- Medical Devices

- North America Dental 3D Printing Market

North America Dental 3D Printing Market Size, Share, and Growth Forecast, 2026 – 2033

North America Dental 3D Printing Market by Product Type (Printers/Hardware, Materials, Services), Application (Prosthodontics, Orthodontics, Implantology), Technology (Stereolithography, Digital Light Processing, Others), and Country Analysis 2026 – 2033

North America Dental 3D Printing Market Size and Trends Analysis

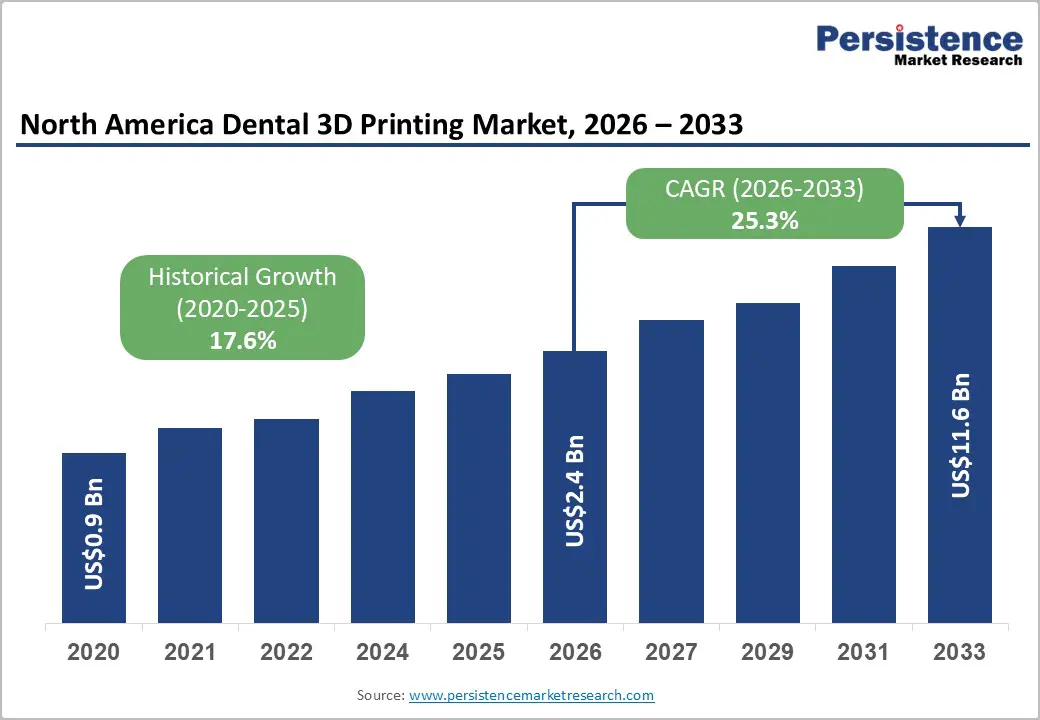

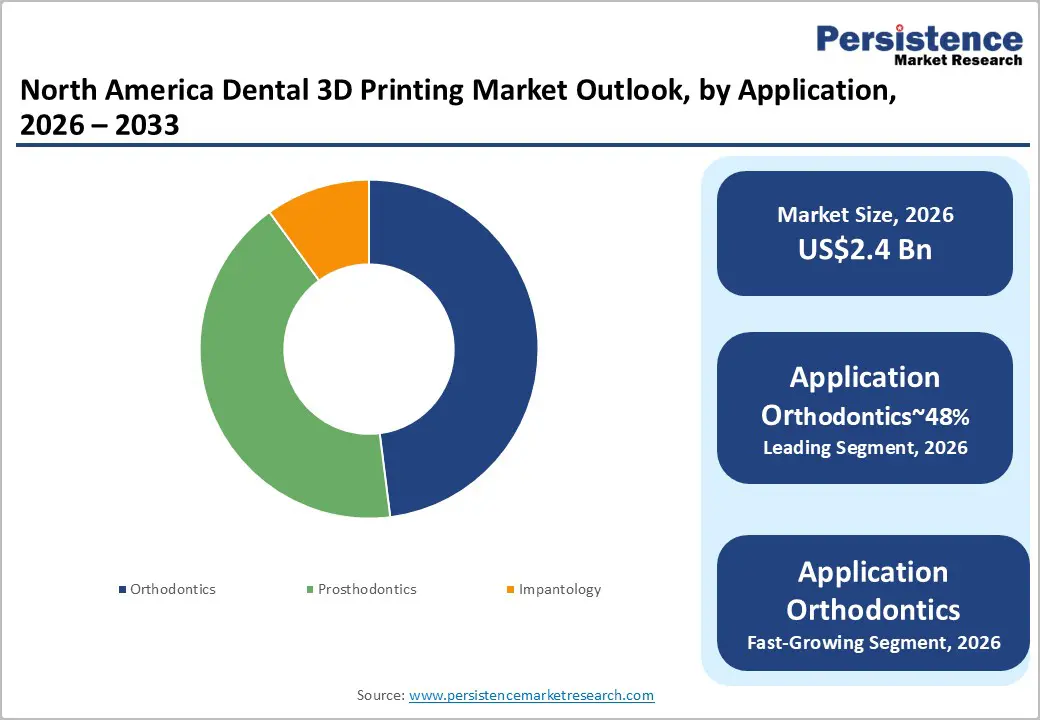

The North America dental 3D printing market size is likely to be valued at US$2.4 billion in 2026 and is expected to reach US$11.6 billion by 2033, growing at a CAGR of 25.3% during the forecast period from 2026 to 2033, driven by the accelerating transition from traditional subtractive manufacturing to high-precision additive processes within clinical and laboratory settings.

Key growth factors include the increasing prevalence of dental disorders, a rising geriatric population requiring prosthodontic interventions, and a robust regulatory environment that supports the commercialization of biocompatible resins. Furthermore, the integration of artificial intelligence (AI) in digital CAD/CAM workflows has reduced human error and turnaround times, positioning 3D printing as an essential pillar of modern dental care delivery in North America.

Key Industry Highlights:

- Leading Region: The U.S. is projected to lead due to a mature innovation ecosystem, high concentration of specialized clinics, and widespread adoption of digital dentistry, accounting for approximately 86% share in 2026, driven by technology adoption, and ecosystem advantages.

- Fastest-growing Region: Canada is anticipated to grow the fastest due to the rising digital literacy, government-supported innovation, and accelerated adoption of same-day dentistry in urban centers.

- Leading Product Type: Materials are projected to dominate for simplicity, cost, adoption, and functional use across key sectors, holding approximately 54% share in 2026.

- Leading Application: Orthodontics is expected to lead, accounting for approximately 48% share in 2026 through industrial adoption, throughput, quality, and high-value applications.

| Key Insights | Details |

|---|---|

| North America Dental 3D Printing Market Size (2026E) | US$2.4 Bn |

| Market Value Forecast (2033F) | US$11.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 25.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 17.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Advancements in High-Precision Additive Manufacturing for Dental Applications

Continuous innovation in dental additive manufacturing technologies is strengthening production accuracy across restorative and orthodontic workflows. Vat photopolymerization systems dominate due to their capability to deliver extremely fine layer resolution for dental appliances. These systems support fabrication of aligners, surgical guides, and anatomical models with highly consistent dimensional fidelity. Regulatory approvals for dental printing devices have expanded rapidly, reflecting growing clinical validation of digital manufacturing processes.

Regulatory recognition reinforces practitioner confidence and accelerates adoption across dental laboratories and chairside clinical environments. The technology, therefore, integrates seamlessly with digital dentistry ecosystems centered on intraoral scanning and computer-aided design.

Precision printing capabilities significantly reduce fabrication timelines compared with conventional casting and milling techniques. Dental laboratories benefit from streamlined digital workflows that minimize manual processing and reduce material wastage. Faster turnaround enables clinics to deliver customized restorations within single treatment visits, strengthening patient convenience and treatment continuity. Digital fabrication also enhances repeatability across prosthetic manufacturing, supporting standardized quality control in dental laboratories. These efficiencies reshape operational cost structures by lowering labor intensity while improving production scalability. Consequently, advanced additive manufacturing platforms are becoming central infrastructure within the evolving digital dental care ecosystem.

Integration of End-to-End Digital Dentistry and CAD CAM Production Workflows

The North America dental ecosystem is rapidly transitioning toward fully integrated digital dentistry platforms. Clinical practices increasingly adopt intraoral scanning technologies that replace traditional analog impression procedures. Digital scans seamlessly connect with computer-aided design and additive manufacturing platforms for prosthetic production. This workflow integration improves procedural precision while reducing manual intervention across diagnostic and fabrication stages.

Regulatory acceptance of digital dental devices further supports the credibility of technology-driven treatment pathways. Consequently, dental laboratories and clinics are restructuring operational models around digitally connected diagnostic and manufacturing infrastructures.

Clinical efficiency improves as digital impressions interface directly with computer-controlled design and printing systems. Chairside workflows become faster because prosthetic designs are transmitted instantly to manufacturing platforms. This integration significantly reduces clinical appointment durations and simplifies communication between dentists and dental laboratories.

Labor-intensive manual fabrication steps decline as digital design automation standardizes restorative manufacturing procedures. These efficiencies restructure cost allocation across prosthodontic workflows by lowering labor dependence and minimizing material wastage. As a result, integrated digital production ecosystems are reshaping service delivery models throughout the North America dental care sector.

Barrier Analysis – Liability Ambiguity and Malpractice Coverage Gaps in Chairside Additive Dentistry

The expansion of chairside dental printing introduces unresolved liability questions across clinical manufacturing responsibilities. Dentists increasingly design and fabricate permanent restorations within clinical environments using integrated printing systems. This shift blurs traditional boundaries between laboratory fabrication and practitioner-delivered treatment services. When printed restorations fail prematurely, determining responsibility becomes complex across design, material, and equipment variables.

Malpractice insurers, therefore, encounter difficulties defining standardized coverage frameworks for digitally manufactured dental prosthetics. This regulatory and legal uncertainty discourages cautious practitioners from rapidly adopting chairside additive production capabilities.

Insurance frameworks historically evolved around laboratory-fabricated restorations produced by certified dental technicians. Chairside manufacturing alters this structure by transferring fabrication control directly to clinical practitioners. Liability attribution may involve practitioner design choices, printer calibration conditions, or material performance characteristics. Such multidimensional risk complicates underwriting models used by malpractice insurers within dental care systems.

Conservative practitioners, therefore, delay adoption until clearer legal precedents and insurance policies emerge. These unresolved accountability structures slow clinical diffusion of chairside additive manufacturing despite strong technological maturity.

High Capital Investment Requirements and Specialized Material Cost Structures

The expansion of dental additive manufacturing faces structural constraints arising from elevated capital investment requirements. Professional-grade dental printers require substantial upfront expenditure, creating financial barriers for smaller clinics. Advanced resins and specialized photopolymer materials further increase operational costs for laboratories and practices. These inputs demand controlled storage conditions, post-processing equipment, and certified clinical validation protocols.

Such cost layers intensify procurement risks for independent dental practices with limited capital reserves. Consequently, market participation remains concentrated among larger laboratories and well-capitalized dental service organizations.

Material supply chains also influence cost predictability across dental additive manufacturing workflows. Proprietary printing resins are often restricted to specific hardware ecosystems through certification requirements. This compatibility structure limits supplier flexibility and increases dependency on specialized material vendors. Smaller clinics face difficulties achieving the production scale necessary to offset equipment depreciation and material costs.

Rural and independent practices, therefore, encounter a slower digital transition compared with urban clinical networks. These financial pressures collectively restrict market penetration despite strong technological momentum within advanced dental manufacturing platforms.

Opportunity Analysis – Transition toward Direct Printed Clear Aligner Manufacturing

Orthodontic production workflows are undergoing structural change as additive manufacturing evolves toward direct printed aligner fabrication. Conventional aligner production depends on printing sequential dental models followed by thermoforming plastic sheets. Direct printing technologies eliminate this intermediate modeling step by fabricating aligners directly from specialized photopolymer materials. This shift significantly simplifies orthodontic manufacturing pipelines while reducing material handling and manual forming processes.

Research activity across dental material science is therefore accelerating the development of flexible and optically transparent printing resins. These innovations position direct printed orthodontic appliances as a transformative advancement within digital dental manufacturing ecosystems.

Regulatory clearance of elastic and biocompatible resins represents a critical milestone for commercial adoption. Material suppliers are actively developing formulations capable of maintaining durability, clarity, and controlled orthodontic force delivery. Successful certification would allow orthodontic providers to transition from multi-stage model fabrication toward streamlined digital production workflows. This transition reduces processing steps, lowers production costs, and accelerates aligner delivery timelines. Dental laboratories and orthodontic providers, therefore, anticipate significant operational advantages through direct appliance printing technologies. Consequently, direct printed aligner manufacturing represents a high-value opportunity across the evolving digital orthodontics landscape.

Expansion of Outsourced Dental Additive Manufacturing Service Models

The growing demand for digital dental production is creating strong opportunities for specialized outsourced printing services. Many dental laboratories lack the internal infrastructure required to support advanced additive manufacturing workflows. Service providers offering centralized production capabilities can therefore address unmet fabrication requirements across distributed clinical networks.

Cloud-based design platforms enable laboratories and clinics to transmit digital case files directly to production centers. This model reduces equipment investment burdens while allowing laboratories to access advanced printing technologies. As a result, outsourced manufacturing services are emerging as a scalable operational layer within digital dentistry ecosystems.

Centralized service providers also benefit from production efficiencies generated through higher utilization of industrial printing platforms. Aggregating demand from multiple laboratories allows optimized material consumption and streamlined post-processing operations. These efficiencies reduce unit production costs compared with decentralized in house manufacturing environments. Integrated digital workflows further enable real-time case tracking, automated design validation, and standardized quality control protocols.

Dental service organizations and multi-clinic networks increasingly favor such infrastructure for predictable turnaround timelines. Consequently, outsourced additive manufacturing services are becoming a strategic growth channel across the North America dental technology landscape.

Category–wise Analysis

Product Type Insights

Materials are projected to lead the market, accounting for approximately 54% share in 2026, supported by the recurring consumption of specialized resins and powders across laboratory and chairside workflows. Demand remains anchored in high-performance photopolymers that support aligner model fabrication, surgical guides, dentures, and restorative components within digital dental production environments. Expanding portfolios of permanent biocompatible materials, including ceramic composites and reinforced resins, have elevated the segment from diagnostic modeling toward clinical-grade restorations.

Technology providers, including SprintRay, 3D Systems through its NextDent platform, and Desktop Health with Flexcera biomaterials, continue advancing formulation science and curing compatibility across digital printing ecosystems. The combination of recurring demand, validated clinical performance, and ecosystem lock-in sustains material segment leadership.

Services are projected to be the fastest-growing segment, driven by the growing preference for outsourced digital manufacturing and design support across dental laboratories and clinics. Many mid-sized practices rely on remote design and fabrication networks that convert intraoral scans into finished prosthetic components without maintaining internal production infrastructure. Cloud-connected platforms now allow clinical data to move directly from chairside scanners into centralized printing hubs operating advanced additive manufacturing equipment.

Companies such as Argen and Stratasys support distributed manufacturing environments through high-volume production platforms and digital workflow integration technologies. As distributed smart-factory networks expand, outsourced additive manufacturing services are rapidly scaling within the regional dental technology ecosystem.

Application Insights

Orthodontics is projected to lead, accounting for approximately 48% share in 2026, underpinned by its entrenched role in clear aligner therapy across adult and pediatric patient populations. The segment’s dominance is reinforced by high-volume production of 3D-printed models that support both traditional thermoformed aligners and emerging direct-print workflows. Providers prioritize rapid, same-day appliance delivery, workflow integration, and material reliability, while platform evolution includes AI-driven staging.

Multi-material indirect bonding trays and cloud-connected design software sustain replacement cycles and utilization intensity. Leading brands such as Align Technology, Formlabs Dental, and uLab Systems lock in enterprise workflows through proprietary software, high-speed printers, and FDA-cleared materials. This combination of high patient demand, recurring material use, and integrated digital ecosystems maintains Orthodontics’ structural leadership in North America dental 3D printing.

Orthodontics is also expected to be the fastest-growing segment in the North America dental 3D printing market, driven by emerging demand for direct-printed aligners and patient-specific orthodontic appliances. Growth is catalyzed by shape-memory polymers, AI-assisted treatment planning, and cloud-integrated workflows that accelerate case preparation, reduce chair time, and enable multi-material printing for advanced indirect bonding. Adoption is supported by distributed manufacturing hubs and digital design-as-a-service platforms, lowering operational friction for first-time adopters and smaller practices.

Brands including LuxCreo, SprintRay, and Angelalign are expanding direct-print aligner solutions and high-speed photon printers. As cloud-based orthodontic ecosystems mature and consumer adoption of aesthetic, rapid treatments rises, this segment outpaces overall market growth, capturing both clinical and technological momentum across North America.

Country Insights

U.S. Dental 3D Printing Market Trends

The U.S. is anticipated to dominate the North America dental 3D printing market, accounting for approximately 86% share in 2026, underpinned by a mature innovation ecosystem and a high concentration of specialized clinics across major urban hubs. Market dominance is reinforced by widespread adoption of digital dentistry, rapid chairside workflows, and high patient demand for elective orthodontic and restorative procedures. Platform evolution, including AI-driven design, multi-material printing, and cloud-integrated planning, supports high-volume throughput and operational efficiency.

Leading brands such as 3D Systems, Stratasys, Formlabs, and SprintRay anchor enterprise workflows, offering validated materials, high-speed printers, and proprietary software. This combination of established infrastructure, recurring material demand, and regulatory clarity through FDA 510(k) pathways sustains U.S. dominance while enabling ongoing innovation and scale economies across clinical and laboratory settings.

Canada Dental 3D Printing Market Trends

Canada is expected to be the fastest-growing country in the North America dental 3D printing market, driven by rising digital literacy, government-supported innovation, and accelerated adoption of same-day dentistry in urban centers. Growth is catalyzed by high per-capita intraoral scanner adoption, hybrid lab workflows, and tele-dentistry integration that enable distributed, local production for remote populations.

Leading brands such as Formlabs Dental, Stratasys, and Structo are expanding local support, high-speed MSLA systems, and cloud-enabled service models, embedding workflow integration and operational efficiency. These dynamics position Canada to outpace regional growth while fostering innovation adoption ahead of broader U.S. deployment.

Competitive Landscape

The North America dental 3D printing market is moderately consolidated, with top players such as Stratasys, 3D Systems, and Formlabs controlling a substantial share of the hardware and material ecosystem. These companies leverage extensive patent portfolios, proprietary software, and established distribution networks through partners such as Henry Schein and Patterson Dental to reinforce their competitive positioning. While the hardware and material segments are dominated by a few integrated leaders, the software and service sectors remain fragmented, with numerous startups introducing AI-driven design and cloud-based workflows. Market behavior reflects ongoing platform evolution, selective M&A activity, and service-led innovations, enabling leading players to embed themselves within clinical and laboratory ecosystems, while smaller entrants capture niche applications in design, optimization, and localized production models.

Key Industry Developments:

- In January 2026, Rapid Shape and Circle entered a strategic partnership to accelerate chairside manufacturing via cloud-based AI design. This collaboration integrates the Circle One cloud solution with Rapid Shape printers, allowing dental assistants to initiate complex prosthetic prints with a single click, drastically reducing office turnaround times.

- In December 2025, SprintRay announced the successful launch of its "Duo Kit" for the Pro 2 printer to enable multi-material dental workflows. By splitting the build platform, this accessory allows for the simultaneous printing of different dental components, increasing throughput for high-volume North America dental labs.

- In May 2025, Dental Materials Ricoh developed a novel 3D inkjet printing technology for full-color, biocompatible resin components. This innovation introduces high-mechanical-strength resins that mimic natural tooth aesthetics, providing a significant competitive edge for dental labs focused on high-end cosmetic restorations.

Companies Covered in North America Dental 3D Printing Market

- Formlabs

- 3Shape

- Envista

- Stratasys

- Carbon

- Desktop Metal / Desktop Health

- 3D Systems

- Dentsply Sirona

- SprintRay

- Align Technology

- EnvisionTEC

- LuxCreo

- Asiga

- Glidewell Laboratories

- Planmeca

- Renishaw

Frequently Asked Questions

The market is estimated to increase from US$ 1.36 Bn in 2024 to US$ 6.55 Bn by 2031.

Increasing demand for personalized dental solutions, high cost-efficiency, and growing trend of digital dentistry are anticipated to push demand.

Leading players include Stratasys, 3D Systems, Formlabs, EnvisionTEC, and Carbon, Inc.

The market is projected to record a CAGR of 25.2% from 2024 to 2031.

3D printing provides the ideal solution in dentistry, thereby enabling the production of superior implants, splints, and surgical guides.