ID: PMRREP16030| 160 Pages | 20 Jun 2025 | Format: PDF, Excel, PPT* | Healthcare

The UK Private Healthcare Market is likely to be valued at US$ 14.3 Bn in 2025 and is estimated to reach US$ 18.1 Bn by 2032, growing at a CAGR of 3.4% during the forecast period from 2025 to 2032.

The UK private healthcare market is expanding due to rising demand for outpatient care services, a shift toward more flexible and accessible healthcare options, and growing out-of-pocket spending. Rising NHS wait times have driven a 30% surge in Priory Group inquiries and admissions (2022–2023), expanding beyond residential care to outpatient services such as counselling and therapy. Meanwhile, private mental health insurance policies grew by 20% (Association of British Insurers, 2025), reflecting a shift toward faster, personalized care.

Key Highlights:

|

Market Attributes |

Key Insights |

|

Private Healthcare Market Size (2025E) |

US$ 14.3 Bn |

|

Market Value Forecast (2032F) |

US$ 18.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.6% |

The UK private healthcare market is experiencing robust growth driven by mounting NHS pressures, especially long waiting lists and limited capacity post-pandemic. A notable rise in self-pay patients opting for non-urgent elective procedures has emerged, aided by private hospitals offering transparent package pricing and fixed consultant fees.

National Health Service (NHS) GP referrals to private providers are increasing, supported by the NHS e-Referrals system, which empowers patients to choose their preferred care facility. Trusts' spending on outsourced private care nearly doubled from £1.66 billion in 2019/20 to £3.12 billion in 2022/23, reflecting the urgent need to address backlogs (Nuffield Trust, 2024).

Planned NHS patient admissions in private hospitals rose from 5.6% pre-pandemic to 7.5% in 2022/23. Meanwhile, self-funded admissions surged across the UK, with out-of-pocket care rising 32% since 2019. Additionally, privately insured admissions are climbing as employers and individuals adjust to ongoing NHS delays, signaling a structural shift toward mixed public-private healthcare provision across the UK.

Recent strategic collaborations in 2024 further reflect growing investment and innovation in private healthcare delivery, enhancing service accessibility, patient guidance, and international collaboration in the UK’s evolving healthcare landscape. For instance, Aclarion, Inc. extended its commercial agreement with The London Clinic in June 2024 to enhance chronic low back pain services. GenesisCare partnered with Ramsay Health Care in May 2024 to launch a new radiation therapy service at Peninsula Private Hospital, strengthening cancer care within a local network.

The UK private healthcare market faces several restraints that may impact its medium-term expansion. Despite rising NHS waiting times, less than a quarter of the population is willing to pay for private care or insurance, limiting market expansion.

Geographic disparities further restrict access, with private facilities concentrated in affluent urban areas, leaving rural and disadvantaged regions underserved. The sector is highly fragmented, with many providers competing for a relatively small patient base, which exerts downward pressure on pricing and profitability. Aggressive discounting and promotional offers erode profit margins, making it difficult for providers to sustain high-quality care or invest in innovation. This price competition leads to cost-cutting that affects patient outcomes and staff morale. Providers also face rising marketing and branding costs to differentiate themselves, further squeezing finances, especially for smaller players.

Additionally, the UK Government has unveiled plans to open 13 new community diagnostic centres (CDCs) nationwide to leverage the independent sector and alleviate NHS waiting lists. In Southwest England, five independent sector-led CDCs were established in Bristol, Redruth, Yeovil, Torbay, and Weston-super-Mare in 2024. Further expansions are planned for Southend, Northampton, and South Birmingham, increasing competition and putting further pressure on private healthcare providers, challenging private providers to maintain market share amid NHS efforts to reduce waiting lists.

The UK private healthcare market presents strong growth opportunities driven by NHS capacity constraints, shifting patient preferences, and digital transformation. In 2023, private hospital admissions reached a record 898,000 a 7% increase year-on-year surpassing pre-pandemic levels (Private Healthcare Information Network (PHIN), 2024). Moreover, the NHS waiting lines for the consultant-led elective care reached 7.46 million by the end of December 2024 (British Medical Association 2025). This rise reflects the growing number of patients not receiving treatment within the NHS’s 18-week target, creating a significant gap, and private providers are increasingly positioned to fill.

Notable opportunity lies in the adoption of private healthcare by the younger demographic, with admissions among those aged 20–39 growing by 13% in Q1 2024, indicating a trend toward early and proactive healthcare consumption. Furthermore, the expansion of private medical insurance (PMI) with a 6% rise in insured admissions in early 2024 suggests increasing affordability and accessibility for wider segments of the population. These trends offer private healthcare providers a chance to expand reach, innovate service delivery, and play a complementary role alongside the NHS.

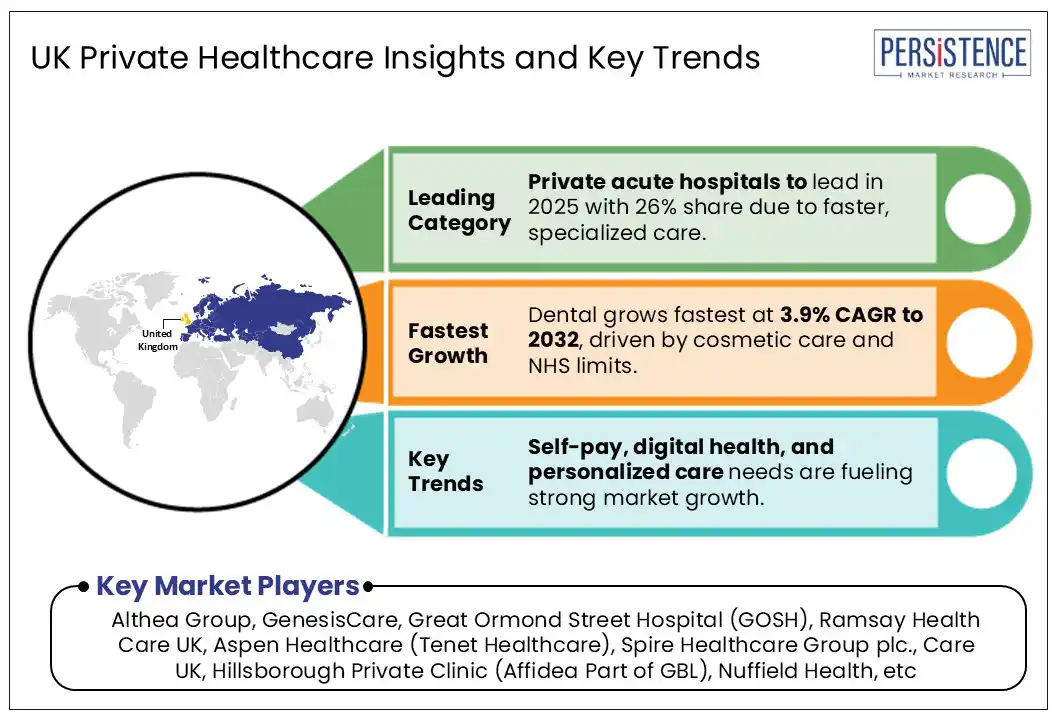

The private acute care hospitals segment is set to dominate the UK private healthcare market in 2025 and is likely to maintain its dominance in the forthcoming years, recording a positive CAGR during the forecast period . This growth is driven by increasing demand for timely, specialized, and high-quality treatment, particularly in areas where public health systems are strained. Acute care hospitals offer a range of services, including surgical procedures, emergency care, and complex diagnostics, which are attracting patients seeking faster access and advanced facilities.

Rising incidences of chronic diseases, an ageing global population, and a shift toward value-based, patient-centric care models are further fuelling demand. These hospitals are investing in cutting-edge medical technologies and integrated digital systems to improve outcomes and operational efficiency. As healthcare needs become more complex and time-sensitive, private acute care hospitals are well-positioned to capture growing patient volumes and expand their footprint.

Trauma and orthopaedics, together with the 'Others' category which includes specialties such as gastroenterology, neurology, ophthalmology, ENT, dermatology, and plastic surgery-are poised to capture nearly half of the UK private healthcare market share in 2025. This growth is driven by rising patient awareness, increased demand for specialist consultations, and long NHS wait times for non-urgent but quality-of-life-impacting procedures.

The Private Healthcare Information Network (PHIN), 2024 report highlights the private sector’s top 10 procedures by volume in the first quarter of 2024, which includes cataract surgery, chemotherapy, upper gastrointestinal endoscopy, colonoscopy, hip replacement, and knee arthroscopy. This indicates strong and sustained demand for these services in the private sector, reflecting a growing shift towards private care for specialist procedures, positioning these segments for continued expansion in the coming years. Furthermore, these specialties also benefit from greater adaptability to outpatient or day-case models, making them cost-effective and attractive to both patients and providers.

The UK private healthcare market is highly competitive and fragmented, comprising a mix of large hospital groups, independent clinics, specialty providers, and digital health platforms. Key players offer a wide range of services from acute care to diagnostics and specialist procedures. These providers compete through service innovation, digital integration, strategic partnerships, and major acquisitions to enhance patient care and market reach.

The UK private healthcare market is set to reach US$ 14.3 Bn in 2025.

The market is projected to record a CAGR of 3.4% during the forecast period from 2025 to 2032.

Growing self-pay patients, NHS waiting list pressures, advancements in medical technology, rising chronic diseases, and increasing demand for personalized, convenient care is driving the UK private healthcare market.

Althea Group, GenesisCare, Great Ormond Street Hospital (GOSH), Ramsay Health Care UK, Aspen Healthcare (Tenet Healthcare), Spire Healthcare Group plc., Care UK, Hillsborough Private Clinic (Affidea Part of GBL), Nuffield Health are a few leading players.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Mn/Bn |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Service Type

By Application

By End-user

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author