- Pharmaceuticals

- Hairy Cell Leukemia Treatment Market

Hairy Cell Leukemia Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Hairy Cell Leukemia Treatment Market by Cancer Type (Leukemia, Lymphoma, Multiple Myeloma, Others), Therapy (Chemotherapy, Immunotherapy, Targeted Therapy, Combination Therapy), Route of Administration (Intravenous, Oral, Subcutaneous), End-user (Hospitals, Cancer Treatment Centers, Specialty Clinics, Diagnostic Laboratories, Research Institutes), and Regional Analysis, 2026 - 2033

Hairy Cell Leukemia Treatment Market Share and Trends Analysis

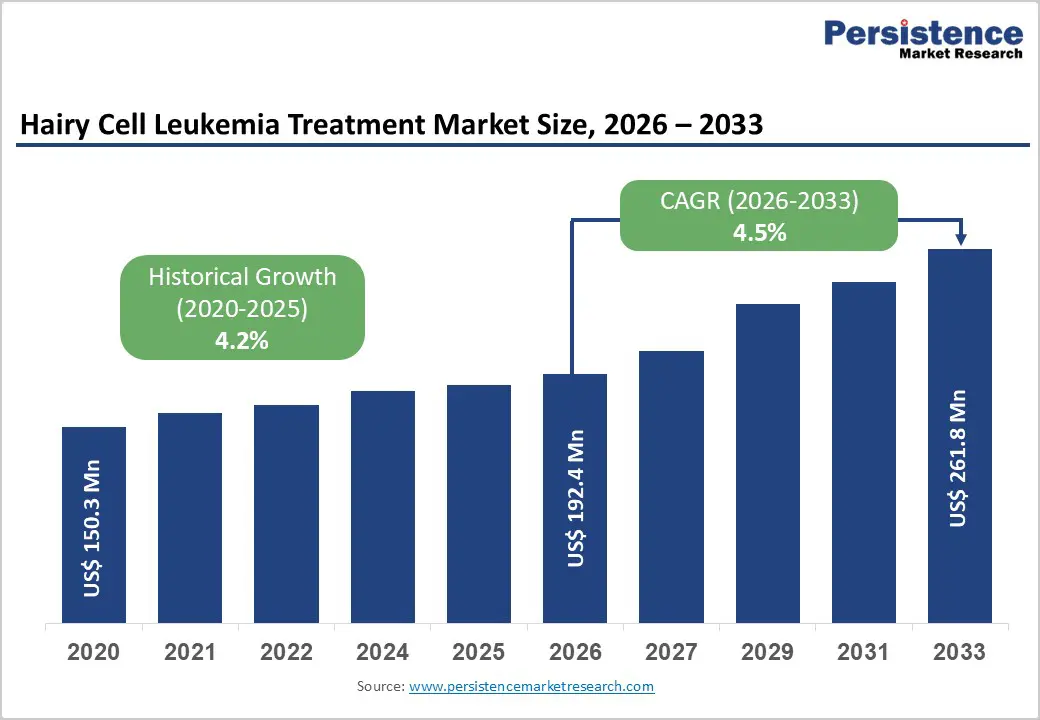

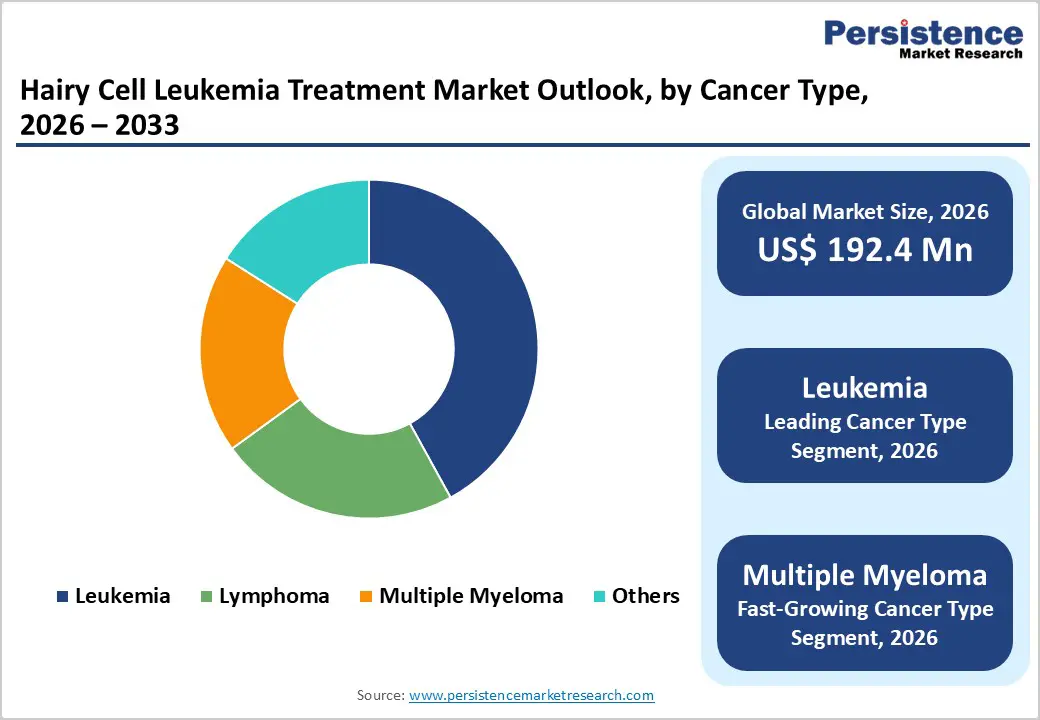

The global hairy cell leukemia treatment market size is expected to be valued at US$ 192.4 million in 2026 and projected to reach US$ 261.8 million by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

This steady expansion reflects rising diagnosis rates of this rare leukemia, improving survival that extends treatment duration, and rapid adoption of targeted and immunotherapy-based regimens alongside established purine analog chemotherapy. Growing emphasis on personalized oncology, orphan drug incentives, and stronger clinical evidence for BRAF inhibitors and anti-CD20 monoclonal antibodies are further anchoring long-term demand across major oncology centers.

Key Industry Highlights:

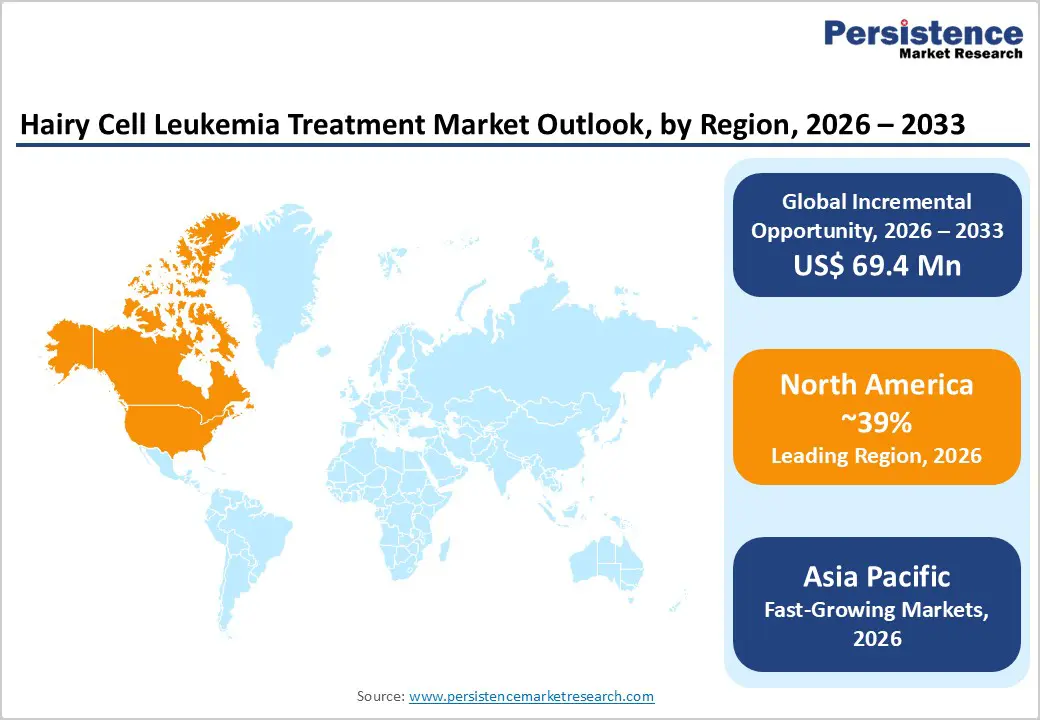

- North America remains the leading region in the hairy cell leukemia treatment market, driven by high diagnosis rates, strong reimbursement, advanced infusion infrastructure, and dense networks of comprehensive cancer centers and academic hematology programs.

- Asia Pacific is projected to be the fastest-growing region, as expanding oncology infrastructure, better access to flow cytometry and molecular testing, and improving insurance coverage in China, India, Japan, and ASEAN support rapid therapy uptake.

- Within cancer types, the leukemia segment—encompassing classic hairy cell leukemia and related entities dominates market share due to clearer diagnostic criteria, robust treatment algorithms, and strong evidence for long-term survival benefits from purine analog-based regimens.

- On the therapy axis, targeted therapy and combination therapy are the fastest-growing segments, propelled by BRAF inhibitors, anti-CD20 antibodies, and chemo-immunotherapy sequences that achieve high MRD-negative remission rates and appeal to clinicians seeking less myelotoxic options.

- A key market opportunity lies in integrating personalized medicine with expanded access in emerging markets, combining genomic profiling, companion diagnostics, and innovative regimens to address unmet needs in relapsed HCL while capturing high-growth patient pools in Asia Pacific and other developing regions.

| Key Insights | Details |

|---|---|

|

Hairy Cell Leukemia Treatment Market Size (2026E) |

US$ 192.4 million |

|

Market Value Forecast (2033F) |

US$ 261.8 million |

|

Projected Growth CAGR (2026-2033) |

4.5% |

|

Historical Market Growth (2020-2025) |

4.2% |

Market Dynamics

Drivers - Rising incidence, aging population, and improved survival

A key demand driver is the combination of low but steadily recognized incidence, aging demographics, and markedly improved survival in hairy cell leukemia (HCL). Epidemiological studies indicate an incidence of roughly 0.28–0.30 cases per 100,000 people in Europe and North America and around 2% of all adult leukemias, translating into approximately 700–1,240 new cases annually in the United States. Median age at diagnosis is typically in the mid- to late-50s, and long-term survival now approaches that of the general population for many patients, supported by complete remission rates of 85–90% with modern regimens. As more patients live longer with chronic HCL, the prevalent pool under surveillance and at risk of relapse expands, sustaining recurrent demand for therapeutics, diagnostic monitoring, and supportive care across hospitals and cancer centers.

Clinical success of purine analogs and combination chemo-immunotherapy

The long-standing clinical success of purine analog chemotherapy and its evolution into combination chemo-immunotherapy is another fundamental growth engine. Agents such as cladribine and pentostatin have been the standard of care for over three decades and routinely deliver complete response rates of 75–90% in first-line treatment. Recent phase II data show that combining cladribine with concurrent or sequential rituximab can achieve complete response rates near 97% and minimal residual disease (MRD) negativity in roughly 77–97% of patients, with durable event-free and overall survival beyond 10 years. These robust outcomes solidify purine analog-based regimens as a clinical benchmark, reinforcing clinician confidence and guideline support, while also catalyzing incremental innovation in add-on monoclonal antibodies and sequencing strategies that expand overall market value per patient.

Restraints - Treatment-related immunosuppression and safety concerns

Despite their efficacy, purine analogs and several targeted therapies are associated with significant myelosuppression and immunosuppression, which can limit uptake, especially in older or comorbid patients. The National Cancer Institute (NCI) notes that cladribine, with or without rituximab, remains standard of care, but highlights risks of serious and prolonged immune suppression, prompting consideration of non-chemotherapy options in frail populations. Clinical reviews similarly document substantial rates of neutropenia, lymphopenia, infections, and related complications, sometimes persisting long after treatment completion. These safety concerns can delay treatment initiation, necessitate hospitalization or intensive monitoring, and drive clinician preference toward less myelotoxic regimens, tempering the pace of adoption for some high-intensity protocols and constraining overall market expansion.

Diagnostic complexity and limited awareness of a rare malignancy

Hairy cell leukemia remains a rare and often under-recognized B-cell malignancy, and its diagnosis requires specialized hematopathology expertise and access to advanced immunophenotyping and molecular testing. Accurate identification depends on recognition of characteristic "hairy" lymphocytes in blood or marrow, expression of markers such as CD11c, CD25, CD103, CD123, and detection of BRAF V600E mutations, capabilities not uniformly available in smaller or resource-limited centers. These requirements, combined with the disease’s low incidence, can delay diagnosis, lead to misclassification as other leukemias or lymphomas, and limit enrollment in clinical trials. In many emerging markets, underdiagnosis and underreporting reduce the addressable treated population versus the true epidemiologic burden, dampening near-term commercial penetration despite underlying unmet need.

Opportunity - Expansion of targeted therapies and non-chemotherapy regimens

A major opportunity lies in the expanding role of targeted agents, particularly BRAF inhibitors and next-generation monoclonal antibodies, as frontline or relapse options that reduce reliance on myelotoxic chemotherapy. The discovery that BRAF V600E mutations are present in nearly all classic HCL cases has enabled potent oral agents such as vemurafenib and dabrafenib, which have demonstrated high response rates in relapsed or refractory disease and can be combined with anti-CD20 antibodies. Phase II programs testing vemurafenib with obinutuzumab in previously untreated or relapsed HCL indicate promising responses and the potential to offer fully non-chemotherapy regimens, particularly attractive for patients with severe cytopenias or infection risk. As regulatory pathways for orphan indications remain supportive in North America and Europe, and targeted agents gain broader label expansions and guideline inclusion, targeted therapy and combination therapy segments are poised for above-average growth.

Personalized medicine, genomic profiling, and growth in emerging markets

The shift toward personalized oncology and comprehensive genomic profiling is opening new revenue streams across diagnostics, therapeutics, and long-term disease monitoring in HCL. Routine testing for BRAF V600E and other mutations such as KMT2C, CCND3, and U2AF1 is increasingly used to guide therapy choice, predict resistance to BRAF inhibitors, and identify candidates for investigational MEK inhibitors or novel immunotherapies. At the same time, improving hematology infrastructure and healthcare expenditure in the Asia Pacific, driven by economic growth in China, India, and Japan, are enabling earlier detection of rare leukemias and better access to advanced treatments, with regional CAGR estimates outpacing mature markets. Together, these trends create attractive opportunities for companies to bundle companion diagnostics with branded therapies, localize manufacturing, and expand clinical trial networks in high-growth emerging economies.

Category-wise Analysis

Cancer Type Insights

Leukemia remains the leading cancer-type segment in the broader hematologic malignancy context, accounting for about 42% market share in 2025 within the defined scope, supported by the predominance of leukemic presentations such as classic hairy cell leukemia. Leukemia in adults shows annual incidence rates in the tens of thousands globally, with HCL representing approximately 2% of adult leukemia cases and around 700–1,240 new diagnoses each year in the United States alone. Robust clinical data, well-established diagnostic algorithms, and clear treatment pathways from purine analogs to targeted BRAF inhibitors have led to earlier intervention and high remission rates, reinforcing leukemia’s dominant share relative to lymphoma, multiple myeloma, and other rarer B-cell entities. As molecularly defined subtypes such as HCL gain further visibility, the leukemia segment is expected to retain leadership.

Therapy Insights

Within the therapy landscape, chemotherapy, primarily purine analogs cladribine and pentostatin, continues to command the largest share of hairy cell leukemia treatment utilization and revenue in 2025, even as immunotherapy and targeted therapy grow rapidly. Multiple guidelines and real-world studies confirm that a single course of cladribine or pentostatin can induce complete remissions in 75–90% of patients, with median remission durations extending beyond 10 years in many cohorts. Sequential or concurrent addition of anti-CD20 antibodies such as rituximab further deepens responses while preserving the chemotherapy backbone. Because these regimens are widely available, relatively standardized, and reimbursed as first-line options in most high-income markets, chemotherapy retains a leading market position, while targeted therapy and combination therapy represent the fastest-growing subsegments.

End-user Insights

Among end-users, hospitals and cancer treatment centers together represent the leading share of the hairy cell leukemia treatment market in 2025, driven by the need for specialized hematology expertise, infusion capacity, and sophisticated diagnostics. Initial diagnosis of HCL typically involves bone marrow biopsy, flow cytometry, and molecular testing for BRAF V600E, which are most readily available in tertiary hospitals and dedicated oncology centers. Purine analog infusions, monoclonal antibody therapy, management of severe cytopenias, and handling of infectious complications also require multidisciplinary inpatient or day-hospital environments. Although specialty clinics and research institutes play growing roles in follow-up care and clinical trials, the complexity and risk profile of HCL treatment ensure that hospitals and integrated cancer centers remain the dominant end-user segment globally.

Regional Insights

North America Hairy Cell Leukemia Treatment Market Trends and Insights

North America, led by the United States, is the largest regional market, accounting for around 39% of global hairy cell leukemia treatment revenues in 2025, underpinned by advanced oncology infrastructure, high per-capita healthcare spending, and well-established referral networks. HCL accounts for about 2% of adult leukemias in the region, with an estimated 700–1,000 new cases annually and strong representation in academic cancer centers that drive adoption of novel regimens. The U.S. Food and Drug Administration (FDA) has approved purine analogs and several BRAF inhibitors for related indications, while off-label and trial-based use in HCL is supported by robust clinical data.

Regulatory frameworks for orphan and rare diseases, including accelerated approval pathways and market exclusivity, further incentivize innovation by companies such as F. Hoffmann-La Roche Ltd, Johnson & Johnson (Janssen), Amgen Inc., Gilead Sciences, Inc., and AstraZeneca plc. North American centers are heavily involved in phase II and III trials evaluating combinations such as vemurafenib plus obinutuzumab versus standard cladribine-rituximab, and long-term follow-up of cladribine-rituximab sequences shows 10-year event-free survival above 85% and overall survival around 90%. This innovation ecosystem, coupled with strong reimbursement for high-cost biologics, will help the region maintain leadership through 2033.

Asia Pacific Hairy Cell Leukemia Treatment Market Trends and Insights

The Asia Pacific region is the fastest-growing market for hairy cell leukemia treatment, supported by rising healthcare investment, expanding oncology infrastructure, and increasing recognition of rare hematologic malignancies in China, Japan, India, and ASEAN countries. Historically, reported HCL prevalence in Asia has been lower than in Western populations, but improved access to flow cytometry and molecular diagnostics is beginning to close the diagnostic gap, revealing a broader underlying patient base. PMR analysis indicates that Asia Pacific is poised for a higher CAGR than mature regions over 2024–2031, reflecting this catch-up in diagnosis and treatment access.

Regional manufacturing strengths and a large generics industry, especially in India and China are also enhancing the affordability of purine analogs and anti-CD20 antibodies, which should accelerate therapy penetration beyond top-tier urban centers. Local players and subsidiaries of multinational firms such as Takeda Pharmaceutical Company, Dr. Reddy’s Laboratories, and Teva Pharmaceutical Industries Ltd. are increasingly involved in supplying chemotherapy agents and biosimilars, while major Japanese and Chinese research institutions participate in global HCL trials. As governments roll out cancer control programs and insurance coverage expands, the Asia Pacific is expected to deliver the fastest incremental growth in patient volumes and revenue through 2033.

Competitive Landscape

The Hairy Cell Leukemia treatment market is highly specialized and moderately consolidated, driven by a small patient population and well-established standard-of-care therapies. Competition is shaped by strong clinical efficacy, long remission duration, and favorable safety profiles rather than high treatment volumes. Innovation is increasingly focused on targeted and immune-based approaches for relapsed or refractory patients, where unmet needs remain. Pricing pressure is limited due to the rarity of the disease, but treatment adoption depends heavily on physician experience and long-term outcomes.

Key Market Developments

- In June 2024, F. Hoffmann-La Roche Ltd advanced obinutuzumab into phase II clinical development for hairy cell leukemia, exploring its use alone and in combination with vemurafenib to improve outcomes in relapsed or high-risk patients.

Companies Covered in Hairy Cell Leukemia Treatment Market

- Pfizer Inc., F. Hoffmann-La Roche AG

- Johnson & Johnson (Janssen)

- Novartis AG

- AstraZeneca PLC

- AbbVie Inc.

- Amgen Inc.

- Gilead Sciences, Inc.

- Merck & Co., Inc.

- Sanofi S.A.

- Takeda Pharmaceutical Company,

- Teva Pharmaceutical Industries Ltd.,

- Dr. Reddy’s Laboratories,

- Hospira,

- Astex Therapeutics, Incyte Corporation

- BioGenomics Limited

Frequently Asked Questions

The global hairy cell leukemia treatment market size is expected to reach around US$ 192.4 million in 2026, supported by rising diagnosis rates, improved survival, and ongoing adoption of purine analog and targeted therapy regimens.

Key demand is driven by effective purine analog chemotherapy and chemo-immunotherapy, which achieve complete response rates above 75–90% and long-term survival, encouraging guideline endorsement and sustained treatment demand across major oncology centers.

North America leads the global market, accounting for an estimated 39% share in 2025, underpinned by advanced oncology infrastructure, orphan-drug incentives, and high uptake of innovative targeted and immunotherapy-based regimens.

A major opportunity lies in expanding personalized, genomics-guided treatment, including BRAF inhibitors and next-generation monoclonal antibodies, into high-growth Asia Pacific markets, leveraging improved diagnostics and healthcare coverage to reach under-treated HCL populations.

Major players include F. Hoffmann-La Roche AG, Johnson & Johnson (Janssen), Pfizer Inc., AstraZeneca PLC, Amgen Inc., AbbVie Inc., Gilead Sciences, Inc., Merck & Co., Inc., Sanofi S.A., Takeda Pharmaceutical Company, and Teva Pharmaceutical Industries Ltd., alongside regional and specialty firms.