- Pharmaceuticals

- Acute Myeloid Leukemia Treatment Market

Acute Myeloid Leukemia Treatment Market Size, Share and Growth Forecast for 2025 - 2032

Acute Myeloid Leukemia Treatment Market By Disease (Myeloblastic Leukemia, Myelomonocytic Leukemia, Others), Treatment (Chemotherapy, Targeted Therapy, Others), Route of Administration (Parenteral, Oral), and Regional Analysis for 2025 - 2032

Acute Myeloid Leukemia Treatment Market Share and Trends Analysis

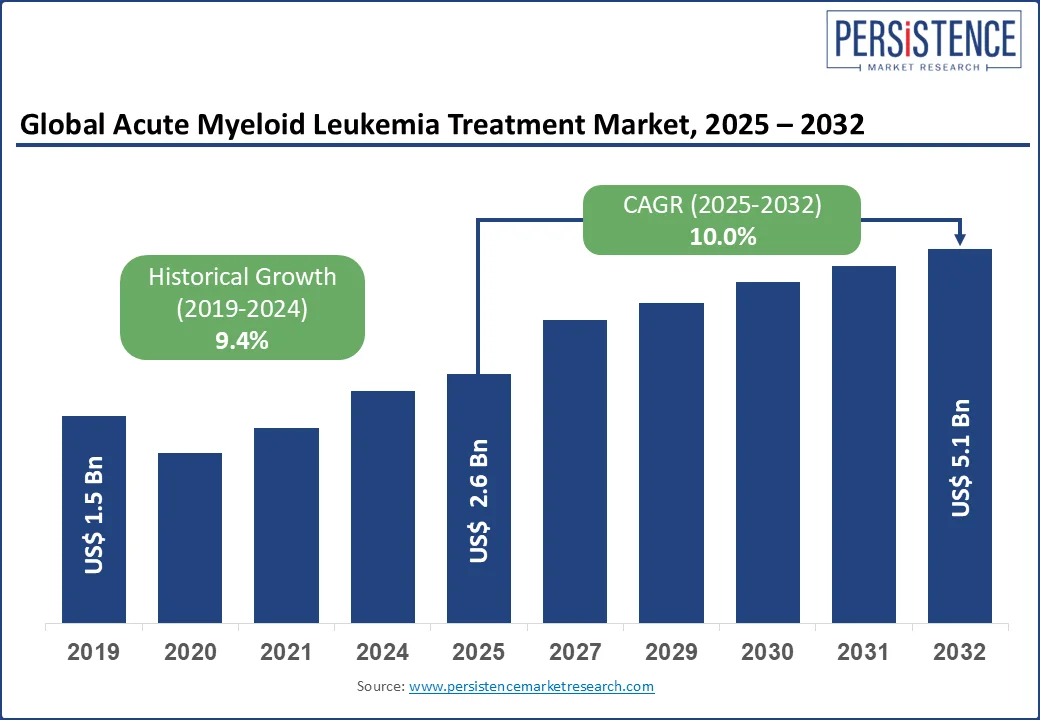

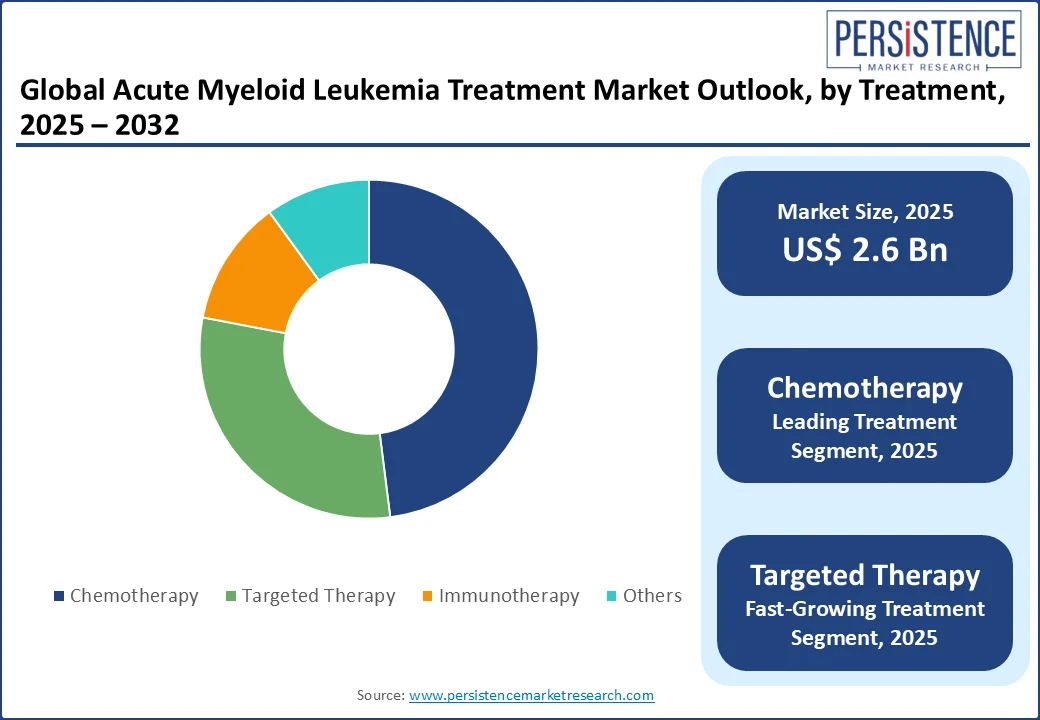

The global acute myeloid leukemia treatment market size is likely to be valued at US$ 2.6 Bn in 2025 and is estimated to reach US$ 5.1 Bn in 2032, growing at a CAGR of 10.0% during the forecast period 2025 - 2032. The acute myeloid leukemia treatment market growth is driven by the growing emphasis on precision medicine and the tailoring of treatments based on individual genetic profiles to improve outcomes.

Key Industry Highlights

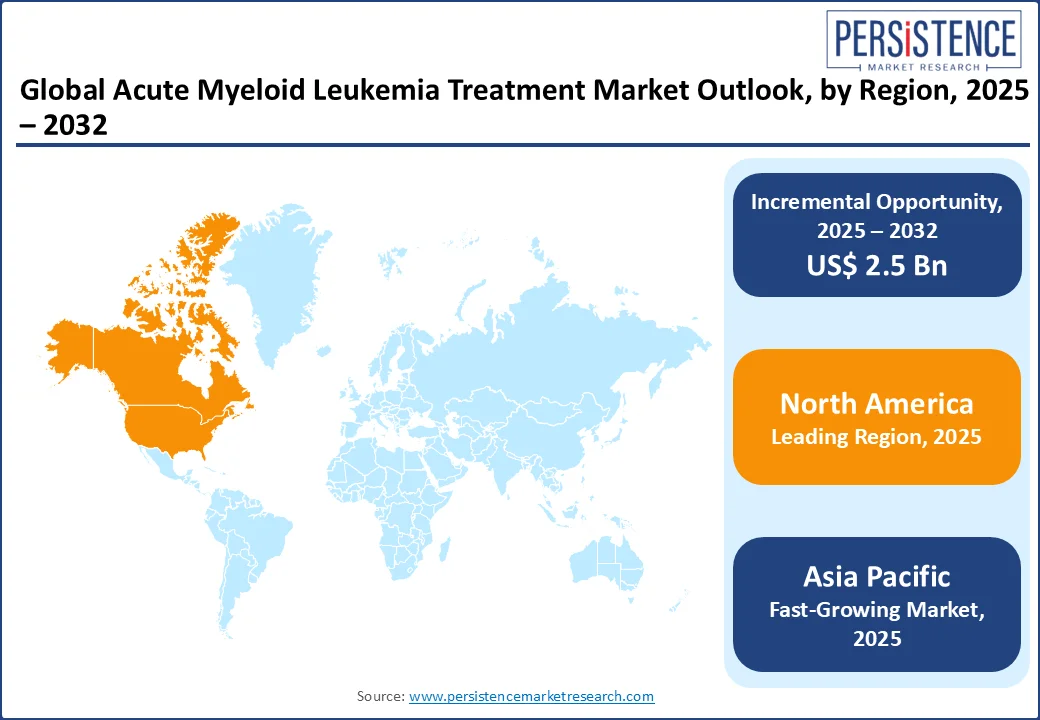

- Leading Region: North America held nearly 38.2% share in the acute myeloid leukemia treatment market driven by FDA-approved therapies and high AML incidence rates.

- Fastest-growing region: Europe is a vital region, contributing 25.6%, supported by an aging population and advanced clinical research networks.

- Advances in Targeted Therapies and Immunotherapies: Targeted therapies and immunotherapies are gaining traction, with FLT3 inhibitors approved for molecularly defined AML subtypes.

- Challenges in Early Diagnosis: Disease heterogeneity hampers early diagnosis, leading to late-stage treatments and impacting the overall therapeutic outcomes.

- Future Growth in Combination Regimens: Ongoing trials for combination regimens offer future growth, especially in high-risk or refractory AML patients.

|

Market Attribute |

Key Insights |

|

Acute Myeloid Leukemia Treatment Market Size (2025E) |

US$ 2.6 Bn |

|

Projected Market Value (2032F) |

US$ 5.1 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

10.0% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

9.4% |

Market Dynamics

Driver - Advancements in Targeted Therapies and Immunotherapies

Advancements in targeted therapies and immunotherapies are reshaping the Acute Myeloid Leukemia (AML) treatment landscape, supported by robust clinical and government-backed data. The FDA has approved several targeted agents since 2017, including FLT3 inhibitors (midostaurin and gilteritinib), IDH inhibitors (ivosidenib and enasidenib), BCL-2 inhibitor (venetoclax), and antibody–drug conjugate (gemtuzumab ozogamicin), which have significantly improved the outcomes; for instance, chemotherapy plus midostaurin extended median overall survival from 25.6 to 74.7 months in FLT3-mutated AML.

The NIH’s NCI launched the precision medicine trial myeloMATCH in late 2024 to match AML patients to genetically targeted treatments, enrolling thousands across U.S. and Canadian centers. In immunotherapy, immune checkpoint inhibitors such as nivolumab, when combined with azacitidine, have produced response rates of 47% among elderly or relapsed patients, with median overall survival exceeding 13 months in some studies. Meanwhile, early CAR T cell therapies such as KITE 222, targeting antigens present in up to 90% of AML cases, have received FDA orphan drug designations and shown promising remission rates in phase I trials. These innovations reflect a shift toward personalized, mutation-specific, and immune-based treatments in AML.

Restraint - Challenges in Early Diagnosis and Disease Heterogeneity

The early diagnosis of Acute Myeloid Leukemia (AML) is hampered by both rapid symptom onset and profound disease heterogeneity, posing major restraints on effective treatment initiation. Typical AML symptoms such as fatigue, fever, or bruising, emerge over a short period of just four–six weeks before diagnosis, often making early detection difficult. AML exhibits significant genetic complexity, with mutations such as FLT3 occurring in approximately 25–30% of patients and being associated with poorer outcomes while IDH1/IDH2 mutations are found in about 6–13% of cases, particularly among older adults. Additionally, most AML (~60–70%) arises in patients with a normal karyotype but varying molecular profiles, complicating risk classification and treatment selection. Diagnostic infrastructure also varies, as molecular testing required for targeted therapy decisions is often delayed beyond the recommended three to seven days, particularly in non-academic centers, forcing therapy initiation before precise mutation-driven planning. These combined challenges restrain personalized care and limit market growth in AML.

Opportunity - Development of Novel Combination Therapies

Advances in novel combination therapies, especially BCL-2 inhibitor venetoclax paired with hypomethylating agents (HMAs) such as azacitidine or decitabine, are creating significant opportunities in AML treatment. In October 2020, the FDA granted full approval for this combination in newly diagnosed patients who are ineligible for intensive chemotherapy, based on VIALE-A data, which demonstrated a significant improvement in median overall survival, 14.7 months versus 9.6 months with azacitidine alone (HR 0.66; p<0.001). Meta-analyses confirm overall response rates of over 80%, with complete remission or complete remission with incomplete recovery (CR/CRi) rates exceeding 70% in older or unfit AML patients.

Beyond venetoclax-HMA, combinations targeting specific mutations, such as venetoclax plus IDH inhibitors in IDH1/2-mutant AML, have produced CR/CRi rates above 85–90% in early-phase trials. Emerging immunotherapy combinations, such as venetoclax with STING agonists, have shown eradication of AML cells in lab models and are entering early clinical testing. These developments highlight the growing opportunity for novel combination strategies to improve survival in AML.

Acute Myeloid Leukemia Treatment Market Key Trend

Precision Medicine and Targeted Therapies Redefine Care

The Acute Myeloid Leukemia (AML) treatment market is evolving rapidly, driven by rising incidence, an aging global population, and the growing adoption of targeted therapies. AML is an aggressive blood cancer that primarily affects older adults, with most diagnoses occurring after age 60. Traditional treatments such as chemotherapy and stem cell transplantation remain common, but targeted drugs such as FLT3 and IDH inhibitors are transforming the treatment landscape. Regulatory approvals and ongoing clinical trials are expanding therapeutic options, especially for relapsed or unfit patients. Combination regimens, including venetoclax-based therapies, are gaining traction due to improved response rates. As unmet needs persist and survival rates remain modest, pharmaceutical innovation, early diagnosis, and personalized medicine are emerging as key trends shaping the future of AML care.

Category-wise Analysis

Disease Insights

Based on disease, the market is divided into myeloblastic leukemia, myelomonocytic leukemia, and promyelocytic leukemia. The myeloblastic leukemia disease segment is anticipated to lead capturing a market share of approximately 45.6% in 2025, owing to the high incidence and prevalence of this disease category, which generates substantial demand for effective therapies. The segment growth is further bolstered by the ongoing advancements of novel medicines and the enhancement of current treatments. In July 2023, the FDA sanctioned a novel targeted therapy for AML, quizartinib, in conjunction with traditional chemotherapeutic regimens, precisely targeting genetic alterations in some AML patients.

Treatment Insights

Based on treatment type, the market is further divided into chemotherapy, targeted therapy, and immunotherapy, with chemotherapy currently dominating. The chemotherapy treatment segment is projected to hold around 50.1% of the total market share in 2025, owing to its recognized function as a principal therapeutic approach.

The dependence on chemotherapy is due to its effectiveness in attaining remission in AML patients, especially during induction therapy. Recent FDA approvals, including quizartinib in conjunction with standard chemotherapies for particular genetic alterations in AML patients, highlight the continuous progress in this field and its essential function in standard care procedures.

The amalgamation of chemotherapy with contemporary targeted therapies, shown by the combination of low-dose cytarabine and novel medicines such as glasdegib, improves results for elderly patients and individuals with considerable comorbidities who may be unable to endure aggressive chemotherapy. The strategic application of chemotherapy as a monotherapy and in combination regimens secures its substantial market share and ongoing significance in AML treatment approaches.

Regional Insights

North America Acute Myeloid Leukemia Treatment Market Trends

North America is anticipated to account for approximately 38.2% market share in 2025. North America leads the Acute Myeloid Leukemia (AML) treatment market due to its high disease burden, advanced healthcare infrastructure, and strong research ecosystem. The American Cancer Society reports over 20,000 new AML cases annually in the U.S., with most patients diagnosed above age 65, driving significant demand for treatment.

The region also benefits from regulatory support for novel AML drugs such as enasidenib and gilteritinib, received FDA approval through accelerated pathways. Public funding bodies such as the National Cancer Institute (NCI) and NIH support a large share of global AML clinical trials, many of which are based in the U.S. In addition, widespread insurance coverage allows greater access to advanced treatments, such as venetoclax-based regimens and stem cell transplants.

These factors, combined with a robust pipeline of targeted therapies, strong diagnostics infrastructure, and early adoption of new standards of care, position North America at the forefront of the global market.

Europe Acute Myeloid Leukemia Treatment Market Trends

Europe plays a vital role in the global acute myeloid leukemia (AML) treatment market due to its substantial disease burden, aging population, and improving healthcare systems. According to EU-wide data, the incidence of AML in Europe rose from approximately 11,185 cases in 1990 to about 23,705 in 2021, with deaths increasing from 10,796 to 21,665 over the same period, illustrating a growing public health challenge. The Global Cancer Observatory estimates AML incidence in Europe at around 5.06 per 100,000 people, with annual mortality between 4 and 6 per 100,000.

In the U.K. alone, there are about 2,900 new AML cases each year (2017–2019 average), causing roughly 2,700 deaths annually, mostly in patients aged 75 and over; nearly 41% of new diagnoses occur in that age group. Germany sees approximately 3,600 AML diagnoses per year, with a median age at diagnosis of around 63.

Survival for AML in Europe remains modest, with five-year relative survival rates at around 15 %, compared to much higher rates for other myeloid diseases, highlighting ongoing unmet needs and justifying the demand for new treatments.

Competitive Landscape

The competitive landscape of the Acute Myeloid Leukemia (AML) treatment market is shaped by a mix of established pharmaceutical companies and emerging biotech firms focused on targeted and immunotherapies. Key players are actively developing mutation-specific drugs, with several FLT3, IDH1/2, and BCL-2 inhibitors gaining regulatory approval.

Clinical trials involving CAR-T cells, antibody–drug conjugates, and combination regimens are expanding globally. Public research institutions, particularly in the U.S. and Europe, collaborate with industry to accelerate innovation. The market remains dynamic with continuous R&D efforts, strategic partnerships, and increasing investments in personalized medicine aimed at improving AML patient outcomes.

Key Industry Developments

- In June 2025, Servier India officially launched Ivosidenib (Tibsovo®), a first-in-class oral targeted therapy for IDH1-mutated acute myeloid leukemia (AML) and cholangiocarcinoma in India. The drug received approval from India's Central Drugs Standard Control Organisation (CDSCO) on 14 May 2025, following a favorable recommendation from the Subject Expert Committee in April.

- In June 2025, Pfizer confirmed that the U.S. Food and Drug Administration had approved updated labeling for TALZENNA® (talazoparib) in combination with XTANDI® (enzalutamide) for patients with homologous recombination repair (HRR) gene-mutated metastatic castration-resistant prostate cancer (mCRPC).

- In November 2024, Lin BioScience announced that its lead candidate, LBS 007, had received Fast Track Designation from the U.S. Food and Drug Administration for treating acute myeloid leukemia (AML).

- In April 2024, Actinium disclosed the findings of the Phase 3 SIERRA study for Iomab-B, demonstrating a survival benefit in patients with high-risk relapsed or refractory acute myeloid leukemia possessing TP53 mutations. The findings were accepted for oral presentation at the 50th Annual Meeting of the European Bone Marrow Transplantation.

Companies Covered in Acute Myeloid Leukemia Treatment Market

- Astellas Pharma Inc.

- Bristol Myers Squibb Company

- Daiichi Sankyo Company, Limited

- Jazz Pharmaceuticals, plc

- Novartis AG

- Pfizer, Inc.

- Rigel Pharmaceuticals, Inc.

- AbbVie Inc.

- Servier Laboratories

Frequently Asked Questions

The global acute myeloid leukemia treatment market is estimated to be US$ 2.6 Bn in 2025.

The acute myeloid leukemia treatment market is driven by rising AML incidence, aging population, targeted therapy approvals, clinical research advancements, and supportive regulatory frameworks.

The acute myeloid leukemia treatment market is projected to record a CAGR of 10.0% during the forecast period from 2025 to 2032.

Opportunities include novel drug combinations, precision medicine, immunotherapies, early diagnosis tools, and expanding access in emerging healthcare markets.

Major players include Astellas Pharma Inc., Bristol Myers Squibb Company, Daiichi Sankyo Company, Limited, Jazz Pharmaceuticals, plc, Novartis AG, and Pfizer, Inc.