- Pharmaceuticals

- Antibody-mediated Rejection Prevention Market

Antibody-mediated Rejection Prevention Market Size, Share, and Growth Forecast, 2026 - 2033

Antibody-mediated Rejection Prevention Market by Product Type (Monoclonal Antibodies, Others), Application (Kidney Transplants, Heart Transplants, Others), End-user (Hospitals & Transplant Centers, Others), and Regional Analysis for 2026 – 2033

Antibody-mediated Rejection Prevention Market Size and Trends Analysis

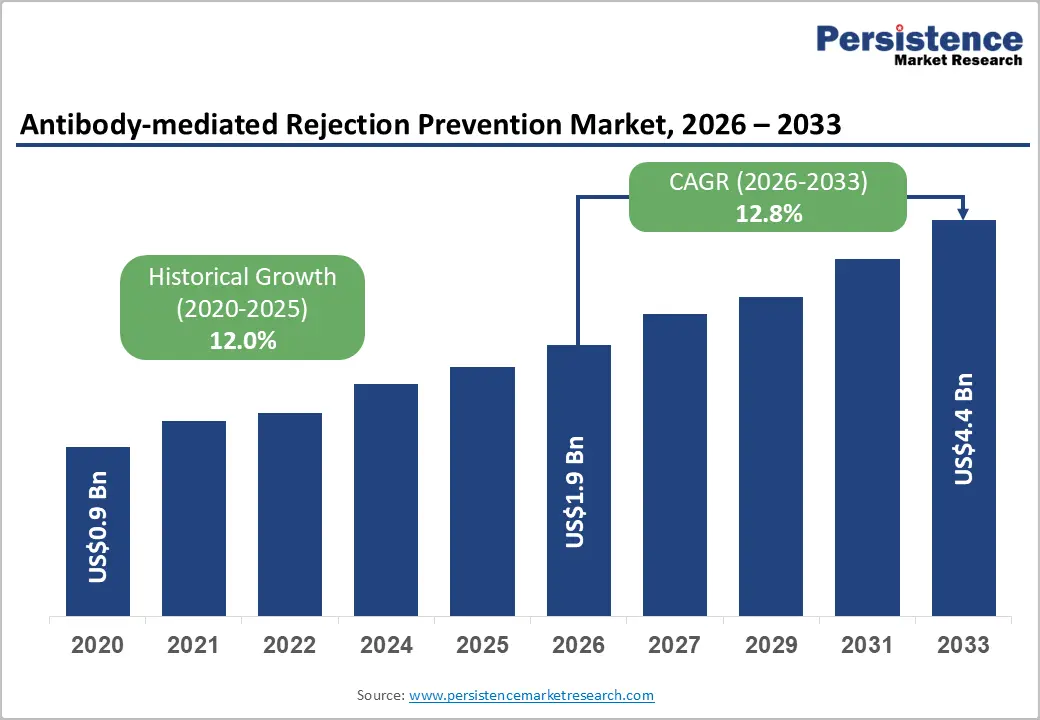

The global antibody-mediated rejection prevention market size is likely to be valued at US$1.9 billion in 2026, and is expected to reach US$4.4 billion by 2033, growing at a CAGR of 12.8% during the forecast period from 2026 to 2033, driven by the increasing number of solid organ transplants worldwide, rising incidence of antibody-mediated rejection (AMR) due to sensitization and donor-specific antibodies (DSA), growing adoption of desensitization protocols and novel biologics to improve graft survival, and expanding clinical research into complement inhibitors and B-cell targeted therapies.

Increasing recognition of antibody-mediated rejection prevention as critical for long-term transplant success, reduced chronic allograft dysfunction, and improved patient quality of life in emerging transplant immunology markets remains a major driver of market growth.

Key Industry Highlights:

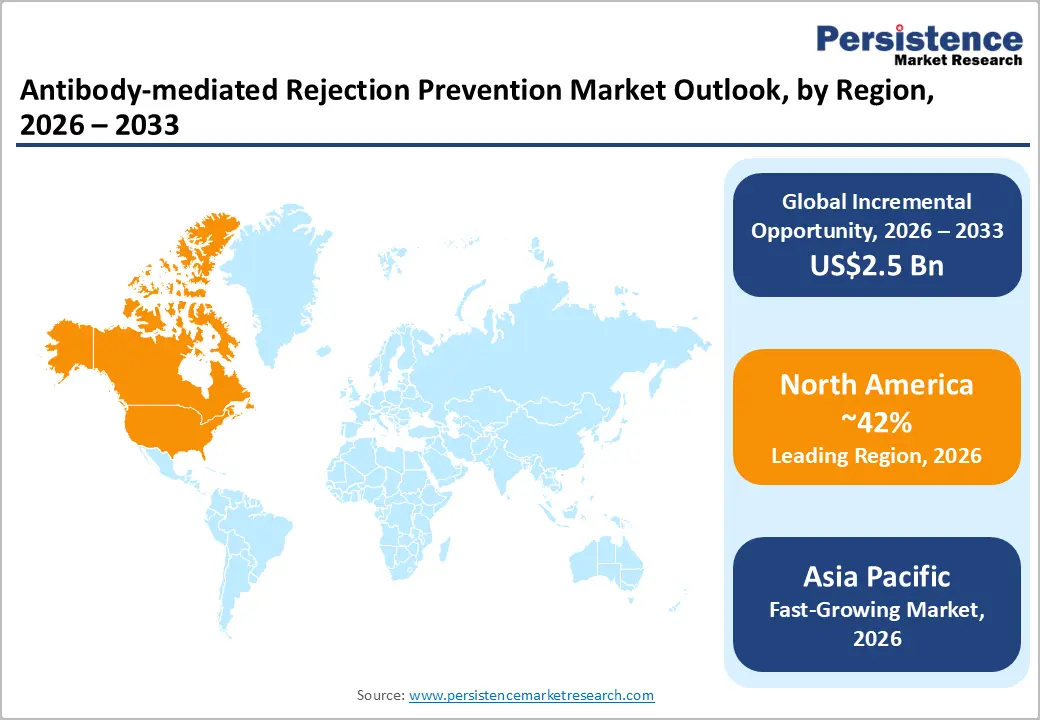

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by the highest transplant volumes, advanced desensitization programs, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rapidly increasing transplant activity, growing sensitization awareness, and expanding specialized transplant centers in India and China.

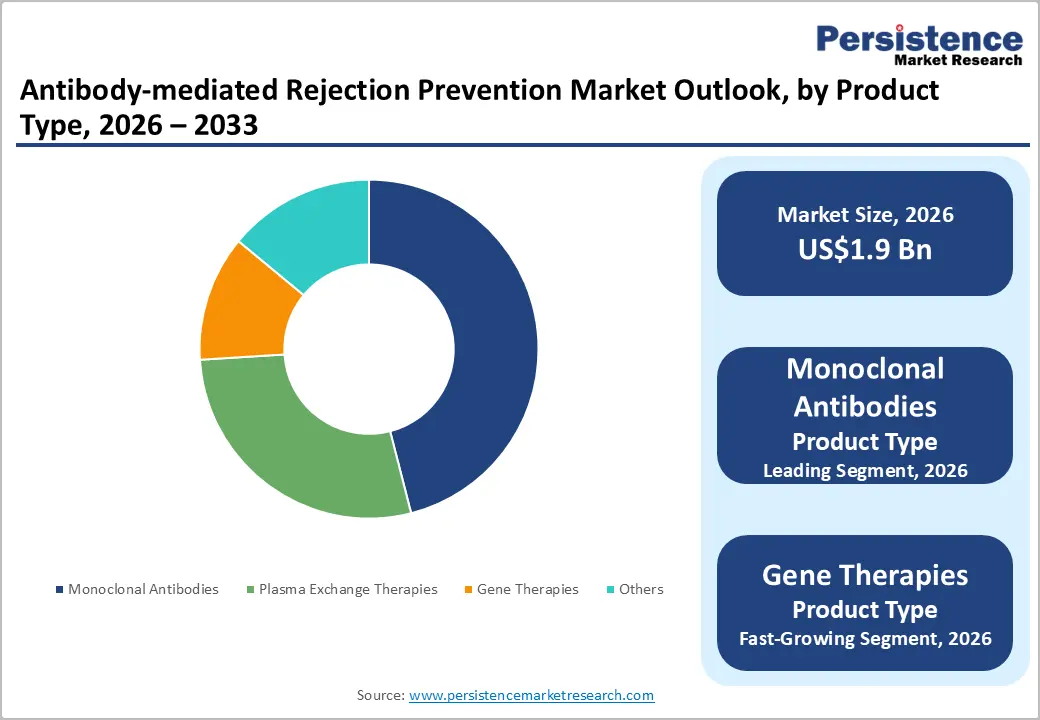

- Dominant Product Type: Monoclonal antibodies, to hold approximately 52% of the market share, as they remain the cornerstone of AMR prevention and desensitization.

- Leading Application: Kidney transplants, to contribute nearly 65% of the market revenue, due to the highest transplant frequency and AMR risks.

| Key Insights | Details |

|---|---|

|

Antibody-mediated Rejection Prevention Market Size (2026E) |

US$1.9 Bn |

|

Market Value Forecast (2033F) |

US$4.4 Bn |

|

Projected Growth CAGR (2026-2033) |

12.8% |

|

Historical Market Growth (2020-2025) |

12.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Transplant Volumes and Sensitization Challenges

The growing number of organ transplants worldwide is increasing the complexity of patient matching and post-transplant care. As more patients undergo kidney, heart, liver, and lung transplantation, the likelihood of individuals becoming immunologically sensitized also rises. Sensitization occurs when a patient develops antibodies against human leukocyte antigens (HLA), often due to previous transplants, blood transfusions, or pregnancy. These antibodies can make it more difficult to find compatible donors and increase the risk of transplant rejection.

Highly sensitized patients typically require more extensive compatibility testing and careful donor selection to ensure successful outcomes. Advanced immunological screening techniques, including antibody identification and crossmatch testing, are therefore becoming essential components of transplant evaluation protocols. Healthcare providers and transplant centers are increasingly adopting sophisticated diagnostic tools to identify donor-specific antibodies and assess immunological risk before surgery. Transplant waiting lists continue to expand as the number of patients with end-stage organ failure grows. This trend places greater pressure on healthcare systems to optimize donor matching processes and improve graft survival rates. Laboratories and transplant programs are focusing on enhanced immunological monitoring both before and after transplantation.

Growth Analysis – Novel Biologics and Gene Therapy Pipeline Momentum

The rapid expansion of advanced therapeutic pipelines is significantly influencing the development of biologics and gene-based treatments. Pharmaceutical and biotechnology companies are increasingly focusing on therapies that target diseases at the genetic or molecular level, particularly for rare genetic disorders, cancers, and previously untreatable conditions. Unlike conventional drugs that manage symptoms, biologics and gene therapies aim to correct or modify the underlying biological mechanisms of disease, which can lead to longer-lasting or even curative outcomes.

Advances in technologies such as viral vectors, gene editing platforms, and cell engineering have improved the feasibility and safety of these treatments. Research institutions and biotechnology firms are investing heavily in preclinical and clinical programs to explore therapies that deliver functional genes, repair defective DNA, or stimulate the body’s immune response. For example, companies such as Novartis and Bluebird Bio have developed gene therapies targeting inherited blood disorders, demonstrating how pipeline innovation is translating into approved therapies. Regulatory agencies are introducing accelerated approval pathways and supportive frameworks to encourage the development of breakthrough treatments for rare and life-threatening diseases.

Barrier Analysis – Technical Challenges in Gene Delivery

Delivering therapeutic genes accurately to the intended cells remains a major scientific and technological hurdle. Gene therapies typically rely on delivery vehicles such as viral vectors or non-viral systems to transport genetic material into target cells. However, achieving efficient delivery without triggering immune responses or damaging healthy tissues is complex. Some viral vectors may provoke immune reactions that reduce treatment effectiveness or prevent repeat dosing. In addition, certain tissues, such as the brain, lungs, or muscles, are difficult to reach due to biological barriers that limit the penetration of gene delivery systems.

The challenge involves ensuring that the inserted gene functions correctly and maintains stable expression over time. If the genetic material fails to integrate or remain active within the target cells, the therapeutic benefit may diminish. Researchers and biotechnology companies are continuously developing improved vectors and delivery platforms to enhance targeting accuracy, safety, and durability of gene therapies. For example, organizations such as Sarepta Therapeutics and Spark Therapeutics are actively working on advanced gene delivery technologies to address these limitations.

Barrier Analysis – Complex Patient Selection and Risk of Over-Immunosuppression

Careful patient evaluation is essential before initiating advanced biologic or gene-based therapies because these treatments often involve modifying immune responses or introducing genetic material into the body. Not every patient responds in the same way, and factors such as disease severity, genetic profile, immune status, and prior treatment history must be assessed to determine eligibility. In many cases, clinicians need to perform detailed diagnostic tests, biomarker analysis, and genetic screening to identify suitable candidates, which can increase the complexity and time required for treatment decisions.

An important concern is the potential for excessive immune suppression. Some biologic therapies reduce immune activity to control disease progression, but if the immune system becomes too suppressed, patients may become more vulnerable to infections or other complications. Managing the balance between therapeutic effectiveness and immune safety requires close monitoring by healthcare professionals.

Opportunity Analysis – Growth in Complement Inhibitors and Gene Therapies

Advances in targeted biologic therapies and genetic medicine are accelerating the development of treatments that address diseases linked to immune system dysfunction and genetic abnormalities. Complement inhibitors have emerged as an important therapeutic class designed to block specific components of the complement system, a part of the immune response that can become overactive in certain rare and autoimmune disorders. By selectively inhibiting complement proteins, these therapies help prevent inflammation and tissue damage while improving disease control for patients with conditions such as paroxysmal nocturnal hemoglobinuria and atypical hemolytic uremic syndrome. Pharmaceutical companies such as Alexion Pharmaceuticals, a subsidiary of AstraZeneca, have played a major role in advancing complement-targeted treatments through therapies designed to block complement protein C5.

Gene therapies are gaining momentum as innovative approaches that address the underlying genetic causes of diseases rather than only managing symptoms. These therapies introduce functional genes or modify defective genetic material to restore normal cellular function. Progress in viral vector design, gene editing technologies, and improved delivery systems has strengthened the development pipeline. Biotechnology firms such as Sarepta Therapeutics are actively developing gene therapies for inherited disorders, highlighting the growing role of genetic medicine in transforming treatment strategies and expanding therapeutic possibilities for previously difficult-to-treat diseases.

Expansion in Transplant Markets

Growth in organ and tissue transplantation procedures worldwide is creating new opportunities for advanced biologic and gene-based therapies. As the number of patients requiring kidney, liver, heart, and lung transplants continues to rise due to chronic diseases and aging populations, the demand for therapies that improve transplant success and long-term graft survival is increasing. Biologic drugs and cell-based therapies are being explored to regulate immune responses, reduce organ rejection, and improve compatibility between donors and recipients.

Innovations in immunomodulatory biologics allow physicians to control the body’s immune reaction more precisely after transplantation. These therapies can help prevent acute and chronic rejection while minimizing the side effects commonly associated with traditional immunosuppressive drugs. In addition, gene-based approaches are being investigated to modify donor organs or patient immune cells to enhance tolerance and reduce immune-mediated damage. Leading biotechnology and pharmaceutical companies such as Novartis and Roche are involved in developing biologic therapies that support transplant patients by targeting immune pathways associated with rejection. Continuous research in cell therapy, gene editing, and precision medicine is further strengthening the transplant treatment landscape.

Category-wise Analysis

Product Type Insights

Monoclonal antibodies are anticipated to dominate the market, accounting for 52% of the market share in 2026, driven by their high specificity and effectiveness in targeting disease-related molecules. These therapies are designed to bind to specific antigens, allowing precise treatment of conditions such as cancer, autoimmune disorders, and infectious diseases while minimizing damage to healthy cells. Their strong clinical success, wide therapeutic applications, and continuous product approvals contribute significantly to their market share. Ongoing advancements in antibody engineering and biologic manufacturing technologies have improved treatment efficacy and safety. Keytruda (pembrolizumab), a monoclonal antibody developed by Merck & Co., is an immune checkpoint inhibitor that targets the PD-1 receptor on T cells, helping the immune system recognize and attack cancer cells. It is widely used to treat multiple cancers, including melanoma, non-small cell lung cancer, head and neck cancer, and bladder cancer.

Gene therapies represent the fastest-growing product type, as they offer the potential to treat diseases at their genetic root rather than only managing symptoms. These therapies work by replacing, modifying, or repairing defective genes responsible for certain disorders. Advances in viral vector technology, gene editing tools, and precision medicine have improved the safety and effectiveness of these treatments, encouraging increased research and clinical development. Zolgensma, a gene therapy developed by Novartis for treating spinal muscular atrophy (SMA), a rare genetic neuromuscular disorder. Zolgensma works by delivering a functional copy of the SMN1 gene into a patient’s cells using an adeno-associated viral (AAV) vector. This therapy targets the underlying genetic cause of the disease rather than only managing symptoms.

Application Insights

Kidney transplants are expected to dominate the market, contributing nearly 65% of revenue in 2026, fueled by the high global prevalence of end-stage renal disease (ESRD) and the increasing number of patients requiring long-term renal replacement therapy. Compared with other organ transplants, kidney transplantation is performed more frequently because chronic kidney disease is widely associated with conditions such as diabetes and hypertension. In addition, kidney transplant procedures generally have well-established surgical techniques, higher success rates, and improved patient survival compared with long-term dialysis. Prograf (tacrolimus) is an immunosuppressive drug developed by Astellas Pharma. Prograf is widely used in kidney transplant patients to prevent organ rejection by suppressing the immune system’s response to the transplanted kidney. It is one of the most commonly prescribed maintenance immunosuppressants after kidney transplantation and plays a critical role in improving graft survival and long-term transplant success.

Heart transplants represent the fastest-growing application, propelled by the rising incidence of advanced heart failure and the increasing need for life-saving treatment options when conventional therapies become ineffective. Improvements in surgical techniques, donor organ preservation, and post-transplant care have significantly enhanced survival rates and long-term outcomes for patients. Advancements in immunosuppressive biologics and personalized treatment strategies help reduce the risk of organ rejection and complications after transplantation. Simulect is a monoclonal antibody developed by Novartis. Simulect (basiliximab) is used as an induction immunosuppressive therapy during organ transplantation, including heart transplants, to prevent the body’s immune system from rejecting the transplanted organ. It works by blocking the interleukin-2 receptor on activated T-lymphocytes, which reduces immune activation that could damage the new heart.

Regional Insights

North America Antibody-mediated Rejection Prevention Market Trends

North America is projected to dominate account for nearly 42% of the revenue in 2026, driven by advances in transplant immunology and the increasing focus on improving long-term graft survival. One major trend is the growing adoption of targeted immunotherapies and biologic drugs that specifically suppress immune pathways responsible for antibody-mediated damage to transplanted organs. Therapies that inhibit B-cells, plasma cells, or complement activation are increasingly incorporated into transplant protocols to reduce the risk of rejection while maintaining immune balance.

The expansion of advanced diagnostic and immune-monitoring technologies. Transplant centers across the U.S. and Canada are increasingly using donor-specific antibody (DSA) testing, molecular diagnostics, and immune profiling to identify patients at high risk of rejection before clinical symptoms appear. Early detection enables clinicians to implement preventive interventions such as adjusted immunosuppressive regimens or desensitization therapies, improving graft survival outcomes. The region is seeing increased clinical research and innovation in transplant immunology.

Europe Antibody-mediated Rejection Prevention Market Trends

Europe is witnessing a steady growth of strong research collaboration, advanced transplant programs, and increasing adoption of precision medicine in transplant care. One of the key trends in the region is the growing emphasis on personalized immunosuppressive therapy. European transplant centers increasingly tailor immunosuppressive regimens based on patient-specific immune risk factors, such as donor-specific antibodies (DSA) and human leukocyte antigen (HLA) compatibility. This approach helps clinicians identify patients at higher risk of rejection and implement preventive interventions early, improving graft survival rates.

Expansion of collaborative research and clinical trials across European transplant institutions. Countries such as Germany, France, and the U.K. host leading transplant centers and academic institutions that actively study innovative therapies targeting immune pathways involved in AMR. These collaborations support the development of new biologics, monoclonal antibodies, and targeted therapies aimed at reducing antibody production and protecting transplanted organs. Europe is witnessing increased adoption of advanced immune-monitoring and diagnostic technologies. Regular screening for donor-specific antibodies and improved donor-recipient matching strategies are increasingly integrated into transplant protocols. These diagnostic tools enable earlier detection of immune activity against transplanted organs, allowing physicians to adjust preventive treatments before severe rejection occurs.

Asia Pacific Antibody-mediated Rejection Prevention Market Trends

Asia Pacific is likely to be the fastest-growing market for antibody-mediated rejection prevention, with expanding organ transplant programs, improving healthcare infrastructure, and increasing awareness of transplant immunology. One major trend in the region is the rapid rise in organ transplantation procedures, particularly in countries such as China, Japan, South Korea, India, and Australia. Regional transplant networks report thousands of transplant procedures performed annually across hundreds of transplant centers, reflecting a growing patient population requiring effective rejection-prevention therapies.

The increasing adoption of advanced immunological monitoring techniques, including donor-specific antibody (DSA) testing and molecular diagnostics. These technologies help clinicians detect immune responses against transplanted organs at an early stage, allowing physicians to adjust immunosuppressive therapy and prevent antibody-mediated rejection. Monitoring DSA levels is considered essential because persistent antibodies significantly increase the risk of graft rejection and reduced transplant survival. The region is also witnessing greater use of desensitization therapies and combination immunosuppressive treatments to manage highly sensitized transplant recipients. Hospitals increasingly use strategies such as plasmapheresis, intravenous immunoglobulin (IVIG), and targeted antibody therapies to reduce antibody levels before and after transplantation, improving graft acceptance.

Competitive Landscape

The global antibody-mediated rejection prevention market is characterized by competition between established biopharmaceutical companies and emerging biotechnology firms focused on transplant immunology. Companies such as CSL Behring and Hansa Biopharma play a leading role in North America and Europe due to their strong clinical research capabilities, established transplant-center collaborations, and advanced therapeutic pipelines. These firms focus on therapies designed to reduce donor-specific antibodies (DSA) and modulate immune responses that can damage transplanted organs. Their development programs increasingly emphasize targeted biologics, including monoclonal antibodies and complement-pathway inhibitors, which help prevent antibody-mediated rejection and improve long-term graft survival.

In the Asia Pacific region, regional pharmaceutical manufacturers are strengthening their presence by introducing cost-competitive biologics and biosimilars that improve patient access to advanced immunosuppressive therapies. Companies across all regions are actively pursuing strategic partnerships with transplant centers, academic institutions, and biotechnology startups. These collaborations support clinical trials, expand therapeutic indications, and accelerate regulatory approvals for next-generation therapies aimed at improving transplant outcomes.

Key Industry Developments:

- In December 2025, Hansa Biopharma AB submitted a Biologics License Application (BLA) to the U.S. Food and Drug Administration, requesting priority review for imlifidase as a treatment for the desensitization of highly sensitized adult patients undergoing deceased donor kidney transplantation. The company filed the application to support the use of imlifidase in reducing donor-specific antibodies before transplantation, which can help improve transplant eligibility and reduce the risk of antibody-mediated rejection in kidney transplant recipients.

- In October 2024, Biogen Inc. announced that felzartamab, an investigational anti-CD38 monoclonal antibody, received Breakthrough Therapy Designation (BTD) from the U.S. Food and Drug Administration for the treatment of late antibody-mediated rejection (AMR) without T-cell-mediated rejection in kidney transplant patients. The designation recognized felzartamab’s potential to provide significant improvement over existing therapies for this serious transplant complication, based on preliminary clinical evidence demonstrating its therapeutic benefit.

Companies Covered in Antibody-mediated Rejection Prevention Market

- CSL Behring

- Hansa Biopharma

- Sanofi

- Talaris Therapeutics

- Horizon Therapeutics

- Novartis AG

- Biogen

- Teva Pharmaceutical Industries Ltd.

- Eli Lilly and Company

- Bristol-Myers Squibb Company.

Frequently Asked Questions

The global antibody-mediated rejection prevention market is projected to reach US$1.9 billion in 2026.

Rising transplant volumes and increasing sensitization challenges are key drivers of the antibody-mediated rejection prevention market.

The antibody-mediated rejection prevention market is poised to witness a CAGR of 12.8% from 2026 to 2033.

Complement inhibitors, gene therapies, and expansion in Asia Pacific and emerging transplant markets are the key opportunities.

CSL Behring, Hansa Biopharma, Sanofi, Talaris Therapeutics, and Novartis AG are the key players.