- Technology

- Connected Agriculture Market

Connected Agriculture Market Size, Share, and Growth Forecast, 2025–2032

Connected Agriculture Market by Component (Solutions, Services), Technology (IoT Devices & Smart Sensors, AI, ML, & Predictive Analytics, Robotics, Drones & Automation Systems, Connectivity Infrastructure), Application (Livestock Monitoring, Precision Farming, Supply Chain Management, Market Access Solutions), and Regional Analysis 2025-2032

Connected Agriculture Market Size and Trends Analysis

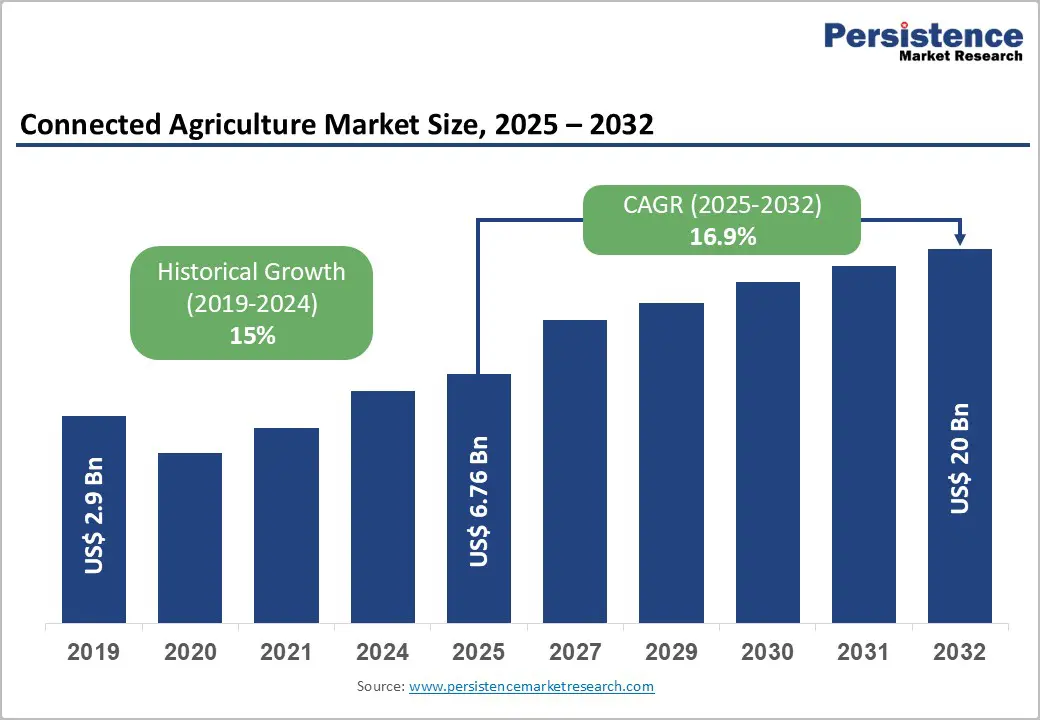

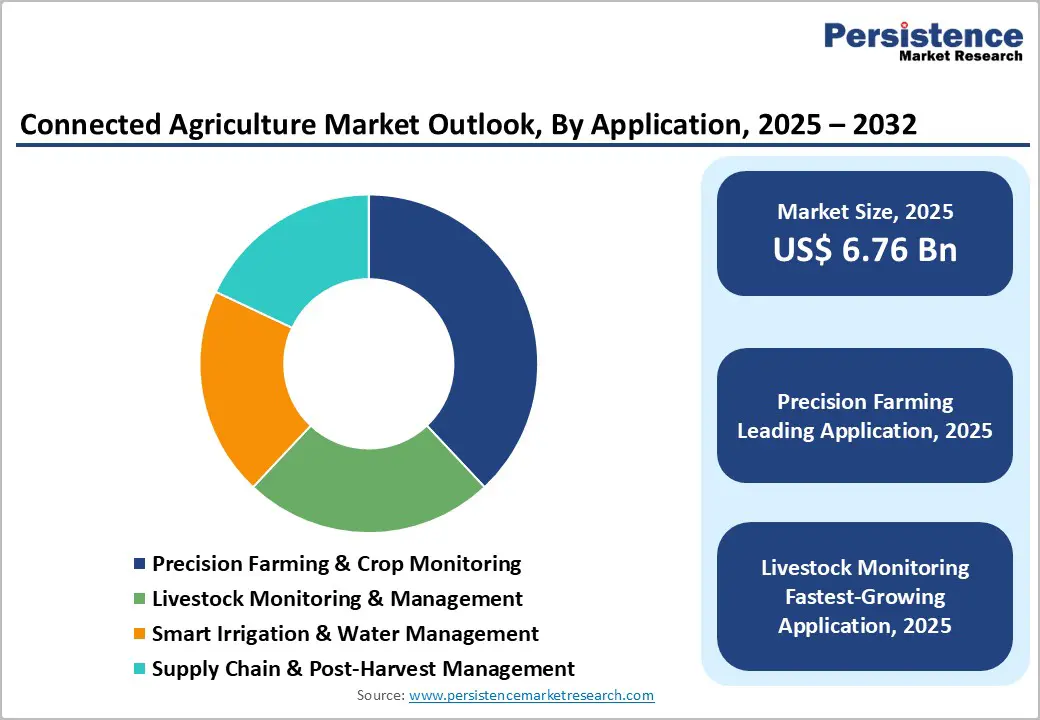

The global connected agriculture market size is likely to be valued at US$ 6.76 billion in 2025, and is projected to reach US$ 20.0 billion by 2032, growing at a CAGR of 16.9% during the forecast period 2025-2032. This expansion is fueled by rising global food demand, increasing pressure to optimize farm productivity and resource efficiency, and the rapid adoption of Internet of Things (IoT) and analytics platforms in agriculture. Elevated connectivity in rural regions and supportive government initiatives are further accelerating market uptake. As farmers and agribusinesses seek to enhance yield, reduce waste, and comply with sustainability goals, the integration of advanced technologies is becoming essential. The market fir connected agriculture solutions is poised for strong growth, driven by digital transformation and the need for smarter and more resilient farming practices.

Key Highlights

- Leading Component: Solutions currently dominate the market by component, while services, including consulting, integration, and maintenance, are expected to record the fastest growth through 2032.

- Leading Technology: IoT devices & smart sensors led the market in 2025 with about 40% revenue share, underpinned by growing adoption of precision agriculture for real-time soil, crop, and environmental monitoring.

- Fastest-Growing Application: Livestock monitoring is anticipated to be the fastest-growing application, expanding at a CAGR of around 24% through 2032, due to an increased demand for traceability and animal health analytics.

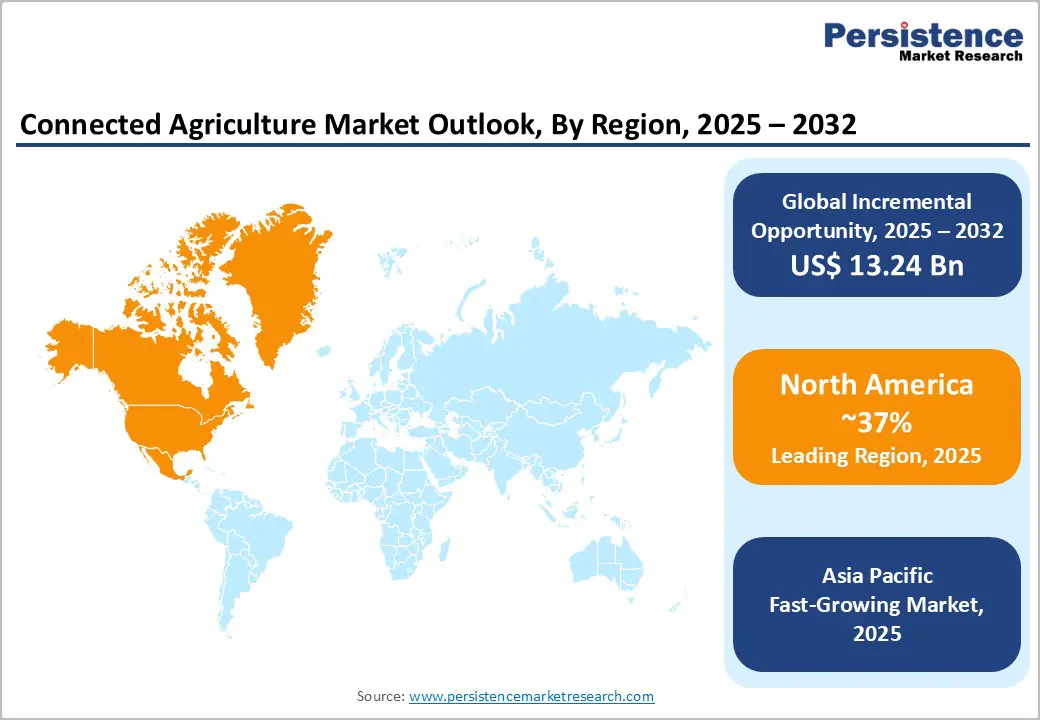

- Dominant Region: North America dominated the market with over 37% share in 2025, supported by advanced connectivity and the strong presence of key players such as Deere & Company and Trimble.

- Fastest-Growing Market: The Asia Pacific market is poised to grow the fastest at over 25% CAGR through 2032, driven by expanding digital agriculture programs in China, India, and ASEAN countries.

- April 2025: Lauritz Knudsen Electrical and Automation launched SMARTCOMM Irrigation Management System (IMS), an IoT-enabled platform for remote farm monitoring, automated irrigation/fertigation, and resource optimization via mobile apps,

| Key Insights | Details |

|---|---|

|

Connected Agriculture Market Size (2025E) |

US$ 6.76 Bn |

|

Market Value Forecast (2032F) |

US$ 20.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

16.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

15% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Food Demand, Technological Innovation, and Policy Support Fueling Market Growth

The global surge in food demand, combined with shrinking arable land, is driving farmers to adopt technology-driven solutions for higher productivity. Connected agriculture, encompassing crop monitoring, livestock tracking, and autonomous machinery, enables increased yields, reduced input costs, and improved resource efficiency. The adoption of imaging technology for precision agriculture is further enhancing real-time crop monitoring and decision-making accuracy, supporting yield optimization and sustainable farming practices.

Advancements in IoT, cloud computing, and analytics, along with strong government support for sustainable and digital farming, are accelerating the adoption of connected agriculture. For example, India’s Ministry of Agriculture & Farmers’ Welfare is investing INR 6,000 crore in the Smart Precision Horticulture Programme, promoting precision farming using AI, IoT, and drones across 15,000 acres to benefit 60,000 farmers. Public policies supporting precision agriculture, resource optimization, and integration across hardware and software ecosystems are positioning connected agriculture as a critical enabler of global food security and sustainable growth.

High Implementation Costs and Connectivity Challenges Hindering Adoption

The adoption of connected agriculture has seen steady progress, but it continues to face significant hurdles due to high initial investment and technical complexity. Deploying IoT devices, sensors, connectivity networks, and integrated software platforms requires substantial capital, making it difficult for small and medium farms to participate. In emerging markets, limited financial resources and low levels of technical awareness further restrict access, resulting in a slow pace of digital transformation across fragmented agricultural sectors. These challenges have created a gap between technological potential and real-world implementation, especially for farmers who stand to benefit most from digital tools.

Persistent issues such as poor rural connectivity and lack of interoperability between various systems also undermine the efficiency of connected agriculture solutions. Inconsistent data transmission, delayed alerts, and fragmented analytics reduce the overall value of these platforms, discouraging wider adoption. To address these barriers, coordinated action among technology vendors, government agencies, and telecommunications providers is essential. Investing in robust infrastructure and developing cost-effective financing or subscription-based models can help bridge the gap, enabling broader participation and accelerating the digital transformation of agriculture.

Expanding Connected Agriculture to Underserved Markets

There is significant growth potential in introducing connect agriculture technologies to underserved regions and smallholder farmers that have not yet adopted such solutions, particularly in areas such as South Asia, Africa, and Latin America. With the help of digital tools such as mobile-based platforms, affordable sensors, and flexible subscription models, agricultural technology (agritech) firms have been expanding into large adjacent markets. From a strategic perspective, scalable Agriculture-as-a-Service (AaaS) models specifically designed for smaller farms have delivered both long-term revenue streams and meaningful social impact. These approaches have enabled farmers to access modern technologies without heavy capital investment, fostering inclusivity across rural economies.

Simultaneously, emerging applications such as smart irrigation systems, market-access platforms, and autonomous agricultural machinery have been accelerating innovation. Increased funding activities have further supported this momentum. For instance, agrifood technology (agrifoodtech) investment in developing economies reached US$ 3.7 billion in 2024, reflecting a 63% year-on-year increase. Additionally, the European Space Agency (ESA) has been funding connected agriculture pilot initiatives by offering up to € 60,000 per contract for satellite-data-enabled services. Such initiatives are strengthening the ecosystem, creating new opportunities for cross-sector partnerships, and paving the way for data-driven, resilient farming systems.

Category-wise Analysis

Component Insights

The solutions segment dominates, capturing around 62% of the connected agriculture market revenue share in 2025. This leadership is due to its central role in enabling farm connectivity through hardware such as sensors and IoT devices, as well as software platforms that support analytics and automation. The widespread adoption of sensor installations, cloud-based dashboards, and imaging technologies for precision agriculture has further strengthened this segment’s position. These tools are directly improving productivity, operational efficiency, and resource management across diverse farming environments, making them indispensable for modern agricultural practices.

The services segment, which holds about 38% of the market revenue share, is experiencing the fastest growth. This rise is fueled by the increasing complexity of connected agriculture systems, which demand expert consulting, seamless integration, and ongoing maintenance. As farmers and agribusinesses adopt multi-vendor platforms, the demand for technical support and lifecycle management services is growing rapidly. These services are generating strong recurring revenue streams and are becoming critical to ensuring the long-term success and scalability of digital agriculture initiatives.

Technology Insights

The IoT devices & smart sensors segment is the leading contributor to the connected agriculture market, capturing approximately 40% of the revenue share in 2025. This dominance is due to the critical function of connected sensors, weather stations, and soil monitors in gathering real-time data for informed farm management. Acting as the backbone of digital agriculture, these technologies facilitate seamless integration with farm-management platforms, empowering farmers to make smarter decisions. Their widespread adoption in developed regions, coupled with affordable deployment initiatives in Asia Pacific supported by government-backed smart farming programs, continues to reinforce their leading position in the market.

The AI, machine learning & predictive analytics segment is likely to be the fastest-growing, expanding at a CAGR of nearly 18% through 2032. This rapid growth is driven by the rising demand for predictive insights that optimize yield, irrigation, and crop health. The integration of robotics, drones, and automation systems further enhances operational efficiency and reduces reliance on manual labor. Meanwhile, advances in connectivity infrastructure such as fifth-generation (5G) networks, low-power wide-area networks (LPWAN), and satellite communication ensure reliable data transmission across rural areas, supporting the smooth operation of all digital farming technologies.

Application Insights

Precision farming holds approximately 38% of the connected agriculture market share, driven by the widespread adoption of GPS-guided machinery, drones, and AI-driven analytics for crop management. This segment’s leadership is due to its demonstrated ability to optimize yields, reduce input waste, and enhance farm-level profitability, particularly among large commercial farms in North America and Europe. The integration of imaging technologies further strengthens its position by enabling more accurate, data-driven decision-making in agriculture. As farmers increasingly seek reliable tools to maximize productivity and sustainability, precision farming continues to set the standard for digital transformation in the sector.

The livestock monitoring segment is anticipated to be the fastest-growing, expanding at a CAGR of nearly 17%. Rising demand for traceability, animal health monitoring, and sustainable dairy and meat production are the primary factors driving this segment’s rapid expansion. At the same time, Smart Irrigation and Market-Access Solutions are gaining momentum as farmers leverage digital tools to optimize water usage and improve price transparency throughout the supply chain. These developments highlight the sector’s shift toward comprehensive, integrated solutions that address both crop and livestock needs, paving the way for a more resilient and efficient agricultural ecosystem.

Regional Insights

North America Connected Agriculture Market Trends

North America holds a leading position in the connected agriculture market, accounting for approximately 37% share. This dominance is driven by the region’s advanced connectivity infrastructure, widespread adoption of precision farming technologies, and a robust ecosystem of key players such as Deere & Company and Trimble Inc. Initiatives like the United States Department of Agriculture (USDA)’s Digital Agriculture Strategy and investments in rural broadband expansion have further accelerated adoption. These efforts support the large-scale integration of IoT, AI, and automation technologies across farms, resulting in improved efficiency and sustainability outcomes for agricultural operations.

Emerging technologies such as autonomous tractors, AI-driven crop analytics, and satellite-based imaging systems are gaining traction in North America, enhancing real-time decision-making and optimizing yields. Agritech firms in the region are also investing in robotics and cloud-based farm-data platforms, reinforcing North America’s role as a global innovation hub for digital agriculture. While market growth remains steady, expansion is maturing due to high penetration rates and advanced adoption levels, signaling a shift toward optimizing existing solutions and driving incremental improvements across the sector.

Europe Connected Agriculture Market Trends

Europe maintains a significant presence in the market for connected agriculture technologies. The prominent position of the region is driven by robust policy support and sustainability objectives outlined in the European Union (EU) Farm to Fork Strategy and Common Agricultural Policy (CAP). The region has witnessed rapid adoption of precision irrigation, data-driven crop management, and traceability systems. Countries such as Germany, France, and the Netherlands have taken the lead through integrated public-private partnerships and smart farming demonstration projects, fostering widespread technological integration across diverse agricultural landscapes.

Emerging technologies in Europe, including IoT-enabled irrigation systems, edge analytics, and the Common European Agricultural Data Space, are enhancing cross-platform data sharing and operational efficiency. The focus on lowering carbon emissions and optimizing resource use has accelerated the implementation of sustainable digital farming practices. While market saturation in Western Europe is moderating near-term expansion, opportunities in emerging Eastern European economies promise continued growth and innovation in the sector.

Asia Pacific Connected Agriculture Market Trends

Asia Pacific is poised to be the fastest-growing market for connected agriculture, expanding at an estimated CAGR of 25% from 2025 to 2032. This rapid growth is fueled by a vast agricultural base, accelerated digitalization, and targeted government initiatives such as India’s Smart Precision Horticulture Programme, China’s Digital Village Strategy, and the 14th Five-Year Plan. These programs prioritize the deployment of 5G-powered agricultural IoT systems, AI-based pest and crop monitoring, and autonomous machinery, laying the foundation for large-scale digital transformation in farming.

Emerging technologies such as AI-based monitoring, drone-enabled imaging, and low-cost sensor platforms are revolutionizing agricultural operations across India, China, and Southeast Asia. Increased venture capital investment and the rise of agritech start-ups are driving the development of mobile and cloud-based platforms tailored for smallholder farmers. Although challenges such as fragmented farms and inconsistent rural connectivity persist, Asia Pacific offers the greatest long-term potential for scalable innovation and sustainable agricultural advancement.

Competitive Landscape

The global connected agriculture market structure is moderately consolidated, with key players such as Deere & Company, Trimble Inc., AG Leader Technology, IBM Corporation, and Topcon Positioning Systems collectively accounting for nearly half of the market share. These companies maintain strong competitive positions through comprehensive hardware–software integration, robust IoT ecosystems, and extensive global distribution networks. Their continued investments in AI-driven analytics, cloud-based farm management platforms, and autonomous equipment are reshaping productivity and sustainability in agriculture. Strategic collaborations with telecom operators and satellite-data providers further enhance connectivity and data insights for end users.

While major players dominate large-scale commercial farming, a dynamic layer of emerging agritech startups and regional vendors is rapidly expanding the competitive frontier. These firms focus on affordable, modular, and mobile-based solutions tailored for smallholder farmers in Asia, Africa, and Latin America. Increasing venture-capital funding, government-backed digital-agriculture initiatives, and the rise of “agriculture-as-a-service” models are creating space for innovation-driven entrants. Overall, the market’s balanced structure, marked by strong incumbents and agile disruptors, promotes continual technology evolution without excessive monopolization, ensuring steady advancement toward smarter, connected, and sustainable farming systems.

Key Industry Developments

- In December 2025, AvironiX Drones unveiled the AviSpray-10c, a compact backpack-sized agricultural spraying drone that is 53% smaller than conventional models and designed to cut costs, complexity, and manpower for precision farming in India. It offers higher spraying efficiency, two-wheeler portability, and a customer success model supported by a national network of trained experts.

- In November 2025, DJI Agriculture made the Agras T100, T70P, and T25P drones commercially available in Europe, Central Asia, and Africa, featuring higher payloads, AI automation, and advanced safety systems such as LiDAR and radar for precision spraying, spreading, and lifting. Showcased at Agritechnica 2025 in Hannover, these models target large-scale, mid-sized, and solo operations to boost sustainable farming efficiency.

- In September 2025, CIMMYT and the Borlaug Institute for South Asia (BISA) launched the Atlas of Climate Adaptation in South Asian Agriculture (ACASA), the region's first web-based platform assessing high-resolution climate risks for 15 crops and six livestock species across India, Bangladesh, Nepal, and Sri Lanka. Co-developed with partners such as the Indian Council of Agricultural Research (ICAR) and supported by the Gates Foundation, it provides expert-validated adaptation strategies, downloadable data, and tools to attract climate finance for smallholders facing floods, heat, and droughts.

Companies Covered in Connected Agriculture Market

• Deere & Company

• Trimble Inc.

• AGCO Corporation

• BASF SE

• Bayer AG

• Hexagon AB

• SAP SE

• Topcon Corporation

• Kubota Corporation

• XAG Co., Ltd.

Frequently Asked Questions

The global connected agriculture market is projected to reach US$ 6.76 billion in 2025.

Key growth drivers include rising global food demand, pressure on arable land, technological advancements in IoT and analytics, and government-backed initiatives promoting precision and sustainable agriculture.

The market is poised to witness a CAGR of 16.9% from 2025 to 2032.

Opportunities lie in emerging markets across the Asia Pacific, Africa, and Latin America, where smallholder farms are embracing mobile-based solutions, and in AI-driven predictive agriculture, autonomous farming, and agriculture-as-a-service (AaaS) business models.

Some of the leading companies in the market include Deere & Company, Trimble Inc., AGCO Corporation, BASF SE, Bayer AG, and Hexagon AB.