- Healthcare IT

- Dental Simulator Market

Dental Simulator Market Size, Share, and Growth Forecast, 2026 – 2033

Dental Simulator Market by Product Type (Manikin-Based Dental Simulators (Phantom Heads), Virtual Reality (VR) Dental Simulators, Others), Component (Hardware, Software), End-user (Dental Schools, Hospitals, Dental Clinics, Others), and Regional Analysis for 2026 - 2033

Dental Simulator Market Share and Trends Analysis

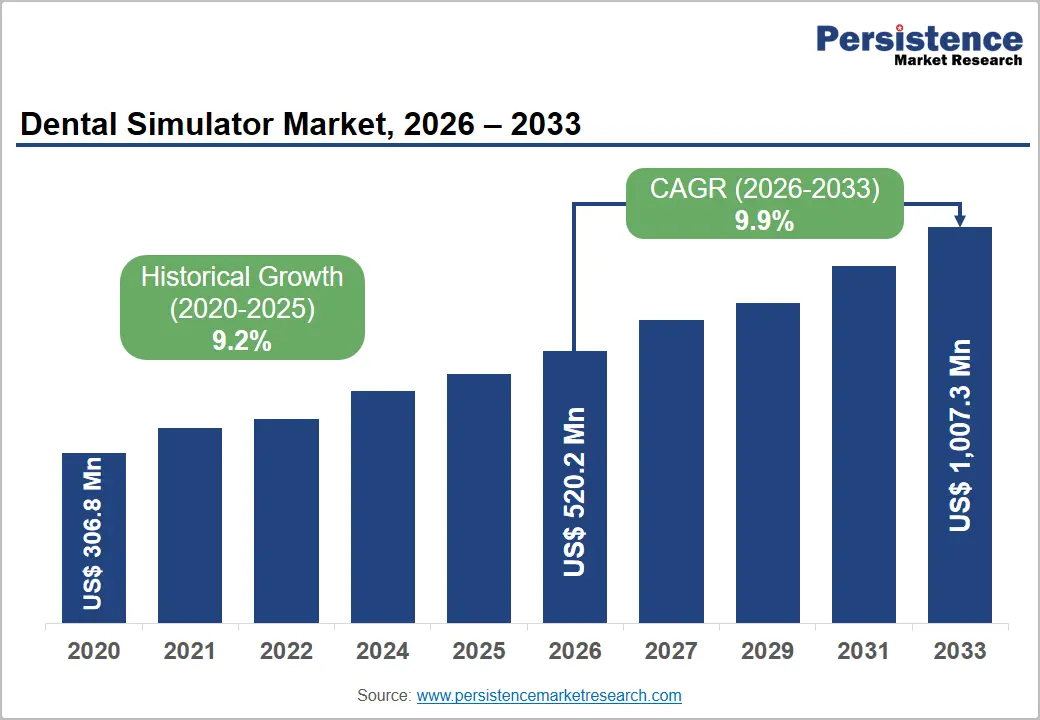

The global dental simulator market size is likely to be valued at US$520.2 million in 2026 and is estimated to reach US$1,007.3 million by 2033, growing at a CAGR of 9.9% during the forecast period 2026−2033, driven by increasing integration of digital learning technologies within dental education and clinical training environments. Rising enrollment in dental education programs is creating demand for advanced simulation platforms that improve procedural competency before patient interaction. Regulatory emphasis on patient safety and competency-based training is accelerating the adoption of virtual and haptic learning systems. Rapid advancements in virtual reality, artificial intelligence, and tactile feedback technologies are enhancing training accuracy and educational outcomes.

Key Industry Highlights:

- Leading Product Type: Manikin-based dental simulators (Phantom Heads) are set to hold around 38% revenue share in 2026, driven by widespread curriculum integration.

- Fastest-growing Product Type: Virtual reality (VR) dental simulators are projected to be the fastest-growing segment, driven by increasing immersive learning adoption.

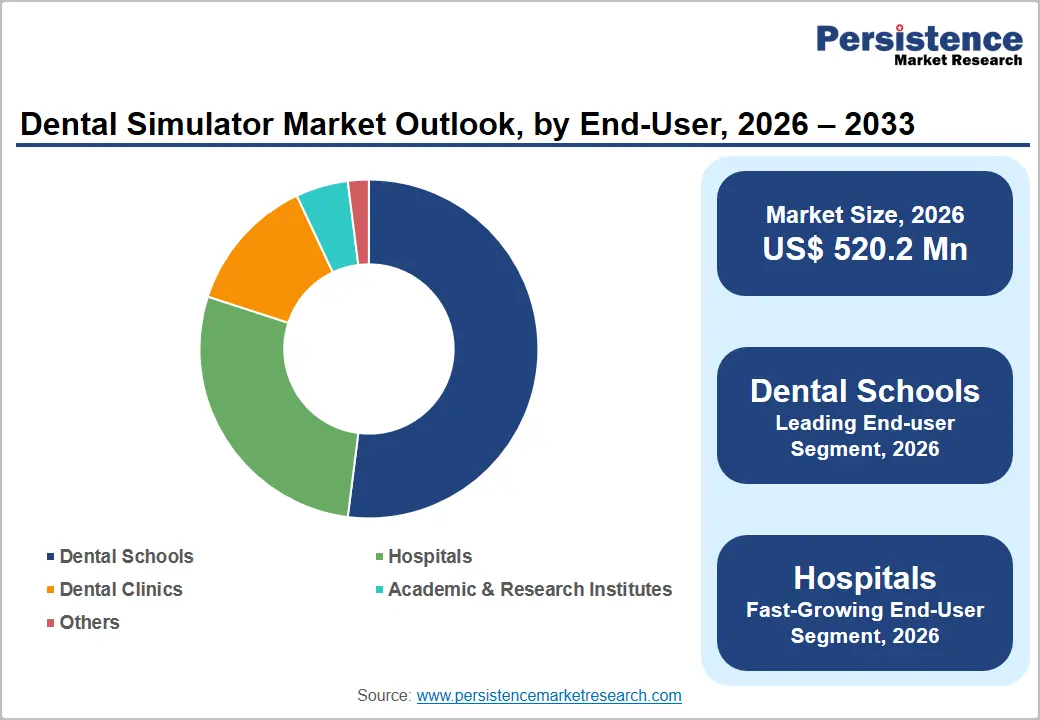

- Leading End-user: Dental schools are estimated to hold roughly a 52% revenue share in 2026, driven by expanding simulation-based education requirements.

- Fastest-Growing End-user: Hospitals are forecast to record the fastest growth, driven by rising clinician training initiatives.

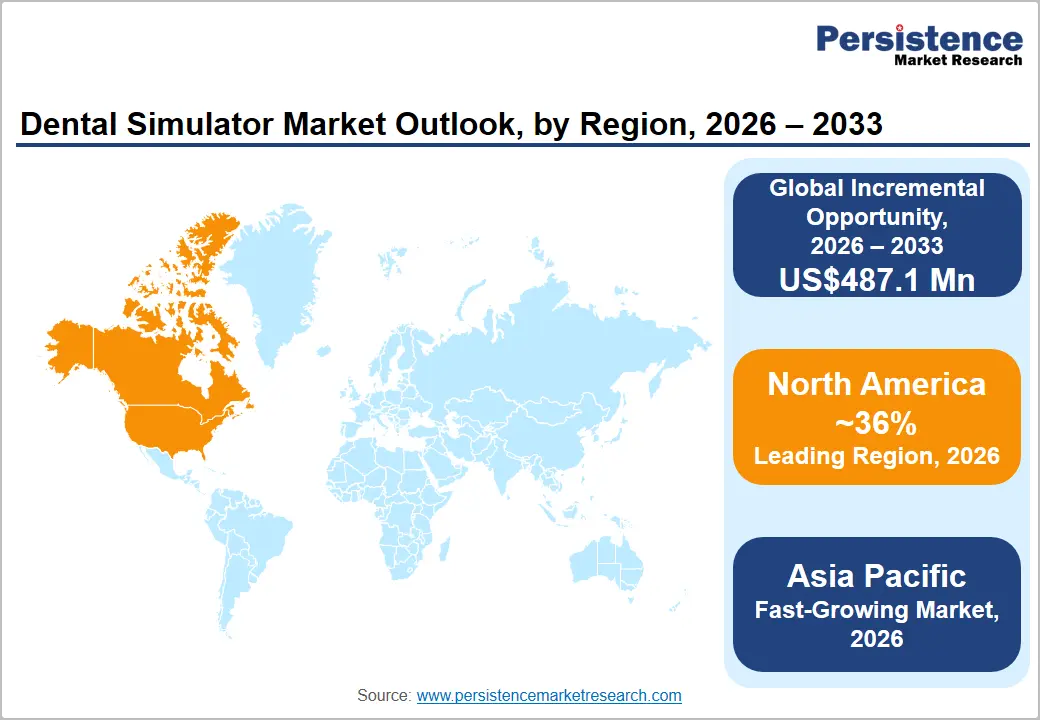

- Regional Leadership: North America is projected to capture roughly 36% of the market share by 2026, while Asia Pacific is also forecast to record the fastest growth due to expanding dental education infrastructure.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players including Dentsply Sirona, Virteasy, SimtoCare, and Nissin Dental Products focusing on technology advancement.

DRO Analysis

Driver - Rising Demand for Competency-Based Dental Education

Dental education institutions are increasingly adopting simulation-based learning to improve procedural accuracy and reduce training risks associated with live patient practice. Growing emphasis on evidence-based education has encouraged universities and accreditation bodies to incorporate simulation modules into curricula. Realistic training environments support skill development, improve confidence levels among students, and allow repeated practice without clinical consequences, resulting in greater investment in simulator technologies.

According to the National Center for Education Statistics (NCES), health profession enrollments across postsecondary institutions in the U.S. exceeded 3.4 million students in 2025. Growth in healthcare education enrollment is increasing pressure on institutions to provide standardized practical training experiences. Simulation systems address faculty shortages and clinical training limitations by enabling scalable learning environments capable of supporting larger student populations while maintaining consistent educational quality.

Restraint - High Capital Investment and Maintenance Requirements

Advanced simulation platforms require significant investment in hardware, software licensing, maintenance contracts, and periodic system upgrades. Budget constraints within educational institutions can delay procurement decisions, particularly among smaller dental schools and training centers. Long replacement cycles reduce purchasing frequency and create barriers to widespread deployment.

Specialized technical support requirements increase operating expenditures throughout the equipment lifecycle. Dependence on proprietary software ecosystems limits flexibility and raises total ownership costs. Elevated implementation expenses can reduce profit margins for providers and slow scalability across resource-constrained institutions seeking cost-effective training alternatives.

Opportunity - Expansion into Emerging Digital Dental Education Ecosystems

Growing investments in healthcare education infrastructure present significant opportunities for simulator providers. Educational institutions increasingly seek digital learning environments capable of supporting larger student cohorts while improving training quality. Strategic partnerships with universities, accreditation organizations, and professional associations can accelerate technology adoption and strengthen long-term revenue streams.

Government initiatives supporting healthcare workforce development are encouraging the modernization of training facilities. Development of subscription-based software platforms and cloud-enabled assessment tools can expand accessibility among institutions with limited capital budgets. Scalable digital learning ecosystems create pathways for recurring revenue generation while supporting broader penetration into underserved educational markets.

Category-wise Analysis

Product Type Insights

Manikin-based dental simulators (Phantom Heads) are anticipated to secure around 38% of the dental simulator market share in 2026, reflecting established adoption across dental schools and training centers requiring realistic procedural practice. Institutions continue using physical simulation platforms for foundational clinical education. Several university training laboratories maintain phantom head systems for operative dentistry instruction. Consistent curriculum integration supports sustained demand globally.

Virtual reality (VR) dental simulators are expected to be the fastest-growing segment, propelled by increasing adoption of immersive learning technologies that enhance procedural visualization and assessment capabilities. Advanced digital environments support repeated practice without material consumption. VR platforms developed by leading simulator manufacturers provide real-time feedback and competency tracking. Growing emphasis on digital education continues to strengthen deployment across institutions.

Component Insights

The hardware segment is poised to dominate with a forecast market share of over 64% in 2026, powered by demand for haptic devices, simulation workstations, tracking sensors, and physical training interfaces. Educational institutions prioritize infrastructure investment when establishing simulation laboratories. For example, advanced phantom head units and tactile feedback systems remain central training components. Strong equipment replacement cycles sustain revenue generation.

The software segment is estimated to be the fastest-growing segment, fueled by increasing demand for analytics, performance monitoring, artificial intelligence assessment tools, and cloud-based learning platforms. Educational institutions seek scalable solutions supporting remote training environments. Simulation software capable of recording procedural metrics enhances competency evaluation. Continuous innovation is accelerating software adoption across training ecosystems.

End-user Insights

Dental schools are likely to be the leading segment with a projected 52% of the dental simulator market share in 2026 due to extensive integration of simulation technologies within undergraduate and postgraduate dental education programs. Academic institutions require structured training environments supporting skill development. Universities increasingly incorporate virtual and haptic systems into preclinical curricula. Enrollment growth sustains procurement activity.

Hospitals are anticipated to be the fastest-growing segment, fueled by expanding focus on clinician training, continuing education, and procedural standardization initiatives. Healthcare organizations increasingly utilize simulation technologies to improve clinical competency and reduce procedural risks. Teaching hospitals are investing in advanced digital training laboratories. Rising workforce development requirements support strong adoption momentum during the forecast period.

Regional Insights

North America Dental Simulator Market Trends

North America is expected to lead with an estimated 36% of the dental simulator market share in 2026, supported by advanced dental education infrastructure, strong adoption of simulation-based learning, and continuous investment in digital healthcare training technologies. The presence of leading companies, including Dentsply Sirona and SimtoCare, supports innovation and commercialization activities.

U.S. Dental Simulator Market Insights

The U.S. is projected to account for nearly 85% of North America revenue share in 2026, supported by extensive dental school networks and significant investment in healthcare education technologies. Expansion of simulation laboratories within universities is increasing adoption of advanced training platforms. Continuous product innovation by industry participants is strengthening digital learning integration and competency assessment capabilities across educational environments.

Canada Dental Simulator Market Insights

Canada is expected to contribute around 15% of North America revenue share in 2026, driven by the modernization of healthcare education infrastructure and the growing implementation of digital learning solutions. Academic institutions are increasingly adopting virtual and haptic simulators to improve clinical training outcomes. Government support for workforce development programs is creating favorable conditions for continued technology adoption.

Europe Dental Simulator Market Trends

Europe is anticipated to hold approximately 26% of the dental simulator market share in 2026, supported by established healthcare education systems, strong regulatory focus on clinical competency, and increasing investment in simulation-based training. Universities and professional training centers are integrating advanced digital platforms to improve procedural accuracy and educational efficiency. Technology providers continue expanding partnerships with academic institutions across the region.

Germany Dental Simulator Market Insights

Germany is forecast to represent nearly 22% of Europe's revenue share in 2026, supported by advanced healthcare infrastructure and strong technology adoption across educational institutions. Investment in digital laboratories and immersive learning platforms is increasing the demand for simulation solutions. Collaboration between universities and technology developers continues to support innovation and implementation of modern training methodologies.

U.K. Dental Simulator Market Insights

The U.K. is expected to account for approximately 18% of Europe's revenue share in 2026, driven by ongoing modernization of dental education facilities and increasing focus on competency-based training frameworks. Adoption of virtual simulation platforms is improving practical learning experiences. Strategic collaborations between educational institutions and solution providers are strengthening technology deployment across academic environments.

Asia Pacific Dental Simulator Market Trends

Asia Pacific is forecast to be the fastest-growing market for dental simulators, driven by expanding dental education infrastructure, increasing healthcare expenditure, and rapid digitalization of training environments. Rising enrollment in dental programs and government support for healthcare workforce development are creating substantial opportunities for simulator deployment across universities and teaching institutions.

China Dental Simulator Market Insights

China is projected to contribute nearly 34% of Asia Pacific revenue in 2026, supported by large-scale expansion of dental education capacity and increasing investment in advanced healthcare training technologies. Universities are strengthening simulation laboratory infrastructure to improve practical skill development. Domestic manufacturing capabilities and technology partnerships are enhancing accessibility to advanced training solutions.

India Dental Simulator Market Insights

India is expected to account for approximately 19% of Asia Pacific revenue in 2026, driven by rising numbers of dental colleges and growing emphasis on technology-enabled education. Expansion of healthcare training infrastructure is increasing demand for simulation platforms. Government initiatives focused on improving educational quality and workforce preparedness are supporting broader adoption of virtual and haptic learning systems.

Competitive Landscape

The global dental simulator market is moderately fragmented, characterized by a combination of established healthcare technology providers and specialized simulation developers. Competition centers on innovation, training realism, software capabilities, and integration of immersive technologies. Key participants include Dentsply Sirona, Virteasy, SimtoCare, and Nissin Dental Products.

Companies are investing in virtual reality, haptic feedback systems, and artificial intelligence-enabled assessment platforms to strengthen competitive positioning. Strategic collaborations with universities and healthcare institutions support product validation and adoption. Continuous software upgrades and curriculum-focused solutions remain important factors influencing market differentiation and customer retention.

Key Industry Developments:

- In February 2026, Stratasys launched a multi-material 3D-printed dental anatomical model preset for simulation-based training and clinical education, strengthening adoption of realistic, technology-driven learning environments across dental schools and training centers.

Companies Covered in Dental Simulator Market

- Dentsply Sirona

- SimtoCare

- Virteasy

- Nissin Dental Products

- KaVo Dental

- 3D Systems

- Realityworks

- Kyoto Kagaku

- Dental Education Laboratories

- Navadha Enterprises

- Image Navigation Ltd.

- Columbia Dentoform

- Zhengzhou Linker Medical Equipment

- HRV Simulation

Frequently Asked Questions

The global dental simulator market is projected to reach US$520.2 million in 2026.

Rising adoption of simulation-based dental education, increasing demand for competency-focused clinical training, and advancements in virtual reality and haptic technologies drive market growth.

The dental simulator market is poised to witness a CAGR of 9.9% from 2026 to 2033.

Integration of artificial intelligence-driven assessment tools and expansion of digital simulation platforms across emerging dental education institutions create significant market opportunities.

Some of the key market players include Dentsply Sirona, Virteasy, SimtoCare, and Nissin Dental Products.