- Animal Feed & Additives

- Soybean Rust Control Market

Soybean Rust Control Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Soybean Rust Control Market by Form (Powder, Liquid), by Species (Phakopsora pachyrhizi, Phakopsora meibomiae), by Fungicide (Protective, Curative), and Regional Analysis from 2025 to 2032

Soybean Rust Control Market Share and Trends Analysis

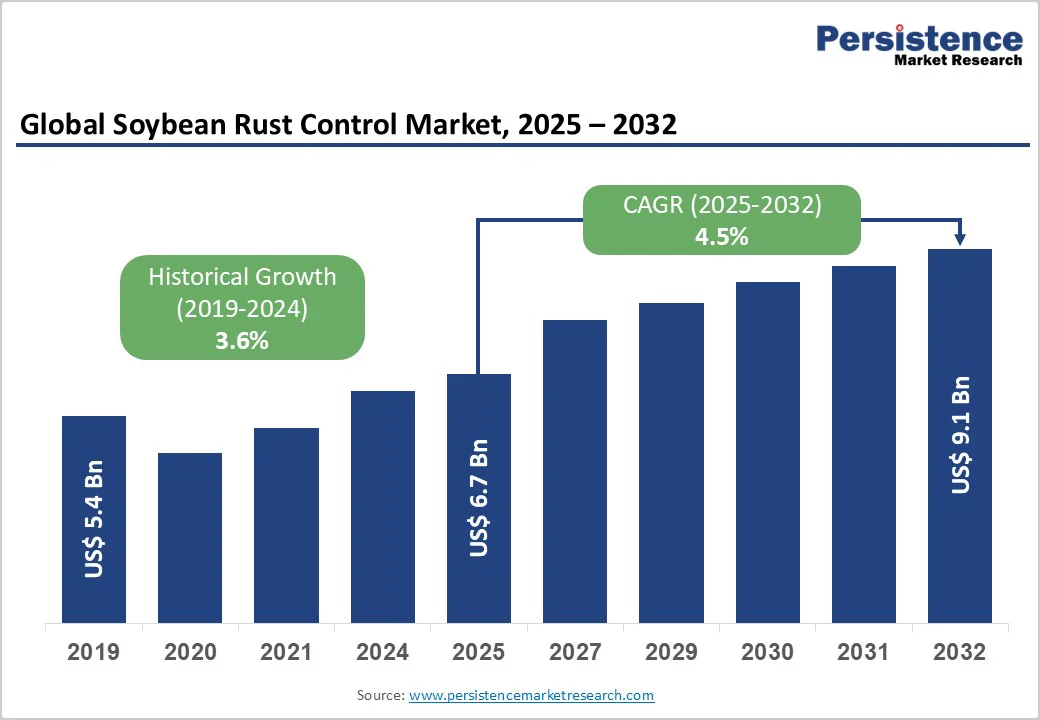

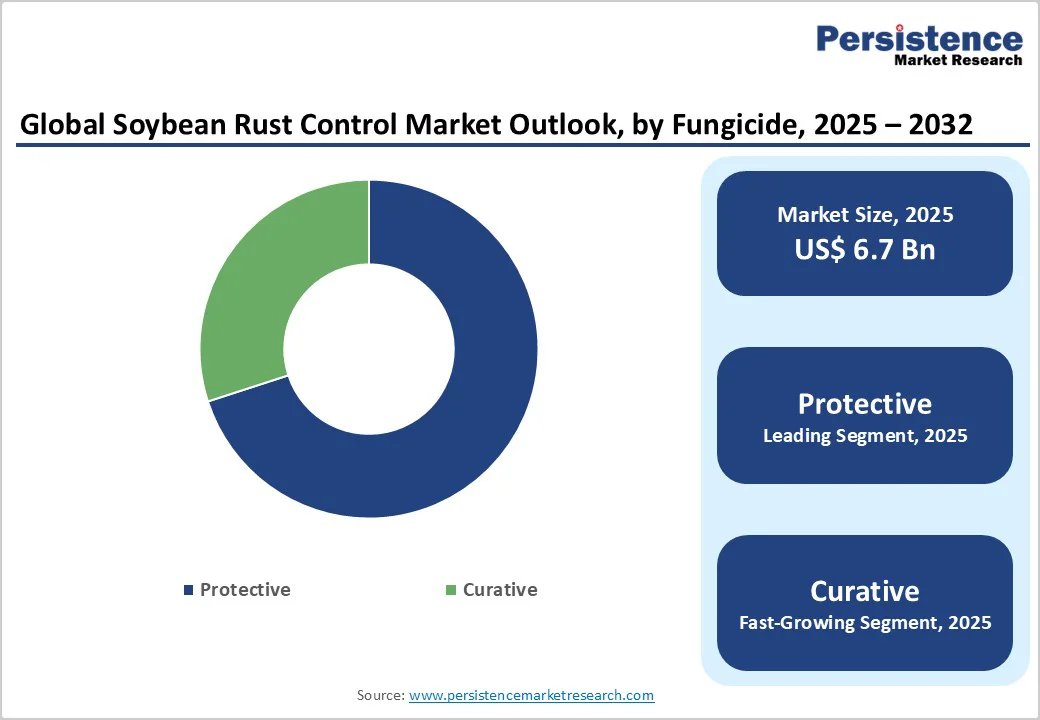

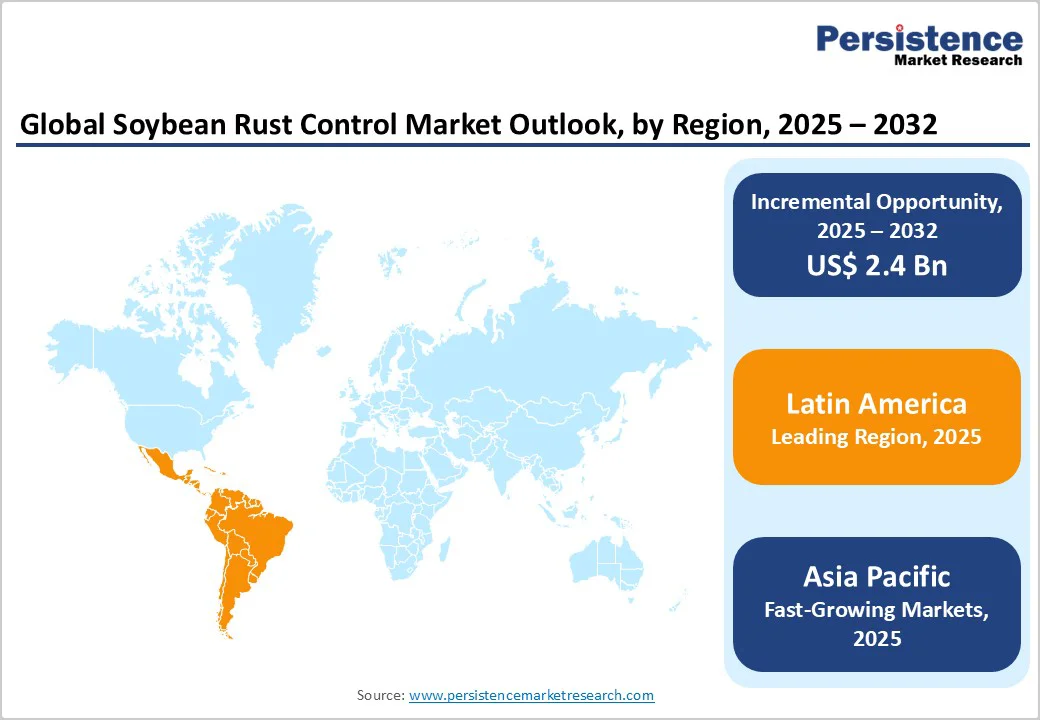

The global soybean rust control market size is valued US$ 6.7 billion in 2025 to US$ 9.1 billion by 2032. The market is projected to record a CAGR of 4.5% during the forecast period from 2025 to 2032.

The global soybean rust battle is intensifying as growers confront faster pathogen cycles, shifting climates, and rising production targets. Innovation is accelerating across fungicides, resistant genetics, and digital disease-management systems, reshaping how producers secure yield stability.

Key Industry Highlights

- Leading Region: Latin America dominates the market, holding a major share due to Brazil, Argentina, and Paraguay’s large-scale soybean output and continuous investment in multi-mode fungicide programs, resistant cultivars, and climate-adaptive rust management systems.

- Fastest-Growing Region: Asia Pacific is set for the strongest growth momentum, supported by India’s structured spray programs, China’s adoption of region-specific resistant varieties, and rapid integration of AI-based monitoring and precision spraying tools.

- Fastest-Growing Fungicide Segment: Curative fungicides are projected to surge at a CAGR of 7.8%, driven by farmers’ need for rapid recovery during high-pressure rust seasons and their increasing reliance on intervention-ready solutions to complement routine protective sprays.

- Dominant Species Segment: Phakopsora pachyrhizi leads with about 88% market share, driven by its aggressive biology and severe yield impact, while Phakopsora meibomiae remains relevant mainly for monitoring and evolutionary risk assessment.

- Growth Indicators: Rising global soybean demand is pushing farmers to intensify rust protection strategies as production pressures escalate across protein and biofuel value chains, increasing the uptake of fungicides, resistant seed genetics, and integrated disease-management tools.

- Key Opportunities: Partnering with seed companies to bundle rust-tolerant genetics with tailored crop protection packages unlocks high-value differentiation, enabling season-long protection while reducing dependency on frequent spray cycles.

- Key Developments: In June 2025, BASF filed regulatory dossiers for its new Adapzo Active fungicide in Brazil and Paraguay, with Bolivia next in line, strengthening options against Asian soybean rust. In March 2025, 2Blades and Bayer formed a strategic collaboration to accelerate durable resistance solutions and reinforce long-term crop-protection innovation pipelines.

| Key Insights | Details |

|---|---|

| Global Soybean Rust Control Market Size (2025E) | US$ 6.7 Bn |

| Market Value Forecast (2032F) | US$ 9.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.6% |

Market Dynamics

Driver - Rising Global Soybean Demand is Pushing Farmers to Protect Yields From Rust Outbreaks

Rising global demand for soybeans is pushing farmers to aggressively protect yields against rust outbreaks, fueling growth in the soybean rust control market. According to USDA data, 2024/25 global soybean production hit about 420.9 million metric tons, underscoring how critical disease management is for output security.

As rust, especially Asian and American soybean rust, threatens profits, growers are investing in robust fungicides, resistant seed varieties, and integrated disease-management systems. This is particularly true for major producers racing to meet protein and oil demand from the feed and biofuel sectors. As a result, the fungicide and biocontrol industry is scaling rapidly to deliver effective, market-aligned rust solutions.

Restraint- High Application Costs Make Multiple Spray Rounds Unaffordable for Small And Mid-Size Farmers

High application costs are becoming a critical barrier in soybean rust management, making repeated spray cycles increasingly unaffordable for small and mid-size farmers. Many growers operate on thin margins, and the need for multiple fungicide rounds during high-pressure rust seasons strains their operating budgets.

Rising prices of active ingredients, fuel, and farm labor further inflate the total cost per hectare, forcing farmers to delay or reduce treatments even when disease pressure intensifies. Limited access to credit and inconsistent subsidy support in several regions deepen this challenge.

As a result, rust outbreaks spread faster in under-treated fields, amplifying regional yield losses and widening the performance gap between large commercial farms and resource-constrained producers.

Opportunity - Partnering with seed companies to bundle rust-tolerant genetics with crop protection solutions

Partnering with seed companies presents a compelling pathway for innovation as soybean producers search for more resilient rust-management strategies. Bundling rust-tolerant genetics with crop protection solutions creates an integrated value proposition that appeals to farmers seeking both security and cost efficiency.

Seed firms are increasingly developing varieties with partial resistance traits, and aligning these with tailored fungicide programs, biological protectants, or seed-treatment packages strengthens overall field performance. This model allows companies to deliver season-long protection while reducing growers’ dependence on frequent spray cycles.

Startups benefit from these alliances by gaining access to established seed distribution networks, accelerating the adoption of their technologies. As resistance evolution becomes a rising threat, genetics-plus-chemistry partnerships position the industry to offer durable and scalable rust-control systems.

Category-wise Analysis

By Species Insights

Phakopsora pachyrhizi accounts for 88% share as of 2025, and its dominance reflects the aggressive biology and rapid spread, making it the most destructive rust species affecting global soybean production. Its ability to produce massive spore loads, survive across seasons, and adapt to shifting climatic conditions forces farmers to rely heavily on fungicides and resistant genetics.

This pathogen drives most control-related investments because outbreaks can cut yields drastically when unmanaged. Phakopsora meibomiae, while present in limited regions, exhibits far lower virulence and spreads more slowly, making it less economically damaging.

It is primarily monitored for its potential to evolve or hybridize, but it currently accounts for minimal intervention demand. The overwhelming threat posed by P. pachyrhizi as the primary target in rust-control strategies worldwide.

By Fungicide Insights

Curative fungicides are projected to grow at a CAGR of 7.8% during the forecast period, driven by growers shifting toward rapid-response disease management as infection pressures intensify across major crop systems. Their ability to halt fungal development after symptoms appear gives farmers a critical recovery window, especially in high-value crops where outbreaks can escalate quickly.

This performance edge is becoming increasingly vital as climate variability accelerates pathogen cycles. Protective fungicides continue to dominate baseline disease prevention due to their cost-effectiveness and strong fit in routine spray programs.

However, rising resistance concerns and the need for flexible, intervention-ready solutions are pushing curative formulations into faster adoption, positioning them as an essential complement to standard protective treatments in integrated crop protection strategies.

Region-wise Insights

Latin America Soybean Rust Control Market Trends

Latin America holds approximately 52% market share in the global Soybean Rust Control Market, reflecting its central role in global soybean supply and its constant battle against aggressive rust outbreaks. Brazil is advancing toward multi-stacked resistant cultivars and increasingly integrating digital scouting platforms to optimize spray timing.

Argentina is seeing rapid adoption of mixed-mode fungicide programs as growers push to counter evolving pathogen strains and stabilize yields under unpredictable weather. Paraguay is accelerating its shift toward preventive spraying calendars supported by early-warning systems and broader use of biological enhancers to reduce chemical load.

Across the region, stronger emphasis on resistance stewardship, real-time field diagnostics, and climate-adaptive disease forecasting is reshaping how farmers tackle this high-impact threat.

Asia Pacific Soybean Rust Control Market Trends

Asia Pacific soybean rust control market is expected to grow at a CAGR of 6.7%, driven by escalating disease pressure across rapidly expanding soybean belts and an industry-wide push for more resilient production systems. India is moving toward structured spray programs supported by state-led extension services, encouraging farmers to combine early detection with rotation-ready fungicide mixes.

China is accelerating the deployment of region-specific resistant varieties and integrating AI-based crop monitoring tools across major producing provinces. Southeast Asian growers are adopting low-drift spraying technologies to improve field coverage under humid, high-risk disease conditions.

Across the region, stronger collaboration between seed developers, ag-tech startups, and chemical manufacturers is shaping a more predictive, precision-focused approach to rust management, improving crop security in highly variable climates.

Market Competitive Landscape

The competitive landscape of the global Soybean Rust Control Market remains moderately consolidated, with a tight circle of agrochemical giants shaping product innovation, resistance-management strategies, and large-scale field deployment. Leading companies are strengthening portfolios by advancing next-generation triazoles, SDHIs, and biologicals backed by stronger regulatory compliance and certifications tied to environmental stewardship.

Many players are upgrading formulation technologies to improve leaf adhesion, rainfastness, and curative reach, while investing in digital scouting tools that integrate seamlessly with growers’ existing extension systems. Regulatory bodies across major soybean-producing nations are tightening residue and resistance-management protocols, pushing firms toward more transparent testing pipelines.

R&D partnerships with universities continue to accelerate pathogen-tracking models, helping farmers gain confidence in adopting integrated solutions aligned with evolving disease dynamics.

Key Industry Developments:

- In June 2025, BASF initiated the registration process for its new fungicide innovation Adapzo Active (Flufenoxadiazam) to combat Asian soybean rust. Regulatory dossiers were submitted in Brazil and Paraguay, with Bolivia next in line, signaling BASF’s push to strengthen disease-control options in major soybean-producing regions.

- In March 2025, 2Blades and Bayer formed a strategic partnership to advance durable resistance solutions against Soybean Rust, a major threat to global soybean yields. The collaboration strengthens crop-protection innovation pipelines and supports long-term resilience in soybean farming systems.

Companies Covered in Soybean Rust Control Market

- Bayer AG

- BASF SE

- Syngenta AG

- Corteva Agriscience

- FMC Corporation

- Sumitomo Chemical

- UPL Limited

- Nufarm Limited

- ADAMA Ltd.

- Others

Frequently Asked Questions

The global Soybean Rust Control market is projected to be valued at US$ 6.7 Bn in 2025.

Growing worldwide demand for soybeans is compelling farmers to safeguard their crops from rust-related yield losses, accelerating the need for effective soybean rust control solutions across global markets.

The global Soybean Rust Control market is poised to witness a CAGR of 4.5% between 2025 and 2032.

A major market opportunity emerges from collaborating with seed developers to integrate rust-tolerant genetics with complementary crop protection solutions.

Major players in the global Soybean Rust Control market include Bayer AG, BASF SE, Syngenta AG, Corteva Agriscience, FMC Corporation, Sumitomo Chemical, and others