- Food Ingredients & Additives

- Organic Soybean Market

Organic Soybean Market Size, Share, and Growth Forecast, 2026 – 2033

Organic Soybean Market by Product Type (Whole Soybeans, Soybean Meal, Soybean Oil, Others), Application (Food & Beverages, Animal Feed & Pet Food, Personal Care & Cosmetics, Pharmaceuticals, Others), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retailers, Direct Sales, Others), and Regional Analysis for 2026-2033

Organic Soybean Market Share and Trends Analysis

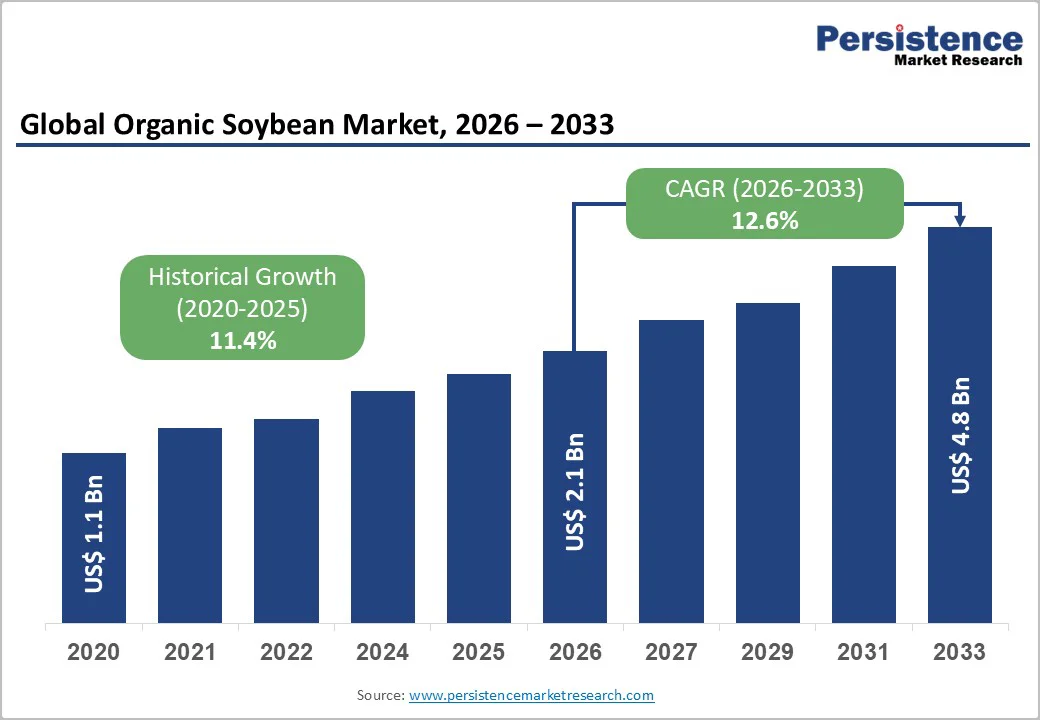

The global organic soybean market size is likely to be valued at US$ 2.1 billion in 2026, and is estimated to reach US$ 4.8 billion by 2033, growing at a CAGR of 12.6% during the forecast period 2026−2033. Primary growth is driven by rising consumer demand for organic and non-Genetically Modified Organism (GMO) food and feed products, increasing adoption of plant-based diets, and supportive regulatory and sustainability initiatives that promote organic farming. Supply-side improvements in organic farming practices and yield efficiency, coupled with expansion into new applications such as cosmetics and nutraceuticals, further underpin this trajectory.

Key Industry Highlights

- Dominant Region: Asia Pacific is expected to lead the market with a 30% share in 2026, driven by high rate of urbanization and government support for certified organic products.

- Fastest-growing Regional Market: North America is poised to be the fastest-growing regional market through 2033, fueled by rising demand for plant-based and sustainably sourced organic food products.

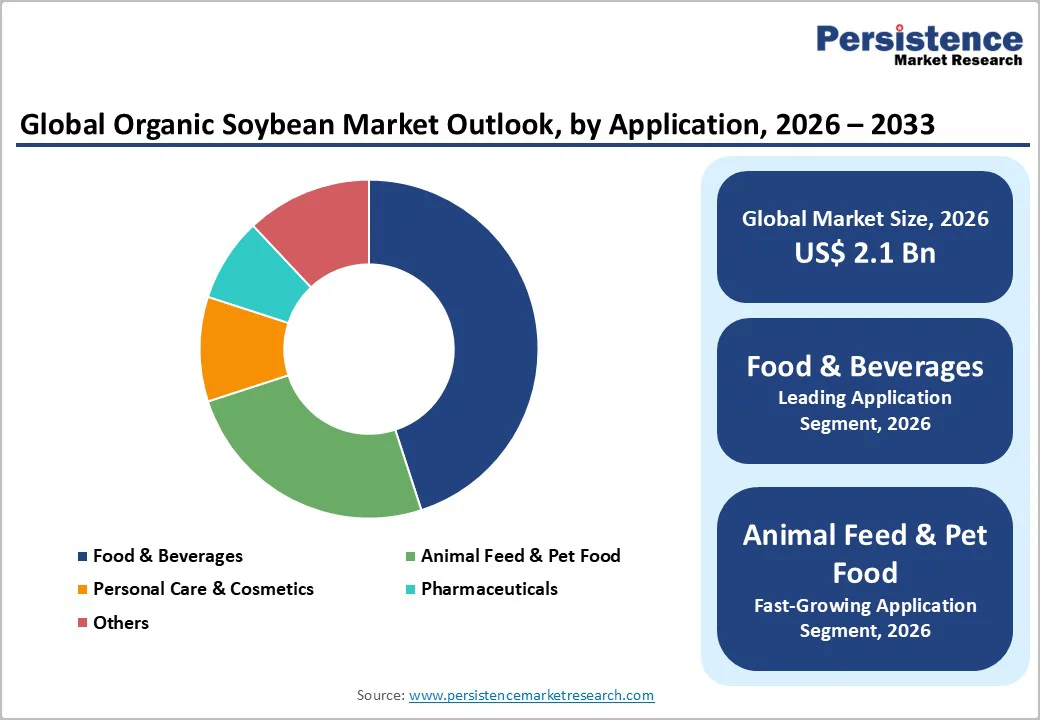

- Leading Application: The food & beverages segment is slated to lead with a 45% revenue share in 2026, driven by a strong demand for organic soybeans in plant-based protein products.

- Fastest-growing Application: The animal feed and pet food segment is likely to the fastest-growing through 2033, boosted by a widening preference for certified organic feed and high-protein meals.

| Key Insights | Details |

|---|---|

| Organic Soybean Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.4 % |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Plant-Based Proteins

Rising demand for plant-based proteins steers market expansion as consumers move toward cleaner nutrition profiles aligned with wellness-focused lifestyles. Organic soybean products deliver high-quality protein with a complete amino acid composition, positioning them as a preferred substitute for animal-derived proteins. Sustainability expectations reinforce this shift, as plant-derived proteins support lower environmental burdens and align with responsible consumption patterns. A consumer study by the International Food Information Council indicates that 24% of respondents increased their intake of plant-based proteins, demonstrating measurable behavioural transition toward plant-forward diets.

This shift influences sourcing strategies across food processors, beverage manufacturers, and alternative protein brands seeking dependable organic protein inputs for product development. Soy-based ingredients integrate effectively into meat analogues, fortified beverages, dairy alternatives, and functional nutrition formats, supporting broad innovation across manufacturing ecosystems. Regulatory encouragement for organic cultivation strengthens supply alignment with clean-label positioning and certification-driven differentiation sought by global brands. These dynamics create sustained procurement momentum for organic protein inputs, reinforcing long-term growth supported by consumer preferences, responsible sourcing goals, and enhanced utilisation of soy-derived raw materials across diversified value chains.

Cost Barriers to Impact Market Growth

Higher production costs act as a significant restraint as organic cultivation demands specialized inputs, certified processes, and stricter compliance. Organic seeds, bio-fertilizers, and natural pest-management solutions carry a higher price tag compared to conventional alternatives. Farmers must meet certification standards, maintain segregated supply chains, and invest in labor-intensive field management. These activities elevate the cost per acre and increase operational complexity. The absence of synthetic chemicals leads to lower yield consistency, raising the cost of producing each unit of output.

Extended transition periods further add to the financial burden. Land must remain chemical-free for a defined duration before organic status is granted, limiting revenue during the conversion phase. Producers face higher risks linked to weather variability and pest pressure, pushing them to allocate more resources to monitoring and manual interventions. These elevated structural costs make price competitiveness challenging, especially in markets where buyers are highly price-sensitive. Such cost dynamics slow expansion, reduce profitability, and create entry barriers for smaller farming enterprises.

Expansion into Emerging Plant-Based Nutraceuticals

Expansion into emerging plant-based nutraceuticals represents a strategic opportunity as consumer preferences shift toward clean-label, functional ingredients that support preventive health. Organic soybean derivatives align with this evolution through their natural protein profile, bioactive compounds and suitability for fortified supplements. Rising interest in immune support, metabolic wellness and sustainable nutrition drives formulators to select inputs that offer traceability and purity, giving organically cultivated soybean ingredients a competitive edge in premium nutraceutical portfolios.

Growing investment in functional food innovation strengthens this momentum, as brands integrate botanical and plant-derived elements into powders, beverages and capsule-based products. Organic soybean inputs deliver formulation versatility, supported by consistent supply chains and growing certification standards that meet evolving regulatory expectations. This convergence of health-focused consumption, product innovation and quality-driven sourcing positions emerging nutraceutical applications as a high-value growth avenue for industry stakeholders.

Category-wise Analysis

Product Type Insights

Whole organic soybeans are expected to remain the leading segment in 2026 with a projected 35% revenue share, supported by their broad utility across food manufacturing, traditional dietary patterns and high-protein product development. Their unprocessed form preserves full nutritional value, driving strong adoption in premium health foods, clean-label formulations and plant-forward product lines. Established consumer familiarity in North America and Europe reinforces sustained demand, while reliable supply structures and long-term preference for minimally processed ingredients strengthen their position as the dominant contributor to overall segment revenue.

Soybean oil is likely to be the fastest-growing segment through 2033, aided by expanding use in cooking applications, personal care formulations and specialized wellness products. Its favorable fatty acid profile aligns with rising interest in heart-healthy oils and plant-derived alternatives, while growth in vegan and flexitarian lifestyles increases formulation uptake across sauces, dressings and packaged foods. Broad applicability in skincare, haircare and natural beauty solutions further elevates its market trajectory. Strong alignment with sustainability-driven purchasing and the shift toward plant-based consumption patterns positions soybean oil for accelerated expansion through the forecast period, increasing its contribution to total market value in the years ahead.

Application Insights

The food & beverages segment is poised to dominate in 2026 with an anticipated 45% of the organic soybean market revenue share, powered by strong utilization of organic soybean inputs in tofu, soymilk, fermented foods and plant-based protein formats. Rising consumer alignment with clean-label nutrition, lactose-free diets and sustainable protein sources reinforces consistent demand across retail and foodservice channels. Product developers prioritize organic soybean ingredients for their nutritional density, functionality and compatibility with plant-forward innovation. This segment maintains its leadership position as dietary shifts, regulatory emphasis on healthier consumption and expanding product portfolios strengthen long-term market relevance.

The animal feed and pet food segment is anticipated to grow the fastest from 2026 to 2033, driven by expanding requirements for certified organic feed within poultry, dairy and livestock operations. Growth in organic meat and dairy production elevates the need for traceable, high-protein feed inputs that align with evolving certification standards. Pet food manufacturers integrate organic soybean meal to support premium positioning and wellness-driven purchasing behavior among pet owners. Policy incentives supporting organic farming strengthen supply visibility, positioning this segment for accelerated expansion and enabling the category to advance toward a significantly higher forecast value within the assessment horizon.

Distribution Channel Insights

Supermarkets and hypermarkets are likely to stand as the leading distribution channel in 2026 with an expected 40% share, driven by their broad accessibility, extensive product visibility and strong influence on mainstream purchasing patterns. These formats offer consumers convenient access to a wide assortment of organic soybean products, supported by established retail networks and high footfall in urban regions. Shelf presence, in-store promotions and trusted retail branding strengthen purchasing confidence, while consistent supply and standardized quality reinforce repeat buying behavior. Their ability to serve diverse consumer segments at scale positions them as the dominant channel within the overall distribution landscape.

Online retailers represent the fastest-growing channel, supported by rising reliance on digital purchasing and expanding e-commerce penetration following shifts in consumer behavior. Demand for transparency in ingredient sourcing and certification details aligns well with digital platforms that offer detailed product information, reviews and subscription-based purchasing options. Improved logistics networks and faster delivery capabilities strengthen adoption among health-conscious buyers seeking convenience and variety. This channel is expected to capture a substantially higher share through the forecast period, driven by evolving consumer expectations, broader product availability and the expanding role of technology-enabled retail ecosystems.

Regional Insights

North America Organic Soybean Market Trends

North America is forecasted to be the fastest-growing market for organic soybeans between 2026 and 2033, on account of a strong consumer preference for health-enhancing, non-GMO, and sustainably sourced products. Increasing adoption of plant-based diets, protein-rich functional foods, and alternative dairy products such as soy milk and tofu has accelerated demand. Widespread awareness of clean-label ingredients and nutritional transparency encourages both household and commercial buyers to favor organic soybeans. Well-established organic certification frameworks and robust regulatory standards further boost consumer confidence and market expansion.

E-commerce growth and modern retail penetration amplify accessibility, enabling consumers to purchase certified organic soy products conveniently across urban and suburban areas. Investments in supply chain traceability, farm-to-table sourcing models, and collaborations between producers and food manufacturers enhance reliability and quality. In addition, rising interest in sustainable and environmentally responsible agriculture supports premium pricing and higher-value product offerings. These structural and consumer-driven factors create a conducive environment for accelerated adoption, positioning North America as the region with the fastest growth trajectory in the organic soybean market during the forecast period.

Europe Organic Soybean Market Trends

Europe represents a key and steadily expanding market for organic soybeans, backed by robust regulatory frameworks, established organic certification systems, and high consumer awareness of sustainability and health. Countries such as Germany, France, and the Netherlands demonstrate consistent demand for plant-based and non-GMO protein sources, including tofu, soy milk, and soy-based snacks. Preference for clean-label, traceable ingredients drives both household consumption and industrial adoption in functional foods, nutraceuticals, and premium foodservice applications. Europe’s mature retail networks, including supermarkets and specialty stores, provide extensive distribution channels that reinforce market stability and accessibility.

Sustainability initiatives and climate-conscious policies further support growth, encouraging the cultivation and sourcing of organically certified soybeans within Europe and through imports from verified global suppliers. Increasing focus on plant-based diets, coupled with rising interest in vegan and vegetarian lifestyles, enhances demand for versatile soybean derivatives. Investments in supply chain transparency and adherence to non-GMO and organic standards strengthen market credibility, while product innovation in fortified beverages, snacks, and meat alternatives positions Europe as a high-value market.

Asia Pacific Organic Soybean Market Trends

Asia Pacific is projected to capture an estimated 30% of the organic soybean market share in 2026. This leadership is underpinned by a combination of demographic, economic, and cultural dynamics that favor plant-based protein adoption. Rapid urbanization and rising disposable incomes across countries such as China, India, and Japan have intensified demand for health-oriented and sustainably sourced food products. Strong traditional consumption patterns, including soy-based staples such as tofu, soy milk, and fermented products, provide a built-in consumer base that naturally aligns with organic alternatives. The region benefits from increasing government support for organic certification and agricultural modernization programs, which enhance supply reliability and quality assurance, reinforcing market confidence among both producers and consumers.

Strategic integration of organic soybeans into emerging sectors such as functional foods, nutraceuticals, and premium animal feed further amplifies Asia Pacific’s market dominance. Expanding e-commerce and modern retail infrastructure improve distribution efficiency, allowing consumers in tier-2 and tier-3 cities to access certified organic products more easily. Investment in traceable supply chains and adherence to non-GMO and sustainability standards position the region as a hub for high-quality, export-ready organic soybeans. These factors, combined with growing awareness of plant-based diets, create a robust ecosystem that supports both volume growth and value capture, solidifying the prime position of Asia Pacific in the market.

Competitive Landscape

The global organic soybean market structure is moderately fragmented, with leading players such as processors, traders, feed companies, and food manufacturers holding a notable portion of the market. A significant share of production remains with small and mid-sized organic farms and cooperatives, highlighting the decentralized nature of the industry. Their growth rate outpaces conventional soy, reflecting rising consumer demand for health-focused, non-GMO, and sustainably sourced products.

The relatively early stage of market adoption means no single company or group exerts complete control, creating a competitive landscape with opportunities for new entrants. Emerging businesses can leverage innovation, supply chain efficiency, or niche product development to capture market share. Strategic consolidation among farms, processors, and distributors could strengthen market positioning, enhance scale, and improve access to premium segments.

Key Industry Developments

- In July 2025, the European Commission authorized imports of GMO soybeans for use in food and animal feed across the European Union (EU), with the approval valid for ten years and subject to strict labeling and traceability rules. This decision has sharply reduced the non-GMO price premium and pushed Ukrainian export prices for non-GMO soybeans down by about US$ 30 to US$ 40 per ton.

- In April 2025, Archer-Daniels-Midland (ADM) ceased operations at its soybean crushing plant in Kershaw, South Carolina, this spring as part of a broader effort to streamline its global Ag Services and Oilseeds network, cut costs, and focus on higher-return assets.

- In March 2025, COFCO International signed a strategic agreement with Mengniu Group subsidiaries to supply 1.5 million tons of certified sustainable soybeans from Brazil to China, strengthening the global plant-based protein supply chain.

Companies Covered in Organic Soybean Market

- Archer Daniels Midland

- Cargill

- CHS

- Louis Dreyfus

- SunOpta

- The Scoular Company

- Perdue Agribusiness

- Wilmar International

- Bunge

- COFCO International

- Corteva Agriscience

- Fuji Oil

- House Foods

- SLC Agrícola

- Olam Group

Frequently Asked Questions

The global organic soybean market is projected to reach US$ 2.1 billion in 2026.

Increasing consumer preference for health-focused, non-GMO, and sustainably sourced plant-based products is driving the market.

The market is poised to witness a CAGR of 12.6% from 2026 to 2033.

Rising demand for organic and non-GMO products, plant-based diets, and expansion into nutraceuticals, cosmetics, and sustainable feed is generating massive market opportunities.

Some of the key market players include Archer Daniels Midland, Cargill, CHS, Louis Dreyfus, SunOpta, The Scoular Company, Perdue Agribusiness, and Wilmar International