- Energy Storage Solutions

- Global Immersion Cooling Market

Global Immersion Cooling Market Size, Share, and Growth Forecast 2026–2033

Immersion Cooling Market by Component (Solution, Services), by Cooling Type (Single Phase, Two Phase), Cooling Fluid (Mineral Oil, Synthetic Fluids, Fluorocarbon based fluids, Bio-Based / Dielectric Fluids, Others), Application (Artificial Intelligence & Machine Learning, High-Performance Computing (HPC), Edge Computing, Cryptocurrency Mining, Enterprise & Cloud Data Centers, Others), and Regional Analysis, 2026–2033

Global Immersion Cooling Market Size and Trend Analysis

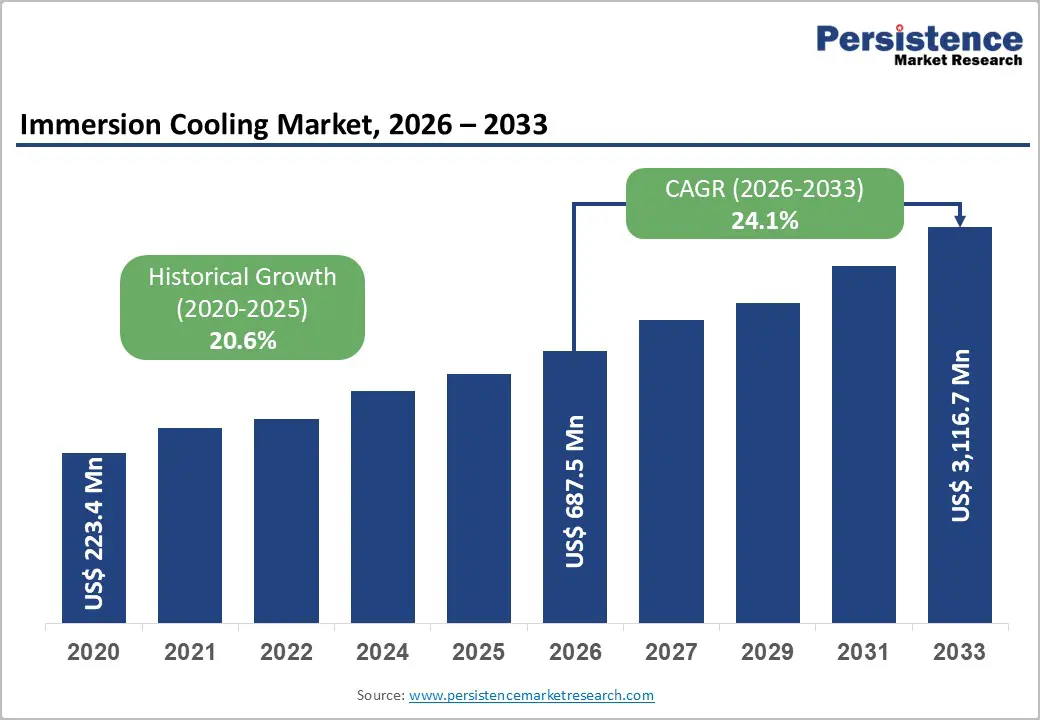

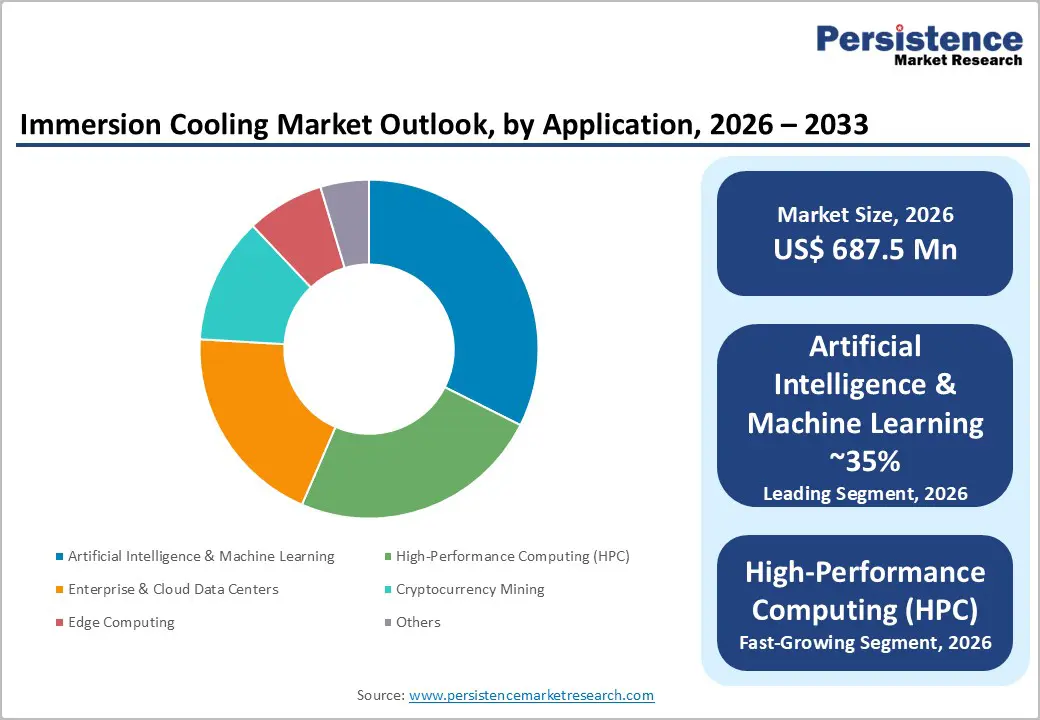

The global immersion cooling market size is expected to be valued at US$ 687.5 million in 2026 and is projected to reach US$ 3,116.7 million, growing at a CAGR of 24.1% between 2026 and 2033, driven by the rising demand for high-density computing in data centers, supported by the rapid expansion of AI workloads, cloud services, and hyperscale infrastructure.

Increasing heat output from advanced processors, GPUs, and servers is pushing traditional air-cooling systems toward their operational limits. Regulatory frameworks such as the U.S. Department of Energy’s Energy Efficiency Improvement Act and the European Union’s revised Energy Efficiency Directive are also compelling operators to reduce power usage effectiveness (PUE), thereby accelerating the shift toward liquid cooling technologies.

Key Industry Highlights:

- Leading Component: Solution segment dominates the market with over 70% share in 2026, driven by strong demand for fully integrated, turnkey immersion cooling infrastructure in hyperscale and HPC environments.

- Leading Cooling Type: Single-phase immersion cooling leads the market with over 63.0% share in 2026, valued at more than US$ 433.1 Million, due to its operational simplicity, lower maintenance needs, and established ecosystem compatibility.

- Leading Cooling Fluid: Mineral oil remains the leading fluid type with over 38.0% share in 2026, valued at more than US$ 261.3 Million, due to its cost efficiency, proven insulation properties, and widespread availability.

- Fastest Growing Cooling Fluid: Bio-based/dielectric fluids are the fastest-growing category, driven by tightening ESG regulations, PFAS phase-out pressures, and corporate sustainability commitments.

- Leading Application: Artificial Intelligence & Machine Learning dominates with over 35% share in 2026, valued at approximately US$ 240.6 Million, driven by GPU-intensive workloads that exceed the limits of air cooling and require continuous high-performance thermal stability.

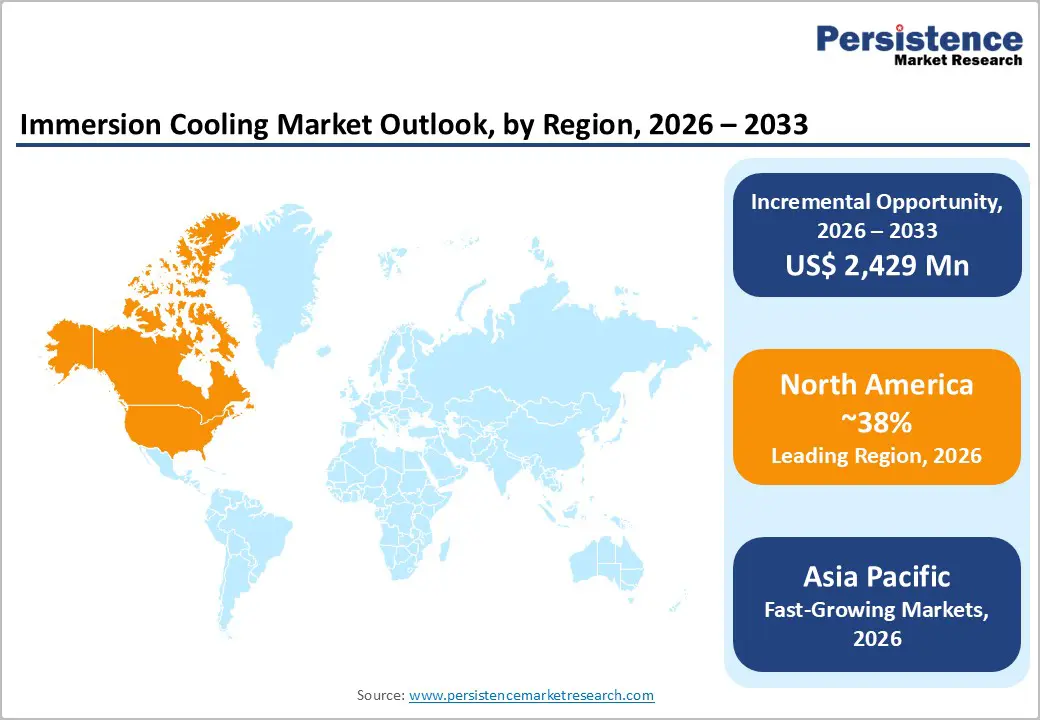

- Leading Region: North America dominates the market with over 38% share in 2026, valued at around US$ 261.25 Million, supported by hyperscale AI infrastructure expansion and strong cloud investment from major providers.

- Fast-growing Market: Asia Pacific is the fast-growing market with a CAGR of 28.9%, driven by sovereign AI programs, national HPC investments, and rapid digital infrastructure buildouts across China, India, and Japan.

Market Dynamics

Drivers - Hyperscale AI Infrastructure Buildout Demanding Next-Generation Thermal Management

The deployment of high-performance AI accelerators such as NVIDIA H100 (up to ~700W per GPU) and H200 is rapidly increasing rack-level power densities in AI data centers, often exceeding 30–100 kW per rack in modern deployments. This is pushing conventional air-cooling systems toward their practical thermal limits, accelerating adoption of liquid cooling and immersion cooling technologies.

Hyperscalers are integrating these cooling approaches directly into next-generation AI infrastructure designs rather than retrofitting existing systems. Government initiatives such as the U.S. CHIPS and Science Act are indirectly supporting the expansion of advanced computing and AI-ready data center capacity. Major cloud providers are scaling AI infrastructure investments at multi-billion-dollar levels, structurally strengthening long-term demand for high-efficiency thermal management solutions.

Regulatory Pressure on Data Center Energy Efficiency Driving Cooling Innovation

Global regulatory frameworks are increasingly focusing on improving data center energy efficiency, particularly through metrics such as Power Usage Effectiveness (PUE), which typically ranges from ~1.2 in advanced facilities to 2.0+ in legacy air-cooled environments. The European Union’s Energy Efficiency Directive requires large data centers to report energy performance and encourages progressive efficiency improvements, pushing operators toward lower PUE targets.

Singapore, through the Infocomm Media Development Authority (IMDA), has also implemented sustainability-linked criteria for new data center capacity approvals. While no universal global PUE cap exists, industry expectations are converging toward highly efficient next-generation facilities. These regulatory and policy pressures are improving the cost-benefit case for liquid and immersion cooling by reducing energy overheads. Tightening efficiency standards are expected to accelerate the replacement of traditional air-cooling infrastructure.

Restraints - High Upfront Capital Cost and Retrofit Complexity Limiting Adoption

Immersion cooling systems typically involve a 2–3× higher upfront capital cost compared to conventional air-cooled data center infrastructure, primarily due to specialized tanks, dielectric fluids, and redesign requirements. Retrofitting existing raised-floor data centers adds further complexity, often requiring reinforcement, liquid containment systems, and electrical and safety redesigns. These modifications significantly increase deployment timelines and engineering costs. Payback periods extend beyond the typical 3–5 year investment horizon preferred by many mid-sized colocation and enterprise operators, limiting broader adoption outside hyperscale players.

Limited Fluid Standardization and Supply Chain Dependency Risks

The immersion cooling market lacks a universally adopted dielectric fluid standard, with industry guidance primarily provided by organizations such as ASHRAE TC 9.9 rather than formal specifications. This creates risks of vendor lock-in, fluid compatibility uncertainty, and potential warranty limitations when switching suppliers or systems.

The supply chain for specialized fluorocarbon-based fluids is highly concentrated among a limited number of chemical producers. The planned global phase-out of PFAS-based products by key suppliers such as 3M by the end of 2025, driven by regulatory and litigation pressures, further increases supply uncertainty and procurement risk for operators.

Opportunities - Edge Computing Densification Opening a New Addressable Market for Compact Immersion Systems

Edge computing expansion driven by 5G densification and distributed cloud architectures is creating a structurally new demand segment for compact, modular immersion cooling systems. Telecom operators and infrastructure vendors are increasingly deploying compute closer to end users to reduce latency, which significantly increases heat density at edge nodes. This shift is encouraging adoption of self-contained liquid cooling units designed for constrained and non–data center environments.

Initiatives supporting rural broadband and 5G expansion, along with telecom ecosystem collaborations involving companies such as Nokia and immersion cooling vendors such as Submer Technologies, reflect growing interest in edge-optimized thermal solutions.. Vendors with IP-rated, remotely managed, and field-serviceable designs are best positioned to capture this emerging opportunity.

Sovereign AI and National HPC Programmes Creating Government-Backed Demand Pools

Sovereign AI initiatives and national high-performance computing (HPC) programs are generating long-term, price-inelastic demand for advanced liquid cooling technologies, including immersion cooling in select deployments. Governments across Europe and other regions are investing heavily in domestic AI infrastructure to reduce dependence on hyperscaler cloud ecosystems, leading to multi-year procurement pipelines. Programs such as France’s France 2030 initiative and the European Union’s EuroHPC Joint Undertaking are supporting deployment of next-generation supercomputing systems. These systems increasingly require high-efficiency thermal management solutions, primarily direct-to-chip liquid cooling, with growing evaluation of immersion cooling for extreme density workloads.

Category-wise Analysis

Component Insights

Solution segment accounts for over 70% of the global immersion cooling market share in 2026, equivalent to US$ 481.3 million, due to the need for fully integrated, turnkey cooling infrastructure in hyperscale and high-performance computing environments. Buyers typically prefer complete systems including immersion tanks, fluid distribution, and heat rejection units rather than sourcing components separately, as integrated procurement reduces engineering risk and deployment complexity.

Large-scale operators prioritize vendor accountability for system performance, especially when deploying thousands of servers across dense computing clusters. This ensures operational consistency and minimizes internal design burden, reinforcing the dominance of solution-led procurement models.

Services are the fast-growing component, supported by the increasing demand for operational expertise in managing liquid-based cooling environments. Many enterprises and data center operators lack in-house capabilities for immersion fluid maintenance, monitoring, and lifecycle optimization. Managed services covering predictive maintenance, fluid health monitoring, and system optimization are gaining traction. These service models help reduce operational risk while ensuring sustained cooling efficiency and system reliability over time. This shift reflects a broader transition from hardware-only adoption to long-term service-based engagement.

Cooling Type Insights

Single phase is poised for more than 63% share in 2026, reaching over US$ 433.1 million, driven by operational simplicity, lower maintenance requirements, and compatibility with existing data center hardware ecosystems. The cooling fluid remains in a stable liquid state, eliminating the complexity associated with phase change processes. This reduces engineering challenges and improves reliability, making it particularly attractive for enterprise deployments and crypto mining operations. The segment’s maturity and well-established vendor ecosystem further strengthen its position as the preferred deployment choice.

Two phase is the fast-growing cooling type, supported by its ability to handle significantly higher heat loads in advanced computing environments. It enables efficient thermal management at rack densities exceeding 200 kW, where conventional and single-phase systems struggle to perform effectively. The use of vaporization-based heat transfer allows superior cooling efficiency, making it suitable for next-generation AI and semiconductor-intensive workloads. This capability is increasingly important as compute density continues to rise in AI training and advanced HPC systems.

Cooling Fluid Insights

Mineral oil is likely to account for over 38% share by 2026, surpassing the value of US$ 261.3 Million, due to cost efficiency, wide availability, and well-established electrical insulation properties. Operators value mineral oil because it provides a proven and low-risk cooling medium with extensive historical usage in industrial electrical applications. Its relatively low cost compared to engineered fluids makes it particularly attractive for large-scale deployments where capital efficiency is critical. This has made it a default choice for applications such as cryptocurrency mining and cost-sensitive computing infrastructure.

Bio-Based/Dielectric Fluids is the fastest growing category, supported by increasing environmental regulations and sustainability commitments. Operators are actively shifting away from fluorocarbon-based fluids due to regulatory pressure and ESG compliance requirements. Bio-based alternatives offer improved environmental profiles while still delivering effective thermal performance for data center applications. Their adoption is further supported by corporate sustainability reporting obligations and long-term decarbonization goals. This is accelerating their integration into next-generation immersion cooling deployments.

Application Analysis

Artificial intelligence & machine learning accounts for over 35.0% of the global immersion cooling market share in 2026, reaching over US$ 240.6 Million, due to the extremely high-power density generated by GPU-intensive AI workloads, which exceeds the limits of traditional air cooling systems. Immersion cooling becomes essential in maintaining stable GPU performance and preventing thermal throttling in large-scale training environments. Hyperscalers and AI-native cloud providers are increasingly designing infrastructure around liquid cooling from the outset. This ensures continuous high-performance computation required for advanced model training and inference workloads.

High-Performance Computing (HPC) is the fastest growing application, supported by strong public and institutional investment in supercomputing infrastructure. National research programs and scientific computing initiatives require advanced thermal solutions to support continuous, high-intensity workloads. Immersion cooling enables stable operation of next-generation HPC systems operating at extreme compute densities. It is increasingly becoming a standard requirement in procurement for advanced research computing environments. This is driving rapid adoption across academic, government, and scientific institutions globally.

Regional Insights

North America Immersion Cooling Market Trends and Insights

North America remains the dominant region, accounting for over 38.0% of the global market in 2026 and reaching US$ 261.25 Million, supported by its dense hyperscale data center footprint and the most advanced AI infrastructure deployment cycle globally. The region benefits from strong structural tailwinds driven by rapid AI model training and inference workloads, which are significantly increasing thermal management requirements. Policy support such as the U.S. Inflation Reduction Act is further enhancing adoption by improving the economics of energy-efficient and low-carbon data center designs.

The United States Immersion Cooling Market is expected to reach over US$ 222.06 Million by 2026, driven by large-scale capital expenditure programs from hyperscalers such as Amazon Web Services, Microsoft Azure, and Google Cloud, all actively integrating advanced liquid cooling solutions into new and existing data center builds. State-level incentive frameworks, particularly in Virginia, the largest data center hub globally by installed capacity, are accelerating deployment momentum.

Europe Immersion Cooling Market Trends and Insights

Europe is expected to register for more than 24% share in 2026, reaching US$ 165 Million, with growth strongly anchored in regulatory compliance pressures under the EU Energy Efficiency Directive and the European Green Deal. These frameworks are compelling data center operators to actively reduce PUE levels and transition toward high-efficiency cooling architectures, including immersion systems. The region’s demand profile is structurally premium-oriented, favoring compliance-certified, energy-optimized solutions over conventional air cooling.

Germany is likely to account for nearly 22% of the Europe immersion cooling market in 2026, valued at US$ 36.30 Million, supported by Frankfurt’s dense colocation ecosystem and major operators such as Equinix and Digital Realty. The country benefits from strong AI compute demand, climate targets under the Climate Action Programme 2030, and continuous hyperscale expansion, making it Europe’s largest data center hub by installed capacity.

The United Kingdom immersion cooling market value is reaching over US$ 28.05 Million, driven by London’s high-density financial trading infrastructure and early adoption of GPU and FPGA-accelerated workloads. France exceeding US$ 21.45 Million value in 2026, supported by sovereign AI initiatives under Plan France 2030 and OVHcloud’s liquid-cooled infrastructure expansion across key campuses.

In the Netherlands, Amsterdam functioning as a major interconnection and colocation hub anchored by AMS-IX. Regulatory constraints on new hyperscale data center builds are accelerating adoption of high-density immersion systems within existing footprints to maximise compute efficiency. In Nordics, particularly Sweden and Finland, where renewable energy availability and strong HPC clustering support advanced cooling adoption. Finland’s LUMI supercomputer further reinforces liquid cooling benchmarks, creating a scalable reference model for future HPC and AI infrastructure deployments across the region.

Asia Pacific Immersion Cooling Market Trends and Insights

Asia Pacific is more likely to register over 31% of the global immersion cooling market share in 2026, reaching approximately US$ 213.12 Million, and is the fastest-growing regional market with a CAGR of 28.9%, driven by state-backed AI, HPC, and digital infrastructure programmes. National initiatives such as China’s 14th Five-Year Plan for digital infrastructure and India’s IndiaAI Mission, which has committed INR 10,372 crore toward domestic AI compute capacity, are accelerating demand for advanced thermal management solutions. As sovereign AI ambitions scale, data center construction pipelines are increasingly embedding immersion cooling as a baseline requirement for high-density workloads.

China immersion cooling market is expected to reach US$91.64 Million by 2026, making it the dominant country in the region. The growth is strongly supported by the Ministry of Industry and Information Technology’s push for sub-1.3 PUE targets in new data centers and the national East Data West Computing initiative, which is building large-scale hyperscale clusters across eight hub regions. Japan market value is reaching approximately US$ 34.10 Million, driven by HPC leadership through programmes such as Moonshot R&D and the influence of the Fugaku supercomputer, which has normalized liquid cooling adoption in high-performance environments.

India immersion cooling market is reaching over US$ 21.31 Million in 2026 & expected to grow at the highest rate and is transitioning from early adoption to accelerated deployment as AI compute demand rises sharply under the IndiaAI Mission. Major data center operators, including Adani Enterprises’ data center arm and CtrlS Datacenters, are actively evaluating immersion cooling for next-generation facilities in key hubs like Mumbai and Hyderabad. South Korea growth is supported by semiconductor-led HPC infrastructure from Samsung Electronics and SK Hynix, where immersion cooling enables continuous high-power chip validation. Government support through the K-Cloud Project further strengthens demand visibility, ensuring sustained adoption momentum across advanced compute ecosystems.

Competitive Landscape

The global immersion cooling market is moderately consolidated, with a mix of established players and emerging specialist vendors competing for market share. Competition is largely driven by the breadth of fluid compatibility across different hardware ecosystems, ensuring safe and efficient performance across diverse server architectures.

Vendors are increasingly focusing on their ability to provide validated, plug-and-play configurations for leading server platforms from NVIDIA, AMD, and Intel. The competitive landscape is further being reshaped by hyperscaler-adjacent OEM partnerships, which are accelerating adoption and enabling large-scale deployments.

Key Developments:

- In March 2026, GRC partnered with UNICOM Engineering to launch fully integrated immersion-cooled AI infrastructure solutions for data centers and edge deployments. The collaboration aims to simplify adoption of immersion cooling technology while improving thermal efficiency, scalability, and support for high-density AI and HPC workloads.

- In March 2026, Asperitas partnered with UNICOM Engineering to deliver a single-contract immersion-cooled compute infrastructure solution for AI, HPC, and data center applications. The collaboration simplifies deployment of immersion cooling systems by combining validated servers, cooling technology, and integrated support under one commercial framework.

- In February 2026, Perstorp expanded its data center liquid cooling portfolio by launching new Synmerse immersion cooling fluids and Synplate cold plate solutions for AI and high-performance computing applications. The new PFAS-free and biodegradable cooling fluids are designed to improve thermal efficiency, fire safety, and sustainability in next-generation data centers.

Companies Covered in Global Immersion Cooling Market

- Green Revolution Cooling (GRC)

- LiquidStack

- Submer Technologies

- Iceotope Technologies

- Asperitas

- Midas Green Technologies

- LiquidCool Solutions

- DCX The Liquid Cooling Company

- Schneider Electric

- Vertiv Group Corp.

- Rittal GmbH & Co. KG

- STULZ GmbH

- CoolIT Systems

- Asetek

- Others

Frequently Asked Questions

The immersion cooling market is valued at US$ 687.5 million in 2026 and is projected to reach US$ 3,116.7 million by 2033, growing at a CAGR of 24.1%, driven by rising demand for GPU-dense AI infrastructure that exceeds the limits of traditional air cooling.

The growth is driven by rapidly increasing power density in AI computing hardware and stricter energy efficiency regulations like the EU Energy Efficiency Directive. These forces are pushing data centers toward immersion cooling as both a performance necessity and compliance requirement.

Solution segment leads with 70.0% market share, as customers prefer integrated systems including tanks, fluid loops, and heat rejection units. This reduces integration complexity and risk, making turnkey solutions the dominant procurement model in early-stage adoption.

North America holds the largest share at nearly 38.0% in 2026, supported by dense hyperscale data center infrastructure and strong AI investment from major cloud providers. Policy support such as the U.S. CHIPS and Science Act further accelerates regional adoption.

The key opportunities lie in sovereign AI and national HPC programs funded by governments across Europe, Asia, and the Middle East. These projects demand high-performance, energy-efficient cooling solutions with long-term reliability and certified supply chains.

The leading companies include Green Revolution Cooling (GRC), LiquidStack, Submer Technologies, Iceotope Technologies, Asperitas, DCX The Liquid Cooling Company, LiquidCool Solutions among others.