- Home Care & Utilities

- Agriculture Nets Market

Agriculture Nets Market Size, Share, and Growth Forecast 2026 - 2033

Agriculture Nets Market by Product Type (Shading Nets, Anti-hail, Anti-insects, Windbreak, Others), Form (Woven, Non-woven), Material Type (Metal, Plastic, Rubber, Others), Application (Farming Area, Animal Husbandry, Horticulture and Floriculture, Aquaculture, Others), Sales Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Agriculture Nets Market Size and Trend Analysis

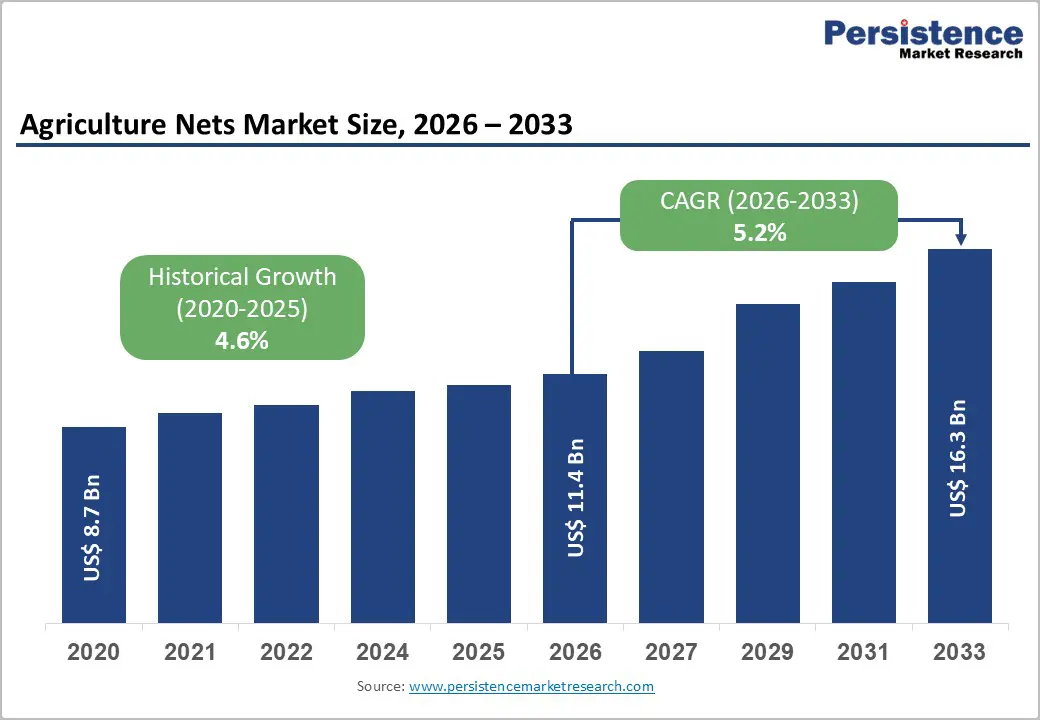

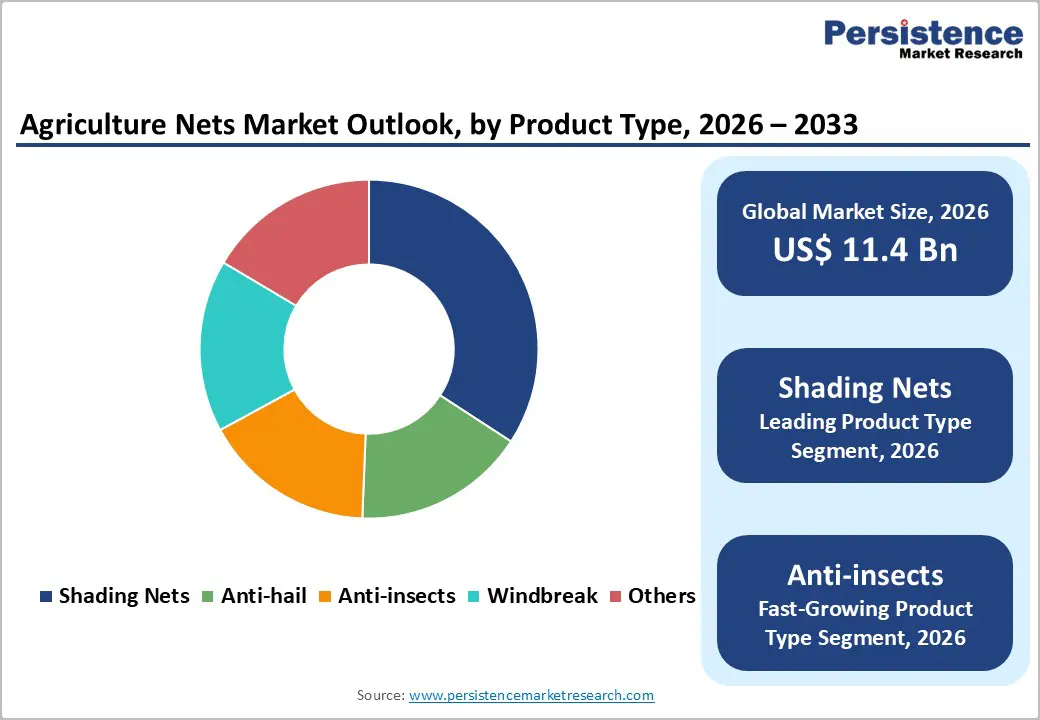

The global Agriculture Nets market size is expected to be valued at US$ 11.4 billion in 2026 and projected to reach US$ 16.3 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

The agriculture nets market is on a strong upward trajectory, driven by escalating global food security concerns, intensifying climate volatility, and the accelerating adoption of protected cultivation techniques worldwide. As extreme weather events, including unseasonal hailstorms, prolonged droughts, and elevated pest pressure, increasingly threaten open-field crop yields, farmers and agribusinesses across both developed and emerging economies are turning to specialty nets for crop protection, microclimate management, and yield optimization. Supportive government subsidy programs for greenhouse and controlled-environment agriculture across the European Union, India, and China further amplify procurement volumes, while rapid growth in horticulture, floriculture, and aquaculture sectors broadens the addressable application base for net manufacturers.

Key Industry Highlights:

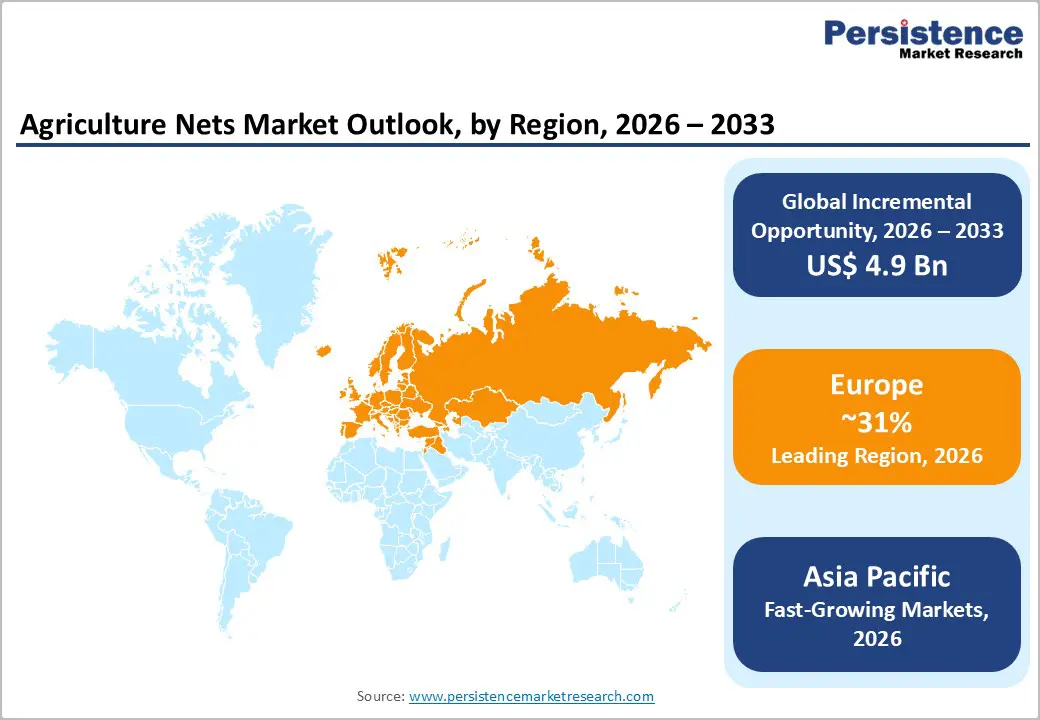

- Leading Region: Europe leads the global Agriculture Nets market with approximately ~31% revenue share in 2025, driven by Spain’s intensive horticulture sector, stringent EU pesticide reduction mandates under the Farm to Fork Strategy, and advanced protected cultivation infrastructure across France, Italy, and Germany.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market for agriculture nets over 2026–2033, fueled by China’s agricultural modernization programs, India’s government-subsidized shade net house schemes under PMKSY, and rapid aquaculture expansion across Vietnam, Indonesia, and Bangladesh.

- Dominant Products: Shading Nets dominate the Product Type segment with approximately ~32% market share in 2025, reflecting their universal application across horticulture, floriculture, livestock shelters, and nursery production in high-solar-radiation agricultural regions globally.

- Fastest Growing Product: Insect-exclusion nets are the fastest growing product type within the market, driven by EU Farm to Fork Strategy pesticide reduction targets and USDA IPM program incentives compelling growers to replace chemical pest control with physical exclusion netting solutions.

- Key Opportunity: Aquaculture net applications represent the key growth opportunity, with FAO data confirming aquaculture’s contribution to 50% of global seafood consumption, creating expanding demand for fish cage nets, predator exclusion nets, and pond covers across Asia Pacific and Latin America.

| Key Insights | Details |

|---|---|

|

Agriculture Nets Market Size (2026E) |

US$ 11.4 Billion |

|

Market Value Forecast (2033F) |

US$ 16.3 Billion |

|

Projected Growth CAGR (2026–2033) |

5.2% |

|

Historical Market Growth (2020–2025) |

4.6% |

Market Dynamics

Drivers - Climate Change-Driven Surge in Crop Protection Net Adoption

Increasing frequency and severity of adverse weather events linked to climate change are among the foremost drivers accelerating agricultural net adoption globally. Anti-hail, shading, and windbreak nets have transitioned from optional supplementary inputs to near-essential protective infrastructure in high-value crop cultivation regions. According to the Food and Agriculture Organization of the United Nations (FAO), climate-related agricultural losses cost the world economy an estimated US$ 123 billion annually, with developing economies bearing a disproportionate share. In apple, cherry, grape, and soft-fruit production, where a single hailstorm can destroy an entire season’s harvest, anti-hail nets deliver documented crop loss prevention rates exceeding 90%, providing clear economic justification for adoption. As climate risk intensifies across Europe’s Mediterranean basin, South America’s Andean fruit belt, and Asia Pacific’s subtropical agricultural zones, the demand for protective agriculture nets is projected to expand consistently throughout the forecast period.

Global Expansion of Protected Agriculture and Controlled-Environment Farming

The global shift toward protected agriculture, encompassing greenhouses, polytunnels, and shade houses, is generating sustained incremental demand for specialty agriculture nets. The International Society for Horticultural Science (ISHS) has documented a persistent increase in protected cultivation area worldwide, with global greenhouse vegetable production area estimated to exceed 500,000 hectares across major producing nations. In countries like the Netherlands, Spain, Israel, and increasingly China and India, intensive horticultural systems depend fundamentally on shading nets, insect-exclusion nets, and anti-bird nets to manage crop microclimate and exclude pest vectors without chemical intervention. This trend aligns closely with stricter pesticide residue regulations being implemented across the European Union under the Farm to Fork Strategy, which targets a 50% reduction in chemical pesticide use by 2030, directly incentivizing growers to replace chemical pest control with physical exclusion solutions such as insect-proof netting.

Restraints - Price Volatility of Petrochemical-Based Raw Materials

The majority of agriculture nets are manufactured from polyethylene (PE), polypropylene (PP), or high-density polyethylene (HDPE), all of which are derived from petrochemical feedstocks. Raw material costs are therefore subject to crude oil price fluctuations, which can be highly volatile. The U.S. Energy Information Administration (EIA) reported crude oil price swings of over 40% in certain twelve-month periods, creating significant cost uncertainty for net manufacturers and compressing margins when price increases cannot be passed on to price-sensitive agricultural end users. For smallholder farmers in developing economies, who constitute the vast majority of global agricultural producers, even moderate input price increases can deter or delay net adoption, creating demand headwinds in growth markets such as sub-Saharan Africa and South and Southeast Asia.

Limited Awareness and Technical Know-How Among Smallholder Farmers

Despite demonstrable agronomic benefits, the adoption of specialty agriculture nets remains constrained in many developing markets due to limited technical awareness and the absence of extension services to guide proper installation and maintenance. According to the World Bank, smallholder farmers manage approximately 84% of the world’s farms and produce roughly 35% of global food supply, yet access to modern agricultural inputs and advisory services remains profoundly uneven. Incorrect net selection, such as using inappropriate shading percentages or failing to properly tension anti-insect nets to prevent gap infiltration, can result in suboptimal outcomes, discouraging further adoption and negatively affecting market penetration rates in regions with the highest growth potential.

Opportunity - Rising Demand for Insect-Exclusion Nets in IPM and Pesticide Reduction Programs

Insect-proof agricultural nets represent one of the fastest-growing product categories within the broader agriculture nets market, and the policy environment is increasingly supportive of this trajectory. The European Union’s Farm to Fork Strategy and the USDA’s Integrated Pest Management (IPM) programs are actively encouraging growers to adopt physical pest exclusion barriers as a primary line of defense, reducing dependence on synthetic insecticides. Insect-exclusion nets with fine mesh apertures of 0.8–1.2 mm have been scientifically validated to exclude key pest vectors including thrips, whiteflies, and aphids while maintaining adequate ventilation for crop health. As regulatory pressure on neonicotinoids and other broad-spectrum insecticides intensifies globally, with several active ingredients already banned or under review in the EU and UK, the commercial opportunity for manufacturers offering certified insect-exclusion net solutions in high-value vegetable, berry, and ornamental crop segments is substantial and structurally growing.

Aquaculture Industry Expansion Driving Demand for Specialty Nets

The rapid global expansion of aquaculture represents a high-potential and underserved growth opportunity for agriculture net manufacturers. Aquaculture is the world’s fastest-growing food production sector: the FAO’s State of World Fisheries and Aquaculture 2022 report documented that aquaculture now contributes approximately 50% of global fish and seafood consumption, and production volumes are projected to grow significantly through 2030 to meet rising protein demand. Fish cage nets, predator exclusion nets, pond covers, and anti-bird nets are indispensable inputs in both marine and freshwater aquaculture operations. In South and Southeast Asia, where countries like China, India, Vietnam, Indonesia, and Bangladesh are among the world’s top aquaculture producers, the formalization and intensification of fish farming operations is creating a rapidly expanding addressable market for durable, UV-stabilized, and chemical-resistant specialty aquaculture nets across the 2026–2033 forecast period.

Category-wise Analysis

Product Type Insights

Shading nets represent the dominant product type within the agriculture nets market, holding an estimated ~32% of total revenue share in 2025. Their widespread adoption is driven by the fundamental agronomic need to regulate solar radiation intensity, manage crop canopy temperatures, and reduce evapotranspiration rates across a broad range of horticultural, floriculture, and vegetable production systems. In regions with intense solar radiation, including the Mediterranean basin, the Middle East, South Asia, and sub-Saharan Africa, shading nets are a near-universal requirement for high-quality crop production. Available in a range of shading factors from 20% to 90%, these nets serve diverse applications from fruit orchards and nurseries to protected greenhouses and livestock shelters. The FAO has actively promoted shading net technology under climate adaptation programs in arid and semi-arid agricultural zones, further reinforcing demand among smallholder and commercial growers alike.

Form Analysis

Woven agriculture nets dominate the form segment, accounting for approximately ~68% of total market share in 2025. Woven nets, manufactured through raschel or flat weaving processes using HDPE or PP monofilaments, offer superior dimensional stability, mechanical strength, and durability compared to non-woven alternatives, making them the preferred choice for demanding outdoor agricultural applications including anti-hail systems, windbreaks, shade structures, and crop support nets. Their ability to maintain consistent mesh aperture under tension and UV exposure is critical for insect-exclusion efficacy and structural performance. Leading manufacturers such as Raschel Textil GmbH and Jubo Group Co., Ltd have invested in advanced raschel knitting technology to produce high-performance woven nets with UV stabilization additives offering service lives of 5 to 10 years in field conditions, delivering compelling economic value to growers.

Material Type Analysis

Plastic-based agriculture nets, primarily those manufactured from high-density polyethylene (HDPE) and polypropylene (PP), dominate the material type segment with an estimated ~72% market share in 2025. The dominance of plastic is attributable to its exceptional combination of light weight, flexibility, UV resistance (when stabilized with carbon black or HALS additives), chemical inertness, and cost-effectiveness, making it the material of choice for virtually all major agricultural net applications. Plastic nets can be engineered with precise mesh geometries for insect exclusion or specific shading factors for light management, and they are compatible with all standard net installation systems. The cost advantage over metal nets, which, while highly durable, are significantly heavier and more expensive, is particularly important for the large smallholder farmer segment. Advances in biopolymer and recycled plastic net formulations are also beginning to expand the sustainable materials segment within this category.

Application Insights

The Farming Area application segment, encompassing row cover nets, crop support nets, anti-bird nets, and general field protection systems used in open-field arable and vegetable cultivation, holds the leading position with approximately ~38% market share in 2025. Open-field farming remains the predominant cultivation mode globally, with the FAO estimating that over 1.4 billion hectares of cropland is under cultivation worldwide, the vast majority of which is open-field. Even modest penetration of protective netting across this enormous base represents a very large absolute demand volume. Fruit and vegetable farms in Europe, North America, and the Asia Pacific increasingly deploy crop net systems as part of integrated crop management protocols to protect against insect pests, birds, wind damage, and hailstorms, with growing adoption driven by insurance requirements and food retailer quality specifications mandating lower chemical residue levels in fresh produce.

Sales Channel Insights

The offline sales channel, encompassing agricultural input dealers, farm supply cooperatives, hardware distributors, and direct manufacturer sales representatives, dominates the agriculture nets market with an estimated ~74% of total sales in 2025. Offline channels remain dominant due to the nature of agriculture net purchasing: farmers typically require physical product assessment, customized cut-to-length specifications, volume-based pricing negotiation, and on-site technical consultation for installation, services that are most efficiently delivered through local dealer networks and direct sales teams. In developing markets across Asia Pacific, Latin America, and Africa, the rural dealership network is the primary and often only reliable point of access for agricultural inputs. However, the online channel is the fastest-growing, particularly in North America and Europe, where digital-native agri-commerce platforms are gaining traction among tech-savvy commercial growers seeking competitive pricing and streamlined procurement.

Regional Insights

North America Agriculture Nets Market Trends and Insights

North America is a mature and technologically advanced market for agricultural nets, with the United States as the dominant country contributor. The U.S. agriculture sector, one of the world’s most productive, with total agricultural output valued at over US$ 460 billion annually according to the U.S. Department of Agriculture (USDA), is experiencing growing adoption of specialty nets in high-value crop segments including berries, tree fruits, vegetables, and nursery stock. The USDA’s Risk Management Agency (RMA) crop insurance programs have increasingly recognized hail and frost damage protection from nets as an insurable mitigation measure, incentivizing grower adoption in apple and wine grape belts of the Pacific Northwest, Michigan, and upstate New York.

Innovation in the region is driven by precision agriculture integration, with manufacturers developing nets embedded with pest monitoring sensors and photoselective pigments that optimize light spectra for target crops. Canada’s expanding greenhouse vegetable sector, particularly in Ontario and British Columbia, contributes incrementally to regional net demand. Regulatory tailwinds from the U.S. Environmental Protection Agency (EPA)’s ongoing pesticide registration review process are also encouraging growers to transition toward physical pest management solutions, including insect-exclusion netting.

Europe Agriculture Nets Market Trends and Insights

Europe represents the leading region in the global agriculture nets market, accounting for an estimated ~31% of global market share in 2025, underpinned by the continent’s highly developed horticulture sector, stringent food safety regulations, and strong government support for sustainable farming practices. Spain, the largest fruit and vegetable exporter in the EU with over EUR 17 billion in annual agri-food exports according to the Spanish Ministry of Agriculture, is one of the world’s most intensive users of agricultural netting systems, spanning shading nets in Almería’s plastic sea, anti-insect tunnels, and anti-hail structures across its Levante fruit orchards. France, Italy, and Germany are also significant markets, driven by viticulture, stone fruit, and specialty vegetable production.

Regulatory harmonization under the EU Farm to Fork Strategy is a defining market force, as EU-wide targets for 50% pesticide reduction by 2030 are compelling growers across member states to invest in physical crop protection infrastructure. Don & Low Ltd and Saint-Gobain are among the established players aligning product development with EU sustainability certification requirements. Demand for biodegradable and recyclable net materials is rising in response to EU Single-Use Plastics Directive implementation, opening innovation opportunities for material suppliers and net manufacturers across the region.

Asia Pacific Agriculture Nets Market Trends and Insights

Asia Pacific is the fastest-growing regional market for agriculture nets over the forecast period, propelled by the region’s enormous agricultural base, rapid modernization of farming practices, and supportive government investment in food security infrastructure. China, the world’s largest agricultural economy and the top producer of vegetables, fruits, and aquaculture products, is a dominant force in regional demand. The Chinese government’s sustained investment under agricultural modernization programs, including the 14th Five-Year Plan for Agricultural Development, prioritizes protected cultivation expansion and agro-technology upgrades, directly stimulating net adoption across millions of hectares of cultivated land.

India is emerging as one of the highest-growth markets globally for agriculture nets. The National Horticulture Board (NHB) of India has been actively subsidizing shade net houses and insect-proof net structures under the Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) and related horticulture development schemes, bringing cost-effective net technology within reach of smallholder farmers. Japan, Vietnam, Thailand, and Indonesia further contribute to regional volume growth, with Japanese precision horticulture driving premium net technology adoption and ASEAN nations expanding aquaculture operations that require specialty cage and predator-exclusion nets. Domestic manufacturers such as Shakti Polyweave Pvt. Ltd and Nippon Filcon Co., Ltd. benefit from low-cost production advantages and deep regional distribution networks.

Competitive Landscape

The global agriculture nets market is highly fragmented, with numerous regional and local manufacturers operating alongside a limited number of multinational suppliers with diversified polymer and technical textile portfolios. Large, vertically integrated participants compete through material science capabilities, advanced extrusion technologies, and well-established global distribution networks. Their strategies emphasize performance differentiation through enhanced durability, UV stabilization, tensile strength optimization, and sustainability-focused product development, including recyclable and bio-based netting solutions aligned with evolving environmental regulations.

Mid-sized and regional manufacturers primarily compete on cost efficiency, customization flexibility, and proximity to farming clusters, enabling faster delivery cycles and tailored solutions for specific crop and climatic conditions. Across the industry, companies are increasingly targeting high-growth segments such as aquaculture and protected cultivation, while investing in product line extensions and digital sales platforms to improve market reach. Strategic focus also includes capacity expansion in emerging markets, partnerships with agri-input distributors, and technical advisory services to strengthen long-term customer relationships.

Key Developments:

- February 2025: Berry Global Inc. announced the expansion of its sustainable agricultural films and nets product line, introducing a new range of 30% recycled content HDPE shade and insect-exclusion nets targeted at European horticulture customers seeking compliance with EU circular economy and packaging regulations.

Companies Covered in Agriculture Nets Market

- Shafeng Grp Co., Ltd

- Jubo Group Co., Ltd

- Greenpro Nets Co., Ltd

- Berry Global Inc.

- Tensar Corporation

- Saint-Gobain

- Mehler Variotex GmbH & Co. KG

- Raschel Textil GmbH

- Nippon Filcon Co., Ltd.

- JX Nippon ANC

- Shakti Polyweave Pvt. Ltd

- Belton Industries Inc.

- Neo Corp International Limited

- B&V Agro Irrigation Co.

- Don & Low Ltd

- Beaulieu Technical Textiles

- Groupe Barbier

- Karatzis S.A.

Frequently Asked Questions

The global Agriculture Nets market is valued at US$ 11.4 billion in 2026 and is projected to reach US$ 16.3 billion by 2033 at a CAGR of 5.2%.

Demand is driven by climate-related crop protection needs, expansion of greenhouse cultivation, pesticide reduction regulations, and supportive subsidy programs.

Europe leads the market with around 31% revenue share in 2025, supported by advanced horticulture practices and strong sustainability policies.

The key opportunity lies in aquaculture, where rising global fish consumption is increasing demand for durable fish cages and anti-predator nets.

Key players include Berry Global Inc., Saint-Gobain, Tensar Corporation, Don & Low Ltd, and Shakti Polyweave Pvt. Ltd, among others, competing through innovation and global expansion.