- Medical Devices

- Artificial Heart Lung Machine Market

Artificial Heart Lung Machine Market Size, Share, and Growth Forecast, 2025 - 2032

Artificial Heart Lung Machine Market By Component Type (Oxygenators, Pumps, Cannula, Monitoring Systems, Heat Exchanger Units, Blood Reservoir, Others), Application Type (Coronary Artery Bypass Grafting (CABG), Heart Valve Surgeries, Heart Transplant, Lung Transplant, Others), End-user Type (Hospitals, Cardiac Centers, Others), and Regional Analysis for 2025 - 2032

Artificial Heart Lung Machine Market Size and Trends Analysis

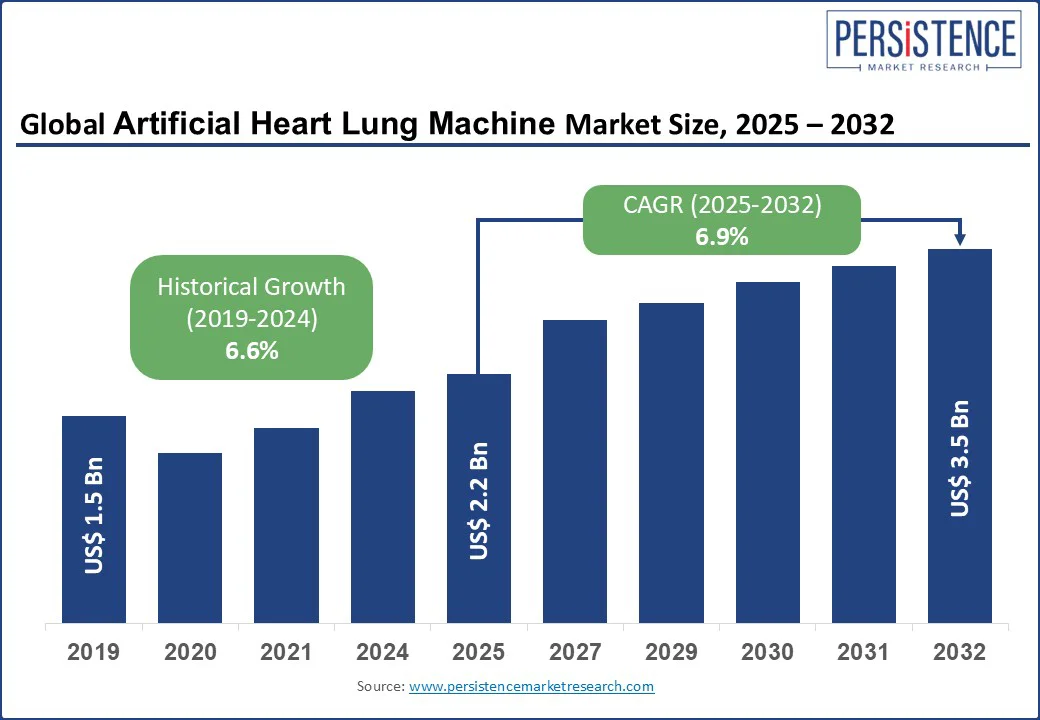

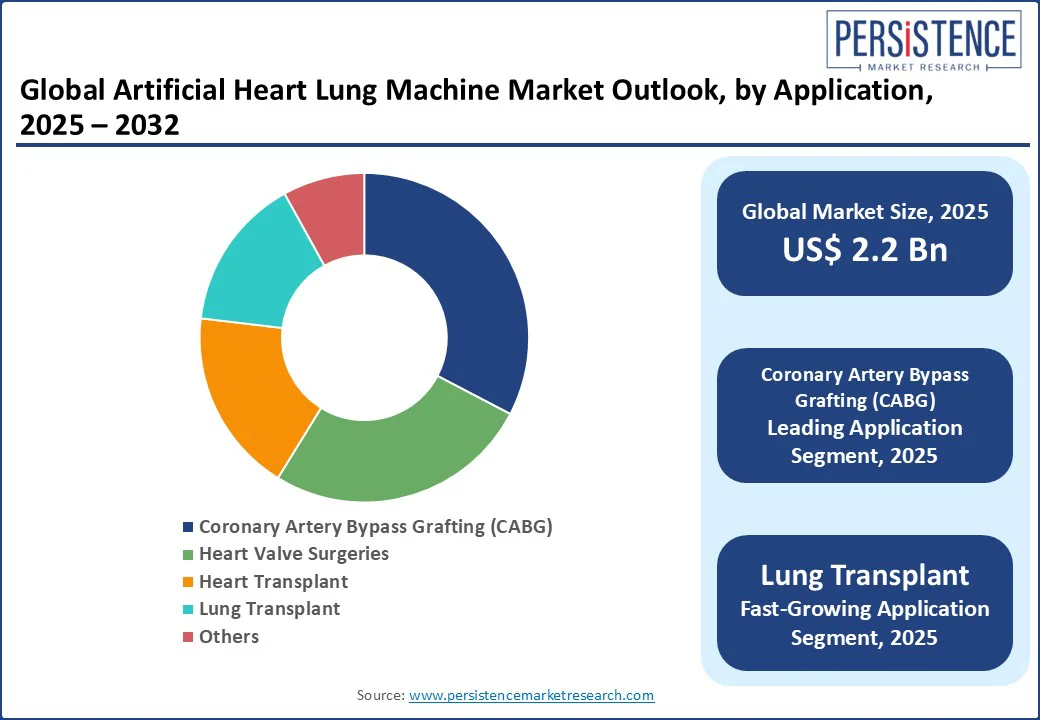

The global Artificial Heart Lung Machine Market size is likely to be valued at US$2.2 Bn in 2025 to US$3.5 Bn by 2032, registering a CAGR of 6.9% during the forecast period.

Rise in prevalence of cardiovascular and respiratory diseases, advancements in medical technology, and the rising demand for minimally invasive surgeries drives the market growth. Artificial heart-lung machines, critical for cardiopulmonary bypass during surgeries, support vital organ functions by oxygenating blood and maintaining circulation.

The Artificial Heart Lung Machine market is propelled by growing healthcare infrastructure, an aging population, and innovations in automated and portable systems, catering to hospitals and surgical centers worldwide.

Artificial Heart Lung Machine Market Highlights:

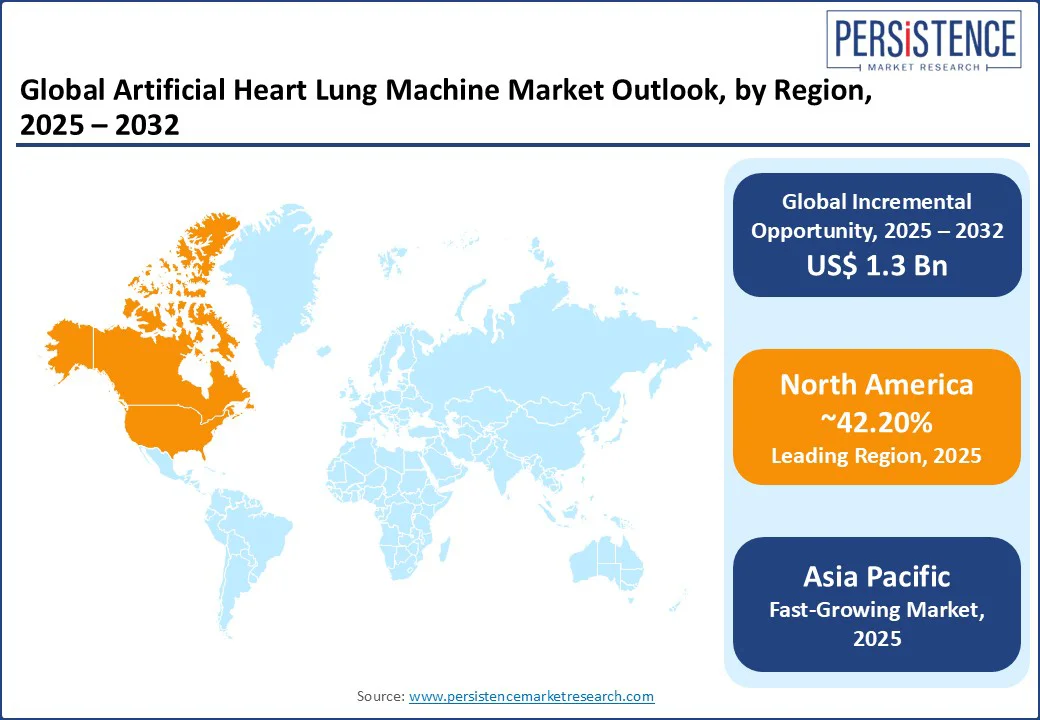

- Leading Region: North America holds a 42.20% market share in 2025, driven by advanced healthcare systems, high surgical volumes, and strong adoption of innovative technologies.

- Fastest-growing Region: Asia Pacific, fueled by rising healthcare investments, increasing cardiovascular disease prevalence, and expanding surgical facilities in countries such as China and India.

- Investment Trends: Europe is advancing with regulatory support for medical device innovation, backed by initiatives such as the EU’s Medical Device Regulation (MDR).

- Dominant Component Type: Oxygenators account for nearly 26.35% of the Artificial Heart Lung Machine market share, driven by their critical role in blood oxygenation during surgeries.

- Leading Application Type: Coronary Artery Bypass Grafting (CABG) leads with a 32.5% share, reflecting its high procedure volume globally.

|

Global Market Attribute |

Key Insights |

|

Artificial Heart Lung Machine Market (2025E) |

US$2.2 Bn |

|

Market Value Forecast (2032F) |

US$3.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.6% |

Market Dynamics

Driver - Rising Cardiovascular Diseases and Technological Advancements Push Demand

The global increase in cardiovascular and respiratory diseases is a key driver of the artificial heart lung machine market. Over 17.9 million deaths annually are attributed to cardiovascular diseases, according to the World Health Organization, with coronary artery disease and heart failure being the leading causes. The rising incidence of these conditions, particularly among aging populations, drives demand for cardiopulmonary bypass procedures. In the U.S., a growing number of CABG procedures have been performed in recent years, necessitating advanced heart–lung machines.

Technological advancements in machine design and automation are also propelling market growth. Modern systems, such as Medtronic’s Affinity Fusion oxygenator, offer improved biocompatibility and reduced blood trauma, enhancing patient outcomes. A recent study reported that automated systems reduce intraoperative complications compared to manual systems. The integration of real-time monitoring and compact designs further supports adoption in minimally invasive surgeries.

Government healthcare initiatives and increased funding for surgical infrastructure also drive market expansion. In India, national health schemes have expanded access to cardiac surgeries, increasing demand for heart–lung machines. In North America, reimbursement policies for CABG and valve surgeries incentivize hospitals to invest in advanced equipment.

Restraint - High Costs and Skilled Personnel Requirements Restrict Adoption

High costs of artificial heart–lung machines continue to hinder widespread adoption, especially in emerging markets. These machines, often equipped with advanced features such as improved oxygenation and biocompatibility, command a high upfront investment. In addition to the initial purchase price, ongoing maintenance, consumables such as oxygenators, and training requirements add to the total cost of ownership. For hospitals in resource-limited regions, such as parts of Latin America and rural India, these financial burdens are difficult to justify, even with growing demand for cardiopulmonary surgeries. As a result, access to life-saving procedures remains limited, underscoring the need for affordable, scalable solutions.

The need for skilled personnel to operate and maintain these complex machines also hinders market growth. Operating a heart-lung machine requires specialized training for perfusionists, and a 2022 survey reported a 30% shortage of certified perfusionists in Asia Pacific hospitals. This skills gap, combined with high training costs, restricts the adoption of advanced systems in developing regions.

Opportunity - Innovation in Portable Systems and Minimally Invasive Surgeries Boosts Consumption

The development of portable and compact heart–lung machines presents significant growth opportunities, particularly by enabling deployment in smaller hospitals, rural clinics, and outpatient settings. These lightweight and mobile systems address the limitations of traditional bulky devices, making them ideal for emergency care, field hospitals, and patient transport scenarios. For instance, Hemovent GmbH’s MOBYBOX, a self-contained portable ECMO system, exemplifies this shift toward mobility and flexibility in critical care. As healthcare systems increasingly prioritize decentralized and responsive cardiac support, demand for portable solutions continues to rise, especially in regions where infrastructure constraints have historically limited access to advanced cardiopulmonary technologies.

The rise of minimally invasive surgeries, such as transcatheter aortic valve replacement (TAVR), offers another growth avenue. These procedures require advanced heart lung machines with precise monitoring capabilities. A 2022 clinical study found that minimally invasive CABG using automated systems improved recovery times as compared to traditional methods, driving demand for innovative equipment.

The growing adoption of digital health platforms for remote monitoring and maintenance also enhances market potential. Companies such as LivaNova are integrating IoT-based diagnostics into their systems, allowing for proactive equipment servicing and minimizing unplanned downtime. This trend supports market expansion by addressing maintenance challenges and improving accessibility.

Category-wise Analysis

Component Type Insights

The global artificial heart lung machine market is segmented into Oxygenators, Pumps, Cannula, Monitoring Systems, Heat Exchanger Units, Blood reservoirs, and Others. Oxygenators dominate, holding approximately 26.35% share in 2025, due to their critical role in oxygenating blood during cardiopulmonary bypass. Advanced oxygenators, such as Getinge’s Quadrox-i, are widely used for their efficiency and biocompatibility.

Monitoring systems are the fastest-growing segment, driven by the increasing demand for real-time data during surgeries. Innovations in sensors and AI-integrated monitoring, such as Medtronic’s CardioLink, enhance patient safety and precision, boosting adoption in high-volume surgical centers.

Application Type Insights

By application type, the market is divided into Coronary Artery Bypass Grafting (CABG), Heart Valve Surgeries, Heart Transplant, Lung Transplant, and Others. CABG leads with a 32.5% share in 2025, driven by its high global procedure volume, with over 1 million CABG surgeries performed annually. Heart lung machines are critical for maintaining circulation during these procedures.

Lung transplant surgeries are the fastest-growing segment, fueled by rising respiratory disease prevalence and advancements in transplant techniques. The increasing success rate of lung transplants drives demand for specialized heart–lung machines in advanced surgical facilities.

End-user Type Insights

By end-user type, the market is segmented into Hospitals, Cardiac Centers, and Others. Hospitals dominate with a 70% share in 2025, driven by their high surgical volumes and advanced infrastructure. Large hospitals, particularly in North America and Europe, rely on fully automated systems for complex cardiac procedures.

Cardiac centers are the fastest-growing segment, fueled by the increasing establishment of specialized facilities for heart and lung surgeries. These centers, equipped with cutting-edge technologies, cater to the growing demand for minimally invasive and transplant procedures, boosting equipment adoption.

Regional Insights

North America Artificial Heart Lung Machine Market Trends

In North America, the U.S. dominates the global artificial heart lung machine market, expected to account for 42.20% market share in 2025, driven by high cardiovascular disease prevalence and advanced surgical infrastructure. In the U.S., demand for oxygenators and automated systems is rising, driven by increasing volumes of CABG and valve surgeries. Leading brands such as Medtronic and Getinge continue to offer innovative, efficient solutions to meet the evolving needs of cardiac surgery teams.

Consumer preferences are shifting toward compact and automated heart–lung systems, with companies such as LivaNova incorporating AI-integrated monitoring to enhance performance and safety. Patient safety remains a priority, and stringent FDA regulations encourage the adoption of biocompatible components. Additionally, favorable reimbursement policies for cardiac surgeries further incentivize hospitals and surgical centers to invest in advanced equipment, supporting the continued expansion of the artificial heart–lung machine market.

Europe Artificial Heart Lung Machine Market Trends

Europe is led by Germany, the U.K., and France, driven by regulatory support and high surgical volumes. Germany holds the largest share of the artificial heart–lung machine market, supported by strong sales from leading brands such as Terumo and Getinge. The EU’s Medical Device Regulation (MDR) fosters innovation and compliance, encouraging the adoption of advanced oxygenators and real-time monitoring systems across major healthcare facilities.

In the U.K., market growth is driven by the rising preference for minimally invasive surgeries. Products such as LivaNova’s S5 are gaining popularity for their precision and compact design. Meanwhile, France is witnessing increased demand for lung transplant-related equipment, with companies such as Braile Biomédica offering specialized cardiopulmonary solutions. Regulatory support for sustainable manufacturing practices across Europe further enhances market prospects.

Asia Pacific Artificial Heart Lung Machine Market Trends

Asia Pacific is the fastest-growing region, with a projected CAGR of 6.53% during the forecast period, led by China, India, and Japan. In India, rising cardiovascular disease prevalence (affecting 60 million adults) and government healthcare initiatives, such as Ayushman Bharat, drive demand for affordable semi-automated systems. Companies such as Tianjin Welcome Medical dominate with cost-effective solutions.

China leads in terms of large-scale hospital expansions, with brands such as MERA leading in fully automated systems. Japan focuses on high-precision equipment for heart transplants, with Technowood International gaining traction. The region’s growing healthcare investments and digital procurement platforms further accelerate market growth.

Competitive Landscape

The global artificial heart lung machine market is highly competitive, with industry players competing on innovation, pricing, and reliability. The rise of portable and automated systems intensifies competition, as companies aim to meet stringent safety standards and surgical demands. Strategic partnerships and regulatory approvals are key differentiators.

Key Developments:

- In July 2025, Medtronic’s VitalFlow ECMO system received CE Mark approval in Europe, marking its official launch and signaling its availability for intensive care use across the region. This fully integrated ECMO solution emphasizes simplicity and adaptability to modern ICU needs.

- In May 2024, Hemovent GmbH’s portable ECMO device, the MOBYBOX, continues to gain traction in Europe. Designed to be compact and lightweight so much so that it fits into a backpack this self-contained ECLS system is expanding into commercial use, dramatically enhancing portable cardiopulmonary support in emergency and transport scenarios.

Companies Covered in Artificial Heart Lung Machine Market

- Medtronic

- Terumo Europe NV

- LivaNova, Inc.

- Getinge

- Braile Biomédica

- NIPRO

- Tianjin Welcome Medical Equipment Co., Ltd.

- ELITE LIFECARE

- Hemovent GmbH

- MERA (Senko Medical Instrument Mfg. Co., Ltd.)

- Technowood International Pte. Ltd.

- Others

Frequently Asked Questions

The Artificial Heart Lung Machine market is projected to reach US$2.2 Bn in 2025.

Rising cardiovascular diseases, technological advancements, and government healthcare initiatives are the key market drivers.

The Artificial Heart Lung Machine market is poised to witness a CAGR of 6.9% from 2025 to 2032.

Innovation in portable systems and minimally invasive surgeries is the key market opportunity.

Medtronic, Terumo Europe NV, and LivaNova, Inc. are among the key market players.