- Pharmaceuticals

- Gastroenterology Market

Gastroenterology Market Size, Growth, Share, Trends, Forecasts, 2025 - 2032

Gastroenterology Market by Type (Branded, Generics), by Application (Crohn's Disease, Ulcerative Colitis, Irritable Bowel Disease (IBD), Others), by End-user (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies), and Regional Analysis for 2025 - 2032

Gastroenterology Market Share and Trends Analysis

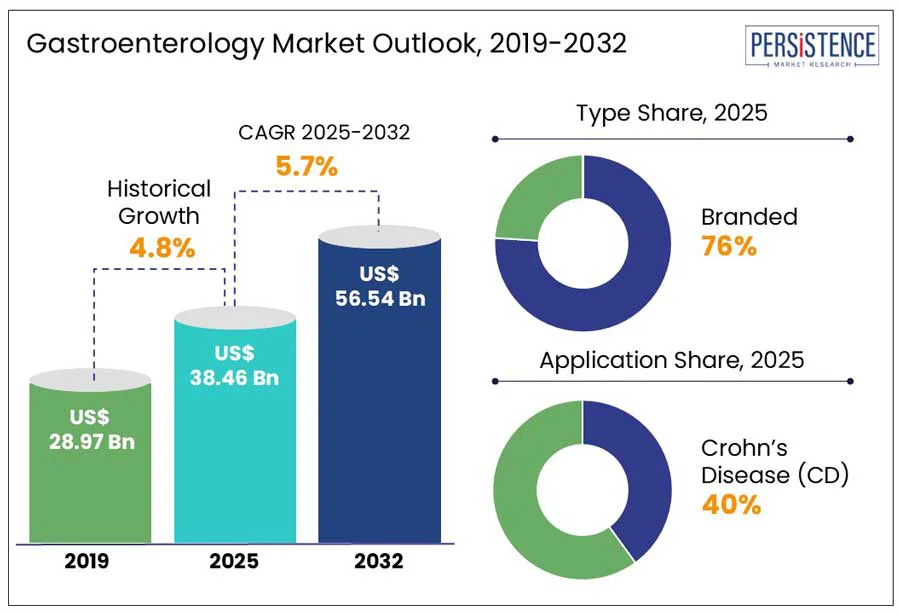

The global gastroenterology market size is projected to rise from US$ 38.46 Bn in 2025 to US$ 56.54 Bn by 2032. The market is further anticipated to register a CAGR of 5.7% during the forecast period, 2025 to 2032. According to the Persistence Market Research report, key growth drivers include the increasing prevalence of gastrointestinal diseases among both older adults and younger population a heightened awareness of advancements in medical technology. Poor dietary habits, driven by sedentary and professional lifestyles with an increased reliance on fast-food, often containing preservatives, additives and artificial ingredients, have contributed to a surge in digestive health issues. Consequently, conditions such as gallstones, ulcerative colitis, and Irritable Bowel Syndrome (IBS) are becoming increasingly common worldwide.

Gastroenterology focuses on the diagnosis, treatment, and prevention of diseases affecting the digestive system, including the GI tract, liver, pancreas, and gallbladder. Rising cases of conditions, such as peptic ulcers, IBD, and colorectal cancer, are driving demand for effective therapies. There is a growing emphasis on early detection and prevention through screenings and lifestyle changes. New diagnostic technologies, such as endoscopic ultrasound, capsule endoscopy, and minimally invasive procedures improve treatment outcomes.

Biological drugs, with targeted action and fewer side effects, are gaining traction, leading to increased regulatory approvals and market growth. According to a 2022 study published in ScienceDirect on AI and gastroenterology, gastroenterology is expected to radically transform in the coming years as advancements in AI and Machine Learning (ML) continue to accelerate.

Key Industry Highlights:

- The gastroenterology market is driven by the global rise in gastrointestinal conditions, largely fueled by sedentary lifestyles and poor eating habits, which significantly contribute to morbidity and mortality.

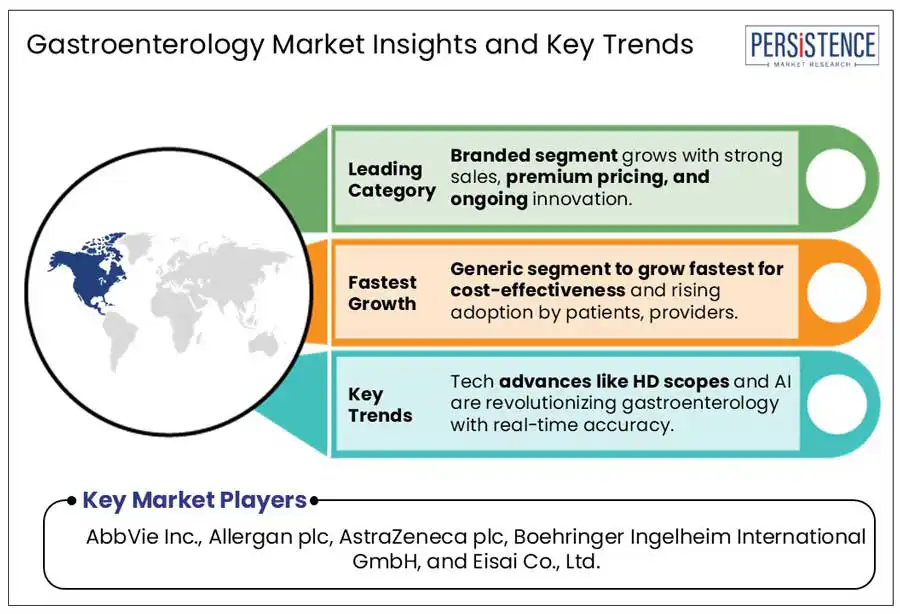

- The branded segment is driven by strong commercial success, premium pricing, and continuous innovation.

- The generic segment is expected to witness the fastest growth due to its cost-effectiveness, rising adoption among patients and healthcare providers, and the increasing availability of generic alternatives for branded drugs.

- North America has the largest revenue share owing to the rising prevalence of gastrointestinal diseases and support from government and non-government organizations.

- Technological advancements are rapidly transforming gastroenterology, with innovations such as high-definition, slimmer endoscopes, and AI integration.

- The convergence of telemedicine, AI, and third-space endoscopy is set to revolutionize gastroenterology.

|

Global Market Attribute |

Key Insights |

|

Gastroenterology Market Size (2025E) |

US$ 38.46 Bn |

|

Market Value Forecast (2032F) |

US$ 56.54 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Dynamics

Driver - The rising incidence of gastrointestinal issues across all age groups

There is a global rise in gastrointestinal conditions, largely driven by sedentary lifestyles and poor eating habits, which significantly contribute to morbidity and mortality. A 2022 ScienceDirect study highlights that gastrointestinal diseases (GIDs) affect the esophagus, stomach, small intestine, colon, and rectum, with common symptoms such as diarrhea, abdominal pain, and bloating. The growing burden of these diseases is driving demand for more effective diagnostic tools and treatments. A May 2023 National Library of Medicine study also notes a concerning increase in colorectal cancer (CRC) among younger adults, especially those in their 20s and 30s, largely linked to modifiable risk factors such as diet, obesity, and substance use. This growing burden of chronic gastrointestinal diseases is forcing pharmaceutical companies and healthcare providers to focus on expanding their offerings in the gastroenterology sector.

Furthermore, a 2024 MDPI study emphasizes that older adults often exhibit gastrointestinal symptoms due to underlying organic diseases, with aging and comorbidities complicating diagnosis and treatment. According to the American Gastroenterological Association (2023), digestive diseases caused eight million deaths and 277 million population lost healthy years in 2019, with little improvement in global incidences since 1990. The increasing number of cases across all age groups is augmenting the demand for minimally invasive and gastroenterology procedures such as endoscopy.

Restraints - The high cost of endoscopy devices

The high cost of medical devices and treatments poses a significant challenge to the growth of the gastroenterology market. Endoscopy procedures, which are central to diagnosing and treating many gastrointestinal (GI) disorders, involve expensive equipment such as endoscopes, biopsy valves, polypectomy snares, clips, and balloon dilation systems. According to a 2019 NLM article, conventional endoscopes range from US$20,000 to US$40,000 per tube, while a full dual-tube system can cost up to US$120,000. Endoscopic ultrasound systems can add another $200,000. These high acquisition costs, along with ongoing maintenance and operational expenses, limit access, particularly in resource-constrained settings.

Additionally, the high cost of gastrointestinal treatments, especially for chronic conditions including Crohn’s disease and ulcerative colitis, further hampers market growth. These illnesses often require long-term use of biologics such as infliximab and vedolizumab, which costs between US$2,500 and US$8,700 per month. With hospitalizations, doctor visits, and connected therapies, the total cost of care becomes a major burden for patients, especially in countries with limited healthcare funding, including India and Brazil. Rising out-of-pocket expenses and limited reimbursement policies for advanced treatments continue major obstacles to wider adoption and market penetration in gastroenterology.

Opportunities - Advancing technologies and AI integration are key trends reshaping the gastroenterology sector

Technological advancements are rapidly transforming gastroenterology, with innovations such as high-definition, slimmer endoscopes and AI integration enabling accurate diagnosis, demonstrated by Olympus’s EVIS X1 and Anthropic’s Peek Gastro. A May 2024 study published in Nature Communications highlights solutions, such as magnetic drive systems and swarm capsule robots, to address miniaturization challenges in capsule endoscopy. Telemedicine, strengthened by 5G and cloud technologies, is expanding access to care in resource-poor regions by enabling remote consultations. Integrating therapeutic functions including Endoscopic Mucosal Resection (EMR) and Endoscopic Submucosal Dissection (ESD) into capsule devices, along with micro/nanorobot applications, is paving the way for minimally invasive GI treatments.

Looking ahead, the convergence of telemedicine, AI, and third-space endoscopy will revolutionize gastroenterology. These innovations offer earlier detection, personalized treatment, and improved outcomes. Advances in microbiome research and gene editing tools, such as CRISPR, are opening new therapeutic avenues, especially for inherited GI disorders. As noted in a Wiley study (June 2024), Endoscopic Full Thickness Resection (EFTR), though currently limited in treating malignant tumors, shows promising potential. Together, these developments are reshaping the field into a more precise, accessible, and patient-centered specialty.

Category-wise Analysis

Type Insights

By type, the branded segment is expected to account for approximately 76% of revenue in 2025, driven by strong commercial success, premium pricing, and continuous innovation. Branded drugs are typically the first to market, developed through extensive research, clinical trials, and regulatory approval, often targeting unmet medical needs such as IBD, IBS, gastrointestinal cancers, ulcerative colitis, Crohn’s disease, and acid reflux. Pharmaceutical companies invest heavily in R&D to create novel therapies with improved efficacy and safety, which justifies their higher cost.

Additionally, strong marketing strategies and physician loyalty to trusted brands further strengthen the segment’s market position. Examples include RINVOQ and Zeposia for ulcerative colitis, along with other well-known products such as Humira, Entyvio, and Nexium. Key players such as AbbVie, Takeda, and Pfizer continue to lead this space. For example, in 2025, Mirikizumab-mrkz (Omvoh) was approved for Crohn's disease.

The generic segment is expected to witness the fastest growth in the coming years, which can be attributed to its cost-effectiveness, rising adoption among patients and healthcare providers, and the increasing availability of generic alternatives for branded drugs. As patents for high-cost branded medications expire, more generics are entering the market, providing inexpensive treatment options without negotiating on efficacy. Additionally, government initiatives to raise awareness and promote the use of generic medicines further support this trend. Some examples of popular generics are Omeprazole, Pantoprazole, and Ondansetron. All these factors in unison will propel segment growth between 2025 and 2032.

End-user Insights

Based on end-user, the Crohn’s Disease (CD) segment is anticipated to dominate, accounting for a revenue share of about 40% in 2025. The incidence of CD, a chronic inflammatory bowel condition, has been steadily rising. According to an October 2024 study by ResearchGate, rates increased from 5.1 per 100,000 in 1988–1990 to 7.9 per 100,000 in 2015–2017. As per the study conducted by NLB in February 2024, the contributing factors of CD include genetic predisposition (NOD2 mutation), environmental changes, and lifestyle habits such as smoking. Globally, the increasing incidence of CD and unmet needs in this segment emphasize its growth over the forecast period.

Ulcerative Colitis (UC) is expected to be the fastest-growing segment, with a 4.3% CAGR, driven by easy drug availability, advancements in medical treatments (biologics and biosimilars), and supportive government approvals. Key players, such as AstraZeneca, Lilly, and Celgene Corporation are actively developing new treatments for UC.

Regional Insights

North America Gastroenterology Market Trends

North America dominated the global gastroenterology market in 2025, accounting for approximately 45% of the revenue share. Many leading companies with extensive gastroenterology portfolios, such as Boston Scientific, Medtronic, and Stryker, are present in North America. Moreover, the rising prevalence of gastrointestinal diseases and support from government and non-government organizations (Crohn’s & Colitis Foundation, U.S.), will fuel regional market growth by promoting research and awareness. Additionally, the easy availability of treatments, such as biologics (Humira, Entyvio) and oral therapies.

The U.S. gastroenterology market accounted for the largest share of North America in 2025. This upward trajectory is fueled by a surge in digestive disorders, a growing elderly population, and higher investments in healthcare. Eli Lilly and Co., Johnson & Johnson, and AbbVie Inc. are some of the prominent companies in the U.S.

Asia Pacific Gastroenterology Market Trends

Asia Pacific is projected to witness a fast-growth rate owing to the rising population, incidence of GI disorders, a growing elderly population, greater investments in R&D, and significant unmet healthcare needs. Takeda Pharmaceutical Company Limited, Gnova Biotech, and Doctris Lifescience are the key players in Asia Pacific.

China’s gastroenterology industry is experiencing steady growth, fueled by significant investments in expanding healthcare services, including gastroenterology and a growing elderly population. For instance, China's healthcare reforms and the expansion of its national health insurance coverage have improved the accessibility to gastroenterology services. Livzon Pharmaceutical Group Inc., a prominent company based in China, manufactures gastroenterology medications.

Europe Gastroenterology Market Trends

Europe is expected to see significant growth in the gastroenterology market from 2025 to 2032, driven by increased use of minimally invasive techniques such as ESD and EMR for early-stage cancer treatment. Rising demand for disposable endoscopic devices, due to hygiene and cost concerns, also supports this trend. Key players include Sequana Medical, Creo Medical, and Norgine, along with global companies such as Ethicon Endo-Surgery, Olympus, and Medtronic.

Germany’s gastroenterology industry is projected to register considerable growth during the forecast period. The growth is driven by an aging population, rising GI disease prevalence, and advanced diagnostic technologies. Key players such as KARL STORZ and Medtronic support innovation, while personalized medicine and preventive care are gaining traction.

Competitive Landscape

The global gastroenterology market is moderately fragmented, with several key players driving growth through product innovations, strategic partnerships, and acquisitions. Ongoing investments in R&D to develop new products are expected to strengthen their market position over the forecast period. Companies, such as AbbVie, Takeda, and Pfizer are among the major players.

Key Industry Developments:

- In January 2025, the U.S. FDA approved Omvoh (mirikizumab-mrkz) for the treatment of moderately to severely active CD in adults, thereby highlighting Eli Lilly's commitment to advancing treatment options for IBD.

- In July 2024, Eli Lilly and Company and Morphic Holding, Inc. announced a definitive agreement for Lilly to acquire Morphic, strengthening the company’s portfolio in chronic disease treatment.

Companies Covered in Gastroenterology Market

- AbbVie Inc.

- Allergan plc

- AstraZeneca plc

- Boehringer Ingelheim International GmbH

- Eisai Co., Ltd.

- GlaxoSmithKline plc

- Johnson & Johnson

- Novartis International AG

- Pfizer Inc.

- Procter & Gamble Co.

- Takeda Pharmaceutical Company Limited

Frequently Asked Questions

The global market is projected to be valued at US$ 38.46 Bn in 2025.

The gastroenterology market is driven by the global rise in gastrointestinal conditions, largely driven by sedentary lifestyles and poor eating habits, which significantly contribute to morbidity and mortality.

The market is poised to witness a CAGR of 5.7% from 2025 to 2032.

Technological advancements are rapidly transforming gastroenterology, with innovations such as high-definition, slimmer endoscopes and AI integration enabling real-time, more accurate diagnosis.

Major players in the oculoplastic surgery industry AbbVie Inc., Allergan plc, AstraZeneca plc, Boehringer Ingelheim International GmbH, and Eisai Co., Ltd.