- Advanced Materials

- Cooling Fabrics Market

Cooling Fabrics Market Size, Share, and Growth Forecast 2026 - 2033

Cooling Fabrics Market by Material Type (Cotton, Linen, Bamboo Fiber, Polyester and Its Blends, Nylon, Far Infrared or Graphene Fabrics, Others), by Application (Sports & Fitness, Healthcare & Medical, Industrial & Workwear, Fashion & Casual Wear, Home Textiles, Military & Tactical, Others), by Distribution Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Cooling Fabrics Market Size and Trend Analysis

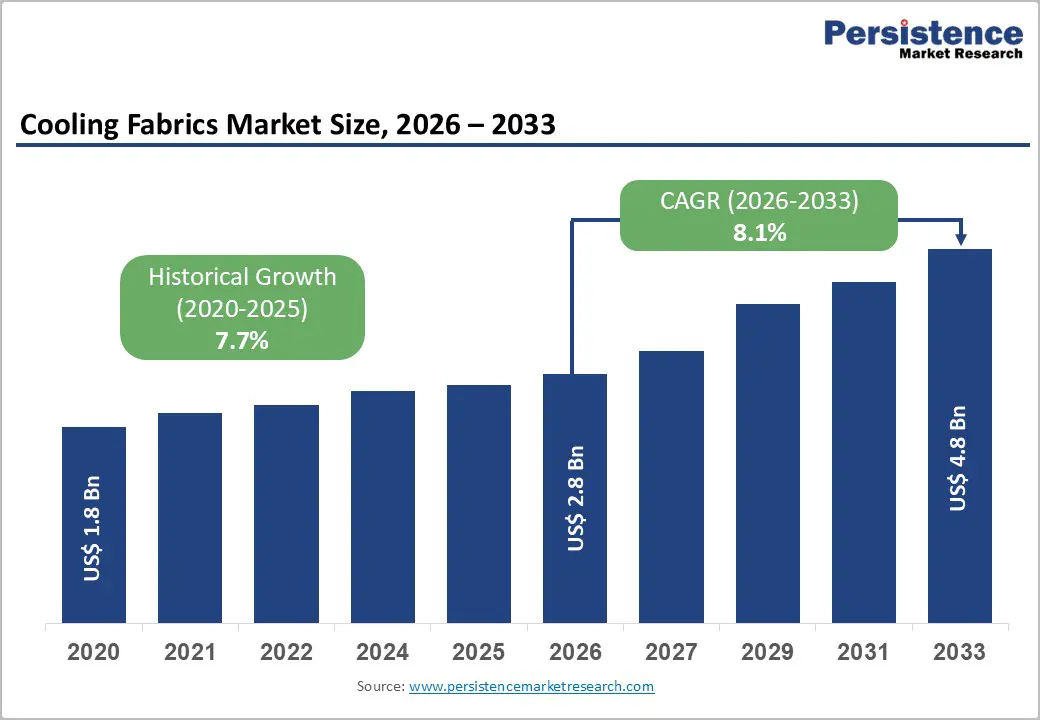

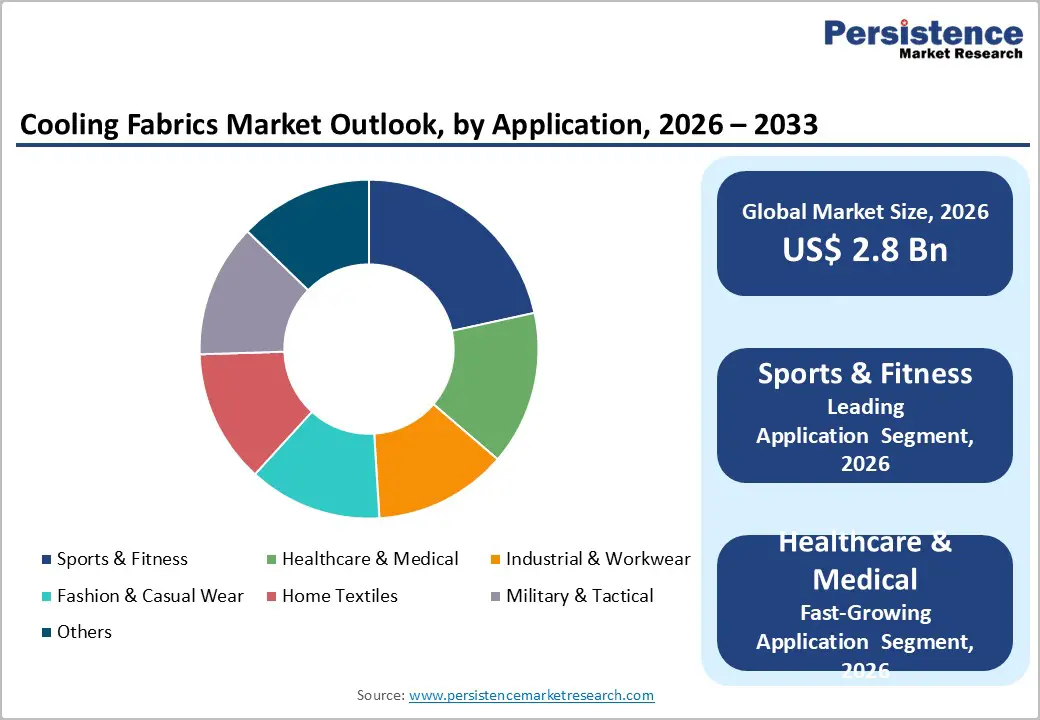

The global cooling fabrics market size is expected to be valued at US$ 2.8 billion in 2026 and projected to reach US$ 4.8 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033.

Rising consumer preference for comfort-driven apparel in extreme climates and active lifestyles is accelerating the adoption of moisture-wicking, phase-change, and thermoregulating textile technologies. Increasing global sports participation, highlighted by over 1 billion viewers of the 2024 Paris Olympics, as reported by the International Olympic Committee, is driving demand for performance wear. Moreover, expanding healthcare applications, supported by the World Health Organization’s projection of 2 billion people aged 60+ by 2050, further strengthen long-term market growth.

Key Industry Highlights:

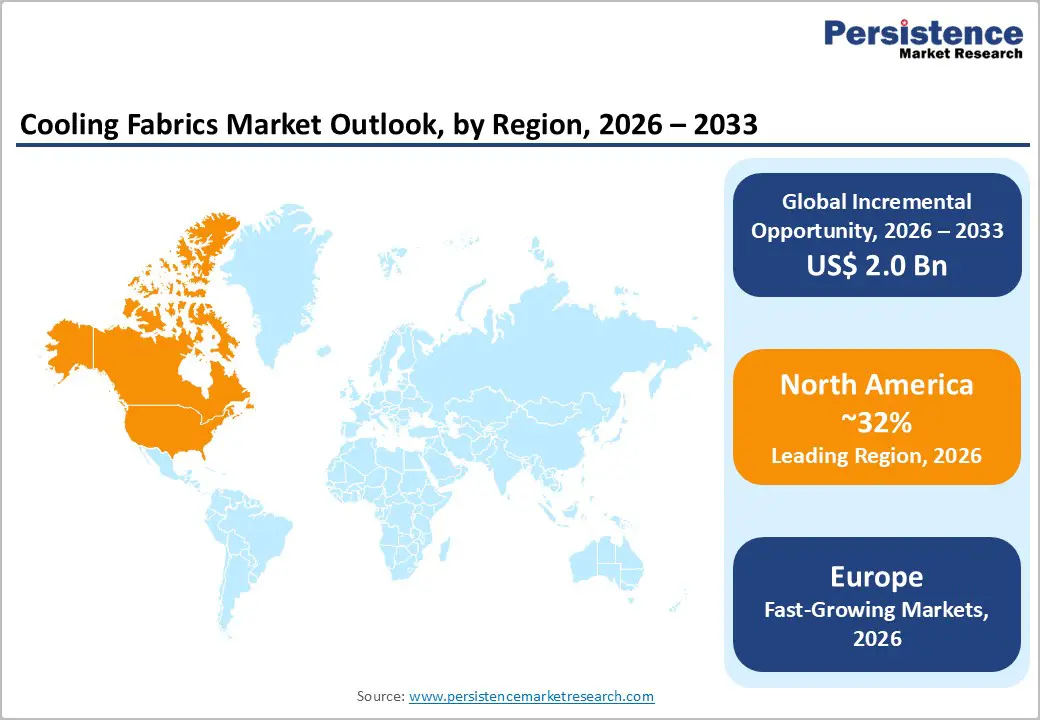

- Leading Region: North America leads the cooling fabrics market with a 32% share in 2025, supported by strong U.S. innovation ecosystems and expanding fitness-driven apparel demand.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, driven by large-scale textile manufacturing capacity and rising performance apparel consumption across China and India.

- Leading Material Category: Polyester and its blends dominate the material segment with a 35% share in 2025 due to superior moisture management, durability, and cost-effective mass production capabilities.

- Leading Application Category: Sports & Fitness holds a 28% market share in 2025, propelled by growing global athletic participation and sustained demand for thermoregulating performance wear.

- Key Opportunity: Expanding healthcare applications present strong growth potential, particularly for temperature-regulating textiles catering to aging populations and institutional medical infrastructure.

| Key Insights | Details |

|---|---|

| Cooling Fabrics Size (2026E) | US$ 2.8 billion |

| Market Value Forecast (2033F) | US$ 4.8 billion |

| Projected Growth CAGR (2026 - 2033) | 8.1% |

| Historical Market Growth (2020 - 2025) | 7.7% |

Market Dynamics

Drivers - Rising Sports & Fitness Participation Driving Cooling Fabric Demand

Growing participation in sports, fitness, and outdoor activities is significantly accelerating demand for cooling fabrics. According to the Global Wellness Institute, global wellness spending reached US$ 5.6 trillion in 2022, with fitness segments expanding at nearly 8% annually. Rising temperatures and increasing awareness of heat-related health risks are prompting consumers to prefer performance apparel with advanced thermoregulation properties.

Cooling fabrics equipped with moisture-wicking and evaporative technologies enhance comfort and endurance during high-intensity workouts. Studies published by the National Institutes of Health indicate that advanced performance textiles can reduce core body temperature by up to 2°C during exercise. Expanding marathon events, gym memberships, yoga participation, and athlete endorsements continue to strengthen sustained global demand.

Sustainable and High-Performance Textile Innovations Fuel Growth

Technological advancements in sustainable cooling textiles are emerging as a strong growth catalyst for the market. Increasing consumer preference for environmentally responsible materials is reshaping product development strategies. The European Textile and Apparel Confederation reports that nearly 70% of consumers favor sustainable fabrics, encouraging manufacturers to adopt bio-based phase-change materials and recyclable fiber solutions.

An article published in the Textile Research Journal highlights that graphene-infused fabrics improves thermal conductivity by approximately 30%, enhancing heat dissipation efficiency. Policy support such as the European Union’s Green Deal, allocating €1 trillion toward sustainable industries by 2030, is further stimulating research and innovation in eco-friendly, high-performance cooling textile technologies.

Restraints - High Production Costs and Supply Chain Pressures

The high cost of advanced raw materials such as graphene and far-infrared fibers remains a major constraint for the cooling fabrics market. According to the International Textile Manufacturers Federation, global raw material prices increased by nearly 15% in 2024 due to supply shortages and logistical disruptions. Dependence on specialty inputs and imported performance fibers further amplifies procurement volatility.

In addition, complex manufacturing processes requiring specialized coating, finishing, and testing equipment significantly raise operational expenses. Cooling fabrics are typically priced 20-30% higher than conventional textiles, limiting affordability in cost-sensitive regions. This pricing disparity restricts large-scale penetration, particularly in developing economies where purchasing decisions are heavily influenced by price competitiveness.

Low Awareness in Emerging Economies

Limited consumer awareness regarding the benefits of cooling fabrics continues to restrain growth across emerging regions such as Latin America and the Middle East & Africa. A United Nations Environment Programme survey indicates that only about 25% of consumers in these regions are familiar with advanced textile functionalities, including moisture management and temperature regulation features.

Persistent misconceptions about product durability, maintenance requirements, and long-term value further discourage adoption. Traditional fabrics continue to dominate due to familiarity and lower upfront costs. The absence of widespread educational campaigns and retail-level product demonstrations slows market penetration compared to more mature markets in North America and Europe.

Opportunity - Expanding Adoption in Healthcare and Medical Textiles

Healthcare applications present a strong growth opportunity as cooling fabrics address thermoregulation needs for patients and medical professionals. The World Health Organization projects chronic disease cases to rise by 57% by 2030, increasing demand for temperature-regulating bedding, patient garments, and medical uniforms. Hospitals are increasingly exploring smart textiles to improve patient comfort and recovery environments.

Innovations such as NASA-inspired phase-change materials have demonstrated the ability to reduce fever-related discomfort by nearly 40%, strengthening clinical interest. Supportive healthcare policies, including expansions under the U.S. Affordable Care Act, are encouraging hospital infrastructure upgrades, creating partnership opportunities for textile manufacturers targeting institutional healthcare procurement.

Rising Demand in Military and Tactical Applications

Military modernization programs are creating significant opportunities for cooling fabric manufacturers, particularly for deployment in extreme climatic conditions. The U.S. Department of Defense allocated approximately US$ 12 billion in 2025 toward advanced textile development, emphasizing soldier endurance, lightweight protection, and thermal regulation technologies for operational efficiency.

Research trials conducted by the U.S. Army Research Laboratory indicate that far-infrared and heat-dissipating fabrics can improve performance in high-temperature environments by nearly 25%. Additionally, expanding defense budgets across Asia Pacific countries, including India, are accelerating procurement of next-generation tactical gear, opening long-term contracts and collaborative research avenues for specialized textile innovators.

Category-wise Analysis

Material Type Insights

Polyester and its blends lead the material type segment, accounting for approximately 35% of the market share in 2025. Their dominance is driven by superior moisture-wicking capability, durability, and cost efficiency, making them ideal for large-scale performance apparel production. The American Fiber Manufacturers Association states that polyester represents nearly 55% of global synthetic fiber output, reinforcing its widespread industrial adoption.

Meanwhile, advanced functional materials such as phase-change incorporated fabrics and graphene-enhanced textiles are emerging as the fastest-growing category. These materials offer enhanced thermal conductivity, improved breathability, and adaptive temperature regulation. Increasing investment in R&D and the push toward sustainable, high-

Application Insights

Sports and fitness applications dominate the cooling fabrics market, capturing around 28% share in 2025. Growth is fueled by the expansion of athleisure trends and rising global sports participation. Statista reports global sports apparel sales surpassed US$ 200 billion in 2024, supporting demand for thermoregulating garments that enhance endurance and comfort during physical activity.

Healthcare and medical textiles are emerging as the fastest-growing application area. Rising demand for patient comfort solutions, temperature-regulating bedding, and smart hospital uniforms is expanding adoption. Increasing awareness of heat stress management and integration of functional textiles in institutional settings are driving new growth avenues beyond traditional athletic usage.

Distribution Channel Insights

Offline channels lead distribution with approximately 60% market share in 2025. Consumers continue to prefer physical retail stores for apparel purchases, valuing the ability to assess fabric texture, fit, and comfort before buying. Insights from the National Retail Federation indicate that nearly 70% of shoppers favor in-store trials for clothing, reinforcing the dominance of specialty sports outlets and department stores.

Online retail is the fastest-growing distribution channel, driven by expanding e-commerce infrastructure and direct-to-consumer brand strategies. Digital platforms offer wider product assortments, customer reviews, and convenient delivery options. Growing smartphone penetration and targeted digital marketing are accelerating online adoption, particularly among younger and tech-savvy consumers.

Regional Insights

North America Cooling Fabrics Market Trends and Insights

North America leads the global cooling fabrics market with an estimated 32% share in 2025, supported by strong innovation capabilities and high consumer awareness. Rising heatwave incidents, highlighted by the U.S. Environmental Protection Agency and over 1,500 heat-related deaths recorded in 2023 by the National Weather Service, are accelerating demand for thermoregulating apparel. A well-established fitness ecosystem further strengthens adoption across performance wear segments.

The United States remains the core growth engine, backed by research initiatives such as the Textile Innovation Lab at MIT and stringent regulatory frameworks such as FTC textile labeling standards that enhance product transparency. Expanding gym memberships and growing athleisure consumption continue to reinforce sustained regional demand.

Europe Cooling Fabrics Market Trends and Insights

Europe demonstrates steady expansion, growing at a CAGR of approximately 7.8% during the forecast period. The region benefits from strong sustainability regulations and rising outdoor participation, with Eurostat reporting a significant increase in recreational activities post-pandemic. Harmonized standards under EU REACH regulations facilitate cross-border textile trade and product compliance across member states.

Germany, the U.K., France, and Spain remain key contributors, supported by sustainable manufacturing initiatives and innovation in bio-based cooling fibers. Institutions such as the German Textile Research Centre are advancing eco-friendly textile technologies, while certification frameworks from the British Standards Institution strengthen export competitiveness.

Asia Pacific Cooling Fabrics Market Trends and Insights

Asia Pacific accounts for approximately 29% of the global market share in 2025 and represents the fastest-expanding regional landscape. Growth is driven by large-scale manufacturing capacity, competitive production costs, and expanding middle-class consumption. China remains a dominant producer, with the China National Textile and Apparel Council reporting nearly 60% of global textile manufacturing capacity concentrated in the country.

India’s Make in India initiative and Japan’s leadership in advanced functional textiles are accelerating innovation and domestic production. Additionally, ASEAN countries such as Vietnam are experiencing strong export momentum, supported by favorable trade policies and increasing international demand for performance-based textile solutions.

Competitive Landscape

The cooling fabrics market is moderately consolidated, characterized by the presence of established global manufacturers investing heavily in research and development to strengthen technological capabilities. Companies compete primarily through innovation in advanced cooling technologies, including phase-change materials, moisture-wicking enhancements, and thermoregulating fiber engineering. Strategic collaborations, sustainability-focused partnerships, and selective acquisitions are common approaches used to expand product portfolios and geographic reach.

Market participants are increasingly emphasizing vertical integration to control raw material sourcing and production efficiency. In addition, emerging competitive strategies include direct-to-consumer online distribution and product customization, enabling improved brand positioning and higher margins amid intensifying competition from regional and mid-sized textile producers.

Key Developments:

- In June 2025, Nike, Inc. launched its AeroCool performance line featuring advanced evaporative cooling fabrics designed for Olympic athletes, improving breathability by nearly 20% and reinforcing its focus on innovation-driven sports apparel for high-temperature competitive environments.

- In March 2024, Under Armour, Inc. partnered with Graphene Manufacturing Group Ltd. to integrate graphene-based cooling technology into industrial workwear, aiming to enhance thermal regulation, durability, and worker comfort across high-heat occupational settings.

- In October 2023, Patagonia, Inc. introduced recycled polyester cooling base layers aligned with sustainability trends, strengthening its eco-friendly portfolio while driving a reported 15% increase in category sales through responsible material innovation.

Companies Covered in Cooling Fabrics Market

- Coolcore LLC

- Ahlstrom

- NILIT Ltd.

- Polartec LLC

- Nan Ya Plastics Corporation

- Formosa Taffeta Co., Ltd.

- Tex-Ray Industrial Co., Ltd.

- Asahi Kasei Corporation

- HeiQ Materials AG

- Outlast Technologies LLC

- Nanotex LLC

- Columbia Sportswear Company

- Adidas AG

- Nike, Inc.

- Patagonia, Inc.

Frequently Asked Questions

The global Cooling Fabrics Market is projected to reach US$ 2.8 billion in 2026 and grow to US$ 4.8 billion by 2033 at a CAGR of 8.1%.

Key drivers include rising sports participation and sustainable tech advancements, with wellness spending at US$ 5.6 trillion and innovations reducing body temperature by 2°C.

North America leads with 32% share in 2025, driven by U.S. regulatory support and innovation ecosystems.

Expansion into healthcare for thermoregulation, targeting 2 billion elderly by 2050 with phase-change materials.

Leading companies include Coolcore LLC, Ahlstrom, NILIT Ltd., Polartec LLC, and Nan Ya Plastics Corporation.