- Automation & Robotics

- Agriculture Drone Market

Agriculture Drone Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Agriculture Drone Market Size, Share, and Growth Forecast by Product Type (Fixed Wing, Others), Coverage Distance (< 3 km, 3 km to 6 km), Application (Crop Spraying & Fertilization, Precision Farming, Others), Payload Capacity (Lightweight (Up to 10 kg), Others, and Regional Analysis for 2025 - 2032

Agriculture Drone Market Share and Trends Analysis

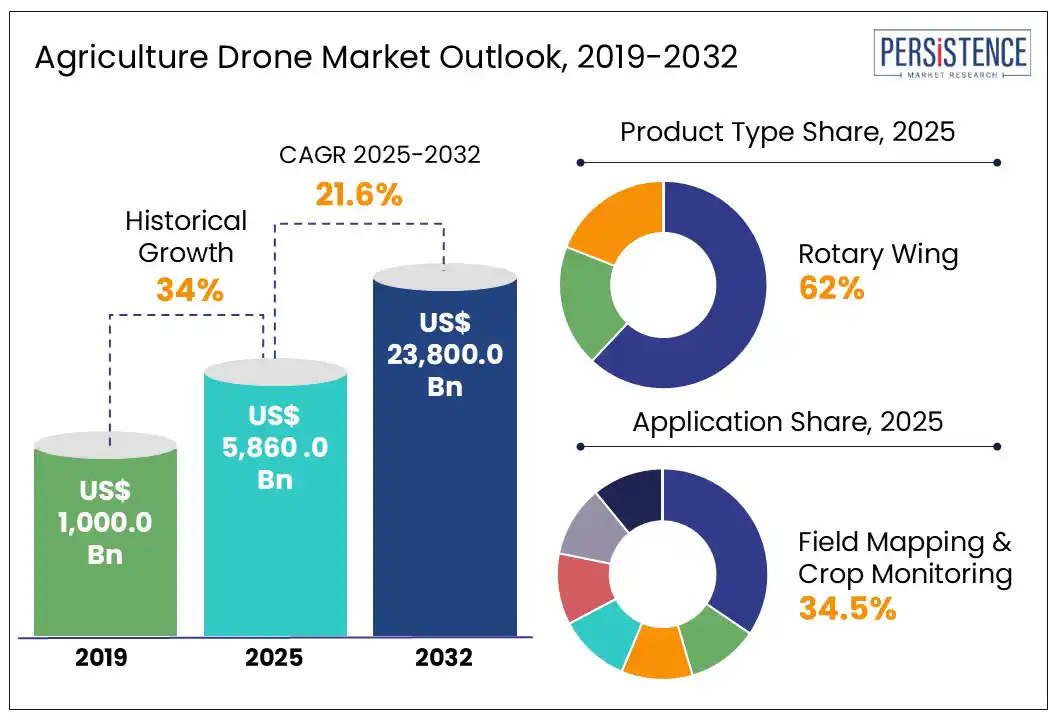

The global agriculture drone market size is likely to be valued at US$ 5.86 Bn in 2025, and is estimated to reach US$23.8 Bn by 2032, growing at a CAGR of 21.6% during the forecast period 2025−2032.

Agricultural drones, also known as Unmanned Aerial Vehicles (UAVs), are revolutionizing modern farming practices by enabling real-time crop monitoring, aerial spraying, field mapping, and variable rate application (VRA). The increasing demand for smart farming solutions, acute labor shortages, and heightening global pressure to enhance agricultural productivity are driving the rapid adoption of drone technology in agriculture.

According to the World Bank (WB), the global food demand is set to increase exponentially as world population is expected to touch 9.7 billion by 2050. Since agriculture contributes nearly 33% of all global emissions, the urgency to adopt climate-smart agriculture (CSA) is growing. The urgency to develop efficient land utilization and resource optimization practices is pushing governments and farmers alike to adopt drone-based precision agriculture systems. Innovations such as multispectral imaging, drone analytics software, and AI-based crop health analysis are further enhancing decision-making capabilities in agriculture.

Key Industry Highlights

- North America is projected to lead the market with a 35% revenue share in 2025, boosted by an early adoption of precision agriculture, favorable FAA regulations, and widespread use of GPS-enabled drones for crop monitoring and irrigation.

- Europe, holding around 30% market share as of 2025, is supported by sustainability-focused policies such as the EU Green Deal, with strong drone adoption in viticulture, orchard management, and livestock monitoring.

- Asia Pacific is the fastest-growing, expected to expand at a CAGR of 23% from 2025 to 2032, fueled by government subsidies in India and China, rising food demand, and increasing use of drones for staple crop cultivation.

- Rotary-wing drones dominate the product segment with a 62% share due to their maneuverability, VTOL capabilities, and suitability for targeted spraying and imaging in diverse terrains.

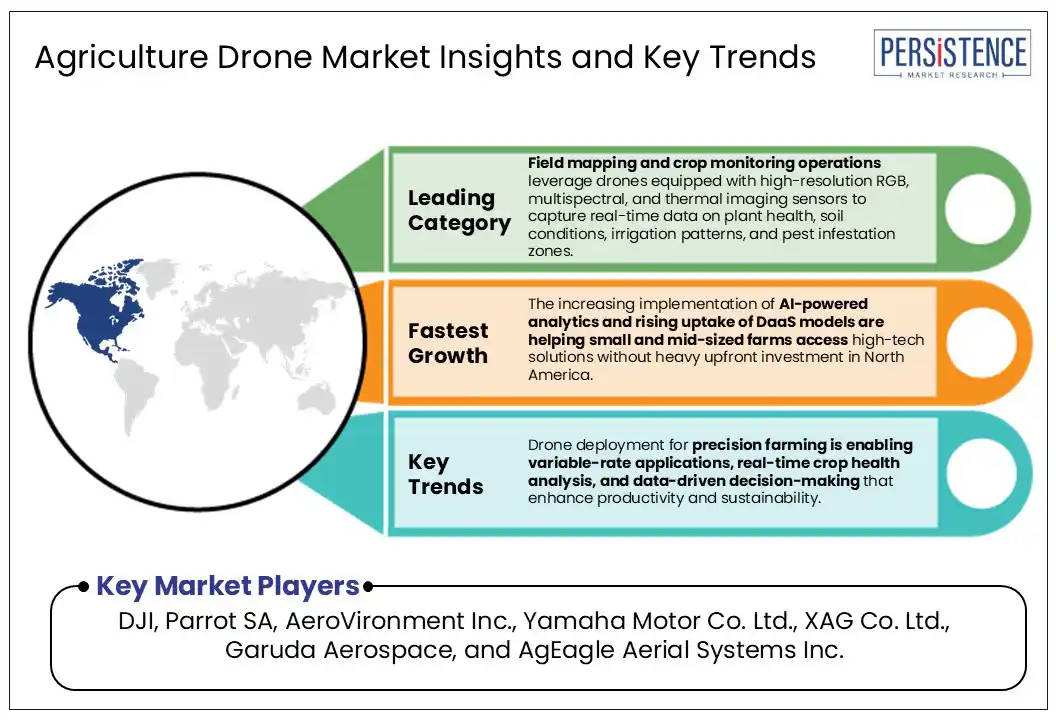

- The field mapping & crop monitoring segment, accounting for around 34.5% of the revenue share, is the largest application area, leveraging multispectral and thermal imaging to detect early signs of crop stress, optimize input use, and improve yield outcomes.

- Drone-as-a-Service (DaaS) models are making promising headway, enabling small and mid-sized farms to access drone technology without high upfront costs, especially in emerging markets such as India, China, and Brazil.

- Precision farming remains a core growth driver, with drones enabling variable-rate applications, real-time crop health analysis, and data-driven decision-making that enhance productivity and sustainability.

- Industry stakeholders are emphasizing the integration of AI, internet of things (IoT), and cloud-based analytics to support sustainable farming practices and meet the global food security goals.

Market Dynamics

Driver - Growing Urgency for Precision Farming Technologies to Fuel the Market

The core driver of the agriculture drone market growth is the rising need to balance agricultural productivity with climate concerns, especially in developing economies where agriculture is the mainstay occupation. In India and the Philippines, initiatives such as CGIAR’s Drones4Rice Project have introduced drone-based solutions for automated seeding, precision spraying, and real-time crop health monitoring, supported by multispectral and thermal sensor payloads. With over 145 million rice farmers in India and around 4.8 million hectares of rice under cultivation in the Philippines, drones are contributing to a significant transformation by reducing labor intensity, improving early detection of nutrient deficiencies and weed stress, and enabling variable-rate application of fertilizers and pesticides.

Furthermore, CropLife International’s recent case study similarly demonstrates how precision agriculture and drone technology are improving the efficiency of crop protection. Agricultural drones equipped with integrated sensors and GPS-based mapping systems enable farmers to apply crop protection products with high accuracy, thereby minimizing overlap, reducing application rates by up to 30 percent, and delivering inputs precisely where needed. Practices that once involved blanket pesticide spraying are now being replaced with targeted applications, resulting in both cost savings and reduced environmental impact.

Restraint - High Initial Costs and Regulatory Complexities to Hinder Mass Adoption

For a large section of small and marginal farmers, the initial investment required for agriculture drones remains prohibitive. A single high-end multispectral drone system can cost anywhere between ?4 lakh to ?10 lakh (US$ 5,000 – US$ 12,000), depending on the payload capacity, imaging features, and software compatibility. The cost of training, repair, and post-processing services often falls outside the operational budgets of smallholders, particularly in price-sensitive markets such as India. This is substantiated by a 2023 survey conducted by the Federation of Indian Chambers of Commerce & Industry (FICCI) that found that only 9% of Indian farmers were aware of drones in agriculture, and just 2% had access to drone-based services despite government subsidies.

On the regulatory front, inconsistencies in drone policies across regions add to operational friction. While countries such as the U.S. have streamlined their drone usage under the FAA's Part 107 regulations, others such as India still impose tight restrictions that limit flexibility. For example, India’s Drone Rules mandate drone registration, pilot certification, and approval of flight paths, which can deter agritech startups from scaling operations quickly. In parts of Europe, environmental compliance requirements and airspace zoning laws are forcing drone service providers to undergo lengthy approval cycles before deploying equipment. These complications have slowed down the agriculture drone market expansion.

Opportunity - Rising Interest in DaaS and Smart Farming Incentives to Unlock New Market Avenues

The shift toward DaaS is aiding the adoption of agriculture drones by mitigating the high upfront costs that have traditionally limited access for small and mid-sized farms. India continues to set trends with policies such as the Kisan Drone Yatra, which subsidizes up to 60% of drone costs for farmer producer organizations (FPOs) and supports rural custom hiring centers. This model has brought in its fold smallholder farmers who previously lacked the resources to invest in drone technology.

China offers another compelling example. XAG, a key drone manufacturer based in Guangzhou, has deployed over 42,000 agricultural drones domestically and operates in over 60 countries. These drones serve farmers via on-demand service teams offering spraying, seeding, and mapping. Similarly, Brazil is harnessing drone services in sugarcane production with measurable results. A partnership between Raízen and ARPAC achieved 47% operational savings and 82% reduced agrochemical usage on 16 hectares of pilot fields.

These examples exemplify a trend toward service-based access rather than ownership, allowing wide farmer adoption irrespective of scale. With the DaaS model gaining momentum, agriculture drones are poised to penetrate previously underserved markets and empower farmers with real-time data and resource-efficient tools.

Category-wise Analysis

Product Type Insights

Holding a revenue share of approximately 62%, rotary-wing drones, particularly multi-rotor variants, have emerged as the most widely adopted UAVs in agricultural settings due to their versatility, ease of operation, and the ability to hover with precision over fixed areas. These drones are ideally suited for tasks such as spot spraying, crop scouting, and close-range imaging, especially in fragmented and small landholdings. The compact design and vertical take-off and landing (VTOL) capabilities of rotary drones allow them to operate in diverse terrains, including orchards, greenhouses, and paddy fields, where fixed-wing drones would be impractical. These features make rotary-wing drones highly suitable for variable-rate application, which requires targeted spraying and fertilizer deployment. Manufacturers such as DJI, XAG, and Parrot are already expanding their multi-rotor product lines with heavy payload capacities and extended flight durations.

Their widespread use is further fueled by government programs aimed at mechanizing smallholder farming capacities. For example, the drone subsidy offered under India’s PM-Kisan targets multi-rotor drones for crop spraying, offering up to 60% financial assistance to rural cooperatives and custom hiring centers. Such policy support has further solidified rotary drones as the gateway technology for digital agriculture adoption, especially in emerging markets.

Application Insights

At 34.5%, the field mapping & crop monitoring segment represents the largest application area for agriculture drones. This segment leverages drones equipped with high-resolution RGB (red, green, blue spectrum), multispectral, and thermal imaging sensors to capture real-time data on plant health, soil conditions, irrigation patterns, and pest infestation zones. The value of this segment lies in its ability to transform raw aerial imagery into actionable insights. Using normalized difference vegetation index (NDVI) and other spectral analysis techniques, drones can detect early signs of crop stress or disease well before symptoms become visible to the human eye. This enables farmers to act preemptively, thereby reducing crop losses and optimizing input use. For instance, growers in the U.S. Corn Belt use drone-based mapping to detect nitrogen deficiencies and adjust fertilizer regimes mid-season, improving both yield and environmental outcomes. Software platforms such as DroneDeploy, Pix4D, and Agremo have further expanded the value of drone mapping by offering cloud-based analytics, geotagged reporting, and integration with existing farm management systems.

Regional Insights

North America Agriculture Drone Market Trends

North America is projected to maintain its leadership in the agriculture drone market, accounting for approximately 35% of the global revenue share in 2025. This dominance is based on the region’s early adoption of precision farming technologies and strong institutional support. The U.S. Department of Agriculture and FAA have streamlined drone regulations, enabling widespread use of drones for crop monitoring, irrigation management, and pesticide spraying. Advanced imaging systems and GPS-enabled drones are increasingly used for real-time field mapping, with a considerable portion of agricultural drone applications in the region involving GPS integration. The increasing implementation of AI-powered analytics and rising uptake of DaaS models are helping small and mid-sized farms access high-tech solutions without heavy upfront investments.

Europe Agriculture Drone Market Trends

Europe continues to be a hugely lucrative region for the market and is expected to grow steadily through 2032. The region’s growth is driven by sustainability-focused policies such as the EU’s Green Deal and Common Agricultural Policy, which are promoting the use of low-emission technologies in farming. Countries such as France and Germany are leveraging drones for precision viticulture, orchard management, and livestock monitoring. The integration of multispectral sensors into agriculture drones has led to significant improvement in yield predictions, while precision spraying has reduced pesticide usage noticeably. These innovations align with Europe’s long-term goals of reducing environmental impact and enhancing food security through smart agriculture.

Asia Pacific Agriculture Drone Market Trends

Asia Pacific is slated to be the fast-growing for the agriculture drone market, fueled by large-scale government initiatives in India and China aimed at enhancing agricultural yields using climate-smart farming practices. For example, India’s Sub-Mission on Agricultural Mechanization (SMAM) provides subsidies for drone purchases, while China supports full-cycle drone operations for staple crops such as rice and wheat. Being home to the largest population in the world, both these countries have to meet the skyrocketing demand for food and nutrition, which is stoking the adoption of smart agriculture technologies. An upcoming trend in Asia Pacific is that the demand for drones with longer flight times and larger payload capacities is showing an upward trajectory, particularly for large-scale field mapping and variable rate applications, which benefits this market.

Competitive Landscape

The global agriculture drone market is highly competitive, featuring an exciting blend of technology leaders and emerging regional players charting its growth path. Companies such as DJI, Parrot SA, AeroVironment Inc., Yamaha Motor Co., Ltd., and PrecisionHawk are at the forefront, leveraging their expertise in drone engineering and data analytics to offer comprehensive solutions for precision farming, crop health monitoring, and aerial spraying. DJI, for instance, currently dictates market dynamics with its extensive portfolio of agriculture-specific drones, which are widely used for spraying and seeding applications across Asia and North America.

Strategic public-private partnerships and regional expansion are central to the competitive strategies of major industry players. As an example, companies such as XAG in China and Garuda Aerospace in India are accruing steady gains by aligning their offerings with government-backed subsidy programs and local manufacturing incentives. These firms are focusing on affordability and scalability, making drone technology accessible to smallholder farmers. With the market maturing at a notable pace, competitive differentiation hinges on incorporating agriculture drones with next-generation software, real-time analytics, and compatibility with other farm management systems.

Key Industry Developments

- In June 2025, Turkish farmers in Gönen started adopting XAG’s P100 Pro agricultural drones to combat severe water scarcity and improve operational efficiency in rice farming. These autonomous drones enabled precise spraying and seeding, reduced reliance on labor, and allowed timely field access even after rain, transforming traditional workflows and boosting productivity.

- In June 2025, Garuda Aerospace inaugurated a 35,000 sq. ft. agri-drone indigenization facility in Chennai to design, manufacture, and test advanced unmanned aerial systems, aiming to boost domestic drone production and reduce import dependency. The launch also featured the government-backed ‘Drone Didi’ initiative, which trained 15,000 rural women as certified drone pilots.

- In May 2025, AgEagle Aerial Systems partnered with India’s Vyom Drones to locally manufacture and distribute its eBee X drones, aiming to enhance precision agriculture across India’s vast farmland. This collaboration combined AgEagle’s advanced drone and sensor technology with Vyom’s regional expertise, supporting crop monitoring, soil analysis, and water resource management while aligning with India’s goal to become a global drone hub by 2030.

Companies Covered in Agriculture Drone Market

- DJI

- Parrot SA

- AeroVironment, Inc.

- Yamaha Motor Co., Ltd.

- PrecisionHawk

- Trimble Inc.

- senseFly

- Delair

- XAG Co., Ltd.

- Garuda Aerospace

- AgEagle Aerial Systems Inc.

- DroneDeploy

Frequently Asked Questions

The market is projected to reach US$ 5.86 Bn in 2025.

The growing urgency for precision farming technologies and rising need to balance agricultural productivity with climate concerns are driving the market.

The market is poised to witness a CAGR of 21.6% from 2025 to 2032.

Rising interest in DaaS and extension of smart farming incentives by governments are key market opportunities.

DJI, Parrot SA, and AeroVironment Inc. are some of the key players in the market.