- Home Appliances

- Water Dispensers Market

Water Dispensers Market Size, Share, and Growth Forecast 2026 - 2033

Water Dispensers Market by Product Type (Bottled, Bottle-less), by End-user (Residential, Commercial, Industrial), by Regional Analysis, 2026 - 2033

Water Dispensers Market Size and Trends Analysis

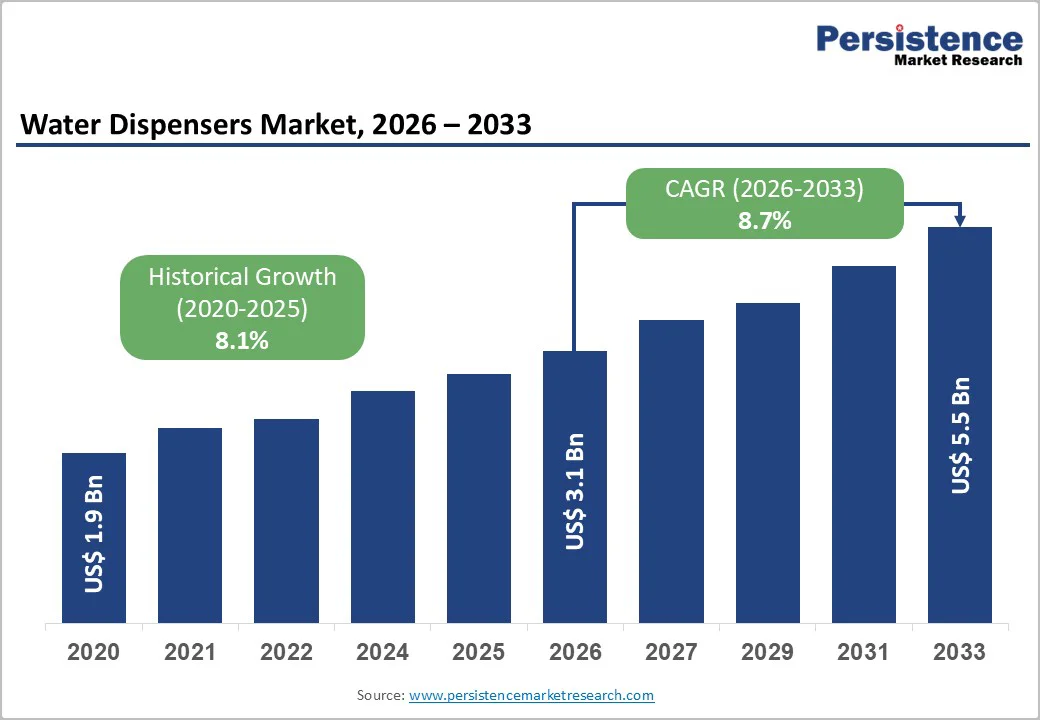

The global water dispensers market size is likely to be valued at US$ 3.1 billion in 2026 and is expected to reach US$ 5.5 billion by 2033, growing at a CAGR of 8.7% during the forecast period from 2026 to 2033.

The market is experiencing robust growth driven by multiple interconnected factors centered on health consciousness and environmental sustainability. Rising awareness of waterborne diseases and contamination in municipal water supplies has created an urgent demand for safe drinking water solutions, with dispensers offering immediate access to purified water without harmful chemicals or microorganisms.

Key Industry Highlights:

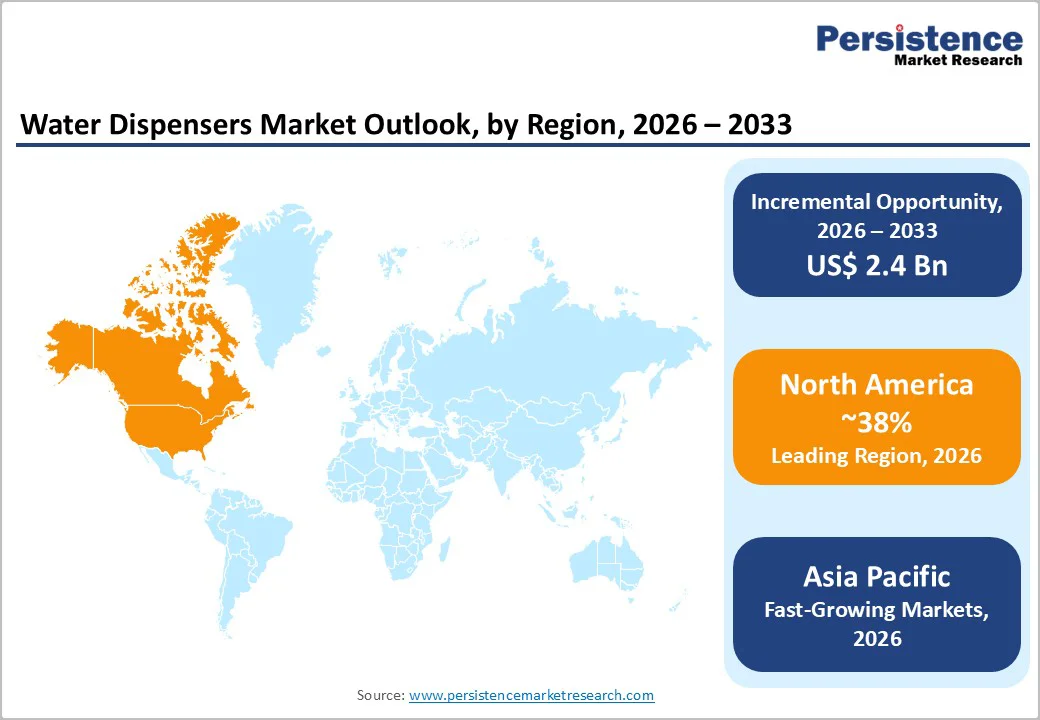

- Leading Region: North America leads the global water dispensers market with a dominant 38% share driven by advanced consumer preferences and strong commercial demand.

- Fastest-Growing Region: Asia Pacific is the fastest-growing water dispensers market, expanding at about 10.8% CAGR due to rapid urbanization, rising incomes, and growing health awareness.

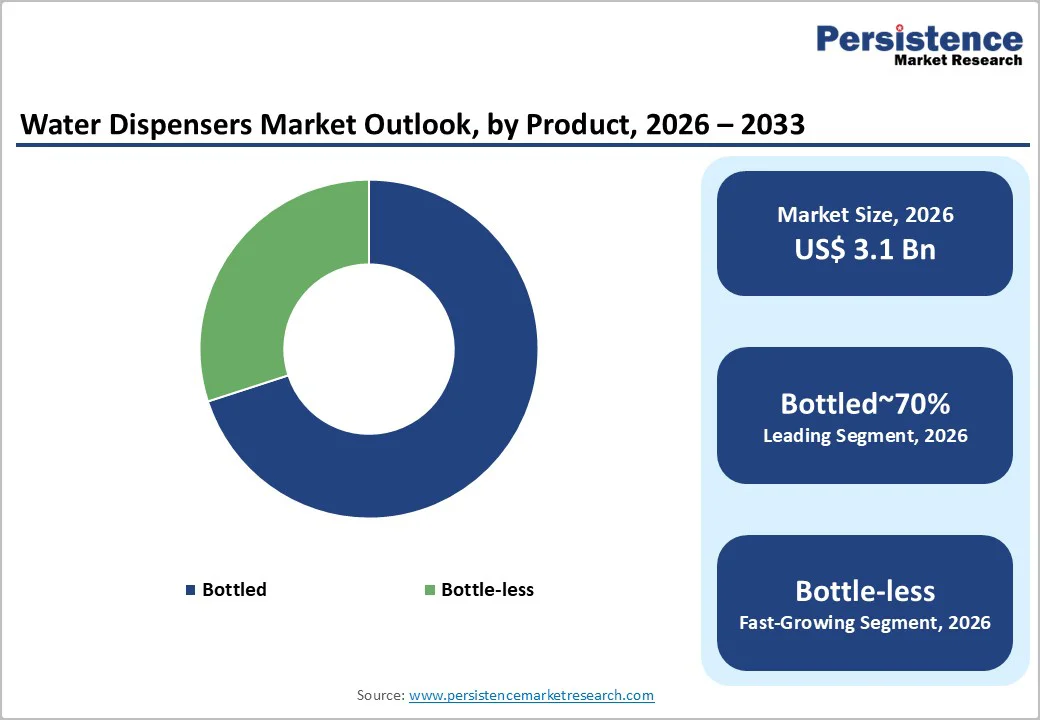

- Leading Segment: Bottled water dispensers remain the largest segment with about 70% share thanks to low installation cost, portability, and strong delivery networks.

- Fastest-Growing Segment: Bottle-less point-of-use systems are the fastest-growing segment at around 9.5% CAGR, driven by sustainability goals and advanced purification technologies.

- Key Opportunity: Smart, IoT-enabled water dispensers create high-value opportunities through real-time monitoring, predictive maintenance, and integration with smart building ecosystems.

| Key Insights | Details |

|---|---|

| Water Dispensers Market Size (2026E) | US$ 3.1 Billion |

| Market Value Forecast (2033F) | US$ 5.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.7% |

| Historical Market Growth (2020 - 2025) | 8.1% |

Market Dynamics

Drivers - Growing Global Concern about Water Contamination is Driving Strong Demand for Safe, Advanced Water Dispensers across Homes and Commercial Spaces

Growing awareness of waterborne diseases and contamination has significantly influenced global consumer behaviour, with widespread reporting from organizations such as the World Health Organization (WHO) and regional health agencies highlighting rising cases linked to unsafe drinking water.

This has encouraged households and businesses to shift toward safer hydration solutions. Primo Water Corporation, as reported in its business updates, has capitalized on this trend by expanding its Water Direct services to millions of homes seeking reliable, high-quality drinking water.

The adoption of advanced purification methods like Reverse Osmosis (RO) and Ultraviolet (UV) technologies has strengthened customer trust in modern water dispensers. Commercial establishments, including hospitals, educational institutions, and corporate offices, now treat dispensers as essential amenities to support employee well-being.

The heightened hygiene consciousness shaped by post-pandemic behaviour has created consistent demand across both residential and commercial segments.

Rapid Urbanization and Expansion of Commercial Facilities Worldwide are Significantly Boosting the Adoption of High-Capacity Water Dispensers

Rapid urbanization, especially in Asia Pacific countries, continues to fuel strong demand for water dispensers, driven by rising commercial real estate, growing office spaces, and expanding hospitality and education sectors. Government projections indicate that India’s urban population will exceed 600 million, accounting for almost 40% of the country’s total population, and reshaping urban water consumption patterns.

Growth in Quick Service Restaurants (QSRs), hospitals, and hotels further strengthens demand for high-capacity dispensing systems. Culligan International Company, as stated in its European business reports, has responded by expanding regional operations, including a turnover of 220 million euros in Italy, representing 10% year-on-year growth.

Modern commercial spaces increasingly treat water dispensers as standard infrastructure, driving installations across office parks, manufacturing plants, and institutional facilities.

Restraints - High Installation and Maintenance Expenses Continue to Limit the Widespread Residential Adoption of Water Dispensers in Cost-Sensitive Markets

Despite their long-term benefits, water dispensers often require significant installation and maintenance investments, which can discourage adoption, especially in price-sensitive markets. Recurring expenses, including filter replacements, sanitization, and repairs, add financial pressure on consumers.

This is particularly challenging in developing regions such as India, Indonesia, and Thailand, where households generally prioritize cost-effective alternatives like basic water filters or packaged drinking water.

The lack of technical expertise also affects smaller businesses and households, reducing equipment efficiency and lifespan. Additionally, plumbed-in water dispensers require professional installation, which increases ownership costs and limits appeal in compact urban homes commonly found in Asian cities. These challenges continue to restrict broader market penetration, despite rising awareness of water quality issues.

Increasing Plastic Waste from Bottled Dispensers poses Major Environmental Challenges, Restricting Market Growth in Sustainability-Focused Regions

Plastic waste generated from bottled water dispensers remains a major environmental concern, as single-use bottles often end up in landfills or oceans despite recycling initiatives. Although many manufacturers promote bottle reusability and collection programs, participation varies widely across regions.

Environmental advocacy groups have frequently highlighted this issue, challenging the sustainability claims of bottled dispenser systems.

Regulatory bodies across Europe, North America, and Asia are tightening plastic waste management rules, which could limit growth in traditional bottled dispenser segments. Environmentally conscious consumers are increasingly shifting toward eco-friendly solutions, questioning the contradiction between promoting clean water and generating plastic waste.

These concerns have also affected public perception of the industry and encouraged businesses to explore greener technologies.

Opportunities - Bottle-Less POU Dispensers are Rapidly Gaining Popularity due to their Sustainability Benefits, Reduced Costs, and Advanced Purification Technologies

Bottle-less point-of-use (POU) systems present one of the strongest growth opportunities in the global market, as noted by multiple industry forecasts. These systems eliminate plastic bottles by directly connecting to existing water lines, reducing manual handling, delivery dependency, and environmental footprint.

Waterlogic Holdings Limited, through corporate disclosures, highlights its proprietary Firewall UVC technology, capable of eliminating 99.99% of harmful microorganisms, positioning it as a trusted solution for businesses focused on water safety.

Sustainability-driven multinational companies increasingly prefer POU systems to align with their environmental commitments. Advancements in energy-efficient cooling and cost-effective filtration technologies have also made POU systems more affordable over the product lifecycle, accelerating adoption in offices, manufacturing units, and hospitality environments.

Smart IoT-Enabled Water Dispensers Are Transforming the Market with Real-Time Monitoring, Touchless Features, and Predictive Maintenance Capabilities

Smart water dispensers equipped with IoT capabilities offer a major revenue opportunity, transforming dispensers into intelligent devices that monitor water quality, predict maintenance needs, track consumption, and automate filter replacements.

These systems enable real-time performance management, which is valuable for commercial buildings and multi-location enterprises. Touchless operation, greatly emphasized after the pandemic, has become a key adoption driver in offices, hospitals, and hospitality centers.

Companies such as Honeywell International Inc. and Midea Group Co. Ltd., as noted in their product releases, are developing advanced smart dispensers featuring mobile app connectivity, temperature customization, and optimized energy consumption.

Integration with broader smart building ecosystems enhances operational efficiency for facility managers. With increasing digital transformation in commercial infrastructure, IoT-enabled dispensers are gaining popularity across global corporate environments.

Category-wise Analysis

Product Type Insights

Bottled water dispensers continue to lead the global market with nearly 70% share, supported by their low initial cost, simple setup, and well-developed delivery networks. Companies such as Primo Water Corporation strengthen this segment through extensive distribution, offering bottle-exchange services at around 26,500 retail locations, according to corporate updates.

These dispensers remain especially popular in emerging markets where water infrastructure is limited or water quality is uncertain. Recent improvements in cooling efficiency and product design are also helping retain demand. However, rising sustainability concerns and tightening plastic waste regulations are gradually encouraging consumers to shift toward more eco-friendly bottle-less systems.

End-user Insights

The commercial sector represents the largest share of the market, accounting for nearly 55% of global revenue, due to heavy usage across offices, educational institutions, hospitals, hotels, and industrial facilities. These establishments rely on dispensers to provide clean drinking water and meet workplace health and safety requirements.

Industrial applications, particularly in manufacturing and pharmaceutical facilities, driven by the need for high-capacity systems with advanced filtration. Residential adoption is strong in developed regions, where 40% of households use water dispensers, while developing markets show slower growth due to affordability challenges. However, rising incomes and growing health awareness in Latin America and Africa indicate significant long-term potential.

Regional Insights

North America Water Dispensers Market Trends

North America leads the global market with a 38% share, driven by advanced water infrastructure, strict regulatory standards, and high health consciousness. The U.S. Environmental Protection Agency (EPA) regulates over 90 contaminants, pushing consumers and businesses toward advanced filtration systems.

Major companies, including Primo Water Corporation and Whirlpool Corporation, dominate the region with strong distribution and technology-focused product portfolios.

The merger forming Primo Brands Corporation in 2024 expanded the region’s most extensive hydration network, featuring 26,500 water exchange locations and 23,500 refill stations, as per company statements. Growing sustainability initiatives are accelerating the shift from bottled to bottleless systems, especially among corporations with environmental commitments.

Additionally, the rising adoption of IoT-enabled dispensers in offices and healthcare facilities highlights a shift toward smart hydration solutions across the region.

Europe Water Dispensers Market Trends

Europe holds around 25% of global market share and demonstrates a strong preference for energy-efficient, eco-friendly hydration solutions. The region’s strict environmental regulations, especially concerning plastic usage and waste management, have accelerated the transition to bottle-less dispensers, which now represent 35% penetration, significantly higher than the global average.

Culligan International Company, supports the inauguration of its Italian headquarters in Bologna in December 2024 continue to expand across the continent. Western Europe, led by Germany, the United Kingdom, and France, shows the highest adoption of hygiene-focused systems featuring antimicrobial materials and touchless controls.

European Union packaging and sustainability directives further push manufacturers toward greener product portfolios. Meanwhile, Eastern Europe presents untapped potential due to lower penetration but rising demand in commercial sectors.

Asia Pacific Water Dispensers Market Trends

Asia Pacific is the fastest-growing market, with a projected 10.8% CAGR through 2033, driven by rapid urban development, rising incomes, and increased focus on safe drinking water. China and India are the largest contributors, with India recording exceptional growth of 14.6% CAGR, according to regional industry analyses.

Companies such as Midea Group and Haier Group Corporation, backed by strong domestic manufacturing and distribution strength, dominate the regional market.

Consumers in Asia Pacific prefer RO and UV filtration due to water quality challenges. India’s market outlook is evolving following the introduction of the BIS Quality Control Order (IS 17681:2022) for Bottled Water Dispensers in 2024, setting strict manufacturing standards.

The rapid rise of e-commerce platforms like Amazon and Alibaba has also supported direct-to-consumer sales. Growing middle-class adoption and commercial infrastructure expansion continue to drive market momentum.

Competitive Landscape

The global water dispensers market exhibits moderate concentration with several dominant international players complemented by numerous regional and niche competitors.

Major global manufacturers including Primo Water Corporation (now Primo Brands Corporation following 2024 merger with BlueTriton Brands), Culligan International Company, Waterlogic Holdings Limited, Whirlpool Corporation, Honeywell International Inc., Midea Group Co. Ltd., and A.O. Smith Corporation collectively maintain substantial market share through extensive distribution networks, established brand recognition, and continuous product innovation.

Key Market Developments:

- November 2024: Primo Brands Corporation completed its merger of Primo Water Corporation and BlueTriton Brands, forming a major North American beverage company trading as PRMB, integrating leading dispenser lines with brands like Poland Spring and Pure Life.

- December 2024: Culligan International opened its new Bologna headquarters, enhancing European operations with over 1,000 employees and supporting strong growth, including 220 million euros in Italian revenue in 2023, reflecting the region’s strategic market importance.

- September 2024: Culligan expanded its Nordic presence by acquiring BE WTR, adding premium beverages, advanced coffee machines, and patented dispensing technologies, reinforcing regional growth while preserving local brand identity and customer relationships.

Companies Covered in Water Dispensers Market

- Whirlpool Corporation

- Primo Water Corporation

- Honeywell International Inc.

- Culligan International Company

- Clover Co. Ltd.

- Waterlogic Holdings Limited

- Midea Group Co. Ltd.

- A.O. Smith Corporation

- Edgar's Water

- Brio Water Technology Inc.

- Haier Group Corporation

- Elkay Manufacturing Company

- Avalon Water

- Oasis International

- Glacier Water Technology

- Voltas Limited

- Blue Star Limited

- Aqua Optima

- LG Electronics

- Cosmetal S.r.l.

Frequently Asked Questions

The global water dispensers market is projected to reach US$ 3.1 Billion in 2026, growing from US$ 1.9 Billion in 2020 and expected to hit US$ 5.5 Billion by 2033 at a 8.7% CAGR.

Demand is driven by rising health awareness, urbanization, disposable incomes, post-pandemic hygiene focus, and regulatory emphasis on water quality, along with workplace wellness initiatives.

Bottled water dispensers dominate the market with around 70% share, while bottle-less point-of-use systems are the fastest-growing segment at roughly 9.5% CAGR.

North America leads with about 38% revenue share, whereas Asia Pacific is the fastest-growing region at 10.8% CAGR due to urbanization and rising incomes.

The biggest opportunities lie in IoT-enabled smart dispensers with predictive maintenance, energy optimization, and the growing adoption of sustainable bottle-less systems.

Key players include Primo Brands, Culligan, Waterlogic, Whirlpool, Honeywell, Midea, A.O. Smith, and regional leaders like Haier, Blue Star, and Voltas.