- Medical Devices

- Dental Implants Market

Dental Implants Market Size, Share, and Growth Forecast 2026 - 2033

Dental Implants Market by Product (Titanium Dental Implants, Zirconium Dental Implants), by Procedure (Root-form Dental Implants, Plate-form Dental Implants), by End-user (Hospitals, Ambulatory Surgical Centers, Dental Clinics), and Regional Analysis, 2026 - 2033

Dental Implants Market Size and Trend Analysis

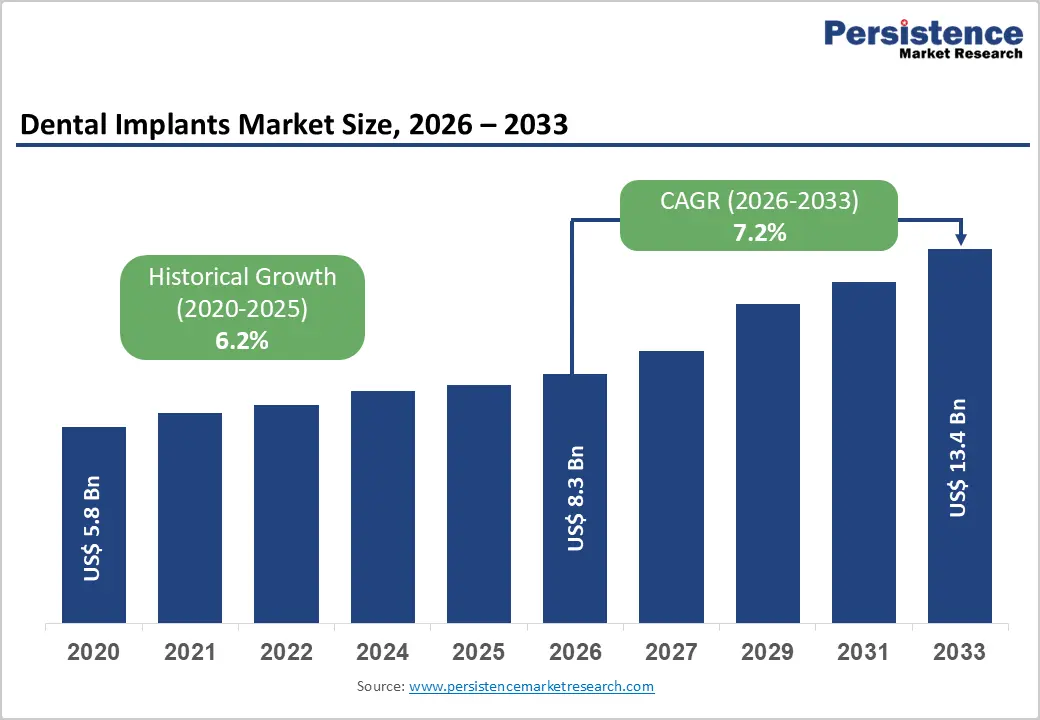

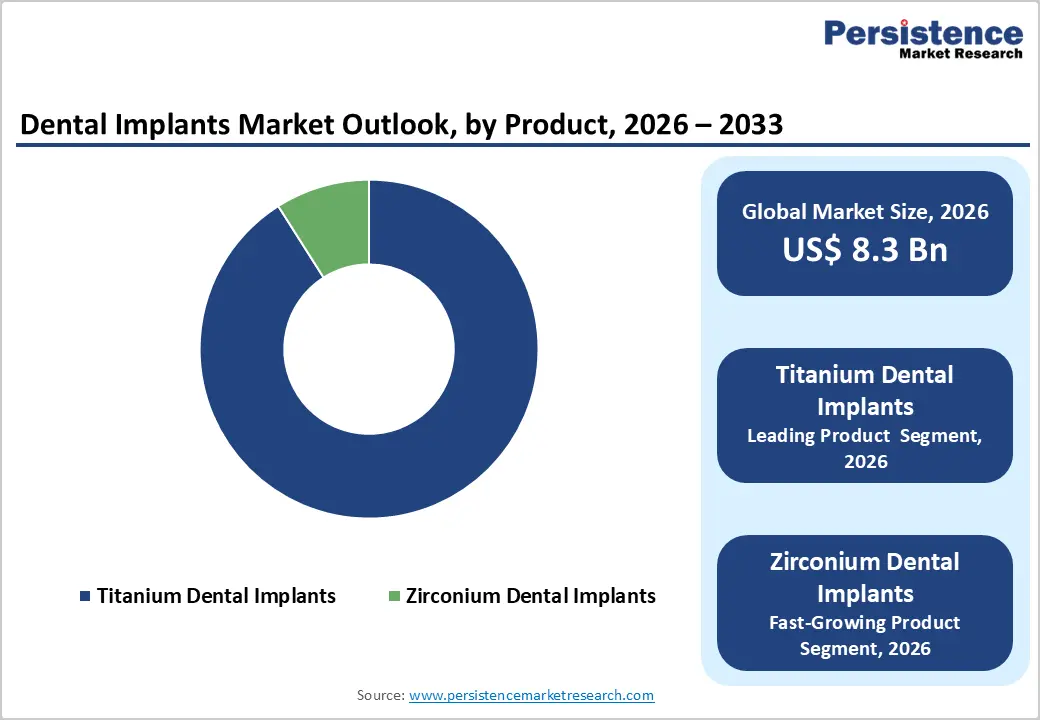

The global dental implants market size is expected to be valued at US$ 8.3 billion in 2026 and projected to reach US$ 13.4 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033. It is advancing on the convergence of a rapidly aging global population, rising rates of edentulism, and expanding access to oral healthcare, particularly across emerging economies.

According to the World Health Organization (WHO), oral diseases affect nearly 3.5 billion people worldwide, with severe tooth loss disproportionately impacting adults over 65. Simultaneously, technological advancements, including digital dentistry workflows, computer-aided design and manufacturing (CAD/CAM), and minimally invasive implant protocols, are broadening the patient-eligible pool, reducing procedure time, and improving clinical outcomes, collectively reinforcing sustained demand growth across all major geographies by 2033.

Key Industry Highlights:

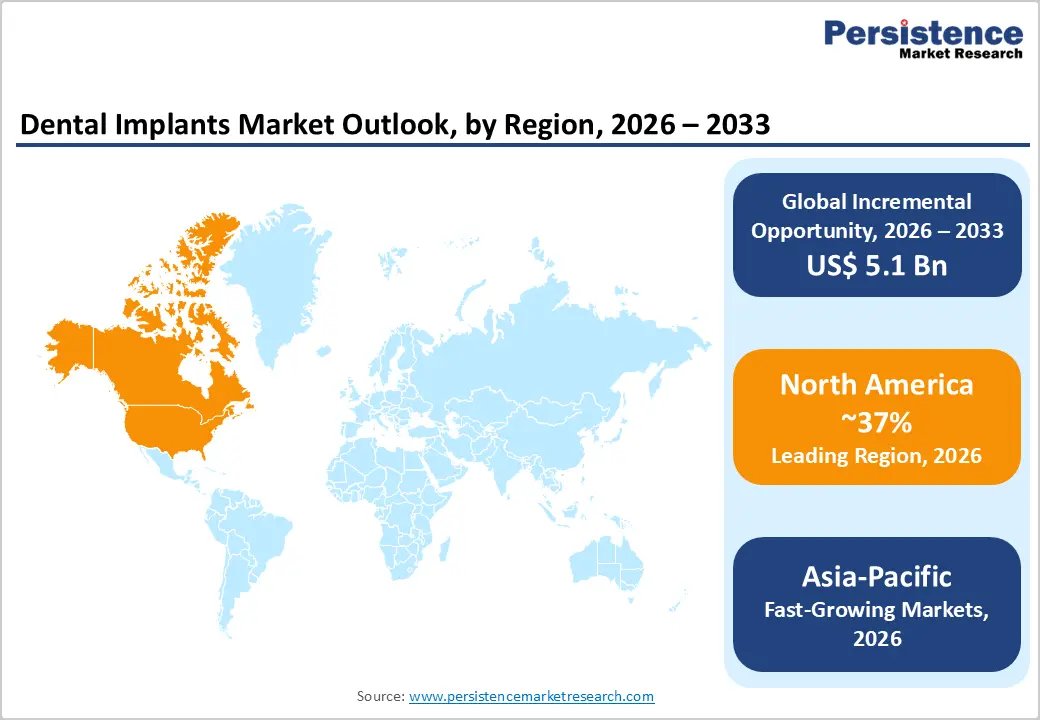

- Regional Leadership: North America held 37% of the global dental implants share in 2025, driven by high dental expenditure per capita, a large edentulous population, regulatory innovation pathways, and expanding DSO-driven procedure volumes.

- Fast-Growing Regional Market: Asia Pacific is the fastest-growing region by 2033, catalyzed by China's government-backed price reforms expanding procedure affordability, South Korea's insurance-covered implant scheme, and India's fast-growing dental clinic sector.

- Dominant Product: Titanium Dental Implants command approximately 91% of global product share in 2025, anchored by decades of clinical evidence, superior osseointegration performance, and the broadest practitioner familiarity of any implant material globally.

- Fast-Growing Product: Zirconium Dental Implants are the fastest-growing product segment, driven by rising demand from metal-sensitive and aesthetics-conscious patients, expanding EAO clinical validation, and growing manufacturer investment in ceramic implant design optimization.

- Opportunity: Manufacturers investing in dental tourism infrastructure in cost-competitive markets, particularly Mexico, Hungary, India, and Thailand, stand to capture a rapidly growing, price-sensitive procedure volume that bypasses the affordability barriers constraining implant adoption in high-cost domestic markets.

Market Dynamics

Drivers - Growing Prevalence of Tooth Loss and Growing Geriatric Population

The expanding global geriatric demographic represents the most structurally significant demand driver for the dental implants market, as tooth loss incidence rises sharply with age and implants increasingly supplant traditional dentures as the preferred restoration solution. The WHO reports that 19% of individuals aged 65 and older are completely edentulous globally, with an estimated 178 million people missing at least one tooth in the U.S. alone, according to the American College of Prosthodontists. As life expectancy increases across North America, Europe, and the Asia Pacific, the absolute volume of potential implant candidates is expanding. Simultaneously, growing patient awareness of the functional and aesthetic superiority of implants over removable dentures supported by dental practitioner education campaigns and expanding insurance reimbursement, is converting latent need into active procedure demand.

Restraint - High Procedure Costs and Limited Dental Insurance Coverage

The cost of dental implant procedures, ranging from US$ 3,000 to US$ 6,000 per implant in the United States, inclusive of surgery, abutment, and crown remains the most significant barrier to patient adoption globally.

The National Association of Dental Plans (NADP) indicates that most U.S. dental insurance plans either exclude implants entirely or provide only partial reimbursement, forcing out-of-pocket expenditure that deters middle- and lower-income patient segments. This cost barrier is particularly acute in emerging markets where oral healthcare financing infrastructure is underdeveloped, fundamentally constraining the addressable patient pool even where clinical need is high.

Opportunities - Accelerating Adoption of Zirconia (Ceramic) Implants Among Metal-Sensitive Patients

The Zirconium Dental Implants segment is the fastest-growing product category within the dental implants market, representing a compelling opportunity for manufacturers to capture a structurally distinct and rapidly growing patient segment. Zirconia implants address the growing clinical demand from patients with titanium allergies or sensitivities estimated to affect 0.6% of the population per data published in Contact Dermatitis journal as well as patients seeking metal-free oral rehabilitation for aesthetic or biocompatibility reasons.

The European Association of Osseointegration (EAO) has increasingly recognized zirconia as a clinically viable implant material in its consensus statements, validating the category for mainstream clinical adoption. Manufacturers investing in zirconia implant design, surface texture optimization, and clinical outcome documentation stand to capture premium pricing and differentiated positioning as the category matures from niche to mainstream through 2033.

Category-wise Insights

Product Analysis

Titanium Dental Implants dominate the global dental implants market with an overwhelming share of approximately 91% in 2025, a position entrenched by decades of clinical evidence demonstrating their superior osseointegration, biocompatibility, and long-term durability.

The American Academy of Implant Dentistry (AAID) cites implant survival rates exceeding 95% over a decade for titanium systems, a clinical track record that drives prescriber confidence and patient acceptance. Within the titanium category, Internal Connectors represent the dominant sub-segment, preferred for their superior biomechanical stability, reduced microleakage risk, and aesthetic outcomes over external connection designs. Zirconium Dental Implants are the fastest-growing segment, but begin from a very small base and are expected to incrementally gain share as clinical validation expands and manufacturing scalability improves through 2033.

Procedure Insights

Root-form Dental Implants command the leading procedural share of approximately 88% of the global market in 2025, reflecting their status as the standard of care for single-tooth and full-arch implant restorations across virtually all clinical settings. Root-form implants designed to mimic natural tooth root anatomy through a cylindrical or tapered screw shape leverage the broadest body of clinical literature, widest practitioner familiarity, and most extensive product portfolio among all implant types.

The International Congress of Oral Implantologists (ICOI) consistently endorses root-form implants as the primary evidence-based implant modality. Plate-form implants, used in patients with limited bone width, represent a smaller niche segment, with applications concentrated in anatomically challenging cases that cannot accommodate conventional root-form designs.

Regional Insights

North America Dental Implants Market Trends and Insights

North America leads due to high oral disease prevalence, aging population, and strong dental expenditure. According to the Centers for Disease Control and Prevention, nearly 1 in 4 adults aged 20–64 has untreated dental caries, while severe tooth loss rises significantly in those above 65. High insurance penetration and advanced implant adoption further sustain demand, making the region the largest revenue contributor globally.

U.S. Dental Implants Market Trends and Insights

The U.S. dominates and is expected to reach ~US$ 3.2 billion by 2026. The Centers for Disease Control and Prevention reports that about 13% of adults aged 65+ have lost all their teeth, directly driving implant demand. Additionally, the National Institute of Dental and Craniofacial Research highlights widespread periodontal disease among adults. High healthcare spending per capita and rapid adoption of digital dentistry technologies make the U.S. the dominant market globally.

Canada Dental Implants Market Trends and Insights

Canada is expected to reach ~7% CAGR, supported by rising elderly population and improving public dental coverage. According to the Statistics Canada, over 1 in 5 Canadians is aged 65 or older, increasing demand for restorative procedures. Expanding government-backed dental care programs and growing awareness of oral health are accelerating implant adoption, particularly in urban centers, positioning Canada as the fastest-growing country in the region.

Europe Dental Implants Market Trends and Insights

Europe remains a key region due to strong dental infrastructure and high practitioner density. According to the Eurostat, many European countries report over 60 dentists per 100,000 population, ensuring high treatment accessibility. Aging demographics and early adoption of advanced dental technologies such as CAD/CAM systems support stable demand across the region.

Germany Dental Implants Market Trends and Insights

Germany leads and is expected to reach ~US$ 1.4 billion by 2026. The Statistisches Bundesamt reports that over 22% of the population is aged 65+, a key driver for implants. High dentist density and strong reimbursement mechanisms support procedure volumes. Germany is also a hub for dental technology innovation, reinforcing its leadership in implant adoption and manufacturing within Europe.

Spain Dental Implants Market Trends and Insights

Spain is expected to grow at ~8% CAGR, driven by dental tourism and cost competitiveness. According to the Instituto Nacional de Estadística, the aging population continues to expand, increasing demand for dental restorations. Spain’s lower treatment costs compared to Western Europe and strong private dental clinic networks are attracting international patients, positioning it as a high-growth implant market.

Asia Pacific Dental Implants Market Trends and Insights

Asia-Pacific is the fast-growing market due to large untreated population, rising income, and improving dental access. The World Health Organization estimates that oral diseases affect nearly 3.5 billion people globally, with a significant share in Asia. Increasing awareness, urbanization, and expansion of private dental chains are accelerating implant adoption across the region.

China Dental Implants Market Trends and Insights

China leads and is expected to reach ~US$ 1.7 billionn by 2026. The National Health Commission of China reports a rising burden of oral diseases, particularly among adults and elderly populations. Government initiatives such as “Healthy China 2030” are improving access to dental care. Growth is further supported by increasing middle-class income and domestic manufacturing of affordable implant systems.

India Dental Implants Market Trends and Insights

India is expected to reach ~10% CAGR, driven by high unmet dental needs and cost advantage. The Ministry of Health and Family Welfare indicates a high prevalence of dental caries and periodontal diseases across the population. Rapid expansion of private dental clinics, coupled with rising dental tourism and affordability of procedures, is accelerating implant adoption, making India the fastest-growing market in Asia-Pacific.

Competitive Landscape

The global dental implants market is moderately consolidated, with the top five players Straumann Holding AG, Nobel Biocare Services AG (part of Envista Holdings), Dentsply Sirona Inc., Osstem Implant Co., Ltd., and Zimmer Biomet Holdings Inc., collectively commanding an estimated 55–60% of global revenue. Market leaders differentiate through digital dentistry platform integration (intraoral scanners, treatment planning software, guided surgery), comprehensive clinician education programs, and premium surface technology. Emerging competitive trends include value-tier product expansion targeting emerging markets, acquisition-led portfolio broadening, and subscription-based digital workflow software that deepens clinical ecosystem lock-in for both implant hardware and restorative components.

Key Developments:

- August, 2025: Osstem Implant Co Ltd expanded its footprint in India by enhancing distribution networks, increasing partnerships with local dental clinics, and investing in training programs for dental professionals. The company focused on promoting its “K-Implant” brand, known for cost-effective yet high-quality implant systems, to capture growing demand in the Indian dental implants market.

- July, 2025: ZimVie Inc. entered into an exclusive partnership with Osstem Implant Co Ltd to strengthen its presence in the Chinese dental implants market. Under the agreement, Osstem leveraged its well-established distribution network and strong clinical relationships across China to market and distribute ZimVie’s premium implant systems.

Global Dental Implants Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 5.8 Billion |

|

Projected Market Value (2026) |

US$ 8.3 Billion |

|

Projected Market Value (2033) |

US$ 13.4 Billion |

|

CAGR (2026-2033) |

7.2% |

|

Leading Region |

North America, 37% share |

|

Dominant Product |

Titanium Dental Implants, 91% share |

|

Top-ranking Procedure |

Root-form Dental Implants, 97% share |

|

Incremental Opportunity |

US$ 5.2 billion |

Companies Covered in Dental Implants Market

- Osstem Implant Co Ltd

- Straumann Holding AG

- Dentsply Sirona Inc

- Nobel Biocare Services AG

- KYOCERA Medical Corp

- Zimmer Biomet Holdings Inc

- AB Dental Devices

- Alpha-Bio Tec Ltd

- Dentis Co., Ltd.

- Dentium Co Ltd

- Others

Frequently Asked Questions

The global dental implants market is valued at US$ 8.3 billion in 2026.

Rising edentulism, aging population, cosmetic dentistry demand, technological advancements, higher income, dental tourism, awareness, insurance expansion.

North America leads the global dental implants market with approximately 37% of global share in 2025

Emerging markets expansion, digital dentistry adoption, zirconia implants demand, cost reduction, dental tourism growth, AI integration.

Osstem Implant Co Ltd, Straumann Holding AG, Dentsply Sirona Inc, Nobel Biocare Services AG, KYOCERA Medical Corp, Zimmer Biomet Holdings Inc.