- Medical Devices

- Dental Biomaterials Market

Dental Biomaterials Market Size, Share, and Growth Forecast 2026 - 2033

Dental Biomaterials Market by Biomaterials Type (Metallic Biomaterials, Ceramic Biomaterials, Polymeric Biomaterials, Metal-Ceramic Biomaterials, Others), by Application (Implantology, Orthodontics, Prosthodontics, Others), by End User (Hospitals, Dental Clinics, Others), by Regional Analysis, 2026-2033

Dental Biomaterials Market Size and Trend Analysis

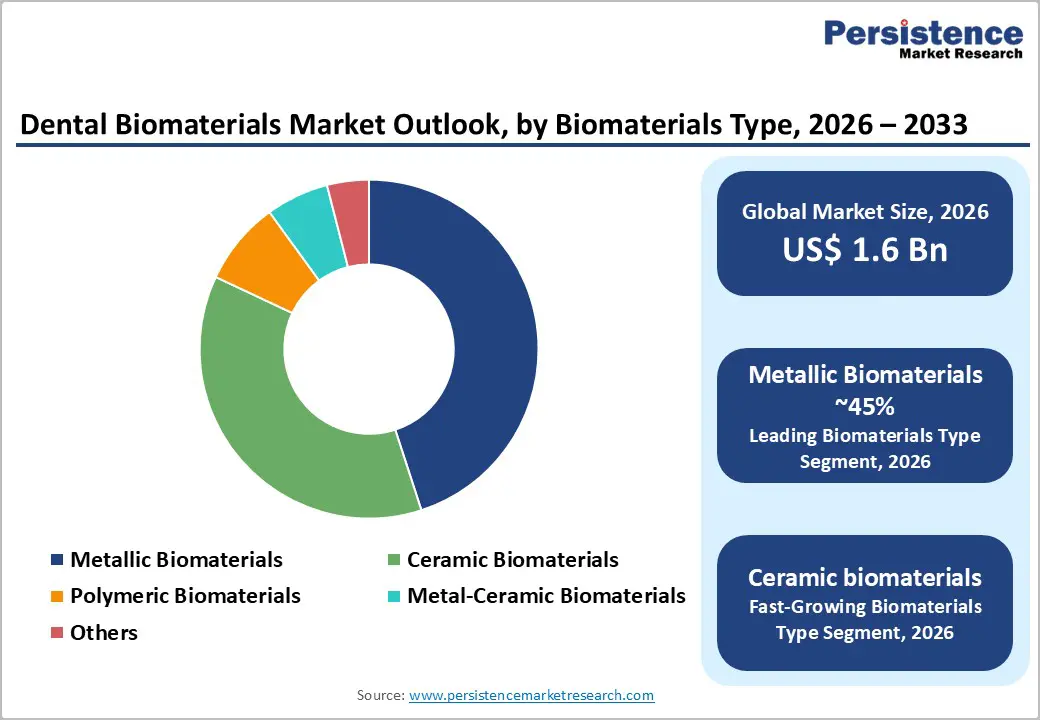

The global dental biomaterials market size is expected to be valued at US$ 1.6 billion in 2026 and projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The dental biomaterials market is experiencing steady growth, driven by the rising prevalence of dental disorders and the rapid expansion of the aging global population. As oral health issues such as tooth decay, periodontal disease, and tooth loss become more common, the need for effective restorative and replacement solutions has increased significantly. Advanced dental procedures, including implants, crowns, and prosthetics, are now considered essential for maintaining both functionality and quality of life. High incidence of dental conditions among adults has further accelerated demand for durable and long-lasting biomaterials. In parallel, the growing popularity of cosmetic dentistry is shaping market trends, with patients increasingly seeking aesthetically pleasing and biocompatible materials. Technological advancements in implant design and materials science continue to enhance treatment outcomes, supporting sustained adoption. These trends collectively position dental biomaterials as a critical component of modern dental care.

Key Market highlights

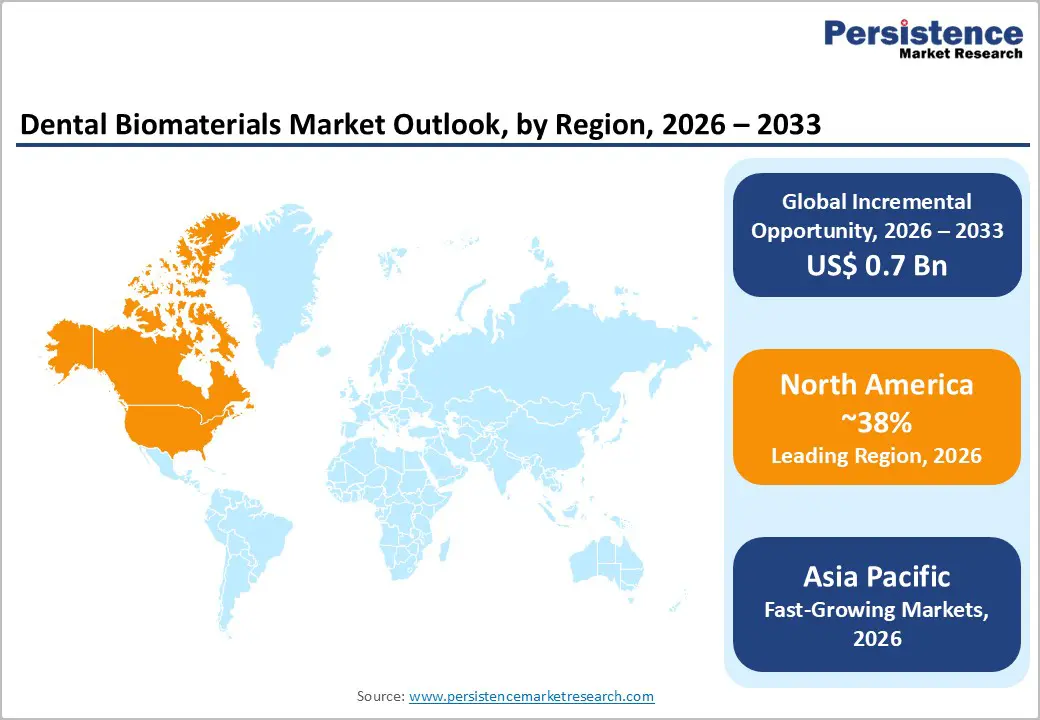

- North America dominates with 38% share in 2025, driven by advanced infrastructure and high dental disorder prevalence.

- Asia Pacific grows fastest at elevated CAGR through 2033, boosted by medical tourism and manufacturing in India, China.

- Metallic biomaterials lead Biomaterials Type at 45% share, excelling in implant strength and biocompatibility.

- Ceramic biomaterials expand rapidly with top CAGR, meeting aesthetic demands in restorative dentistry.

- Ceramic innovations offer premium opportunities in metal-free restorations for cosmetics-driven markets.

| Key Insights | Details |

|---|---|

| Dental Biomaterials Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Driver- Increasing Prevalence of Oral Disorders

The growing incidence of oral health conditions is a major force supporting expansion of the dental biomaterials market. Disorders such as dental caries, periodontal disease, tooth loss, oral infections, halitosis, and oral cancers are increasing across both developed and developing economies due to poor oral hygiene, high sugar consumption, tobacco use, aging populations, and limited preventive care in many regions. As awareness of oral health improves, patients are increasingly opting for clinical interventions rather than delaying treatment, leading to higher volumes of restorative, prosthetic, and implant-based procedures. Dental biomaterials play a critical role in these treatments, offering durability, biocompatibility, and long-term functional outcomes. Materials such as metals, ceramics, and polymers are widely used in fillings, crowns, bridges, dentures, bone grafts, and orthodontic applications.

Additionally, the rise in cosmetic dentistry procedures aimed at improving aesthetics has further increased the use of advanced biomaterials. The high success rates of modern dental procedures, combined with improved patient confidence in biomaterial safety and performance, continue to strengthen demand. Collectively, the expanding patient pool and rising procedural volumes are sustaining long-term growth of the global dental biomaterials market.

Restraint - Regulatory Complexity and Safety Challenges

Strict regulatory requirements and long approval timelines remain a significant constraint for the dental biomaterials market. Regulatory bodies impose rigorous standards related to material composition, mechanical strength, corrosion resistance, biocompatibility, and long-term safety before products can be commercialized. Compliance with evolving regulations increases development time and costs, particularly for innovative materials and modified formulations. Manufacturers are often required to conduct extensive clinical evaluations and post-market surveillance, adding financial and operational pressure. Smaller companies face greater difficulty navigating these processes, which limits competition and slows the entry of new technologies. In addition to regulatory hurdles, concerns related to long-term biocompatibility also restrict adoption of certain materials. Issues such as allergic reactions, inflammatory responses, material degradation, or ion release from metallic implants can negatively affect clinical outcomes and clinician confidence. Any safety-related incidents or product recalls can further reduce trust among dental professionals and patients. As expectations for material performance rise, companies must invest heavily in testing and quality assurance, increasing overall costs. These combined regulatory and safety challenges can delay innovation and limit the pace of market expansion.

Opportunity - Expansion in Emerging Markets via Medical Tourism

Emerging economies present strong growth opportunities for the dental biomaterials market, supported by improving healthcare infrastructure, rising disposable incomes, and expanding access to dental services. Countries in Asia-Pacific and parts of Latin America are witnessing rapid growth in dental clinics and specialty hospitals, alongside increasing awareness of oral health. Medical tourism is also accelerating demand, as international patients seek affordable yet high-quality dental treatments, including implants and cosmetic procedures. This trend creates opportunities for biomaterial manufacturers to supply cost-effective yet reliable solutions through local partnerships and regional production facilities. At the same time, innovations in ceramic biomaterials are opening new revenue streams. Advanced ceramics such as zirconia are gaining popularity due to their superior aesthetics, strength, and metal-free composition, making them ideal for crowns, bridges, and implants. Improvements in translucency and digital manufacturing compatibility have enhanced their clinical appeal. As patient preference shifts toward natural-looking and minimally invasive solutions, ceramic biomaterials are increasingly favored. Companies that invest in research, digital integration, and regional expansion are well positioned to capture demand in both premium and high-volume segments, driving sustained market growth.

Category-wise Insights

Biomaterials Type Analysis

Metallic biomaterials dominate the dental biomaterials market, accounting for approximately 45% of the total share in 2025. Their leadership is primarily driven by superior mechanical strength, durability, and excellent load-bearing capacity, making them highly suitable for demanding dental applications. Titanium and its alloys are the most widely used metallic materials, particularly in dental implants, due to their strong affinity for bone tissue and reliable osseointegration. These materials provide long-term structural stability and minimize implant failure risks, even under continuous masticatory stress. Dentists and oral surgeons favor metallic biomaterials because of their long clinical history, predictable performance, and well-established surgical protocols.

In addition, standardized manufacturing processes and consistent material quality have strengthened clinician confidence worldwide. Metallic biomaterials are extensively used in fixtures, abutments, and frameworks, especially in complex or full-arch restorations. Their compatibility with advanced surface treatments further enhances integration and healing outcomes. While alternative materials are gaining traction for aesthetic purposes, metallic biomaterials remain the preferred choice for strength-critical procedures, ensuring their continued dominance across implantology and restorative dentistry applications.

End User Analysis

Dental clinics account for the largest share of the dental biomaterials market, capturing approximately 55% of total demand in 2025. Their leadership is supported by high patient volumes and the increasing shift toward outpatient dental care settings. Clinics serve as the primary point of contact for routine and specialized dental procedures, including implants, crowns, bridges, and orthodontic treatments. The availability of advanced diagnostic tools and chairside technologies enable clinics to efficiently perform complex procedures using a wide range of biomaterials. Compared to hospitals, dental clinics offer greater convenience, shorter waiting times, and cost-effective treatment options, attracting a broader patient base. The growing number of private dental practices, especially in urban and semi-urban regions, has further strengthened this segment’s position.

Additionally, clinics are quick adopters of innovative biomaterials that enhance treatment precision and patient comfort. Their strong focus on cosmetic and restorative dentistry continues to drive consistent biomaterial consumption, reinforcing their dominance as the leading end-user segment in the market.

Regional Insights

North America Dental Biomaterials Market Trends and Insights

North America holds the leading position in the global dental biomaterials market, accounting for nearly 38% of total market share in 2025. The region’s dominance is supported by a highly developed dental care infrastructure, strong reimbursement frameworks, and early adoption of advanced treatment technologies. The United States plays a central role, driven by a high prevalence of oral health issues such as dental caries, periodontal disease, and tooth loss among adults. These conditions continue to generate sustained demand for restorative and implant-based procedures. Regulatory clarity and structured approval pathways encourage the introduction of innovative biomaterials, particularly in implants and prosthetics. Digital dentistry is widely integrated across dental practices, with CAD/CAM systems and chairside milling accelerating the use of ceramic biomaterials.

Additionally, a strong focus on cosmetic dentistry and minimally invasive procedures has expanded demand for high-performance, aesthetic materials. The presence of leading manufacturers, active clinical research, and continuous product innovation further strengthens market maturity. High patient awareness and willingness to invest in long-term dental solutions ensure stable growth across implantology, prosthodontics, and orthodontic applications in the region.

Asia Pacific Dental Biomaterials Market Trends and Insights

Asia Pacific is the fastest-growing regional market for dental biomaterials, driven by rapid urbanization, rising disposable incomes, and increasing awareness of oral health. Countries such as China, India, Japan, and several ASEAN nations are experiencing a sharp rise in dental procedures due to high prevalence of untreated oral disorders and expanding access to dental care services. India has emerged as a key destination for dental tourism, offering cost-effective implant and cosmetic treatments that attract international patients. China’s large population base and expanding domestic manufacturing capabilities are supporting high-volume demand for dental biomaterials across implants, crowns, and orthodontic applications. Japan stands out for its focus on precision dentistry and advanced ceramic materials, supported by strong technological expertise and aging demographics.

The region also benefits from lower production costs, enabling competitive pricing and export opportunities. Growing investments in private dental clinics and specialty centers are further strengthening consumption. As affordability and accessibility improve, Asia Pacific is expected to remain the primary growth engine for the global dental biomaterials market.

Competitive Landscape

Market Structure Analysis

The dental biomaterials market is moderately consolidated, with leading players maintaining strong positions through continuous innovation and broad product portfolios. Market leaders focus heavily on research and development, particularly in advanced ceramics, implant materials, and digitally compatible biomaterials. Strategic initiatives such as acquisitions, partnerships, and expansion into high-growth regions, especially Asia-Pacific, are widely adopted to strengthen global presence. Companies differentiate themselves through patented biocompatible materials, improved osseointegration technologies, and seamless integration with CAD/CAM and digital dentistry platforms. In parallel, emerging players are introducing flexible business models, including customized material solutions and digitally enabled prosthetics, intensifying competition and accelerating overall market evolution.

Key Market Developments

- In May 2023, Straumann announced its acquisition of GalvoSurge to expand its portfolio of innovative solutions for dental implants, particularly in the peri-implantitis cleaning segment. This strategic move highlights the increasing adoption of laser-based therapies for the effective management and treatment of peri-implantitis.

Companies Covered in Dental Biomaterials Market

- Geistlich Pharma, Inc.

- Zimmer Biomet

- 3 M Company

- Dentsply Sirona

- Institut Straumann AG

- Danaher Corporation (Nobel Biocare Services AG)

Frequently Asked Questions

The global Dental Biomaterials Market is expected to reach US$ 1.6 billion in 2026.

Key drivers include rising geriatric populations and dental disorders, with CDC noting 90% tooth decay in U.S. adults, boosting implant needs.

North America leads with 38% share in 2025, supported by innovation and high procedure volumes.

Innovations in ceramic biomaterials for aesthetics, growing at top CAGR, target metal-free restorations.

Leading players include Straumann Holding AG, Zimmer Biomet Holdings, Inc., and Dentsply Sirona, Inc..