- Agrochemicals

- Water Soluble Fertilizers Market

Water Soluble Fertilizers Market Size, Share, and Growth Forecast 2026 - 2033

Water Soluble Fertilizers Market by Product Type (Nitrogenous, Phosphatic, Potassic, Micronutrient), Crop Type (Field Crop, Horticulture Crop, Turf & Ornaments, Other), Mode of Application (Foliar, Fertigation), and Regional Analysis for 2026 - 2033

Water Soluble Fertilizers Market Size and Trend Analysis

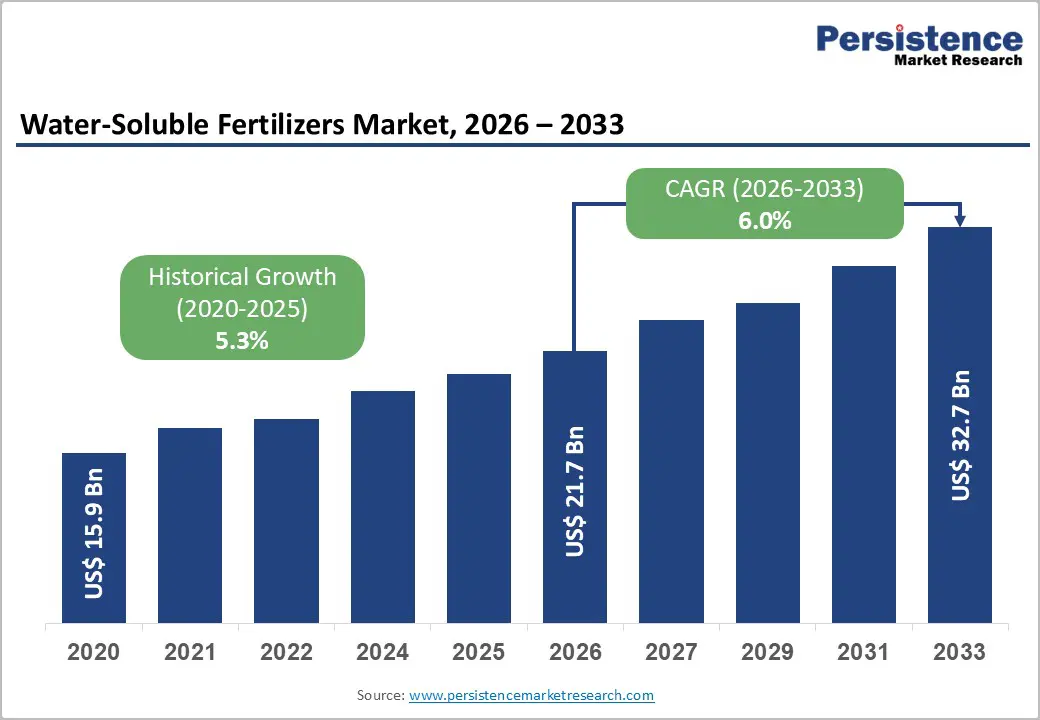

The global water soluble fertilizers market size is likely to be valued at US$23.0 billion in 2026 and is projected to reach US$32.7 billion by 2033, growing at a CAGR of 6.0% between 2026 and 2033.

The increasing adoption of precision agriculture techniques worldwide, that delivers efficient nutrient delivery to optimize crop yields amid shrinking arable land encourages the market growth. As global food production needs are projected to increase by 60% by 2050 for a a population of 9.7 billion, according to FAO estimates, this has prompted farmers to adopt water-soluble formulations for improved nutrient uptake.

Key Market Highlights

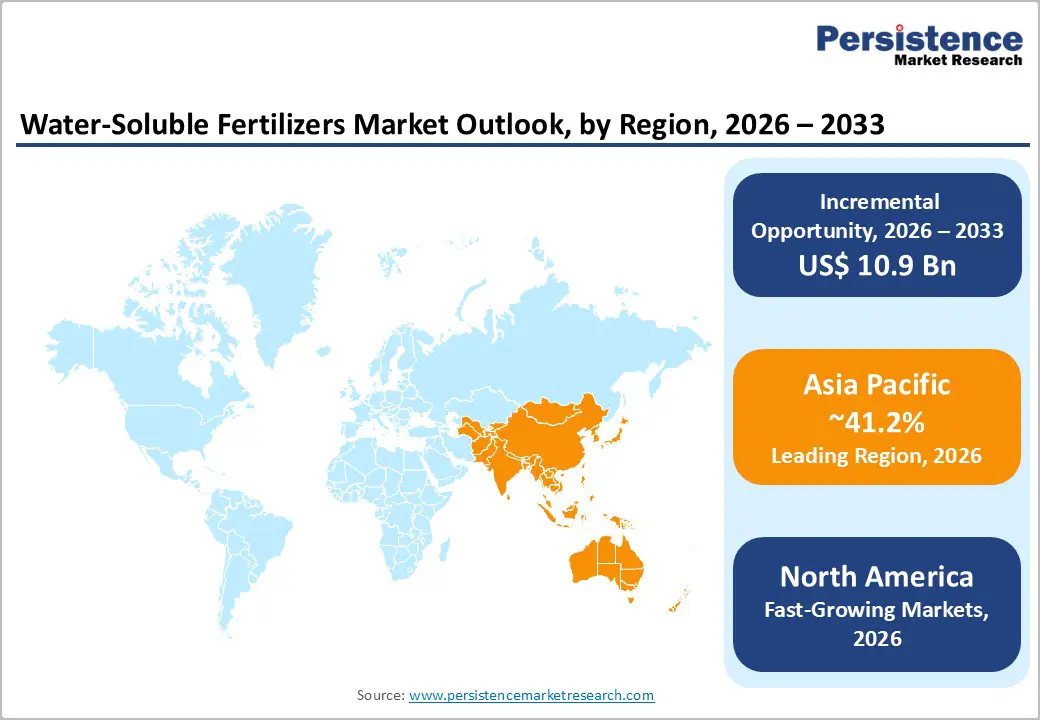

- Regional Leader: Asia Pacific dominates the water-soluble fertilizer market, with a 41.2% market share, driven by irrigation expansions in China and India and manufacturing advantages.

- Fastest-Growing Region: North America is the fastest-growing region in the water-soluble fertilizer market, driven by advanced precision farming and stringent EPA regulations, which drive efficient nutrient use in high-value U.S. crops and sustain leadership.

- Leading Segment: Field Crops dominate, with a 70% share, essential for global food staples like rice and wheat, where solubles optimize yields on vast arable lands amid nutrient-deficiency challenges.

- Fastest-Growing Segment: Horticultural Crops grow fastest, benefiting from rapid nutrient delivery in greenhouses and aligning with rising demand for premium fruits and florals in export-oriented economies.

- Growth Opportunities: Precision irrigation integration offers a key opportunity, enabling 90% nutrient-use efficiency and water savings, particularly in water-scarce regions, thereby supporting sustainable high-yield farming.

| Key Insights | Details |

|---|---|

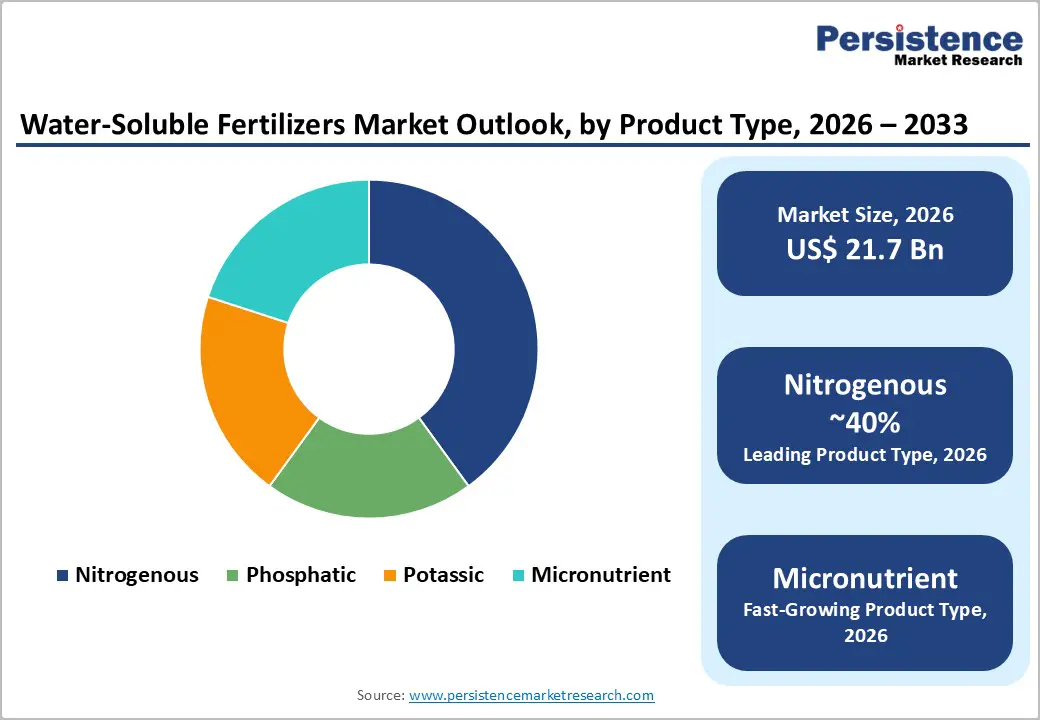

| Water Soluble Fertilizers Market Size (2026E) | US$21.7 Bn |

| Market Value Forecast (2033F) | US$32.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.0% |

| Historical Market Growth (2020 - 2025) | 5.3% |

Market Dynamics

Drivers - Rising Adoption of Precision Fertigation Systems for Enhanced Nutrient Use Efficiency

The integration of water-soluble fertilizers with modern fertigation and drip irrigation systems represents a transformative shift in agricultural practices, delivering nutrients directly to plant root zones with precision timing and dosage control. This approach significantly reduces nitrous oxide emissions compared to conventional irrigation methods while optimizing nutrient-use efficiency, making it particularly attractive in regions facing water scarcity. Research demonstrates that fertigation systems equipped with water-soluble formulations can boost crop yields by 20% to 30% while simultaneously reducing water consumption by up to 25%, creating a compelling value proposition for commercial farming operations.

The Food and Agriculture Organization (FAO) projects that irrigated food production must increase by over 60% by 2050, necessitating a 10% rise in agricultural water use, which further accelerates demand for efficient nutrient-delivery solutions like water-soluble fertilizers. The NPK Fertilizers Market parallels this trend, as balanced, soluble formulations address soil deficiencies more effectively than traditional methods, fostering widespread adoption among commercial growers seeking to boost productivity without environmental harm.

Expansion of High-Value Crop Cultivation

Global soil micronutrient deficiencies present an unprecedented opportunity for water-soluble fertilizer manufacturers, particularly those offering specialized micronutrient formulations. According to a study by the National Institutes of Health, Zinc deficiency affects approximately 49% of global soils, with India experiencing 35% soil zinc deficiency, while boron deficiency affects 31% of soils worldwide. These deficiencies cause documented crop yield losses ranging from 9% to 35%, depending on nutrient type and crop category.

The horticultural crop segment, encompassing fruits, vegetables, and specialty crops, represents the fastest-growing market subsector, with approximately 40% of horticultural cultivation now depending on water-soluble fertilizers for optimal nutrient delivery. Vertical farming and hydroponics segments are experiencing exceptional growth, creating specialized demand for water-soluble nutrients with precise micronutrient enrichment and chelated formulations. Companies like IFFCO Ltd. reported 47% year-over-year growth in nano-fertilizer sales in 2024-2025, demonstrating farmers' recognition of advanced micronutrient delivery technologies. The convergence of premium crop production demands and soil nutrient depletion creates sustainable market expansion opportunities.

Restraints - Raw Material Price Volatility and Rising Production Costs

The adoption of water-soluble fertilizers requires sophisticated fertigation equipment and irrigation infrastructure, creating substantial capital barriers for smallholder farmers in developing economies. World Bank data confirms fertilizer prices have risen substantially since 2022 due to supply disruptions and increased input costs, creating margin compression for manufacturers. The production of nitrogen-containing water-soluble fertilizers depends heavily on natural gas as a feedstock, making the industry vulnerable to energy market volatility.

Geopolitical disruptions, including the Russia-Ukraine conflict and Tariff war, have constrained potash and phosphate fertilizer supply chains, exacerbating cost structures. Regional price variations create competitive disadvantages for manufacturers in higher-cost jurisdictions, particularly impacting smaller enterprises and regional producers. These cost pressures translate into premium pricing for end-users, creating adoption barriers in price-sensitive commodity crop segments dominated by large-scale grain producers in regions with limited irrigation infrastructure.

Import Dependency and Supply Chain Vulnerabilities in Key Agricultural Markets

Major agricultural economies exhibit significant reliance on imported water-soluble fertilizer products, creating supply chain vulnerabilities and price volatility concerns. India imports a major quantity of water-soluble fertilizers from China and other countries, with these products primarily serving cash and horticultural crop segments that are not covered under the government's Nutrient-Based Subsidy (NBS) Scheme. This import dependency exposes farmers to international price fluctuations and potential supply disruptions, as evidenced by concerns regarding China's export policies affecting Indian farmers' access to specialty fertilizer formulations.

Furthermore, the Soluble Fertilizer Industry Association reported that thousands of biostimulant products currently marketed lack government approval, as required testing is conducted at government-designated universities and evaluated by the Indian Council of Agricultural Research. The compliance transition period, estimated at 3-4 years, poses existential threats to smaller manufacturers lacking the resources to navigate regulations, potentially consolidating market share toward larger enterprises. The absence of subsidies for water-soluble fertilizers, unlike conventional urea and NPK products, further limits affordability and adoption rates among price-sensitive farming communities in developing regions.

Opportunity - Advancements in Sustainable Irrigation Technologies

Integrating emerging irrigation technologies offers a significant opportunity, as nano-fertilization systems have proven effective in enhancing nutrient uptake efficiency at application rates 30-40% lower than those of conventional water-soluble formulations. Water-soluble fertilizers excel in these setups, offering 90% nutrient use efficiency and reducing leaching by 50%, ideal for water-stressed areas.

The global shift toward urban agriculture and vertical farming in densely populated regions of North America and the European Union, with emerging adoption patterns in urban Asia Pacific, is driving demand for premium soluble specialty formulations. These controlled environment systems require precise nutrient management capabilities that water-soluble fertilizers uniquely provide, enabling year-round crop production with minimal environmental footprint.

Government Policies Promoting Efficient Fertilization

Supportive policies in emerging markets offer substantial potential, with subsidies for precision tools rising by 15% in India and China as per national agricultural ministries. These initiatives aim to reduce fertilizer subsidies for inefficient products, favoring water-soluble options that comply with environmental standards such as the EU's Farm to Fork Strategy, aiming for 20% less nutrient pollution.

Manufacturers are using these opportunities to expand their market presence by forming strategic alliances to penetrate the growing agricultural market. Haifa Group's collaborative agreement with Deepak Fertilizers in India, signed in March 2024, exemplifies this strategic approach, combining international technological expertise with local market knowledge to deliver advanced crop nutrition solutions customized to regional agricultural requirements. Linking to the Phosphate Fertilizers Market, low-cadmium soluble phosphates meet regulatory demands, positioning manufacturers to secure contracts in policy-driven expansions.

Category-wise Analysis

Product Type Insights

Nitrogenous fertilizers lead the product type category in the Water-Soluble Fertilizers Market, commanding approximately 40% market share due to their critical role in vegetative growth and protein synthesis for major crops. Nitrogen-based formulations, including ammonium nitrate, calcium nitrate, urea, and potassium nitrate, account for the largest share of applications because nitrogen is the primary macronutrient limiting crop yield across most agricultural ecosystems.

The water solubility of nitrogenous compounds enables precise dosing and immediate plant availability, making these products essential for high-value crops that require frequent nutrient applications during critical growth stages. Major manufacturers such as Yara International, Nutrien Ltd., and The Mosaic Company have developed specialized portfolios of water-soluble nitrogenous fertilizers that cater to diverse crop requirements across field crops, horticultural applications, and specialty agricultural segments.

Crop Type Insights

Field Crops dominate the crop type segmentation, holding about 70% of the market share in water-soluble fertilizers, driven by the extensive cultivation of staples like wheat, rice, and maize across continents. This dominance reflects the massive acreage devoted to commodity grain production across North America, Asia-Pacific, and Europe, where mechanized farming systems facilitate the adoption of fertigation through drip and micro-sprinkler infrastructure. In the United States, 78.6% of corn and soybean farmers prioritize fertilizer efficiency, leading to increased implementation of variable-rate pivot fertigation systems that rely on water-soluble nutrient formulations.

Large-scale field crop operations increasingly adopt water-soluble fertilizer applications due to variable-rate technology capabilities allowing site-specific nutrient dosing, directly optimizing nutrient use efficiency while minimizing environmental compliance risks associated with nutrient runoff. The Organic Fertilizer Market is increasingly intersecting with water-soluble fertilizer applications as farmers seek integrated soil health solutions.

Mode of Application Insights

Fertigation is the dominant application method, with an estimated market share of 64%, reflecting the superior efficiency and precision of delivering nutrients directly through irrigation water to plant root zones. This application technique completely dissolves water-soluble fertilizers in irrigation systems, enabling accurate nutrient delivery that significantly reduces waste, minimizes environmental runoff, and optimizes crop productivity compared to conventional broadcast application methods.

Research from the COALA project in Australia demonstrated that precision fertigation systems increased irrigation efficiency by 20%, conserving water resources and enhancing crop yields. Fertigation's market dominance is reinforced by demonstrated advantages, including uniform nutrient distribution across plant populations, reduced nutrient application windows that match specific crop physiological stages, and water conservation benefits of 20-30% compared to flood irrigation combined with conventional granular fertilizer applications.

Regional Insights

North America Water Soluble Fertilizers Market Trends

North America leads in innovative applications of water-soluble fertilizers, with the U.S. dominating through advanced precision farming ecosystems. The EPA enforces strict nutrient management under the Clean Water Act, promoting solubles to curb runoff from the Midwest corn belts. Greenhouse operations in California, spanning 1,000 acres, rely on fertigation for high-value produce, enhancing yields by 20% amid water restrictions.

The U.S. market benefits from regulations supporting sustainable agriculture, farmer education, and strong distribution networks connecting fertilizer manufacturers to growers. Nitrogenous water-soluble fertilizers represent 37.6% of North America's market share, primarily due to high-yield corn and wheat production in the Midwest and Great Plains. With over 320 commercial vertical farms, hydroponic cultivation has driven water-soluble nutrient demand to grow 22% since 2021, particularly in urban centers like Chicago, New York, and Denver.

Europe Water-Soluble Fertilizers Market Trends

Europe's market thrives on harmonized regulations, with Germany, the U.K., France, and Spain excelling in performance under the EU Fertilizing Products Regulation, effective 2022, which mandates low-heavy-metal solubles. France's viticulture benefits from foliar nitrogen, boosting grape quality amid climate challenges.

Precision agriculture adoption across European farming systems is facilitated by German technical expertise in agricultural equipment, UK sustainable farming initiatives, and French expertise in viticulture nutrient management. Eastern European nations, including Poland, Romania, and Hungary, exhibit accelerated growth trajectories at higher compound annual growth rates as agricultural modernization initiatives and European Union subsidy programs drive adoption of advanced fertilizer technologies. Northern European regions, while smaller in absolute market size, demonstrate steady demand for specialized formulations supporting protected cultivation and high-value crop production.

Asia Pacific Water Soluble Fertilizers Market Trends

Asia Pacific dominates the water-soluble fertilizer market, with 41.2% of global share, led by China, India, Japan, and the ASEAN nations, leveraging manufacturing strengths to drive cost-effective production. China leads regional consumption with aggressive government subsidies offering 30% purchase rebates on registered water-soluble products, catalyzing annual domestic sales growth of 18% and establishing the country as a critical market for international suppliers. Israel Chemicals Ltd. (ICL) recognized China as a key strategic region, with its soluble fertilizer products achieving market leadership status and the company securing a substantial US$170 million distribution agreement with AMP Holdings in August 2024 to strengthen its position in the premium specialty fertilizer segment.

India presents significant growth potential with annual water-soluble fertilizer consumption reaching approximately 3.35 lakh tons during the 2023-24 fiscal year, primarily serving cash crop and horticultural applications. The Indian market is characterized by substantial import dependency from China and other countries, with water-soluble fertilizers operating outside the government's Nutrient-Based Subsidy (NBS) Scheme, creating both challenges and opportunities for market participants.

Competitive Landscape

The global water soluble fertilizers market exhibits a moderately consolidated structure, with top players controlling 60% share through integrated supply chains and R&D investments. Leaders pursue expansion via mergers and capacity builds, focusing on low-emission formulations to meet EU and U.S. standards. R&D trends emphasize bio-compatible blends, with 20% of innovations targeting micronutrient chelates for climate-resilient crops. Key differentiators include purity levels above 99% and customized NPK ratios, enabling premium pricing. Emerging models such as subscription-based precision kits and digital dosing apps are gaining traction, fragmenting lower tiers while consolidating high-end segments around sustainability.

Key Market Developments:

- January 2025: Yara International launched a new nitrate-based soluble fertilizer optimized for fertigation in saline soils, enhancing uptake by 25% in field trials across Europe.

- March 2024: Haifa Group established a collaborative partnership with Deepak Fertilizers to expand operations in India, providing Indian farmers with advanced plant nutrition solutions and precision Nutrigation practices focused on resource preservation and yield enhancement.

- August 2024: Israel Chemicals Ltd. (ICL) announced a strategic distribution agreement worth approximately US$170 million with AMP Holdings to expand its specialty soluble fertilizer business in China, reinforcing the company's market leadership position in premium irrigation-based fertilizers.

Top Companies in Water Water-Soluble Fertilizers Market

- Yara International (Norway), a global leader in nitrogen solutions, commands influence through its extensive R&D portfolio, generating US$15 Bn in annual revenues with 30% from solubles. Its maturity in fertigation tech and strong Asia Pacific presence drive market share via innovative, low-carbon products.

- Nutrien Ltd. (Canada), the largest potash producer, excels in integrated supply with US$25 Bn revenues, leveraging scale for cost efficiencies in field crop solubles. Portfolio strength in NPK blends and U.S. distribution networks solidifies its dominance in North American volumes.

- Israel Chemicals Company (Israel), renowned for phosphates, holds key influence with US$7 Bn revenues, focusing on high-purity micronutrients. Its R&D in chelated formulas and Mediterranean export hubs enhances maturity, capturing premium segments in Europe and horticulture.

Companies Covered in Water Soluble Fertilizers Market

- Nutrien Ltd.

- Israel Chemical Company

- Yara International

- Haifa Chemicals Ltd.

- The Mosaic Company

- Coromandal International Ltd.

- IFFCO Ltd.

- K+S Aktiengesellschaft

- Agafert

- Aries Agro Ltd.

- Azoty Group

- Hebei Monband Water Soluble Fertilizers Co., Ltd.

- EuroChem Group

Frequently Asked Questions

The global water soluble fertilizers market is valued at US$21.7 Bn in 2026 and expected to reach US$32.7 Bn by 2033, reflecting steady expansion driven by precision agriculture demands.

Key drivers include precision nutrient management and high-value crop expansion, with fertigation enabling 90% efficiency and supporting 60% global food production growth by 2050, as per FAO.

Nitrogenous leads with 40% share, essential for vegetative growth in cereals, offering rapid uptake that boosts yields by 15-20% in deficient soils worldwide.

Asia Pacific leads the market, with China offering 30% government purchase rebates spurring 18% annual sales growth, while India's consumption reached 3.35 lakh tons in 2023-24, primarily serving cash crop and horticultural applications.

Advancements in sustainable irrigation tech provide an opportunity to integrate solubles for 50% leaching reduction, especially in the Asia Pacific's expanding drip systems by 2030.

Leading players include Yara International, Nutrien Ltd., and Israel Chemicals Company, commanding 60% share through R&D in NPK blends and global distribution networks.