a substantial rise in affected adults worldwide. A significant proportion of these individuals remain undiagnosed, intensifying systemic screening requirements. This latent patient pool embeds sustained demand across primary, secondary, and community care diagnostics. Type 2 diabetes represents the dominant clinical burden within overall diagnosed cases. Its chronic progression necessitates recurring biomarker surveillance across decentralized and centralized laboratory networks.

Persistent screening expansion strengthens reagent consumption and platform utilization rates. Routine monitoring protocols reinforce demand stability for glycated hemoglobin and plasma glucose assays. Technology evolution toward automated analyzers improves throughput efficiency while preserving diagnostic sensitivity standards. Regulatory frameworks increasingly mandate early detection pathways within national noncommunicable disease strategies. These policy interventions institutionalize population-level screening programs across emerging and developed markets. Laboratories respond by scaling biomarker portfolios to accommodate both traditional and advanced assays. This structural demand expansion enhances recurring revenue visibility across diagnostic supply ecosystems.

Technological Convergence and AI-Enabled Predictive Biomarker Integration

The diabetic markers market is advancing through the convergence of biotechnology and digital health infrastructures. Healthcare systems are transitioning from reactive glucose monitoring toward proactive risk stratification models. Adoption of predictive biomarker panels expands beyond conventional glycated hemoglobin assays. Novel markers such as glycated albumin and 1,5-Anhydroglucitol (1,5-AG) enhance short-term glycemic visibility. These biomarkers address temporal variability limitations inherent within traditional monitoring protocols. Clinical laboratories increasingly incorporate multiplex platforms capable of processing diverse metabolic indicators. This evolution broadens diagnostic scope from glucose quantification to integrated metabolic profiling.

Artificial intelligence integration within laboratory information systems amplifies analytical interpretation capabilities. Algorithmic models evaluate multidimensional biomarker datasets to forecast long-term complications. Predictive analytics enable earlier identification of nephropathy and cardiovascular risk trajectories. This shift elevates clinical utility beyond episodic testing toward longitudinal disease modeling. Technology upgrades consequently increase per test economic value across diagnostic workflows. Regulatory acceptance of digital decision support systems reinforces structured adoption pathways. Collectively, technological convergence strengthens value chain sophistication while reshaping revenue composition within diagnostic ecosystems.

Barrier Analysis – High Implementation Costs and Reimbursement Fragmentation

The diabetic markers market faces structural constraints from elevated implementation expenditures across advanced diagnostics. Novel biomarker panels require sophisticated analyzers, automation systems, and specialized reagent chemistries. Inflammatory indicators such as hs-CRP and Interleukin-6 (IL-6) necessitate validated assay platforms. These infrastructure requirements materially increase capital intensity compared with conventional glucose testing. Smaller laboratories encounter financing limitations when upgrading legacy diagnostic equipment. Procurement cycles lengthen as institutions evaluate return on investment assumptions.

Reimbursement disparities further constrain diffusion across diverse healthcare financing systems. Emerging economies lack standardized coverage frameworks for advanced biomarker evaluations. This restricts utilization to self-paying patients and high income urban segments. In developed markets, payer policy revisions lag behind biomarker innovation cycles. Classification of emerging assays under experimental categories delays reimbursement approvals. These dynamics shift cost burdens toward providers and compress operating margins.

Interoperability Gaps and Fragmented Clinical Data Architectures

The diabetic markers market encounters structural friction from fragmented digital health infrastructures. Continuous glucose monitoring platforms operate on proprietary data architectures across manufacturers. Hospital electronic health record systems frequently lack harmonized interoperability standards. This absence of standardized exchange protocols constrains seamless biomarker data aggregation. Clinicians therefore, access fragmented datasets rather than longitudinal metabolic profiles. Incomplete integration limits contextual interpretation within routine clinical workflows. Consequently, diagnostic insights remain underleveraged despite technological sophistication.

Data silos introduce operational inefficiencies across laboratories, device vendors, and care providers. Manual data reconciliation increases administrative burden and workflow latency. Clinical decision support systems struggle to process heterogeneous data formats. Regulatory frameworks emphasize data privacy compliance, further complicating cross-platform connectivity. Integration costs rise as institutions deploy middleware and interface solutions. These additional expenditures reduce margin realization within digitally enabled diagnostics. Collectively, interoperability gaps delay value chain optimization and impede comprehensive decision support adoption.

Opportunity Analysis – Decentralization of Diagnostics and Point of Care Biomarker Expansion

The diabetic markers market is structurally influenced by healthcare delivery decentralization trends. Home based monitoring models are reshaping diagnostic consumption patterns across chronic disease management. Demand is expanding for portable platforms capable of measuring diverse metabolic biomarkers. Current point-of-care systems primarily focus on capillary glucose quantification. Expanding assay menus toward fructosamine and C-peptide enhances clinical decision depth. Such diversification supports longitudinal monitoring outside centralized laboratory infrastructures.

This realignment accompanies migration toward compact and user-friendly diagnostic technologies. Device miniaturization requires integrated biosensor innovation and reagent stabilization advancements. Regulatory pathways for home use diagnostics mandate stringent usability and accuracy validation. Distribution channels increasingly shifting toward pharmacy networks and digital commerce ecosystems. Reduced hospital dependence modifies reimbursement models and procurement structures. Manufacturers benefit from recurring consumable demand embedded within decentralized testing routines. Collectively, point of care expansion diversifies revenue streams while broadening diagnostic accessibility.

Convergence of Novel Biomarkers and Precision Analytics

The diabetic markers market is evolving toward integrated predictive biomarker panels supporting precision medicine frameworks. Targeted subsets within advanced diagnostics are projected to represent significant incremental revenue pools. These panels combine metabolic, inflammatory, and genetic indicators for multidimensional risk stratification. Convergence with artificial intelligence platforms enhances analytical sensitivity and interpretive accuracy. Algorithmic refinement improves complication forecasting across nephropathy and cardiovascular pathways. Such capabilities reposition biomarkers from monitoring tools to proactive therapeutic decision enablers. This evolution strengthens clinical reliance on comprehensive profiling rather than isolated glycemic metrics.

Strategic partnerships between diagnostic developers and artificial intelligence firms accelerate translational deployment. Collaborative models integrate data science expertise with laboratory assay innovation. Research investment in pharmacogenomics expands personalization of antidiabetic treatment pathways. Regulatory scrutiny increasingly evaluates algorithm transparency and clinical validation robustness. Capital allocation shifts toward high value assay development with scalable digital integration. Margin structures improve through differentiated premium panels with enhanced predictive capability. Collectively, biomarker convergence restructures competitive dynamics within advanced diabetic diagnostics ecosystems.

Category–wise Analysis

Diabetes Type Insights

Type 2 diabetes is anticipated to dominate, accounting for 87% of the market in 2026, due to overwhelming patient prevalence and continuous monitoring requirements across global healthcare systems. Demand is driven, as most diabetes patients require lifelong biochemical monitoring for glycemic management. Biomarkers such as HbA1c, fasting plasma glucose, and postprandial glucose form the clinical backbone of diagnosis, disease staging, and long-term therapeutic evaluation. Healthcare institutions rely heavily on these markers because they offer standardized, reproducible measures of metabolic control. Global clinical guidelines from organizations such as the International Diabetes Federation and the American Diabetes Association reinforce HbA1c and plasma glucose as the primary biochemical indicators used across screening and monitoring pathways. High disease prevalence linked to obesity, sedentary lifestyles, and aging populations continues to expand the testing base. Laboratory networks and hospital diagnostic units, therefore, maintain strong operational dependence on routine glycemic biomarker assays.

Type 2 Diabetes is expected to remain the fastest-growing, driven by technological integration, which further strengthens the biomarker ecosystem supporting. Continuous glucose monitoring platforms such as Dexcom G7 and FreeStyle Libre convert glucose biomarker measurements into continuous physiological data streams, allowing clinicians to track glycemic variability rather than isolated laboratory readings. These systems extend the practical utility of glucose biomarkers by enabling real-time metabolic surveillance and treatment adjustments. Pharmaceutical innovation also reinforces biomarker monitoring requirements because advanced therapies rely on precise glycemic indicators to guide dosing and response evaluation. Drugs including Ozempic, Mounjaro, and Jardiance increasingly depend on HbA1c trends and glucose metrics to assess therapeutic performance across patient populations. This convergence of high patient volume and standardized biochemical indicators continues to sustain demand for diagnostic biomarkers globally.

End-user Insights

Hospitals and Clinics are expected to lead, accounting for approximately 45% share in 2026, underpinned by integrated diagnostic workflows and centralized laboratory infrastructure across acute care networks. Initial diabetes diagnoses and complex biomarker panels are predominantly executed within hospital-based laboratories equipped for high-throughput immunoassays and inflammatory marker analysis. Institutional compliance requirements and multidisciplinary care pathways reinforce reliance on structured testing environments. Organizations such as the Organization for Economic Co-operation and Development highlight the concentration of advanced screening capabilities within formal clinical facilities. Leading diagnostic suppliers, including F. Hoffmann-La Roche and Siemens Healthineers, anchor enterprise-grade analyzers within hospital ecosystems. High patient inflow and bundled care reimbursement models sustain volume-driven utilization.

The home care and point of care segment is expected to be the fastest-growing, driven by decentralized monitoring preferences and digital health integration across chronic disease management. Post-pandemic behavioral shifts accelerated acceptance of self-testing and remote consultation models. Portable biosensors and smartphone-connected devices enable real-time transmission of glycemic data to clinicians. Companies such as Abbott Laboratories and Dexcom expand continuous glucose monitoring ecosystems beyond institutional settings. Advancements in miniaturized assays improve analytical reliability within non-laboratory environments. Telehealth platforms integrate biomarker dashboards, reducing dependency on in-person visits.

Regional Insights

Asia Pacific Diabetic Markers Market Trends

Asia Pacific is expected to register the fastest growth trajectory in the diabetic markers market, led by China and India as structural demand accelerators. The region functions as the global volume engine, driven by large undiagnosed populations, rapid urbanization, and expanding digital health penetration. Demand expansion is anchored in the transition from undiagnosed to formally diagnosed patients, creating sustained uptake of traditional markers such as HbA1c and fasting plasma glucose. Urban middle-income cohorts are also moving toward continuous glucose monitoring and novel biomarker panels, reflecting a dual-track adoption curve.

Strategic industrial alignment is reshaping the competitive landscape. Abbott Laboratories has expanded ecosystem integration in India through collaboration with Novo Nordisk, linking sensor data with connected insulin platforms to improve therapy adherence. Roche Diagnostics has reinforced localization strategies in China to enhance supply resilience and affordability across secondary cities. Digital health momentum is further strengthened by regulatory clearance granted to Tencent Healthcare for AI-enabled retinal and biomarker interpretation, enabling scalable rural screening. Regulatory oversight from the National Medical Products Administration and the Central Drugs Standard Control Organization is encouraging domestic manufacturing while intensifying price discipline through procurement reforms. Asia Pacific, therefore combines structural volume expansion with rapid digital convergence, positioning it as the primary global growth catalyst.

North America Diabetic Markers Market Trends

North America is expected to remain the leading regional market, accounting for approximately 39% of the global share in 2026, supported by deep reimbursement alignment, advanced diagnostic infrastructure, and a highly integrated diabetes technology ecosystem. The region is positioned to sustain structural dominance through strong convergence between continuous glucose monitoring, multi-marker laboratory panels, and AI-enabled clinical interpretation. Favorable coverage expansion by the Centers for Medicare & Medicaid Services is expected to institutionalize recurring utilization across broader type 2 populations, reinforcing predictable revenue cycles. Enterprise laboratories such as Quest Diagnostics and Labcorp are anticipated to standardize integrated diabetes panels, embedding novel biomarkers into routine preventive screening. Consolidated platform leadership from Abbott Laboratories and Dexcom is expected to strengthen ecosystem lock-in across payers, providers, and digital health networks.

The U.S. is expected to anchor regional momentum by shaping reimbursement architecture, regulatory velocity, and venture capital concentration within diabetes diagnostics. Accelerated review mechanisms under the Food and Drug Administration are anticipated to streamline software-based biomarker approvals, enabling faster commercialization cycles. Federal research prioritization through the National Institutes of Health is projected to sustain translational pipelines linking pharmacotherapy with predictive marker analytics. Strategic integration between therapeutics and diagnostics, including closed-loop systems from Medtronic, is expected to reinforce bio-convergent care models. Expanding adoption of AI-driven interpretation platforms is likely to convert raw glucose streams into risk-adjusted clinical decision tools.

Europe Diabetic Markers Market Trends

Europe is expected to remain a mature and structurally stable market, supported by regulatory harmonization, universal healthcare coverage, and established laboratory networks across major economies. The region is positioned to sustain steady demand through replacement cycles and compliance-driven upgrades under the European Union Medical Device Regulation and CE marking frameworks, which standardize commercialization pathways across member states. Health systems are anticipated to prioritize long-term cost containment, reinforcing the adoption of predictive and complication-focused biomarkers that mitigate hospitalization burdens. Integrated public reimbursement structures are likely to favor clinically validated multi-marker panels embedded within routine preventive screening. Commercial alignment approaches are expected to align portfolios with digital interoperability mandates and sustainability objectives, strengthening lifecycle optimization rather than greenfield expansion. This disciplined procurement environment preserves margin stability while moderating rapid volume acceleration.

Germany is expected to function as the regional anchor, shaping procurement standards, technology validation benchmarks, and reimbursement discipline across the bloc. The country’s statutory insurance architecture is projected to reinforce evidence-based adoption of novel renal and cardiovascular risk markers within structured diabetes management programs. Industrial strength in laboratory instrumentation and diagnostics manufacturing is likely to support localized production and cross-border export resilience. Strategic investment in digital health infrastructure is anticipated to expand integration between hospital laboratories and outpatient monitoring platforms. As interoperability requirements tighten and value-based evaluation frameworks deepen, Germany is positioned to influence vendor strategy, pricing discipline, and innovation sequencing across the broader European market.

Competitive Landscape

The global diabetic markers market is moderately consolidated, with leadership concentrated among multinational diagnostics and device manufacturers, including Abbott Laboratories, F. Hoffmann-La Roche, Dexcom, Medtronic, LifeScan, and Siemens Healthineers. The leading cohort collectively accounts for a substantial share of global revenues, reflecting entrenched installed bases, regulatory depth, and procurement alignment across hospital and reference laboratory networks. Their influence extends beyond product breadth to include assay standardization, automation platforms, and connected glucose monitoring ecosystems.

The novel biomarker segment remains comparatively fragmented, characterized by emerging biotechnology firms specializing in genomic, proteomic, and metabolomic panels targeting precision stratification. Competitive positioning across the broader market is defined by technological differentiation and ecosystem integration capability rather than single-test dominance. Smaller innovators pursue vertical specialization, focusing on phenotype-specific diagnostics or AI-enabled interpretation layers.

Key Industry Developments:

- In February 2026, Abbott India and Novo Nordisk India launched a strategic collaboration to commercialize Extensior® semaglutide. for advanced type 2 diabetes management. This partnership leverages Abbott’s extensive distribution network to broaden access to GLP-1 therapy across India, offering patients significant HbA1c reduction, weight-loss benefits, and reduced cardiovascular risks.

- In December 2025, Dexcom launched the G7 15-Day Continuous Glucose Monitoring (CGM) system in the U.S. following earlier FDA clearance. The extended wear-time reduces the frequency of sensor changes, improving cost-effectiveness and user convenience for adults with diabetes.

- In April 2025, Dexcom strengthened its continuous glucose monitoring portfolio after the U.S. Food and Drug Administration cleared the Dexcom G7 15 Day Continuous Glucose Monitoring System, introducing the longest-lasting CGM sensor currently available for adults. The upgraded system extends sensor wear time to 15.5 days and achieves an improved Mean Absolute Relative Difference (MARD) of 8.0%, enabling the company to enhance product accuracy, reduce sensor replacement frequency, and minimize user discomfort while lowering sensor waste. This development reflects Dexcom’s strategic focus on advancing CGM technology and strengthening its competitive position in the diabetes monitoring market.

Companies Covered in Diabetic Markers Market

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd.

- Siemens Healthineers

- Danaher Corporation

- Dexcom, Inc.

- Medtronic plc

- Beckman Coulter

- Bio-Rad Laboratories

- LifeScan, Inc.

- Ascensia Diabetes Care

- Arkray, Inc.

- Becton, Dickinson and Company

- Nova Biomedical

- bioMérieux

- Ortho Clinical Diagnostics

- Sinocare Inc.

Frequently Asked Questions

The global diabetic markers market is projected to be valued at US$1.2 billion in 2026 and is expected to reach US$2.3 billion by 2033, driven by rising diabetes prevalence, expanding screening programs, and increasing adoption of predictive biomarker panels.

The growing incidence of type 2 diabetes across aging and urban populations is intensifying routine screening and long-term monitoring requirements. This structural demand reinforces recurring utilization of HbA1c, glucose, and advanced renal and inflammatory biomarkers across hospitals, diagnostic laboratories, and decentralized care settings.

The diabetic markers market is forecast to grow at a CAGR of 10.3% from 2026 to 2033, reflecting sustained demand for early detection, precision risk stratification, and AI-enabled diagnostic integration.

North America is the leading regional market, accounting for approximately 39% share, supported by advanced reimbursement frameworks, high penetration of continuous glucose monitoring systems, strong laboratory automation infrastructure, and regulatory alignment for digital diagnostic tools.

The diabetic markers market is moderately consolidated, with major participants including Abbott Laboratories, F. Hoffmann-La Roche, Dexcom, Medtronic, LifeScan, and Siemens Healthineers. These companies compete through integrated assay platforms, continuous monitoring ecosystems, global distribution networks, and sustained research investment in both traditional and novel biomarker development.