- Agrochemicals

- Agriculture Adjuvants Market

Agriculture Adjuvants Market Size, Share, and Growth Forecast, 2026 – 2033

Agriculture Adjuvants Market by Product Type (Activator Adjuvants, Oil Adjuvants, Surfactants, Utility Adjuvants), Application (Fungicide Adjuvants, Insecticide Adjuvants, Herbicide Adjuvants), and Regional Analysis for 2026 – 2033

Agriculture Adjuvants Market Size and Trends Analysis

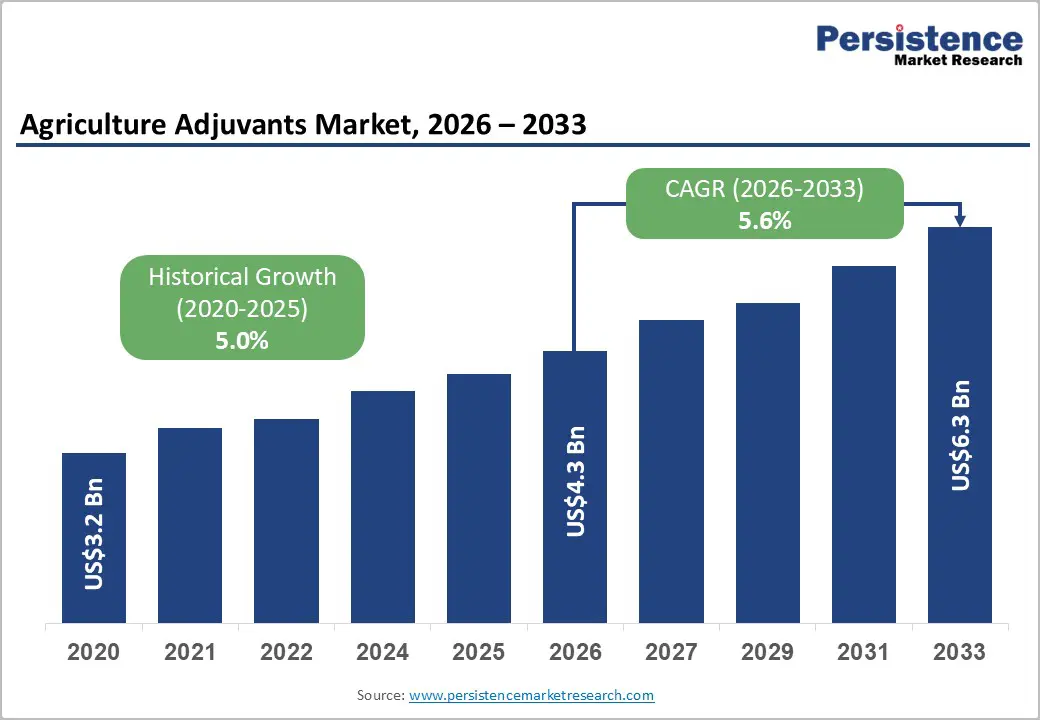

The global agriculture adjuvants market size is likely to be valued at US$4.3 billion in 2026 and is expected to reach US$6.3 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by rising food demand amid population expansion, increasing pressure to maximize crop yields from limited arable land, and the growing adoption of precision agriculture and advanced crop protection practices.

Adjuvants are increasingly used to improve spray efficiency, chemical uptake, and efficacy, enabling farmers to achieve higher productivity while reducing input costs. Regulatory emphasis on sustainable farming and reduced agrochemical usage, particularly in Europe and North America, is accelerating demand for high-performance and environmentally compatible adjuvants. Technological advancements in formulation chemistry, including bio-based and multifunctional adjuvants, are enhancing product adoption across diverse crop types.

Key Industry Highlights:

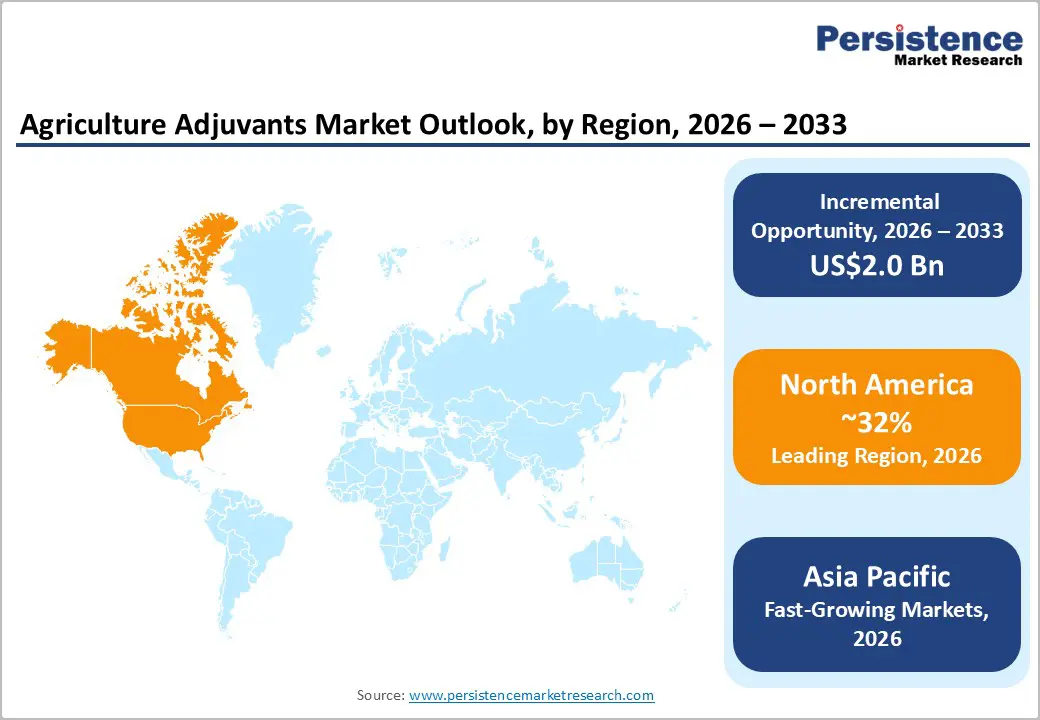

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 32% in 2026, driven by advanced precision farming adoption, strong regulatory frameworks, and high penetration of modern crop protection technologies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the agriculture adjuvants in 2026, supported by expanding agricultural activity, rising food demand, and increasing adoption of modern crop protection practices across emerging economies.

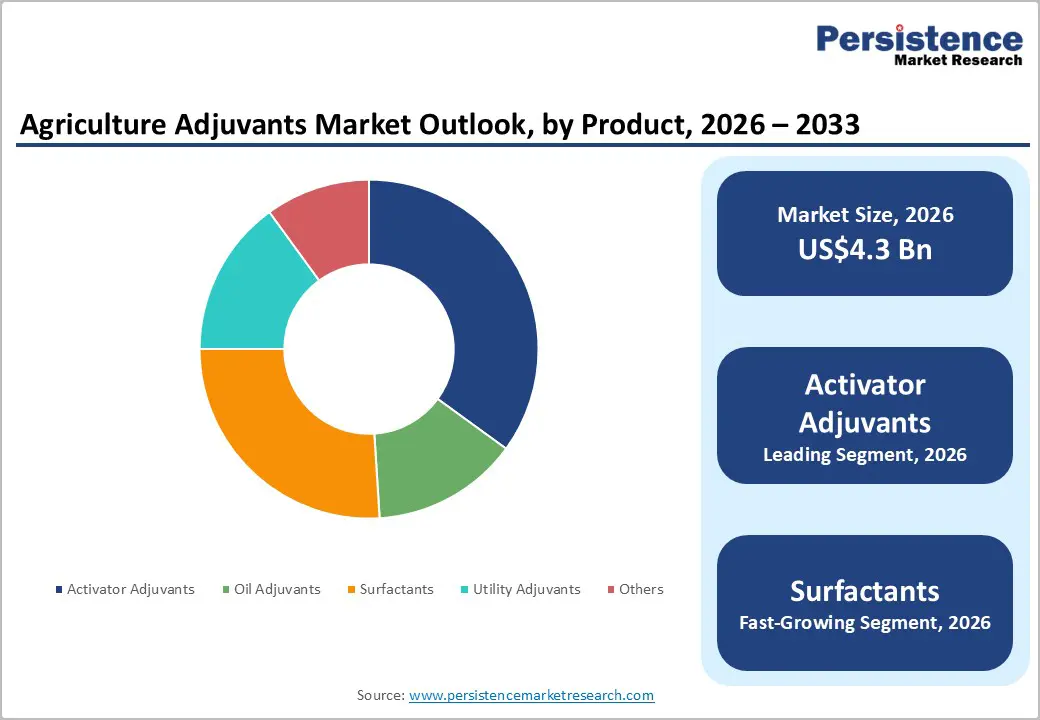

- Leading Product Type: Activator adjuvants are projected to represent the leading product type in 2026, accounting for 35% of the revenue share, driven by their strong role in enhancing pesticide efficacy and crop yield outcomes.

- Leading Application: Fungicide adjuvants are anticipated to be the leading application type, accounting for over 30% of the revenue share in 2026, supported by high usage in disease management for fruits and high-value crops.

| Key Insights | Details |

|---|---|

| Agriculture Adjuvants Market Size (2026E) | US$4.3 Bn |

| Market Value Forecast (2033F) | US$6.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Adoption of Integrated Pest Management (IPM) Practices

Integrated pest management (IPM) emphasizes optimized, targeted, and environmentally responsible pest control. IPM frameworks prioritize combining biological, cultural, mechanical, and chemical methods to minimize crop damage while reducing reliance on excessive pesticide use. Within this approach, agricultural adjuvants play a critical role by enhancing the performance of crop protection chemicals, ensuring effective pest control at lower application rates. By improving spray coverage, adhesion, penetration, and rain fastness, adjuvants help farmers achieve consistent results aligned with IPM principles.

As regulatory bodies and agricultural agencies promote IPM adoption to address pesticide resistance and environmental concerns, the demand for high-performance adjuvants that improve chemical efficiency continues to rise.

The growing focus on resistance management within IPM programs significantly supports adjuvant adoption across agricultural markets. Repeated and improper pesticide usage has led to widespread resistance among weeds, insects, and plant pathogens, reducing the effectiveness of conventional treatments. Adjuvants mitigate this challenge by enabling better absorption and uniform distribution of pesticides, improving control outcomes and reducing the need for repeat applications. This aligns with integrated pest management goals of maintaining long-term pest control efficacy while lowering environmental impact.

IPM adoption is accelerating in regions with strict regulatory frameworks, such as Europe and North America, where reduced chemical usage and residue limits are mandated. Emerging economies are also embracing IPM to improve food security and crop productivity.

High Raw Material Volatility and Supply Chain Disruptions

Agricultural adjuvants rely heavily on petrochemical derivatives, specialty surfactants, oils, and solvents, whose prices fluctuate due to crude oil price instability, geopolitical tensions, and changes in supply-demand dynamics. Sudden increases in raw material costs make it difficult for manufacturers to maintain stable pricing, often forcing them to pass costs on to end users. This price sensitivity can discourage adoption among cost-conscious farmers, particularly in developing regions where margins are already thin.

Variability in raw material quality can affect formulation consistency and product performance, increasing the need for reformulation and quality testing. These challenges limit scalability and create uncertainty in long-term planning, restraining market growth despite strong demand fundamentals.

Supply chain disruptions intensify these challenges by affecting the availability and timely delivery of key inputs and finished products. Agriculture adjuvant supply chains are highly interconnected, with raw materials sourced from multiple regions and finished products distributed across diverse agricultural markets. Disruptions caused by transportation bottlenecks, port congestion, trade restrictions, and extreme weather events can delay shipments and increase logistics costs. Such disruptions impact seasonal agricultural cycles, where delayed availability of adjuvants can reduce their effectiveness during critical crop protection windows.

Smaller manufacturers and regional suppliers are particularly vulnerable due to limited inventory buffers and supplier diversification.

Rise of Bio-Based and Organic Adjuvants

Bio-based adjuvants, derived from renewable sources such as plant oils, natural surfactants, and biodegradable polymers, align well with efforts to reduce the environmental footprint of agriculture. Farmers and agribusinesses seek to comply with stricter regulations on chemical usage and residue limits, these adjuvants offer an effective alternative that enhances pesticide performance while minimizing ecological impact. Their ability to improve spray efficiency, reduce drift, and enhance active ingredient uptake makes them suitable for both conventional and organic farming systems.

The expansion of organic farming acreage worldwide is directly increasing demand for adjuvants that meet organic certification standards.

The adoption of bio-based and organic adjuvants is being accelerated by changing consumer preferences and supply-chain requirements across the agricultural value chain. Food processors, retailers, and exporters are increasingly demanding sustainably produced crops, pushing farmers to adopt inputs that support eco-labeling and traceability initiatives. Bio-based adjuvants help farmers meet these expectations by enabling efficient crop protection with reduced chemical dependency.

Technological advancements in formulation chemistry are also improving the performance and shelf stability of organic adjuvants, addressing earlier concerns related to efficacy and cost competitiveness. Emerging markets present additional opportunities, as governments promote sustainable agriculture to improve soil health and long-term productivity.

Category-wise Analysis

Product Type Insights

Activator adjuvants are expected to lead the agriculture adjuvants market, accounting for approximately 35% of revenue in 2026, due to their critical role in enhancing the effectiveness of crop protection chemicals. These adjuvants improve spray adhesion, spreading, and penetration, enabling active ingredients to perform more efficiently on plant surfaces. Their widespread adoption across major field crops such as cereals, oilseeds, and pulses reflects farmers’ preference for solutions that maximize chemical performance while supporting cost-efficient farming practices.

Activator adjuvants are particularly valued in large-scale commercial agriculture, where uniform application and consistent pest control outcomes are essential for maintaining yield stability. For example, in row crop farming systems, activator adjuvants are commonly used alongside herbicides to ensure better leaf coverage and improved uptake, resulting in more reliable weed control under varying environmental conditions.

Surfactants are likely to represent the fastest-growing segment in 2026, driven by their versatility and suitability for modern farming practices. Their growth momentum is supported by increasing adoption in precision agriculture systems, where accurate spray placement and uniform wetting are essential. Surfactants reduce surface tension, allowing spray droplets to spread evenly across plant leaves, which improves contact with target pests and diseases. This functionality makes them highly effective in foliar applications across fruits, vegetables, and specialty crops.

For example, their growing use in horticulture farming, where uniform coverage on waxy or hydrophobic leaf surfaces is critical for effective fungicide and insecticide performance. Surfactants are also gaining traction due to rising regulatory and consumer preference for low-residue and environmentally compatible formulations.

Application Insights

Fungicide adjuvants are projected to lead the market, capturing around 30% of the revenue share in 2026, supported by their essential role in disease management across high-value crops. These adjuvants enhance fungicide performance by improving spray coverage, adhesion, and rain fastness, which are critical factors in preventing fungal infections. Their importance is particularly evident in fruit, vegetable, and plantation crops, where disease outbreaks can significantly impact yield quality and market value.

For example, in orchard farming, fungicide adjuvants are widely used to ensure consistent coverage across dense canopies, helping protect crops from moisture-driven fungal diseases. The consistent demand for effective disease control solutions, combined with increasing cultivation of horticultural crops, supports the leadership of fungicide adjuvants.

In 2026, insecticide adjuvants are expected to be the fastest-growing application, driven by rising pest pressures and the challenges of evolving pest resistance. These adjuvants enhance insecticide performance by improving deposition, penetration, and residual activity, making pest control more effective and sustainable. Their growth is closely tied to the wider adoption of integrated pest management (IPM) practices, which focus on precise and targeted chemical use. For instance, their use is expanding in vegetable cultivation, where high insect pressure necessitates consistent protection to maintain crop quality.

Additionally, insecticide adjuvants are increasingly being combined with biological and reduced-toxicity insecticides, boosting efficacy while supporting sustainability objectives.

Regional Insights

North America Agriculture Adjuvants Market Trends

North America is anticipated to be the leading region, accounting for a market share of 32% in 2026, driven by the widespread adoption of precision agriculture technologies, stringent regulatory frameworks promoting sustainable chemical use, and high penetration of modern crop protection practices. The U.S. and Canada, as major agricultural producers, are increasingly integrating advanced spraying systems, GPS-guided equipment, and drone-assisted applications that rely on adjuvants to enhance spray efficiency and active ingredient uptake.

For example, Corteva Agriscience has expanded its adjuvant portfolio in North America with formulations that optimize fungicide and herbicide performance, reflecting the growing demand for efficient and sustainable crop protection methods tailored to regional farming systems.

Regulatory focus on reduced chemical usage and environmental protection has also encouraged the development of environmentally compatible adjuvant formulations, attracting farmers aiming to meet stricter residue standards and sustainability goals. Producer interest in multifunctional adjuvants that improve coverage, penetration, and chemical efficacy supports broader adoption across crop types, from cereals in the U.S. Midwest to specialty horticulture in California and Florida. This trend reflects a broader shift toward integrated crop protection systems that optimize agronomic performance and align with regional environmental stewardship priorities, making adjuvants an essential component of modern North American agricultural practices.

Europe Agriculture Adjuvants Market Trends

Europe is likely to be a significant market for Agriculture Adjuvants in 2026, due to strict environmental regulations and sustainable farming initiatives, which are reshaping how adjuvants are developed and deployed. Farmers across major European markets such as France, Germany, Spain, and Italy are increasingly incorporating adjuvants into integrated pest management (IPM) programs to improve spray coverage and uptake, especially under variable climatic conditions that are common across the continent. This trend is supported by robust digital agriculture adoption, where adjuvant recommendations are integrated into decision-support platforms to optimize pesticide tank mixes and application timing.

The advanced farming infrastructure and strong emphasis on eco-friendly crop protection practices make Europe a distinct market where performance and regulatory compliance converge. For example, Evonik Industries AG, a leading German specialty chemicals company, which offers its TEGO® adjuvant portfolio comprising advanced organosilicon and non-ionic surfactants that improve spray retention, systemic uptake, and rain fastness. These products are engineered specifically to meet European regulatory requirements focused on sustainability and reduced environmental impact, helping growers maintain crop protection efficacy with lower chemical use.

Asia Pacific Agriculture Adjuvants Market Trends

The Asia Pacific region is likely to be the fastest growing region in the agriculture adjuvants market, in 2026 driven by the region’s need to support rising food demand, modernize farming practices, and enhance crop protection efficiency. With Asia Pacific emerging as one of the fastest-growing regional markets for agricultural adjuvants, farmers are increasingly adopting adjuvants to improve spray performance, enhance uptake of active ingredients, and maximize yields under diverse climatic conditions. This growth is supported by extensive agricultural activities in major producing countries such as China and India, where the expansion of arable land use and intensification of crop protection programs drive robust demand for adjuvant-enhanced spray formulations.

Government initiatives and extension services in several Asia Pacific nations are promoting efficient pesticide use and input-saving practices, creating a favorable environment for adjuvant adoption and high-value crop sectors. For example, Nufarm Limited, an Australian agricultural chemical company with a strong presence across the Asia Pacific region, which has been enhancing its product portfolio and distribution networks to better serve local farmers with crop protection solutions that include adjuvant packages bundled with herbicide and fungicide formulations.

Nufarm’s strategic focus on Asia reflects the rising importance of markets such as China, India, Southeast Asia, and Australia for crop protection inputs, where the performance of active ingredients is increasingly augmented through optimized adjuvant chemistries designed for varied crop and climate conditions.

Competitive Landscape

The global agriculture adjuvants market exhibits a moderately fragmented structure, driven by the presence of multiple multinational and regional players offering diverse adjuvant solutions to enhance crop protection efficacy and sustainability. Companies in this space vary from large agrochemical conglomerates to specialized chemical manufacturers, creating a competitive environment that emphasizes innovation, product performance, and geographic reach. Demand for eco-friendly formulations, bio-based adjuvants, and advanced spray technologies has intensified competition, encouraging firms to invest in R&D, partnerships, and portfolio expansions to meet evolving farmer needs.

With key leaders including BASF SE, Corteva Agriscience, Evonik Industries AG, Croda International PLC, and Solvay S.A., the market’s major players set strategic direction through innovation and broad distribution networks that span agricultural markets. These players compete through dedicated research and development to introduce multifunctional and sustainable adjuvant products, aggressive geographic expansion to capture high-growth regions, and value-added services such as farmer education and technical support. Enhanced product customization for specific crop types and agrochemical partners, competitive pricing strategies, and strengthening supply chain frameworks are additional tactics used to differentiate offerings.

Key Industry Developments:

- In April 2025, Nouryon launched Adsee® Flex 960 at the ISAA Symposium 2025 in Rio de Janeiro, Brazil. The new crop protection adjuvant features a patented blend of surfactants and colloidal silica, designed to enhance pesticide performance by improving deposition, adhesion, and rainfastness of active ingredients. Field trials conducted demonstrated improved fungicide efficacy. The microplastic-free formulation complies with TSCA, FIFRA, and EU REACH regulations, supporting more efficient and sustainable crop protection by reducing the need for reapplication and conserving resources.

- In November 2025, BRB International relaunched its BRB Silicone Adjuvants for the agrochemicals sector in the Netherlands. The low-viscosity silicone polyether copolymer is designed to enhance wetting, spreading, and penetration of spray solutions. It can be used as a formulation ingredient in water-based herbicides, insecticides, fungicides, and plant growth regulators, or as a tank-mix adjuvant for foliar-applied agrochemicals. The relaunch reflects BRB’s focus on sustainable and efficient crop protection solutions following supply chain corrections and material cost optimization.

Companies Covered in Agriculture Adjuvants Market

- Clariant AG

- Solvay SA

- The Dow Chemical Company

- Huntsman International LLC

- Evonik Industries AG

- Ingevity

- Nufarm Limited

- Corteva Agriscience

- Croda International PLC

- BASF SE

- Miller Chemical & Fertilizer, LLC.

- Helena Chemical Company

Frequently Asked Questions

The global agriculture adjuvants market is projected to reach US$4.3 billion in 2026.

The agriculture adjuvants market is driven by the growing adoption of precision agriculture and integrated crop protection practices to enhance pesticide efficacy and crop yield.

The agriculture adjuvants market is expected to grow at a CAGR of 5.6% from 2026 to 2033.

Key market opportunities in the agriculture adjuvants market include the rising demand for bio-based and organic adjuvants, growth of precision farming technologies, expansion of sustainable crop protection solutions, and increasing adoption of integrated pest management (IPM) practices.

Clariant AG, Solvay SA, The Dow Chemical Company, Huntsman International LLC, and Evonik Industries AG are the leading players.