- Medical Devices

- Artificial Vital Organs and Medical Bionics Market

Artificial Vital Organs and Medical Bionics Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Artificial Vital Organs and Medical Bionics Market by Product (Artificial Vital Organs and Medical Bionics), by Technology (Mechanical and Electronic), by End User (Hospitals, Specialty Clinics, and Ambulatory Surgical Centers), and Regional Analysis from 2026 to 2033.

Artificial Vital Organs and Medical Bionics Market Share and Trend Analysis

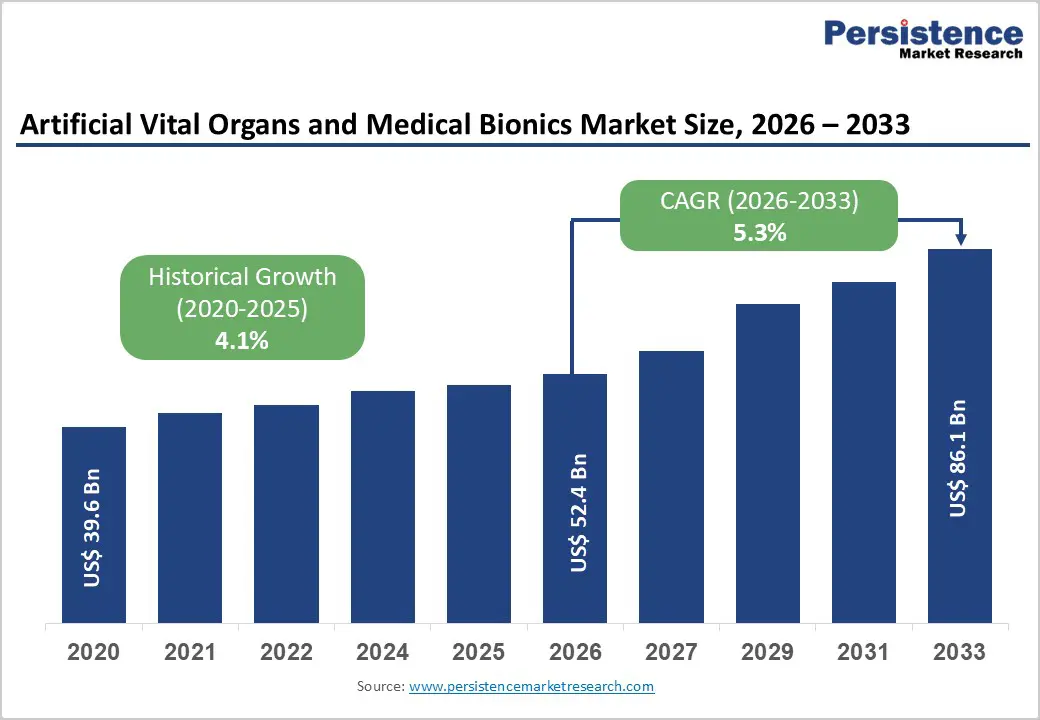

The global artificial vital organs and medical bionics market size is estimated to grow from US$ 52.4 Bn in 2026 to US$ 86.1 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for artificial vital organs and medical bionics is rising steadily, driven by the increasing burden of organ failure, persistent shortages of donor organs, and growing adoption of advanced life-sustaining and rehabilitative technologies. Hospitals and specialty care centers are increasingly integrating artificial hearts, ventricular assist devices, dialysis systems, and advanced bionic implants to manage end-stage cardiac, renal, neurological, and mobility-related conditions. Aging populations, higher prevalence of chronic diseases, and improved survival rates from acute medical events are significantly expanding the patient pool requiring long-term organ support and functional restoration. Medical bionics are gaining traction due to their ability to enhance quality of life, restore mobility, and improve sensory or neurological function. Continuous technological advancements in biomaterials, robotics, sensors, and digital monitoring are improving device safety, durability, and clinical outcomes. Regulatory focus on patient safety and clinical efficacy, along with expanding reimbursement coverage in developed markets, further supports adoption. At the same time, healthcare infrastructure expansion and rising investments in critical care and specialty treatment facilities in emerging markets are reinforcing long-term global demand for artificial vital organs and medical bionics.

Key Industry Highlights

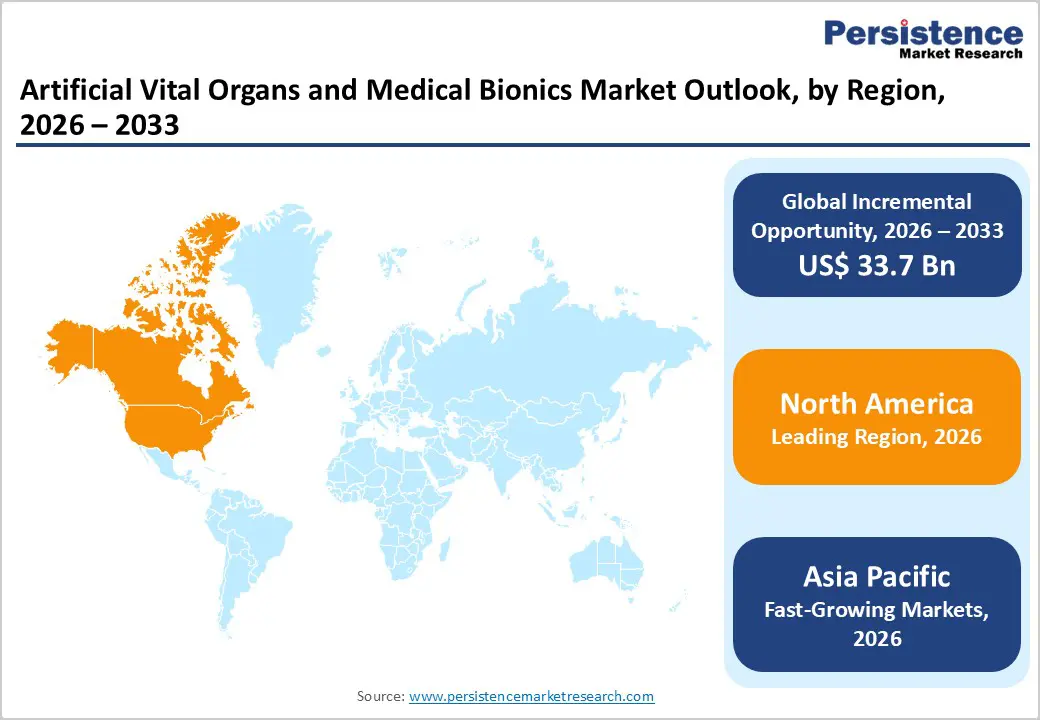

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high prevalence of chronic diseases, strong reimbursement frameworks, and early adoption of innovative artificial organ and bionic technologies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid healthcare infrastructure development, rising disease burden, increasing access to advanced treatments, and growth of private hospitals and specialty centers.

- Leading Product Segment: Artificial Vital Organs dominate the market due to their critical role in sustaining life for patients with end-stage organ failure and limited transplant availability.

- Fastest-Growing Product Segment: Medical Bionics are growing rapidly as demand rises for mobility restoration, sensory implants, and neuro-bionic solutions that improve long-term quality of life.

- Leading End User Segment: Hospitals remain the top segment, driven by complex implantation procedures, critical care needs, and availability of specialized clinical infrastructure.

- Fastest-Growing User Segment: Specialty Clinics are expanding quickly as focused cardiac, renal, neurological, and rehabilitation centers increase adoption of advanced bionic and organ support technologies.

| Global Market Attributes | Key Insights |

|---|---|

| Artificial Vital Organs and Medical Bionics Market Size (2026E) | US$ 52.4 Bn |

| Market Value Forecast (2033F) | US$ 86.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver – Growing Burden of Organ Failure, Aging Population, and Advances in Life-Sustaining Technologies

Market growth is driven by the rising global burden of organ failure and degenerative conditions, particularly cardiovascular diseases, chronic kidney disease, respiratory disorders, and neurological impairments. An aging population is a major contributing factor, as older adults are more susceptible to end-stage organ dysfunction and mobility or sensory loss, increasing reliance on artificial vital organs and medical bionics. Persistent shortages of donor organs further accelerate demand for mechanical circulatory support systems, artificial hearts, dialysis technologies, and advanced bionic implants as bridge-to-transplant or long-term therapy solutions. Continuous technological advancements have significantly improved device safety, durability, and physiological compatibility, making artificial organs more clinically viable and widely accepted. Innovations such as miniaturized pumps, improved biomaterials, sensor-enabled monitoring, and enhanced power management systems are improving patient outcomes and survival rates.

Additionally, growing awareness among clinicians and patients regarding quality-of-life improvements offered by bionic limbs, cochlear implants, and neurostimulation devices is supporting adoption. Expanding healthcare expenditure, improved access to advanced surgical care, and favorable reimbursement frameworks in developed markets further reinforce sustained demand across hospitals and specialty centers.

Restraints – High Device Costs, Complex Regulatory Pathways, and Clinical Adoption Barriers

Market expansion is constrained by the high cost associated with artificial vital organs and advanced medical bionics, which can limit accessibility, particularly in cost-sensitive and resource-limited healthcare systems. These devices often involve sophisticated engineering, premium biomaterials, and complex manufacturing processes, resulting in significant upfront costs for hospitals and patients. In addition, long and stringent regulatory approval processes for implantable and life-sustaining devices can delay product commercialization and increase development expenses. Clinical adoption barriers also persist, including the need for highly specialized surgical expertise, extensive clinician training, and long-term patient monitoring infrastructure. Concerns related to device longevity, infection risk, mechanical failure, and post-implantation complications may influence physician and patient decision-making.

In emerging markets, limited availability of specialized centers and trained personnel further restricts adoption. Reimbursement variability across regions and incomplete insurance coverage for certain bionic and artificial organ therapies can also discourage utilization. Collectively, financial constraints, regulatory complexity, clinical risk considerations, and infrastructure gaps continue to temper market penetration despite strong underlying demand.

Opportunity – Technological Innovation, Emerging Market Expansion, and Shift Toward Patient-Centric Care

Significant opportunities are emerging from rapid technological innovation and expanding healthcare access in emerging economies. Advances in robotics, artificial intelligence, sensor integration, and smart monitoring systems are enabling the development of next-generation artificial organs and bionic devices with improved precision, adaptability, and patient outcomes. Growing focus on patient-centric care is driving demand for solutions that enhance mobility, independence, and long-term quality of life, particularly in prosthetics, neuro-bionics, and sensory implants.

Emerging markets across Asia Pacific, Latin America, and the Middle East present substantial growth potential as governments invest in hospital infrastructure, critical care capacity, and advanced surgical services. Increasing medical tourism and local manufacturing initiatives are further improving affordability and access. Opportunities also exist in pediatric and long-term care segments, where durable and scalable artificial organ solutions are increasingly required. Strategic collaborations between device manufacturers, research institutions, and healthcare providers can accelerate innovation, clinical validation, and adoption. As healthcare systems move toward advanced, technology-driven treatment models, artificial vital organs and medical bionics are well positioned for sustained long-term growth.

Category-wise Analysis

By Product, Artificial Vital Organs Lead Due to Life-Sustaining Applications and High Clinical Dependency

Artificial vital organs are projected to dominate the global artificial vital organs and medical bionics market in 2026, accounting for a revenue share of 70.0%. Their leadership is driven by their critical role in sustaining life in patients with end-stage organ failure, including cardiac, renal, pulmonary, and hepatic conditions. Devices such as artificial hearts, ventricular assist devices, dialysis systems, and artificial lungs are increasingly used as bridge-to-transplant, destination therapy, or long-term organ replacement solutions. The growing prevalence of cardiovascular diseases, chronic kidney disease, and respiratory disorders, coupled with a persistent shortage of donor organs, continues to fuel demand. Advances in biocompatible materials, miniaturization, and long-term durability have significantly improved patient outcomes and device adoption. Additionally, increasing clinical acceptance, expanding reimbursement coverage in developed markets, and rising use of artificial organs in critical care and specialty hospitals further reinforce their dominant position within the overall market.

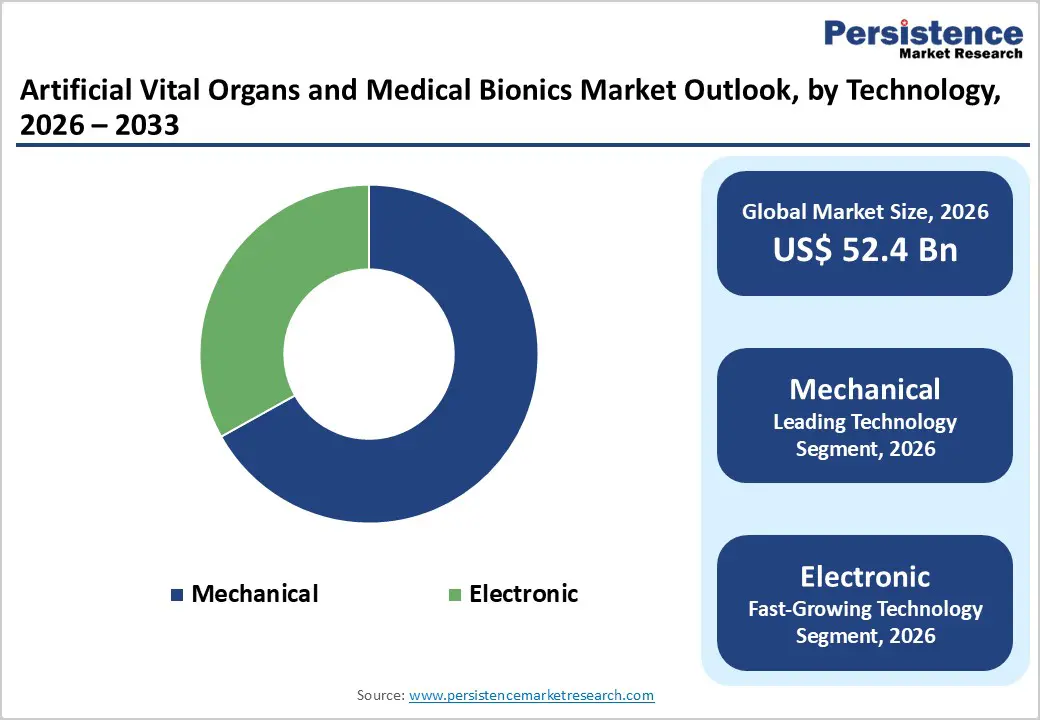

By Technology, Mechanical Systems Dominate Due to Proven Reliability and Established Clinical Adoption

Mechanical technologies are expected to dominate the global artificial vital organs and medical bionics market in 2026, capturing a revenue share of 66.9%. This dominance is primarily attributed to their long-standing clinical use, robust performance, and proven reliability in high-risk, life-supporting applications. Mechanical systems form the backbone of many artificial organs, including ventricular assist devices, artificial hearts, dialysis machines, and extracorporeal support systems, where consistent and predictable performance is critical. Healthcare providers favor mechanical technologies due to their durability, well-documented clinical outcomes, and compatibility with existing hospital infrastructure. Cost-effectiveness compared to advanced electronic or hybrid solutions further supports widespread adoption, particularly in emerging markets. While electronic and biomechanical technologies are gaining momentum through innovations such as neural interfaces and sensor-enabled systems, mechanical solutions remain the standard of care in many critical applications, ensuring their continued leadership in the market.

By End User, Hospitals Lead Due to Complex Procedures and High Volume of Critical Care Patients

Hospitals are projected to dominate the global artificial vital organs and medical bionics market in 2026, accounting for a revenue share of 50.0%. This leadership is driven by the concentration of complex surgical procedures, intensive care units, and multidisciplinary clinical teams required for the implantation, operation, and long-term management of artificial organs and advanced bionic devices. Hospitals manage a high volume of patients with severe organ failure, trauma, and chronic conditions, necessitating continuous use of life-sustaining technologies. The availability of specialized infrastructure, including cardiac catheterization labs, transplant units, and advanced monitoring systems, further supports adoption. Hospitals also play a central role in clinical trials, regulatory compliance, and post-implantation follow-up care. While specialty clinics and ambulatory surgical centers are increasingly adopting select bionic solutions, hospitals remain the primary revenue contributors due to procedural complexity, patient acuity, and continuous demand.

Region-wise Insights

North America Artificial Vital Organs and Medical Bionics Market Trends

North America is expected to dominate the global artificial vital organs and medical bionics market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a highly advanced healthcare infrastructure, strong presence of leading medical device manufacturers, and early adoption of innovative life-support and bionic technologies. High prevalence of cardiovascular diseases, kidney failure, and age-related degenerative conditions continues to drive demand for artificial organs and advanced bionic implants. Favorable reimbursement frameworks and significant healthcare spending enable hospitals to adopt high-cost, technologically advanced solutions.

Regulatory bodies emphasize safety, clinical validation, and long-term performance, supporting trust and adoption among healthcare providers. North America also leads in clinical research, product approvals, and commercialization of next-generation artificial hearts, ventricular assist devices, and neuro-bionic systems. Increasing focus on remote monitoring, digital integration, and patient-centric care models is expected to sustain the region’s dominance as the most mature and revenue-generating market globally.

Europe Artificial Vital Organs and Medical Bionics Market Trends

The Europe artificial vital organs and medical bionics market is expected to grow steadily, supported by well-established healthcare systems and stringent regulatory oversight across countries such as Germany, the U.K., France, Italy, and Spain. European healthcare providers place strong emphasis on patient safety, clinical efficacy, and compliance with medical device quality and performance standards, driving consistent adoption of artificial organs and bionic technologies. An aging population and rising incidence of chronic diseases, particularly cardiovascular and renal disorders, are increasing demand for long-term organ support solutions.

Public healthcare systems across Europe are gradually integrating advanced artificial organ technologies to improve patient survival and quality of life. Expansion of specialized cardiac, nephrology, and rehabilitation centers further supports market growth. Additionally, ongoing investments in clinical research, cross-border healthcare collaboration, and adoption of minimally invasive implantation techniques contribute to stable market expansion, positioning Europe as a key and reliable regional market.

Asia Pacific Artificial Vital Organs and Medical Bionics Market Trends

The Asia Pacific artificial vital organs and medical bionics market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by rapid healthcare infrastructure development and rising demand for advanced medical technologies. Countries such as China, India, Japan, South Korea, and Australia are witnessing increased investments in hospital expansion, critical care facilities, and specialty treatment centers. Growing prevalence of cardiovascular diseases, diabetes-related kidney failure, and trauma cases is significantly increasing the need for artificial organs and bionic implants. Improving healthcare access, rising awareness of advanced treatment options, and expanding medical insurance coverage are supporting market penetration.

Cost-sensitive markets are increasingly adopting mechanical and modular artificial organ systems, while developed healthcare centers are investing in advanced bionics and hybrid technologies. Government healthcare reforms, increasing medical tourism, and local manufacturing initiatives further position Asia Pacific as the fastest-growing regional market.

Market Competitive Landscape

The global artificial vital organs and medical bionics market is highly competitive, with strong participation from companies such as SynCardia Systems, LLC, BiVACOR Inc., CARMAT, Jarvik Heart, Inc., Abbott, and Medtronic. These players leverage extensive global distribution networks, strong brand recognition, and diversified portfolios of artificial organs, mechanical circulatory support systems, and advanced bionic implants to address the growing burden of organ failure, chronic diseases, and unmet transplant needs across healthcare settings.

Their offerings emphasize device reliability, long-term performance, physiological compatibility, patient safety, and improved quality of life, with a focus on minimally invasive implantation, durability, and integration with digital monitoring and clinical workflows in hospitals and specialty centers. Continuous product innovation, regulatory approvals, clinical validation, biocompatible materials, and adherence to stringent international medical device standards remain critical for sustaining competitive positioning in the global artificial vital organs and medical bionics market.

Key Industry Developments:

- In June 2024, the Centre for Eye Research Australia, along with the Bionics Institute, the University of Melbourne, and the Royal Victorian Eye and Ear Hospital, published detailed results from a bionic eye clinical trial in Ophthalmology Science. The study demonstrated that the second-generation bionic eye developed by Bionic Vision Technologies delivered rapid functional improvements in four patients with blindness caused by retinitis pigmentosa.

Companies Covered in Artificial Vital Organs and Medical Bionics Market

- SynCardia Systems, LLC

- BiVACOR Inc.

- CARMAT

- Jarvik Heart, Inc.

- Abbott

- Medtronic

- Edwards Lifesciences Corporation

- ABIOMED

- Cochlear Ltd.

- Ekso Bionics

- Berlin Heart

Frequently Asked Questions

The global artificial vital organs and medical bionics market is projected to be valued at US$ 52.4 Bn in 2026.

Rising incidence of organ failure, chronic diseases, and donor organ shortages, combined with rapid advances in medical bionics and bioengineering.

The global artificial vital organs and medical bionics market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Development and adoption of advanced, AI-enabled artificial organs and smart bionic implants to address unmet long-term care needs.

SynCardia Systems, LLC, BiVACOR Inc., CARMAT, Jarvik Heart, Inc., Abbott, and Medtronic are some of the key players in the body artificial vital organs and medical bionics market.