- Medical Devices

- AI in Medical Imaging Market

AI in Medical Imaging Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

AI in Medical Imaging Market by Product (Hardware, Software Tools/ Platform, Services), Indication (Oncology, Cardiovascular, Digital Pathology, Neurology, Oral Diagnostics, Others), Modality (Computed Tomography, Magnetic Resonance Imaging, X-Ray, Molecular Imaging, Ultrasound Imaging, Others), End User (Hospitals and Clinics, Research Laboratories, Diagnostic Centers, Others), and Regional Analysis from 2026 to 2033

AI in Medical Imaging Market Size and Trend Analysis

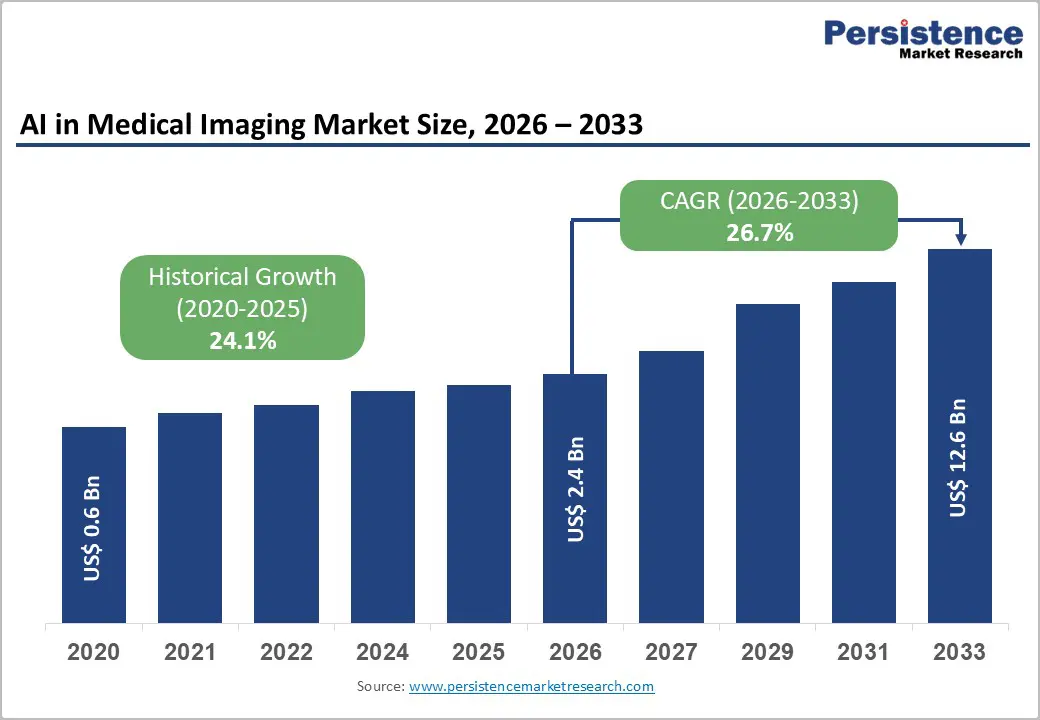

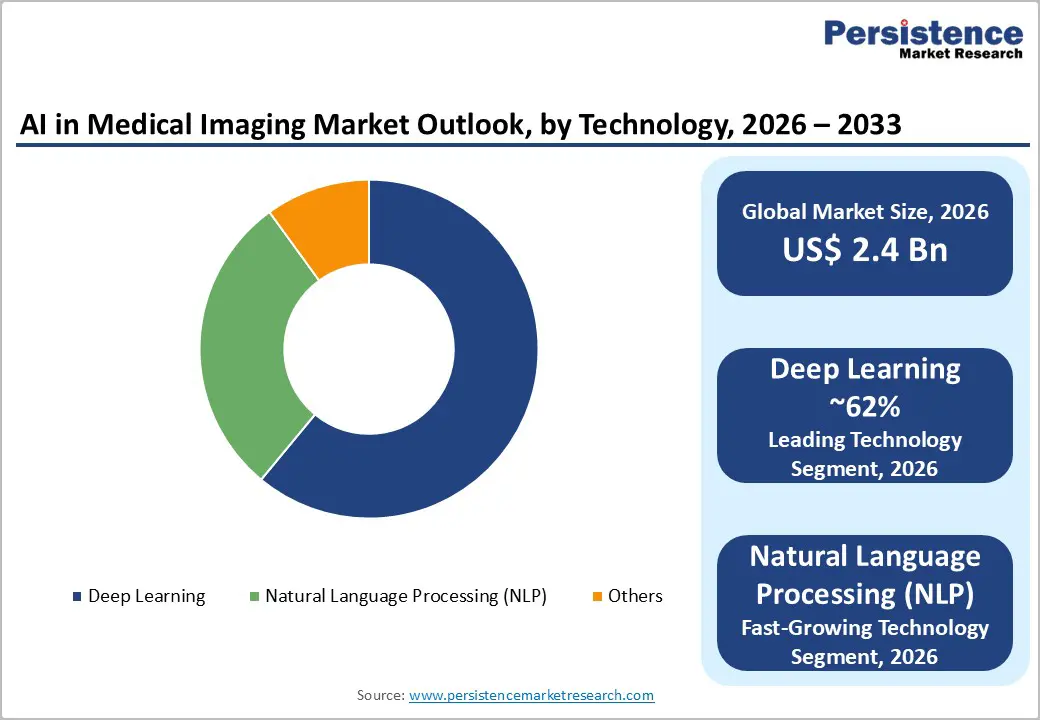

The global AI in medical imaging market is estimated to grow from US$ 2.4 Bn in 2026 to US$ 12.6 Bn by 2033. The market is projected to grow at a CAGR of 26.7% from 2026 to 2033.

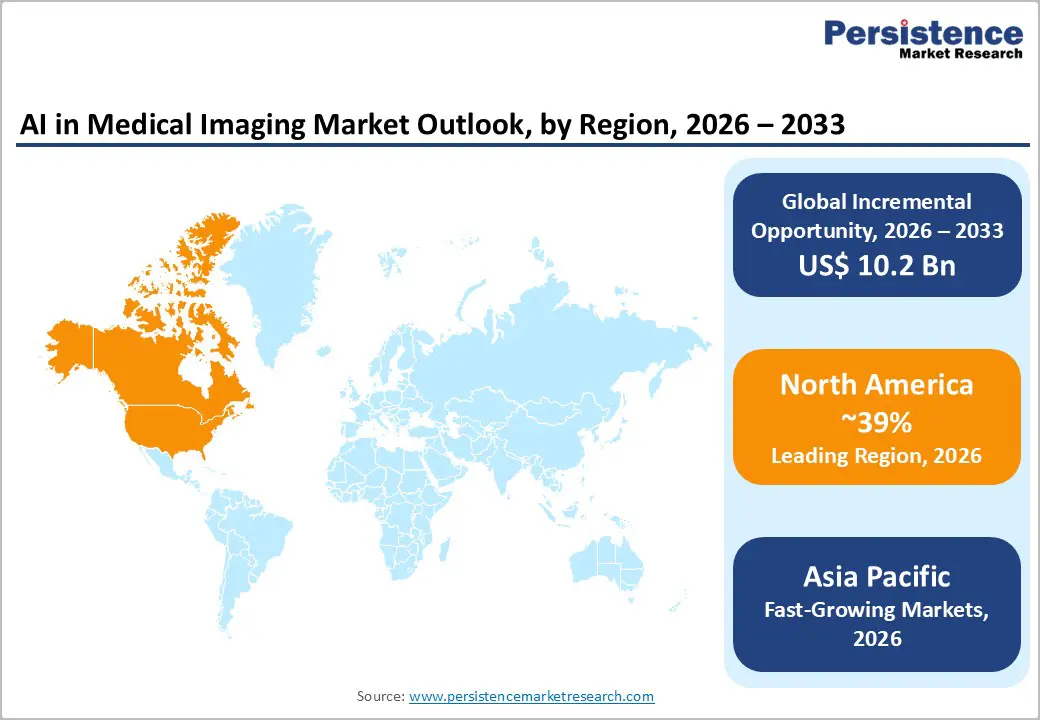

The global AI in medical imaging market is growing steadily, fueled by demand for precise diagnostics, targeted therapies, and advancements in biologic drug development. North America leads with robust healthcare infrastructure, regulatory support, and advanced manufacturing, while Asia-Pacific grows fastest due to improving healthcare systems, government initiatives, rising patient awareness, and increased investment in digital imaging and biologics

Key Industry Highlights

- Dominant Segment: Software and AI platforms lead the AI in Medical Imaging Market with 56.7% share in 2025, driven by their ability to enhance diagnostic accuracy, streamline workflows, and integrate with imaging devices across radiology, oncology, cardiology, and ophthalmology. These solutions improve clinical decision-making and efficiency, making them essential in modern healthcare diagnostics.

- Dominant Region: North America leads due to advanced healthcare infrastructure, early AI adoption, strong regulatory frameworks, and the presence of major technology providers. Asia-Pacific is the fastest-growing region, supported by improving healthcare systems, rising patient awareness, government initiatives, and increased adoption of AI-driven imaging solutions.

- Market Drivers: Growth is fueled by the rising prevalence of chronic diseases, increasing imaging demand, the adoption of AI-assisted diagnostics, technological advancements in imaging software, and supportive reimbursement policies.

- Market Opportunity: Key opportunities include AI in oncology and cardiology imaging, cloud-based platforms, integration with electronic health records, market penetration in emerging markets, and the development of AI solutions for underserved clinical indications.

| Global Market Attributes | Key Insights |

|---|---|

| AI in Medical Imaging Market Size (2026E) | US$ 2.4 Bn |

| Market Value Forecast (2033F) | US$ 12.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 26.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 24.1% |

Market Dynamics

Driver: Increasing adoption of AI-assisted diagnostic tools in hospitals and clinics

The adoption of AI-assisted diagnostic tools in healthcare settings has been rapidly accelerating as hospitals and clinics seek to improve diagnostic accuracy and efficiency. According to recent industry data, 67% of hospitals now use AI specifically for diagnostic imaging applications, making it one of the most widely deployed clinical AI use cases globally. Radiology departments report among the highest integration rates, with approximately 81% adoption of AI in radiology workflows, compared with other specialties. AI tools in imaging are already showing tangible benefits, helping reduce interpretation time and improve diagnostic consistency, which is critical in high-volume imaging environments.

In the United States, physician-level adoption of AI has surged, with 66% of physicians using AI tools in clinical practice by 2024, representing a 78% increase from the prior year. This includes the use of AI to assist with image interpretation as well as workflow optimization and decision support. Despite variations in adoption across regions and facility types, the trend indicates rapid integration: the global market for AI imaging tools is expanding in line with increased digital transformation in healthcare, with nearly half of hospitals worldwide expected to adopt AI technologies by 2025.

Restraints: High implementation and integration costs of AI imaging systems

One of the key restraints on the broader adoption of AI in medical imaging is the high cost of implementing, integrating, and operating these systems, particularly for smaller clinics and imaging centers. Industry insights indicate that a comprehensive AI imaging solution typically incurs a capital cost of approximately $250,000 to $500,000 per system for initial deployment. Annual maintenance fees can add 15–20% to the original investment, further increasing the total cost of ownership and reducing the financial incentives for smaller healthcare facilities to adopt such technology.

Beyond purchase price, there are substantial expenditures tied to necessary infrastructure upgrades, including high-speed data networks, secure storage systems, and cybersecurity measures, as well as integration with existing hospital information systems like PACS (Picture Archiving and Communication Systems) and EHRs (Electronic Health Records). Regulatory validation and clinical trials, which are often required before AI diagnostic software can be deployed, also contribute to extended development costs. In aggregate, these financial and technical barriers can slow down adoption, especially in resource-constrained settings where budgets and technical expertise are limited, limiting the penetration of AI imaging solutions despite their clinical promise.

Opportunity: Development of AI solutions for oncology, cardiology, and neurology imaging

The development of AI-driven imaging solutions targeted at specialty areas such as oncology, cardiology, and neurology presents a significant market opportunity within the AI in medical imaging sector. These clinical domains involve complex imaging modalities, such as PET/CT for cancer staging, MRI for neurological disorders, and echocardiography for heart disease, where AI can enhance detection, quantification, and interpretation beyond human capability. Recent market reports show that AI-powered imaging devices improve early cancer detection and neurological disorder diagnosis by approximately 25% compared to traditional approaches, indicating measurable clinical impact in specialty imaging.

Investment in these areas is growing as healthcare systems emphasize precision diagnostics and personalized treatment planning. For example, oncology imaging is a field where thousands of subtle radiomic features need to be analyzed on high-resolution scans, a task that AI algorithms can perform with greater consistency and speed than manual review. Similarly, cardiology imaging benefits from algorithms that enhance the detection of subtle functional abnormalities. Neurology, with its reliance on complex, multi-sequence MRI scans, is another area where AI can reduce interpretation time and increase diagnostic confidence, especially for conditions like stroke, Alzheimer’s disease, and multiple sclerosis. Market forecasts position these specialty applications as high-growth segments as developers refine AI models for disease-specific tasks and clinicians increasingly adopt tailored solutions for high-value imaging needs.

Category-wise Analysis

By Product, Software Tools/ Platform Dominates the AI in Medical Imaging Market

Software Tools/ Platform occupies 56.7% share of the global market in 2025, because they are the primary drivers of AI functionality, enabling algorithm-based interpretation, workflow automation, and integration with hospital systems like PACS and EHRs.

For example, as of 2024 the U.S. FDA has cleared over 950 AI/ML-enabled medical devices, most of which are software-centric diagnostic tools for radiology and imaging interpretation, rather than hardware machines. Software platforms scale across modalities (MRI, CT, X-ray) without requiring physical upgrades and support cloud deployments that enhance accessibility and enable updates. These platforms leverage deep learning algorithms to enhance image clarity, automate anomaly detection, and reduce diagnostic turnaround time, which hospitals and diagnostic centers increasingly prioritize for efficiency and accuracy in patient care.

By Indication, Neurology dominates due to high disease burden and AI-enhanced brain imaging accuracy

The neurology segment leads by indication because neurological imaging poses complex diagnostic challenges that benefit significantly from AI interpretation. AI systems excel at extracting subtle patterns in brain MRI and CT scans that may be difficult for human readers to detect, improving early diagnosis of conditions like Alzheimer’s, stroke, and brain tumors. Globally, neurological disorders affect billions. A major analysis published in The Lancet Neurology estimated that approximately 3.4 billion people experienced nervous system conditions in 2021, driving demand for advanced diagnostic tools.

AI’s ability to automate segmentation, quantify structural change, and prioritize critical cases accelerates clinical decision-making. This combination of high disease burden and diagnostic complexity explains why neurology accounts for the largest share of AI imaging applications.

Regional Insights

North America AI in Medical Imaging Market Trends

North America dominates the AI in medical imaging market because of advanced digital healthcare infrastructure, regulatory support, and high adoption rates of AI technologies. The region accounted for 42.1% of the global market share in 2025, led by the United States and Canada, driven by hospitals and imaging centers integrating AI to streamline radiology workflows and improve diagnostic accuracy. More than 52% of radiologists in the U.S. use AI tools in daily practice for tasks such as cancer and cardiovascular detection, reflecting widespread clinical use.

North America also benefits from substantial R&D investments and supportive reimbursement environments, which enable faster commercialization of AI imaging solutions and solidify its leadership position in the global market.

Europe AI in Medical Imaging Market Trends

Europe is a strategically important region in the AI in medical imaging market due to its robust public healthcare systems, clean regulatory environment, and strong cross-country digital health collaboration. Countries such as Germany, the UK, and France are increasingly integrating AI tools into clinical diagnostics to improve care quality and address shortages in the radiologist workforce. A significant share of hospitals participating in national e-health programs have adopted AI-enabled imaging solutions, indicating broad institutional uptake.

European regulatory frameworks, including CE certification and evolving AI governance rules, emphasize safety, transparency, and clinical validation, which strengthens clinician trust. Continued public investment in AI research, education, and hospital digitization further supports sustained adoption and innovation.

Asia-Pacific AI in Medical Imaging Market Trends

The Asia-Pacific region is the fastest-growing market for AI in medical imaging, driven by rapid healthcare digitization, rising disease burden, and increasing investment in AI technologies. Countries such as China, India, Japan, and South Korea are actively adopting AI tools to manage growing imaging volumes and radiologist shortages. In China, a large share of top-tier hospitals have deployed AI-based imaging platforms, while in India, adoption has accelerated significantly through national digital health and interoperability initiatives.

Strong government support, including digital health missions and AI-focused healthcare policies, is accelerating deployment. At the same time, the increasing prevalence of chronic diseases and expanding healthcare infrastructure continue to drive strong demand for AI-enabled imaging solutions.

Market Competitive Landscape

The competitive landscape of the AI in medical imaging market is led by established tech and medical imaging firms, with intense innovation in deep learning algorithms, strategic partnerships, and acquisitions. Key players compete on software performance, integration capabilities, and clinical validation to capture market share in radiology, oncology, cardiology, and neurology imaging.

Key Industry Developments:

- In January 2026, AGFA HealthCare showcased its latest imaging innovations at ECR 2026, positioning itself as a true empowerer of diagnostic excellence. The company highlighted advanced enterprise imaging platforms, AI-enabled workflow solutions, and cloud-based technologies designed to improve clinical efficiency and diagnostic confidence.

- In November 2025, Enlitic announced a global partnership with Philips to advance the adoption of AI-driven medical imaging solutions across healthcare systems. The collaboration focused on integrating Enlitic’s AI and data management capabilities with Philips’ imaging platforms to improve workflow efficiency, data standardization, and clinical decision-making.

- In December 2024, AGFA HealthCare and Rad AI announced a strategic collaboration to enhance radiology workflows through advanced AI integration. The partnership focused on combining AGFA HealthCare’s enterprise imaging and workflow platforms with Rad AI’s radiology reporting and automation solutions.

Companies Covered in AI in Medical Imaging Market

- Agfa-Gevaert Group

- Ada Health

- Enlitic Inc

- CellmatiQ GmbH

- General Electric Company

- IBM

- NVIDIA Corporation

- Microsoft

- Koninklijke Philips N.V.

- Siemens

- Others

Frequently Asked Questions

The global AI in medical imaging market is projected to be valued at US$ 2.4 Bn in 2026.

Rising imaging volumes, AI-driven diagnostic accuracy, workflow automation, chronic disease burden, and healthcare digitization.

The global AI in medical imaging market is poised to witness a CAGR of 26.7% between 2026 and 2033.

AI expansion in oncology, neurology, cloud platforms, emerging markets, and integrated diagnostic workflows.

Agfa-Gevaert Group, Ada Health, Enlitic Inc, CellmatiQ GmbH, General Electric Company, IBM.