- Technology

- Artificial Intelligence Systems Spending Market

Artificial Intelligence Systems Spending Market Size, Share, and Growth Forecast, 2026 - 2033

Artificial Intelligence Systems Spending Market by Component (Software, Hardware, Services), Deployment (Cloud, On-Premise, Edge), Vertical Industry (BSFI, Healthcare, IT-Telecom, Others), and Regional Analysis 2026 - 2033

Artificial Intelligence Systems Spending Market Size and Trends Analysis

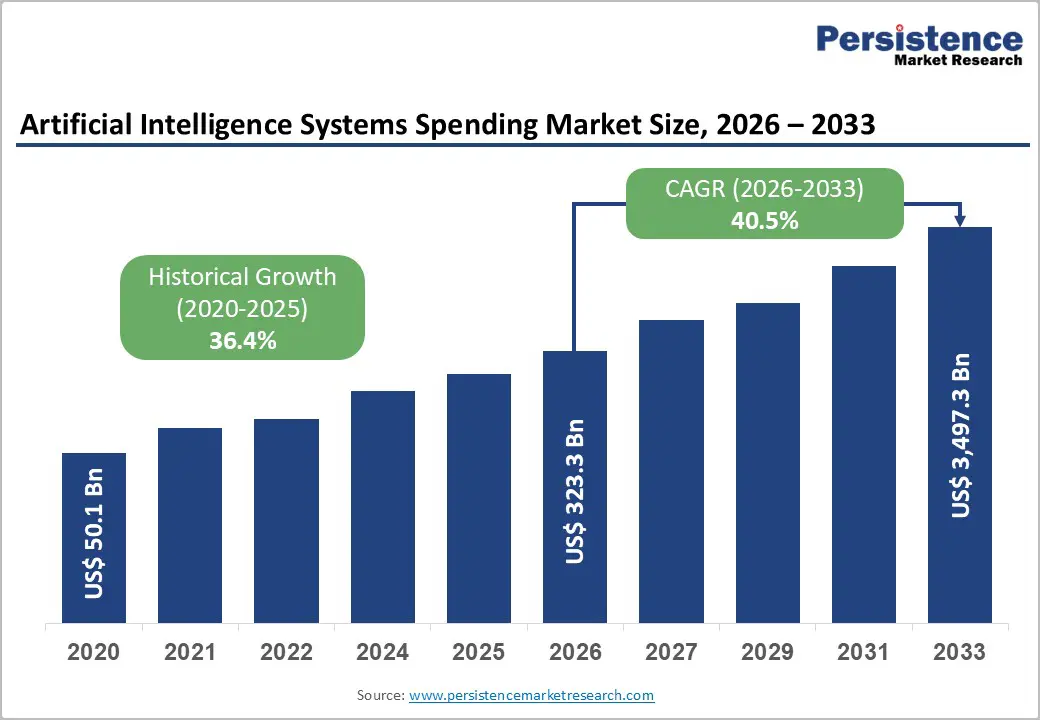

The global artificial intelligence systems spending market size is likely to be valued at US$323.3 billion in 2026 and is expected to reach US$3,497.3 billion by 2033, growing at a CAGR of 40.5% during the forecast period from 2026 to 2033, driven by the rapid integration of AI across primary industry sectors, which fundamentally drives this continuous market expansion.

Growth stems from rising adoption in the BFSI and healthcare sectors, advancements in deep learning and NLP technologies, and surging investments in AI infrastructure. Key macroeconomic trends, including widespread enterprise digitization and advancements in computing infrastructure, establish a robust foundation for scalable AI deployment. Mounting competitive pressures compel organizations to adopt advanced algorithms for operational efficiency.

Key Industry Highlights:

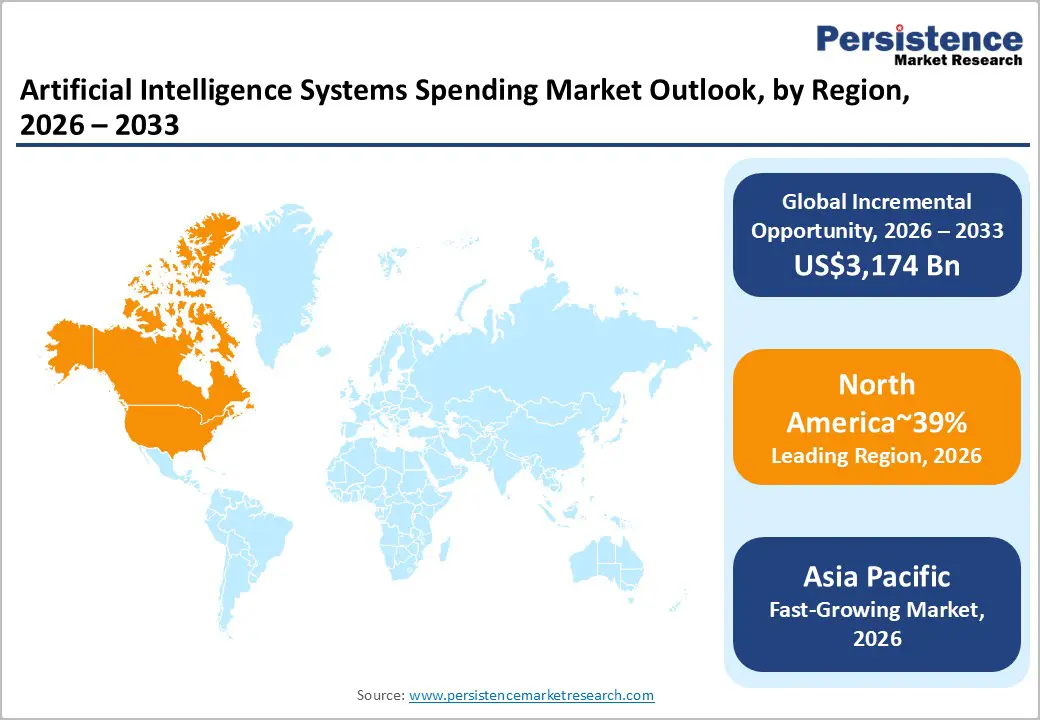

- Leading Region: North America, accounting for a market share of around 39%, driven by strong enterprise AI adoption, advanced digital infrastructure, and ecosystem advantages.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to industrial digitization, government policy support, and adoption across BFSI, healthcare, and smart city sectors.

- Leading Deployment: Public cloud is expected to lead, accounting for approximately 44% share in 2026, driven by scalable enterprise adoption, elastic compute, model throughput, and high-value AI applications.

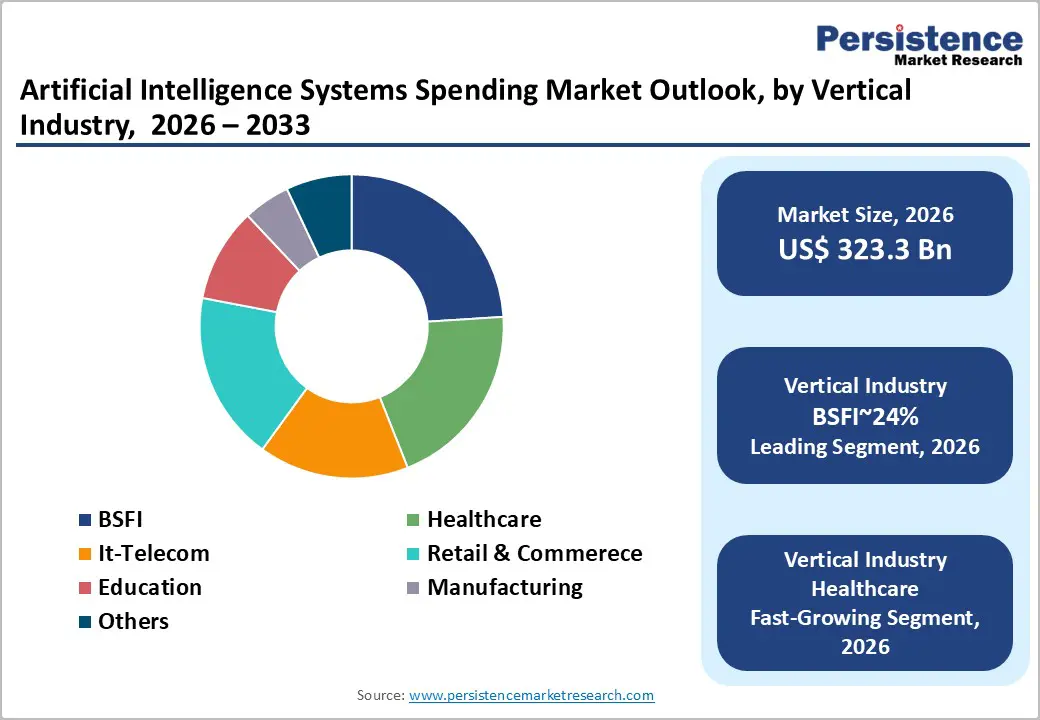

- Leading Vertical Industry: BFSI is projected to dominate for simplicity, regulatory compliance, adoption, and functional use across key sectors, holding approximately 24% share in 2026.

| Key Insights | Details |

|---|---|

| Artificial Intelligence Systems Spending Market Size (2026E) | US$323.3 Bn |

| Market Value Forecast (2033F) | US$3,497.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 40.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 36.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Cloud Native Artificial Intelligence Infrastructure and Accelerated Enterprise Modernization

The rapid proliferation of cloud native artificial intelligence platforms is structurally accelerating global Artificial Intelligence Systems Spending across enterprise ecosystems. Hyperscale offerings such as Microsoft Azure OpenAI, Amazon Bedrock, and Google Vertex AI embed scalable model deployment within enterprise architectures. Parallel investments in accelerated computing infrastructure, including advanced graphics processing units from NVIDIA and Advanced Micro Devices, enhance throughput for data intensive workloads. This infrastructure maturation lowers performance bottlenecks and standardizes access to high capacity model training environments.

Enterprises are reallocating digital transformation budgets toward intelligent automation and predictive analytics capabilities. Infrastructure as a service architectures shift expenditure from capital intensity toward operating expenditure models. This transition mitigates balance sheet constraints while enabling continuous scalability across distributed environments. Regulatory scrutiny around data governance further incentivizes centralized cloud orchestration and auditability. Collectively, these dynamics embed artificial intelligence deployment within core enterprise computing stacks, expanding addressable spending across software, hardware, and managed services layers.

Institutionalization of Data Centric Decision Architectures across Enterprise Value Chains

The exponential expansion of enterprise data across digital interfaces necessitates advanced analytical orchestration capabilities. Organizations increasingly deploy machine learning and natural language processing to operationalize unstructured datasets. These frameworks transform fragmented information streams into predictive and prescriptive intelligence layers. Sectors including banking, financial services, retail, and supply chains integrate analytics into core workflows. Regulatory reporting, fraud surveillance, and customer lifecycle management increasingly depend on algorithmic modeling precision.

Executive mandates now position artificial intelligence as a foundational enterprise decision infrastructure. Integration into standardized business applications embeds analytics directly within transactional systems. Retrieval augmented generation and semantic search architectures enhance knowledge discovery across distributed repositories. Demonstrable operational efficiency gains reinforce sustained budget reallocation toward advanced analytics ecosystems. Spending expands across data engineering, model governance, cybersecurity compliance, and cloud optimization layers.

Barrier Analysis - Escalating Deployment Expenditure and Structural Infrastructure Complexity

The progression from pilot initiatives to enterprise-scale deployments introduces material financial strain. Organizations encounter elevated expenditure across licensing, proprietary data storage, and model optimization cycles. Continuous fine-tuning of large language architectures amplifies compute intensity and infrastructure utilization. The scarcity of specialized artificial intelligence engineers and data scientists inflates wage structures globally. These cost pressures disrupt projected efficiency gains embedded within digital transformation roadmaps.

Capital requirements for localized accelerated computing infrastructure remain operationally burdensome across industries. Dependence on hyperscale cloud ecosystems heightens exposure to pricing volatility and contractual rigidity. Vendor concentration risks complicate workload portability and long-term architectural flexibility. Regulatory compliance mandates further increase governance overhead across distributed artificial intelligence systems. Collectively, infrastructure complexity and escalating operational expenditure constrain sustainable margin realization at scale.

Algorithmic Opacity and Escalating Governance Accountability Pressures

Limited transparency within complex algorithmic architectures undermines institutional trust across regulated industry environments. Opaque decision pathways complicate explainability requirements embedded within supervisory compliance frameworks. Regulatory regimes such as the General Data Protection Regulation mandate interpretable outputs for automated decision systems. Financial services and insurance sectors face heightened scrutiny regarding bias detection and model accountability. Audit failures materially increase project discontinuation risk and delay enterprise-wide deployment programs.

Ethical oversight requirements expand compliance expenditure across model validation and governance functions. Independent audit trails, documentation standards, and bias mitigation protocols lengthen development lifecycles. Cross-border data governance rules further intensify operational complexity within multinational deployments. Reputational exposure linked to discriminatory or untraceable outputs elevates board level risk sensitivity.

Opportunity Analysis - Synthetic Data Integration for Privacy Aligned Model Development

The expansion of synthetic data generation frameworks creates structurally significant opportunities within artificial intelligence training pipelines. Privacy legislation, such as the General Data Protection Regulation and the Health Insurance Portability and Accountability Act, constrains access to sensitive real-world datasets. Synthetic data architectures replicate statistical properties of regulated information without exposing personally identifiable elements. This capability reduces compliance risk while expanding training corpus availability across healthcare and computer vision domains. Accelerated model development cycles enhance operational responsiveness within data-restricted environments.

Demand reallocates toward data simulation platforms and validation tooling ecosystems. Reduced dependency on scarce real-world datasets lowers acquisition costs and legal exposure. Shortened model training timelines improve compute utilization efficiency and infrastructure throughput. Healthcare analytics and advanced vision systems benefit from controlled scenario generation capabilities. These dynamics position synthetic data as a strategic enabler of privacy-compliant artificial intelligence scaling.

Verticalized Artificial Intelligence Expansion across Healthcare, Autonomous Systems, Synthetic Data, and Operational Intelligence

The expansion of artificial intelligence across emerging healthcare systems creates structurally significant value chain opportunities. Digital health record modernization and diagnostic automation address unmet clinical capacity constraints. Deployment of advanced diagnostic models, including solutions pioneered by IBM, demonstrates scalable screening capabilities within resource constrained environments. Advanced deep learning diagnostics and robotic-assisted platforms improve procedural precision and resource allocation efficiency. Regulatory harmonization efforts across developing regions support scalable deployment of compliant medical intelligence systems. These dynamics expand demand for secure infrastructure, clinical analytics software, and interoperable data architectures.

Simultaneously, the evolution toward industry specific autonomous agents enhances enterprise workflow automation capabilities. Organizations require agentic systems capable of executing regulated, multi-step operational processes. Integration with legacy enterprise resource planning environments increases switching costs and embedded software revenues. Rising privacy constraints elevate demand for secure synthetic data ecosystems supporting model validation. Generative architectures optimized for structured and computer vision datasets strengthen operational intelligence monetization pathways. Collectively, these developments reposition artificial intelligence from experimental deployment toward mission-critical enterprise infrastructure.

Category-wise Analysis

Deployment Insights

Public cloud is expected to lead the global market, accounting for approximately 44.0% share, underpinned by its ability to deliver elastic compute, pre-trained models, and integrated development environments at scale. Hyper-scalers such as Amazon Web Services, Microsoft through Azure, and Google through Google Cloud provide GPU-dense clusters and model marketplaces that compress deployment timelines. GPU as a service offerings powered by advanced accelerators enable enterprises to avoid capital-intensive infrastructure buildouts. Integrated storage, orchestration, and machine learning toolchains reduce latency and streamline production-in-action across complex workflows. The operating expenditure model aligns with enterprise budgeting preferences while supporting burst training demand. This convergence of scalability, ecosystem depth, and compliance-ready infrastructure sustains public cloud dominance.

Public cloud is expected to be the fastest-growing, driven by escalating demand for high-performance training capacity and rapid experimentation cycles across industries. Enterprises increasingly adopt multi-cloud orchestration frameworks using Kubernetes and infrastructure automation tools to enhance portability and resilience. Serverless inference architectures lower entry barriers for startups and departmental innovation initiatives. Sovereign cloud zones and localized regions address data residency requirements while preserving centralized management efficiencies. Specialized providers such as Core Weave and Lambda Labs expand dedicated accelerator supply for compute-intensive workloads. As artificial intelligence workloads intensify, public cloud environments capture incremental spending through continuous optimization and service layer expansion.

Vertical Industry Insights

BFSI is expected to lead, accounting for approximately 24% of the global market share, supported by its structurally data-intensive operating model and continuous risk management requirements. Financial institutions embed artificial intelligence across fraud detection, algorithmic trading, credit underwriting, and regulatory reporting infrastructures. Large incumbents such as JPMorgan Chase and HSBC allocate sustained technology budgets toward generative models, legacy code modernization, and agentic automation. Platform partners, including FIS and Fiserv, integrate artificial intelligence directly into core banking stacks. Compliance mandates under Basel frameworks and the EU AI Act further intensify spending on explainable and auditable systems. This combination of defensive fraud mitigation and offensive revenue optimization sustains structural dominance within enterprise deployments.

Healthcare is expected to be the fastest-growing segment, driven by structural clinical capacity constraints and accelerating digital health data expansion. Providers deploy artificial intelligence across imaging diagnostics, robotic assisted interventions, and clinical decision support systems. Technology ecosystems led by Microsoft, Google Health, and NVIDIA enable multimodal analytics and scalable model training environments. Medical device innovators such as GE HealthCare and Medtronic embed artificial intelligence within imaging and therapeutic platforms. Workforce shortages and chronic disease prevalence accelerate automation of documentation, triage, and personalized treatment pathways. As validation pathways mature and hospital infrastructure digitizes, artificial intelligence becomes integral to care delivery economics and operational resilience.

Regional Insights

Asia Pacific Artificial Intelligence Systems Spending Market Trends

Asia Pacific is expected to register the fastest growth trajectory, driven by large-scale industrial digitization, urbanization, and manufacturing modernization. Regional momentum is anchored by China, Japan, and India, where government-led AI initiatives, sovereign cloud deployments, and high-volume data ecosystems accelerate enterprise adoption across BFSI, healthcare, and smart city infrastructure. Core demand drivers include predictive maintenance, robotic process automation, and supply chain optimization, while technological enablers such as edge AI, multilingual foundation models, and generative AI platforms support rapid scaling. The competitive landscape is highly dynamic, with dominant regional players including Alibaba Cloud, Baidu, Huawei, and Tencent competing alongside emerging startups, fostering ecosystem depth. Investment flows are concentrated in AI-enabled manufacturing, digital commerce logistics, and next-generation data center expansion, supported by regional 5G and IoT proliferation. Fragmented regulatory frameworks are gradually evolving into enforceable statutes, balancing innovation promotion with data localization and security requirements.

China anchors regional growth, shaping Asia Pacific’s trajectory through massive state-backed AI R&D, advanced semiconductor and GPU infrastructure, and industrial digitalization programs. National policies prioritize domestic AI stack development, sovereign large language models, and integration of generative and agentic AI across high-value sectors. Vendor strategies focus on localized platforms, predictive industrial applications, and workforce upskilling, while capital allocation targets high-impact verticals, including manufacturing, healthcare, and e-commerce logistics. China’s ecosystem of hyperscalers, AI startups, and research institutions ensures robust industrial scaling, enabling Asia Pacific to remain the fastest-growing regional market through the forecast horizon, with technology adoption and regulatory alignment evolving in tandem to sustain exponential AI expansion.

North America Artificial Intelligence Systems Spending Market Trends

North America is expected to remain the leading regional market, accounting for approximately 39% of global AI deployment in 2026, supported by deep enterprise penetration, mature digital infrastructure, and concentrated innovation ecosystems. The region’s dominance is structurally anchored by high-performance computing infrastructure, advanced semiconductor manufacturing, and hyper-scaler-led cloud platforms such as AWS, Microsoft Azure, and Google Cloud Platform. Widespread adoption of agentic AI and vertical-specific models across BFSI, healthcare, and defense sectors reinforces replacement cycles and operational intensity. Enterprise demand is driven by automation, historical dataset availability, and scalable AI-as-a-Service solutions, while massive venture capital inflows accelerate the commercialization of both specialized AI hardware and software. Leading vendors, including Microsoft, NVIDIA, OpenAI, Anthropic, and IBM, further cement North America’s structural leadership through integrated AI ecosystems, cloud orchestration, and next-generation foundation model deployment, ensuring sustained technological and industrial dominance.

The U.S. is positioned to anchor North American momentum through its dense concentration of AI innovators, robust R&D investment, and market-leading infrastructure. Federal initiatives and state-specific legislation, such as the California AI Transparency Act, shape deployment while supporting enterprise trust frameworks and ethical AI adoption. U.S.-based cloud providers and infrastructure partners are expected to expand sovereign, hybrid, and multi-cloud architectures to meet domestic computational demand, while specialized AI startups continue to commercialize autonomous agents and multimodal systems across high-value sectors. As venture capital and industrial investment flows persist, the U.S. will continue driving regional growth, reinforcing North America’s status as the primary reference market for AI innovation, operational deployment, and technology export leadership.

Europe Artificial Intelligence Systems Spending Market Trends

Europe is expected to remain a mature and structurally stable AI market, with demand primarily anchored in replacement cycles, compliance-driven upgrades, and enterprise optimization strategies rather than greenfield capacity expansion. Market positioning is reinforced by industrial automation in Germany, the U.K., and France, where AI adoption spans automotive, energy management, and public-sector workflows. Structural drivers include rich public and industrial datasets, multilingual AI requirements, and SME inclusion initiatives, while technological momentum is sustained through sovereign cloud deployments, deep learning, and generative AI integration. Leading vendors, such as SAP AI, Aleph Alpha, DeepMind, Mistral AI, and DeepL, reinforce adoption through enterprise-ready platforms, federated learning frameworks, and energy-efficient AI systems, ensuring high operational resilience despite a rigorous regulatory environment dominated by the EU AI Act, GDPR alignment, and emerging digital compliance mandates.

Germany anchors regional AI performance, shaping Europe’s steady momentum through its industrial depth, advanced manufacturing digitization, and automotive sector leadership. National initiatives supporting sovereign large language models and energy-efficient AI infrastructure drive enterprise adoption while ensuring alignment with stringent EU regulatory frameworks. Vendor strategies focus on combining localized AI platforms with ethical and privacy-preserving technologies, and industrial investment flows emphasize synthetic data, machine vision, and generative AI for high-value applications. Germany’s ecosystem of established multinationals and innovative startups ensures predictable replacement cycles, drives knowledge transfer across the EU, and reinforces Europe’s role as a stable, compliance-oriented regional AI hub through the forecast horizon.

Competitive Landscape

The global artificial intelligence systems spending market is moderately consolidated at the infrastructure level, with leadership concentrated among major players such as Microsoft, Google, AWS, and NVIDIA, while remaining highly fragmented across application and software layers where specialized startups operate. This dual structure shapes a competitive environment in which hyperscalers exert significant influence over cloud platforms, AI compute resources, and foundational model deployment, whereas smaller entities focus on niche solutions, industry-specific applications, and customized integrations, reflecting a bifurcated ecosystem with differentiated capabilities across segments. Market behavior is driven by enterprise demand for scalable AI infrastructure, the proliferation of large language models, and an evolving regulatory landscape emphasizing security, data privacy, and compliance, which collectively guide procurement and technology adoption choices across sectors.

Leading players are significant due to their control over critical compute and AI service ecosystems, enabling widespread influence on technology standards, platform interoperability, and enterprise operational workflows. Competitive positioning is marked by horizontal integration of cloud and AI platforms, vertical specialization in industry-focused models, and differentiated service offerings, including hardware, software, and lifecycle management. Industry dynamics indicate sustained emphasis on platform consolidation, strategic partnerships, and mergers or acquisitions, with hyperscalers expanding both infrastructure and ecosystem footprints, while startups continue to innovate in niche operational areas, ensuring a forward-looking, multi-tiered market evolution across global AI spending.

Key Industry Developments:

- In June 2025, Salesforce launched Agentforce 3 with a new "Command Center" for observability, giving enterprises visibility, monitoring, and tracing of AI and human interactions to overcome scaling barriers.

- In May, 2025 Siemens introduced Industrial AI Agents, embedding agentic AI into factory floors for production planning and quality assurance.

- In May 2025, NVIDIA released the Vera CPU, designed for AI supercomputing clusters, enabling 100k+ GPU clusters to run more efficiently and completing the full-stack hardware requirement.

Companies Covered in Artificial Intelligence Systems Spending Market

- Microsoft Corporation

- Alphabet Inc. (Google)

- NVIDIA Corporation

- Amazon Web Services (AWS)

- IBM Corporation

- OpenAI

- Meta Platforms Inc.

- Accenture plc

- Anthropic

- Baidu, Inc.

- Alibaba Cloud

- Infosys Limited

- DataRobot, Inc.

- Hugging Face

- Intel Corporation

- AMD

Frequently Asked Questions

The global artificial intelligence systems spending market is projected to be valued at US$323.3 billion in 2026, driven by adoption across BFSI, healthcare, and enterprise digital transformation initiatives, alongside rapid expansion of AI infrastructure and cloud-native platforms.

Enterprises increasingly integrate AI into core workflows to enhance operational efficiency, predictive analytics, and intelligent automation. Investments in cloud-native infrastructure, accelerated computing, and large language models facilitate scalable deployment while addressing regulatory compliance, workflow optimization, and data governance requirements.

The artificial intelligence systems spending market is forecast to grow at a CAGR of 40.5% between 2026 and 2033, reflecting accelerated adoption of AI across industry verticals, generative and agentic models, and large-scale infrastructure investments.

Asia Pacific is anticipated to exhibit the fastest growth, supported by China, India, and Japan. Expansion is fueled by industrial digitization, smart city initiatives, sovereign cloud deployments, and the adoption of edge AI, generative platforms, and multilingual foundation models across BFSI, healthcare, and manufacturing sectors.

The artificial intelligence systems spending market is moderately consolidated at the infrastructure level and fragmented across applications. Key players include Microsoft, Google, AWS, NVIDIA, IBM, OpenAI, Meta, Accenture, Anthropic, Baidu, Alibaba Cloud, Infosys, DataRobot, Hugging Face, Intel, and AMD. These entities influence technology standards, cloud platforms, and enterprise AI adoption, while start-ups focus on niche, industry-specific solutions.