- Agrochemicals

- Agrochemicals Market

Agrochemicals Market Size, Share, and Growth Forecast, 2026 - 2033

Agrochemicals Market by Product Type (Fertilisers, Pesticides, Others (Soil Conditioners, acidifying agents)), Crop Type (Cereals, Pulses and Oilseeds, Fruits and Vegetables, Lawns and Turfs, Others), Application (Crop Protection, Crop Nutrition), and Regional Analysis for 2026 - 2033

Agrochemicals Market Size and Trends Analysis

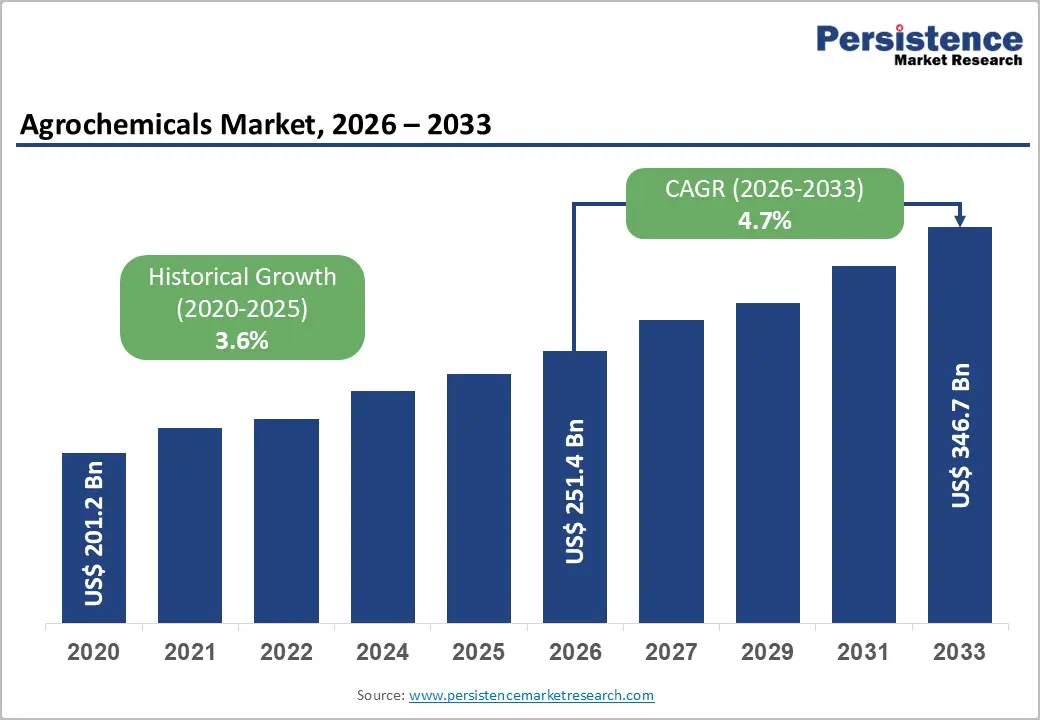

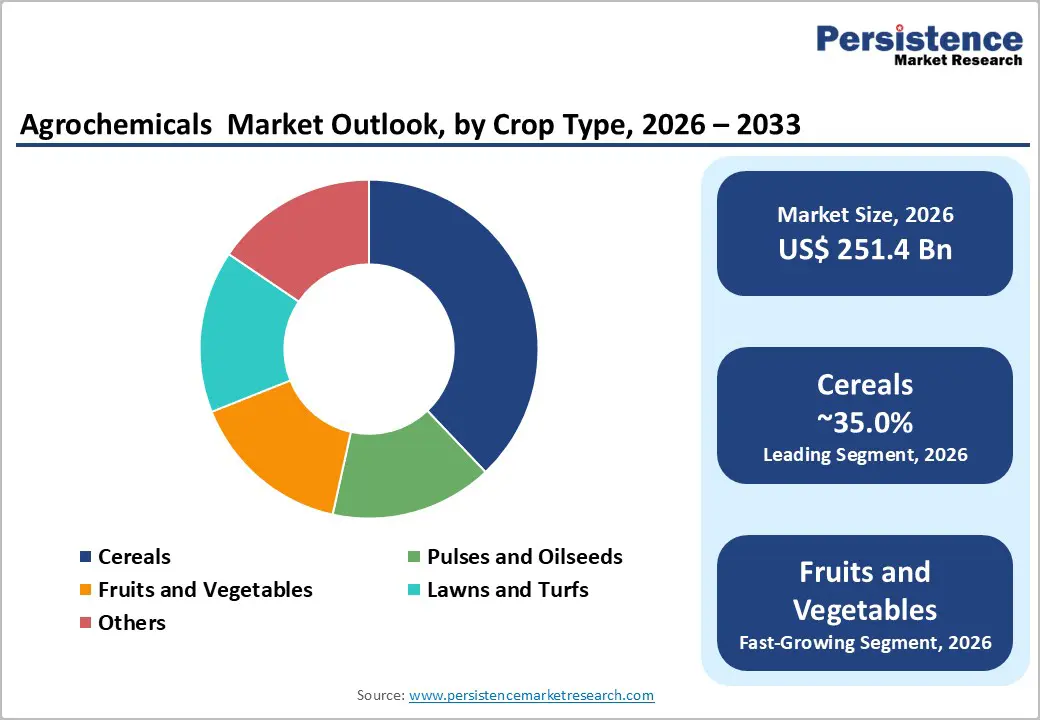

The global agrochemicals market size is likely to be valued at US$ 251.4 billion in 2026 and is projected to reach US$ 346.7 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

This steady expansion reflects the fundamental role of agrochemicals in addressing critical challenges posed by population growth, declining arable land, and the global imperative to enhance crop productivity. The market operates across three primary dimensions: crop protection chemicals, crop nutrition solutions, and emerging biological alternatives, each addressing distinct farmer needs while adapting to increasingly stringent regulatory frameworks.

Enhanced by technological advancements, government policy support in emerging markets, and the transition toward sustainable agricultural inputs, the agrochemicals market remains structurally resilient despite cyclical commodity price pressures and shifting environmental compliance requirements across regions.

Key Industry Highlights:

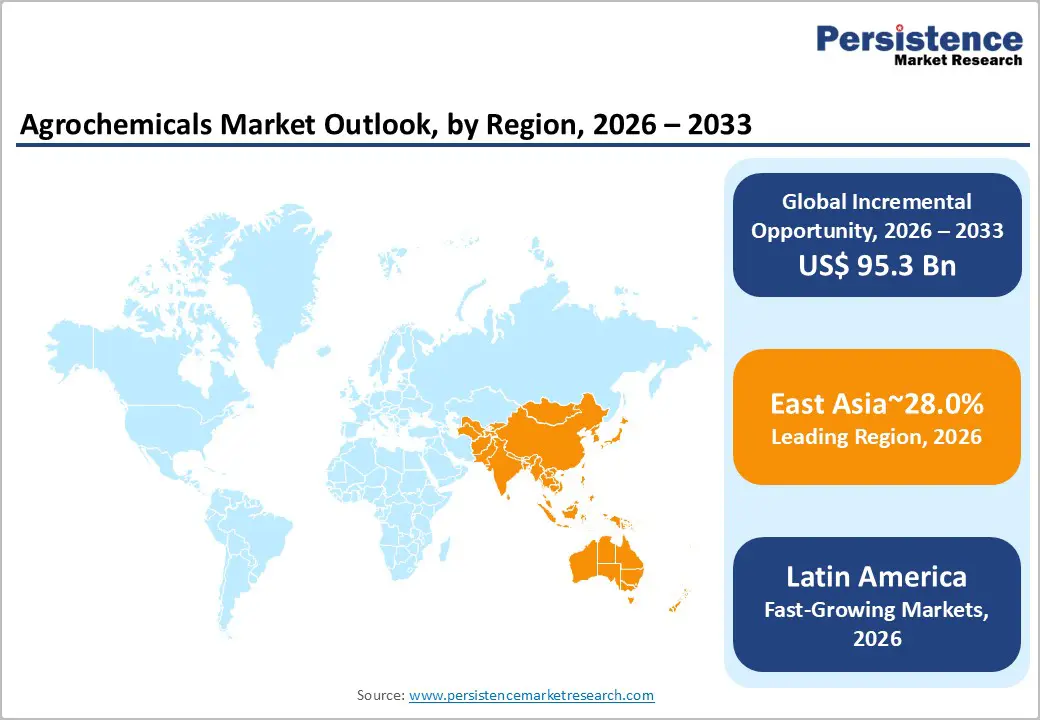

- Regional Leadership: East Asia leads the global Agrochemicals market with a 28% share, driven by China and India’s large agricultural bases, food-security policies, and high consumption of fertilizers and crop protection chemicals.

- Fast-Growing Markets: Latin America is among the fastest-growing regions, driven by large-scale cultivation of soybeans, corn, sugarcane, and coffee, multi-cropping systems, and export-oriented agriculture, particularly in Brazil and Argentina.

- Leading Product: Fertilizers dominate the market with 47% share, reflecting their essential role in cereal production, yield maximisation, and government-backed nutrient management programs.

- Fastest-Growing Product: Pesticides are the fastest-growing segment, driven by increasing pest resistance, climate-induced crop stress, and adoption of integrated pest management practices.

- Leading Application: Cereals account for 35% of agrochemical consumption, anchored in global food security needs and extensive cultivation of wheat, rice, and maize.

| Key Insights | Details |

|---|---|

| Agrochemicals Market Size (2026E) | US$ 251.4 Bn |

| Market Value Forecast (2033F) | US$ 346.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Dynamics

Drivers - Global Food Security Imperative and Population Pressures

The trajectory of the global agrochemicals market is fundamentally anchored to the escalating demand for food production driven by projected global population growth and urbanisation. The Food and Agriculture Organisation projects that global food production must increase by approximately 50% by 2050 to accommodate population growth and shifting dietary patterns, with plant-based products accounting for 80% of this incremental demand. Concurrently, annual crop losses attributable to pests, diseases, and abiotic stress exceed 40% globally, resulting in economic losses exceeding US$220 billion annually.

India's population alone reached 1.4 billion in 2023, creating an estimated requirement for food grain production to reach approximately 300 million tonnes by 2025 to ensure nutritional security. These demographic realities compel intensive agricultural systems in which fertilizers, pesticides, and crop protection chemicals function as essential technologies for extracting maximum yields from constrained agricultural land.

The response to this pressure through expanded fertiliser consumption in cereal production accounts for 35 percent of applications, while simultaneously supporting rapid productivity improvements in high-value crops that require intensive input regimes.

Regulatory Mandate for Sustainable Agriculture and Chemical Reduction

The European Green Deal and its subordinate Farm to Fork Strategy represent transformative regulatory shifts that fundamentally reshape the Global Agrochemicals Market trajectory. The EU targets a 50 percent reduction in overall chemical pesticide use and risk by 2030, coupled with achieving 25 percent of agricultural land under organic farming systems by the same target date.

These policy frameworks have already produced measurable market effects: pesticide consumption across the EU declined to approximately 292,000 tonnes in 2023, the lowest level since 2011, reflecting a deliberate transition toward integrated pest management and biological alternatives. Beyond Europe, regulatory pressures are driving technological differentiation within the global market.

In 2024, the EU's Safe and Sustainable by Design (SSbD) framework began embedding holistic lifecycle sustainability criteria into plant protection product development, creating innovation incentives for manufacturers to advance beyond conventional chemical formulations. India's government subsidy rationalisation program accelerates the adoption of biofertilisers and bio-inputs, contributing approximately 1.8% points to the projected CAGR of India's domestic agrochemicals market through 2030.

These regulatory transitions ensure that the global agrochemicals market is not merely growing in absolute terms but is simultaneously evolving in compositional quality, shifting from indiscriminate chemical inputs toward targeted, sustainable, and environmentally compliant solutions.

Technology-Enabled Precision Agriculture and Adaptive Farming Systems

Technological advancement represents a critical inflexion point in the global agrochemicals market, specifically through the integration of digital agriculture, artificial intelligence, and data-driven agronomic decision-making. Bayer's Climate FieldView™ Plus platform, combined with advanced seed traits and predictive analytics, exemplifies how agrochemical application has evolved from volumetric application toward precision targeting, reducing input costs while enhancing environmental performance.

Drone-based precision spraying technologies unlock untapped smallholder farmer segments in North India and Western states, contributing approximately 0.9 percentage points to the CAGR of the agrochemicals market over medium-term adoption cycles.

IoT sensors, soil monitoring systems, and machine-learning algorithms enable farmers to optimise input timing and dosage, maximising return on agrochemical investments while reducing environmental externalities. These technological advances fundamentally enhance the value proposition of the Global Agrochemicals Market by transforming commodity inputs into integrated technology solutions that command premium prices and deliver quantifiable yield and efficiency gains.

Restraint - Cost Pressures and Input Volatility

Rising production costs, driven by geopolitical supply chain disruptions and energy price volatility, create structural headwinds for the agrochemicals sector. BASF's decision to cease glufosinate-ammonium production at its European facilities by the end of 2024/2025 exemplifies the cost pressures that are forcing consolidation in commodity chemical production. Raw material inflation, particularly in nitrogen fertilizer production, where natural gas costs constitute 70-80 percent of production expenses, constrains manufacturer margins and creates pricing pressures that limit farmer accessibility in price-sensitive emerging markets. The agrochemicals market experiences demand elasticity with respect to input costs, particularly among smallholder farmers in India and Sub-Saharan Africa, where agrochemical expenditures represent 15-25 percent of total cultivation costs.

Opportunity - Low-Carbon Ammonia Production and Regenerative Agriculture Integration

The transition toward low-carbon ammonia production represents a transformational opportunity for the fertiliser segment of the Agrochemicals Market. Current ammonia production, reliant on fossil fuels, produces 450-500 million tonnes of CO2 equivalents annually, a substantial portion of agricultural emissions. Green ammonia production via water electrolysis powered by renewable electricity offers a pathway toward 65-81% emission reductions relative to conventional methods, aligning fertilizer production with net-zero targets and carbon-pricing regimes increasingly prevalent in developed markets.

Air Products' December 2025 partnerships with Yara International (the Louisiana Clean Energy Complex targeting 2.8 million tonnes annually of low-carbon ammonia; the NEOM Green Hydrogen Project targeting 1.2 million tonnes annually in Saudi Arabia) demonstrate the commercial-scale deployment of renewable ammonia production, translating regulatory pressure into capital allocation and supply-chain transformation.

This transition creates a market segmentation opportunity: low-carbon fertilisers command substantial price premiums within sustainability-certified supply chains, carbon-conscious retailers, and supply chains subject to EU Carbon Border Adjustment Mechanism (CBAM) pricing. BASF's November 2025 announcement of its planned Agricultural Solutions IPO explicitly cites sustainable crop protection and nutrient solutions as core growth drivers, signalling institutional recognition that sustainable agrochemical positioning commands higher valuation multiples than commodity-focused competitors.

Bayer's August 2024 Crop Science Vision and March 2025 portfolio integration of seed traits, biotechnology, and digital tools demonstrates strategic convergence: companies combining agrochemical inputs with digital precision-agriculture platforms, regenerative farming incentive programs, and carbon accounting mechanisms create integrated value propositions commanding premium positioning and customer loyalty relative to commodity agrochemical suppliers.

These integrated offerings, combining low-carbon fertilizers with digital monitoring, regenerative agriculture subsidies, and carbon credit mechanisms, represent the frontier of Agrochemicals Market evolution, translating sustainability mandates into commercial differentiation and margin expansion opportunities.

Biological Agrochemicals and Alternative Crop Protection Paradigm

The agricultural biologicals market represents a high-growth derivative opportunity within the broader agrochemical ecosystem. Microbial-based products, encompassing Bacillus thuringiensis (Bt) bioinsecticides, arbuscular mycorrhizal fungi, and Trichoderma-based biocontrol agents, command accelerating adoption among farmers prioritising organic certification compliance and sustainability credentials.

Syngenta's acquisition of Novartis' natural products and genetic strains, combined with the inauguration of its world-scale biologicals production facility in South Carolina, reflects strategic capital deployment toward this high-margin, regulatory-advantaged segment. India demonstrates exceptional biological potential with a projected 9.0 percent CAGR through 2035, driven by government biofertilizer promotion programs and farmer demand for sustainable solutions compatible with smallholder economic constraints.

The biologicals segment compounds the agrochemicals market opportunity through premium pricing power around 40-60 percent above conventional chemical inputs, regulatory tailwinds in developed markets, and farmer preference migration toward integrated pest management protocols that combine biological and chemical inputs for optimal efficacy and environmental stewardship.

Category-wise Analysis

Product Type Insights

Fertilizers hold a dominant position in the global agrochemicals market, accounting for 47% of total market value in 2026 and serving as the foundational input category driving agricultural productivity. Nitrogen-based fertilizers, phosphatic compounds, and potassium-derived products collectively address crop nutrient deficiencies across commodity and specialty crop production systems.

The segment reflects sustained demand underpinned by government procurement programs in India that establish price floors and incentivise farmer adoption, ensuring input demand resilience across commodity price cycles. Emerging biofertilizer technologies incorporating mycorrhizal associations, nitrogen-fixing bacterial consortia, and humic substance complexes enhance the fertiliser segment's growth trajectory by enabling partial substitution of synthetic inputs while maintaining yield targets.

Mechanistic advantages include improved nutrient bioavailability, enhanced soil organic matter accumulation, and reduced leaching losses, thereby addressing environmental concerns in intensive agricultural systems. Pesticides constitute the fastest-growing product category in the global agrochemicals market, driven by intensifying pest and disease pressure resulting from climate variability, expanding agricultural trade routes that facilitate pathogen dispersion, and farmers' adoption of integrated pest management protocols that combine chemical and biological control mechanisms.

Industry Insights

Cereals and grains account for the largest share of the global agrochemicals market, representing 35% of segment value, reflecting their dominance in global agricultural land use and food security priorities. Wheat, rice, and maize collectively account for approximately 65 percent of global cereal production and constitute dietary staples for populations across Asia, Africa, and Latin America, where nutritional dependence on grain-based carbohydrates remains structurally entrenched.

Agrochemical intensity in cereal production remains relatively stable, constrained by farmers' economic conditions in smallholder-dominated systems and by price-sensitive commodity markets, where input costs fundamentally limit profitability. Fertilizer consumption intensity in cereal production supports volume stability: India's leading consumption states, Maharashtra, Andhra Pradesh, and Telangana, demonstrate persistent demand despite commodity price deflation, attributable to government procurement programs that insulate farmers' revenues and support input expenditure levels.

Fruits and vegetables represent the fastest-expanding crop category within the Global Agrochemicals Market segmentation, driven by urbanization-linked dietary preference shifts toward nutritious, fresh produce among emerging market populations and developed market consumers prioritising health attributes over calorie density.

Regional Insights

North America Agrochemicals Market Trends

North America accounts for 18% of the global agrochemicals market, a mature, technology-intensive market characterized by high agrochemical adoption, regulatory sophistication, and advanced application methodologies.

North America is an established, mature agrochemicals market characterized by advanced agricultural infrastructure, high capital intensity, and a premium position in sustainable and precision input solutions. The region's agricultural sector encompasses approximately 375 million acres of farmland across the United States and Canada, supporting corn, soybean, wheat, and specialty crop production systems that collectively demand high-performance crop protection and nutrition inputs.

The U.S. agrochemicals market demonstrates sophisticated adoption by farmers of variable-rate application technologies, soil-specific nutrient management protocols, and integrated pest management systems that optimize input efficiency and environmental stewardship. Digital agriculture penetration in North America, driven by John Deere's precision agriculture ecosystems, Climate FieldView™ platforms, and agronomic advisory services, positions U.S. farmers to apply inputs with unprecedented precision, reducing volumes while enhancing efficacy and environmental compliance.

The North American market reflects structural price stability through diversified crop production systems, policy support mechanisms, and farmer technology adoption rates that sustain input demand across commodity price cycles, positioning the region as a stable, margin-accretive contributor to global agrochemical manufacturer portfolios.

East Asia Agrochemicals Market Trends

East Asia commands 28% of the global agrochemicals market, reflecting the region's position as the world's largest agricultural producer and consumer of agrochemical inputs. The region dominates global agrochemical consumption, accounting for 28 percent of the market, driven by the combined agricultural production scale, population density, and government prioritisation of food security in China and India. China remains the world's largest exporter and manufacturer of pesticide active ingredients, with production capacity spanning herbicides, insecticides, fungicides, and specialty formulations that supply both domestic and global distribution channels.

Government policy support in East Asian markets accelerates agrochemical consumption through subsidy programs, research collaborations with agricultural universities, and extension services that promote the adoption of improved agrochemical technologies among farmers.

Latin America Agrochemicals Market Trends

Latin America represents a high-growth agrochemicals market characterised by large-scale commodity production, export-oriented agricultural systems, and intensive input requirements for soybean, coffee, sugarcane, and grain production.

Brazil dominates the region's agrochemical consumption, supporting the world's largest soybean export volumes and substantial production of corn, sugarcane, and specialty crops across diverse agroecological zones. Agricultural land availability in Brazil and Argentina creates competitive cost structures that support agrochemical-intensive production systems, enabling farmers to maintain commodity export competitiveness despite cyclical price pressures.

Favourable climatic conditions that enable year-round production in Brazil support multiple cropping cycles within a single growing season, resulting in greater agrochemical demand than in temperate agricultural systems with single annual production cycles.

Competitive Landscape

The global agrochemicals market is moderately consolidated with oligopolistic characteristics, dominated by a small group of multinational companies that command strong control overactive ingredient innovation, intellectual property, and global distribution networks. Leading players such as Syngenta Group, Bayer CropScience, BASF SE, Corteva Agriscience, FMC Corporation, and UPL Limited collectively account for a significant share of global revenues.

These companies benefit from scale-driven R&D capabilities, vertically integrated manufacturing, and broad crop- and region-specific product portfolios. High regulatory barriers, long product development cycles, and rising compliance costs further reinforce the dominance of established players.

Key Industry Developments

- December 2025 - Air Products & Yara International: Air Products and Yara International entered advanced negotiations to collaborate on low-emission ammonia projects, including the Louisiana Clean Energy Complex (U.S.) and the NEOM Green Hydrogen Project (Saudi Arabia). The partnership aims to produce 2.8 million tonnes per year of low-carbon ammonia in the U.S. and up to 1.2 million tonnes of renewable ammonia in Saudi Arabia, leveraging Air Products’ low-emission hydrogen and Yara’s global ammonia distribution network. This initiative positions Yara to supply more environmentally sustainable ammonia for fertilisers, supporting decarbonization in the agrochemicals market while meeting growing global demand for low-emission crop nutrition solutions.

- March 2025 - Bayer: Bayer expanded its crop science portfolio by integrating advanced seed traits, biotechnology, and data-driven digital tools to enhance sustainable farming. Through innovations like drought-tolerant hybrids, Bollgard® cotton traits, and predictive analytics via Climate FieldView™, the company provides farmers with precise crop protection, optimised inputs, and resilience against pests, diseases, and environmental stresses. This development strengthens Bayer’s position in the agrochemicals market by combining digital agriculture, advanced seed technologies, and environmentally sustainable crop protection solutions.

Companies Covered in Agrochemicals Market

- Bayer AG

- YARA International ASA

- BASF SE

- Israel Chemicals Ltd.

- Nutrien Ltd.

- FMC Corporation

- The Mosaic Company

- Fengro Industries Corp.

- PhosAgro

- DowDuPont Inc.

- OCI N.V.

- Fertilizantes Heringer S.A.

- WinHarvest Pty Ltd

- Syngenta AG

- K+S KALI GmbH

- Saudi Arabia Fertilizer Company (SAFCO)

- Jordan Abyad Fertilizers and Chemicals Company

- UPL Limited

- Coromandel International.

Frequently Asked Questions

The global agrochemicals market is projected to be valued at US$ 251.4 Bn in 2026.

The Fertilisers segment is expected to account for approximately 47% of the Global Agrochemicals Market by Technology Type in 2026.

The market is expected to witness a CAGR of 4.7% from 2026 to 2033.

Agrochemicals market growth is driven by rising global food demand from population pressure, the need to reduce crop losses, regulatory-led shifts toward sustainable inputs, and the adoption of precision agriculture technologies that improve yield efficiency and input optimization.

Key opportunities in the Agrochemicals Market lie in scaling low-carbon fertilizers integrated with regenerative and digital agriculture platforms, and in the rapid expansion of high-margin biological agrochemicals driven by sustainability regulations, premium pricing potential, and farmer adoption of integrated pest management.

Key players in the Agrochemicals Market include Syngenta Group, Bayer CropScience, BASF SE, Corteva Agriscience, FMC Corporation, and UPL Limited.