- Food Ingredients & Additives

- Roasted Soybean Market

Roasted Soybean Market Size, Share, and Growth Forecast 2026 - 2033

Roasted Soybean Market by Form (Whole, Flour), by Nature (Organic, Conventional), by End Use (Beverages, Bakery, Snacks & Convenience Food, Animal Feed, Others), by Regional Analysis, 2026 - 2033

Roasted Soybean Market Share and Trend Analysis

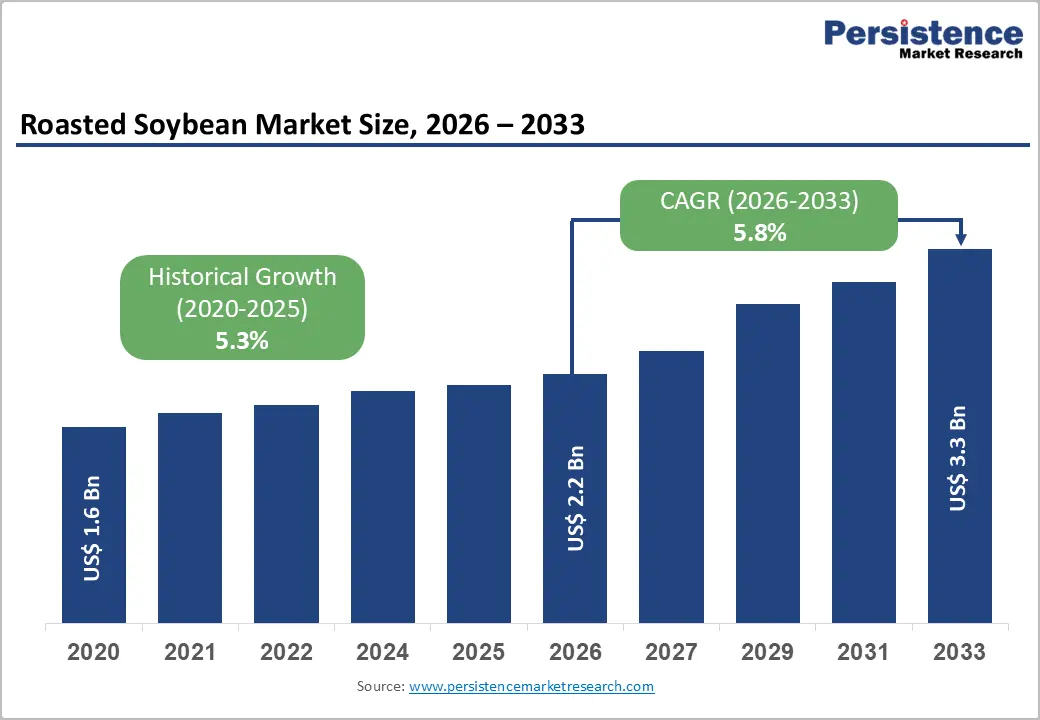

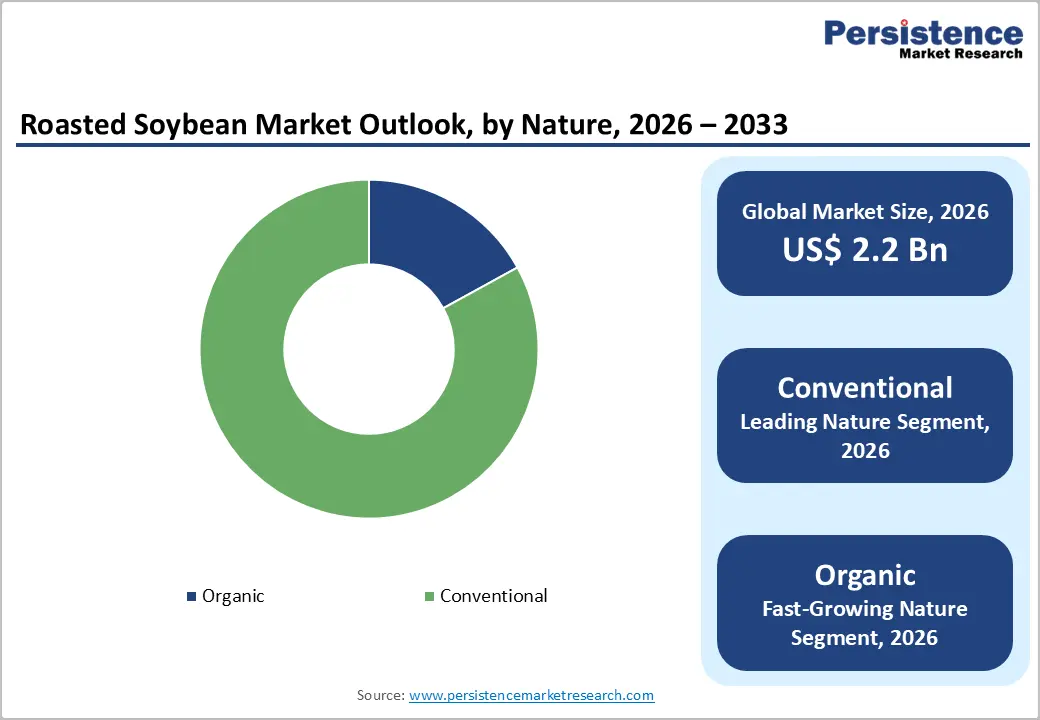

The global Roasted Soybean market size is expected to be valued at US$ 2.2 billion in 2026 and projected to reach US$ 3.3 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The robust expansion of the market is primarily underpinned by the accelerating consumer transition toward nutrient-dense, plant-based protein sources and the escalating demand for clean-label functional food ingredients. This growth is further propelled by the widespread adoption of roasted soy derivatives in the Animal Feed sector, where they serve as a high-quality bypass protein source for ruminants and a highly digestible ingredient for poultry and swine. Additionally, the increasing integration of soy flour in the Bakery and Snacks & Convenience Food industries, coupled with advancements in dry-roasting technologies that enhance flavor while reducing antinutrients, continues to provide a significant competitive edge for market participants.

Key Industry Highlights

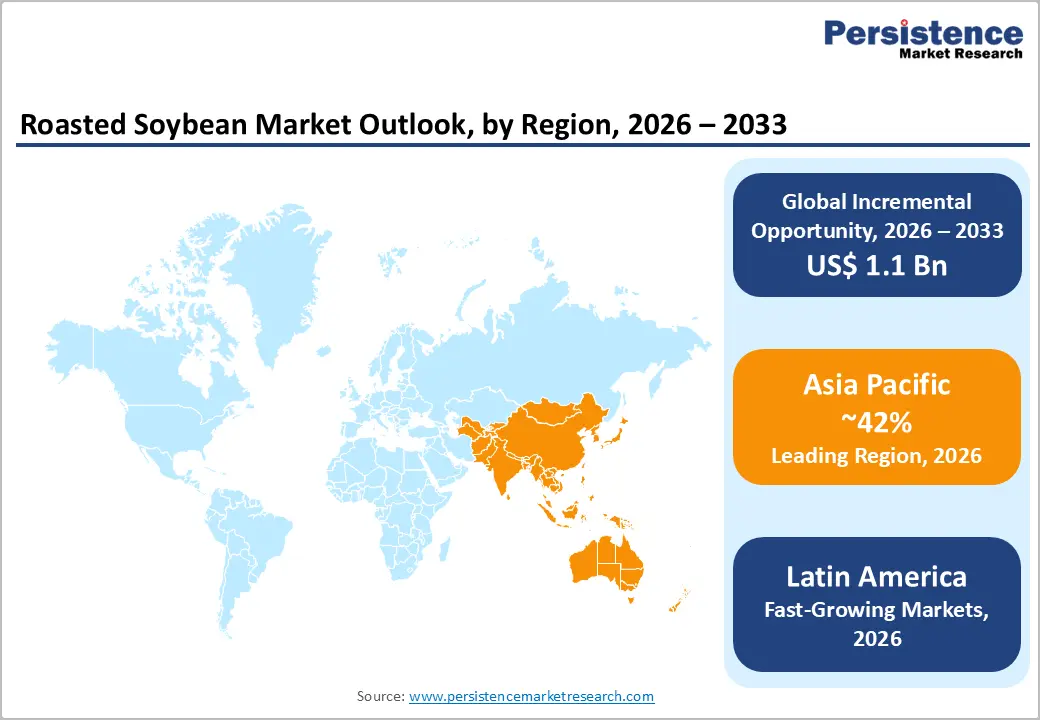

- Asia Pacific is the leading region, holding a 42% market share in 2025, primarily due to the established soy-consumption culture and massive livestock industries in China and India.

- Latin America is identified as the fastest-growing region, with a projected high CAGR driven by its role as a global soybean production powerhouse and increasing local processing investments.

- Conventional roasted soybeans remain the dominant nature segment with an 83% share, benefiting from massive economies of scale and widespread use in the commercial Animal Feed sector.

- Organic roasted soybeans represent the fastest-growing segment from any category, reflecting a global shift toward chemical-free and non-GMO food options among health-conscious consumers.

- The expansion of the Caffeine-Free Beverage sector offers the most significant market opportunity for roasters to utilize soy-based coffee alternatives for the wellness-oriented demographic.

| Key Insights | Details |

|---|---|

| Global Roasted Soybean Market Size (2026E) | US$ 2.2 Bn |

| Market Value Forecast (2033F) | US$ 3.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Dynamics

Driver – Surging Global Demand for Plant-Based High-Protein Snacking Solutions

The foremost driver for the market is the surging consumer appetite for healthy, on-the-go snacks that offer a superior nutritional profile compared to traditional carbohydrate-heavy alternatives. Roasted Soybeans, often marketed as soy nuts, are increasingly recognized as a complete protein containing all nine essential amino acids, which is a rare attribute among plant-based legumes. According to reports from the World Health Organization (WHO) and the Food and Agriculture Organization (FAO), the global shift toward healthier dietary patterns has led to a 15% increase in the consumption of protein-rich legumes over the last five years. The roasting process not only enhances the crunch and savory flavor but also significantly reduces trypsin inhibitors, making the protein more bioavailable. This health-centric trend is particularly strong among millennial and Gen Z demographics who prioritize high-satiety, low-glycemic snacks.

Restraints – Susceptibility to Global Commodity Price Volatility and Supply Chain Disruptions

A primary barrier to the unhindered growth of the market is the significant volatility in raw soybean prices, which are influenced by a complex web of geopolitical, environmental, and economic factors. The Roasted Soybean industry is a high-volume, low-margin business where raw material costs can account for over 70% of the total production expenditure. Historical data from the Chicago Board of Trade (CBOT) indicates that soybean futures can fluctuate by more than 30% within a single growing season due to extreme weather events such as the La Niña phenomenon or shifts in international trade policies. These fluctuations create substantial pricing pressure for mid-sized roasters like KLC Farms Roasting Inc. and Mindals AGRO, who may struggle to pass on these costs to price-sensitive consumers or institutional buyers, ultimately hindering long-term investment in capacity expansion.

Opportunity – Technological Integration of Precision Roasting for Tailored Nutritional Profiles

The adoption of advanced roasting technologies, such as infrared roasting and fluid-bed roasting, presents a significant opportunity to create specialized products with tailored nutritional and sensory attributes. Unlike traditional drum roasting, these modern methods allow for precise control over the time-temperature relationship, ensuring uniform heat distribution and preventing the formation of acrylamide. This precision is vital for the Snacks & Convenience Food segment, where texture and flavor consistency are paramount for brand loyalty. Furthermore, precision roasting can be used to optimize the levels of bioactive compounds, such as genistein and daidzein, which are sought after in the nutraceutical and functional food sectors. By partnering with food technology institutions, manufacturers like SunOpta Inc. can develop proprietary optimal roast profiles that cater to specific health claims, such as heart health or metabolic support, thereby capturing a premium share of the value-added soy market.

Category-wise Analysis

Form Analysis

The Whole roasted soybean segment is the leading segment within the form category, accounting for a significant majority of the value share as of 2025. This dominance is attributed to the widespread popularity of whole beans as a standalone snack, often referred to as soy nuts, and their extensive use in the Animal Feed industry to provide bypass protein for livestock. The structural integrity of the whole bean ensures shelf stability and maintains the oil content, which is rich in essential fatty acids. However, the Flour segment is expected to witness a higher growth rate due to its increasing application as a functional ingredient in the Bakery and Beverages industries. Roasted soy flour is highly valued for its ability to enhance the protein content of wheat-based products while providing a pleasant toasted aroma and improving the moisture retention of baked goods.

End Use Analysis

The Animal Feed segment is the leading end-use category in terms of volume, as roasted soybeans are a critical component for high-performance dairy and poultry rations. The thermal processing involved in roasting improves the digestibility of the beans and increases the rumen-bypass protein levels, making it a staple for commercial livestock producers. Statistics from the American Feed Industry Association (AFIA) highlight that the demand for specialty soy-based feed ingredients is growing at a rate of 4.5% annually. Meanwhile, the Snacks & Convenience Food segment is emerging as the fastest-growing end-use area. The snackification of meals and the increasing demand for plant-based, protein-rich snacks have led to a surge in product launches featuring roasted soy. The high satiety index and nutrient density of roasted soybeans make them an ideal choice for the burgeoning health-conscious consumer base.

Region-wise Insights

North America Roasted Soybean Market Trends and Insights

North America remains a critical hub for the market, characterized by advanced processing infrastructure and a highly developed innovation ecosystem. The United States market leadership is driven by the presence of global agricultural giants like SunOpta Inc. and Bryant Grain Company, who are at the forefront of developing value-added soy products. A key trend in this region is the aggressive shift toward non-GMO and organic offerings, supported by a robust regulatory framework that mandates clear labeling and traceability.

The innovation ecosystem in the U.S. Midwest is focusing on integrating sustainable farming practices with state-of-the-art roasting facilities to reduce the carbon footprint of the production process. Furthermore, the rise of the flexitarian diet in the U.S. and Canada has led to a significant increase in the retail availability of roasted soy snacks and flours in mainstream supermarkets. Collaborative efforts between industry associations like the United Soybean Board (USB) and food scientists are further accelerating the development of soy-based ingredients that meet the strict clean-label requirements of modern North American consumers.

Asia Pacific Roasted Soybean Market Trends and Insights

Asia Pacific is the leading regional market, commanding a 42% market share in 2025. This dominance is rooted in the historical and cultural significance of soy in the diets of populations in China, Japan, and South Korea. The regional dynamics are characterized by a massive manufacturing advantage, as major producers like China and India possess extensive crushing and roasting capacities. Asia Pacific is also home to the world's largest livestock and aquaculture sectors, which consume vast quantities of roasted soy for its high-quality protein.

The rapid urbanization and the expansion of the middle class in India and ASEAN countries are driving a surge in the demand for convenient, packaged soy snacks. Local roasters such as Jabsons Foods and SR Foods are leveraging traditional flavor profiles to capture a larger share of the domestic retail market. Furthermore, government initiatives in India and China to improve protein self-sufficiency and promote the cultivation of indigenous oilseeds are expected to further boost the regional production and consumption of roasted soybean products, maintaining its position as the global market leader.

Market Competitive Landscape

The competitive landscape of the Roasted Soybean Market is a blend of large-scale, vertically integrated agribusinesses and specialized regional players. The market concentration is moderately fragmented, with companies like SunOpta Inc. and KLC Farms Roasting Inc. leveraging their extensive distribution networks and advanced roasting technologies to maintain a dominant presence. Strategic growth initiatives often involve the expansion of processing facilities near major soybean-producing hubs to reduce logistical costs and ensure supply chain resilience.

Research and development trends are currently focused on low-acrylamide roasting and the enhancement of the sensory attributes of roasted soy flour for use in premium bakery products. Key differentiators employed by market leaders include the adoption of identity-preserved (IP) systems for non-GMO soy and the development of proprietary flavor coatings for the snack segment. Emerging business model trends show an increasing focus on B2B partnerships with large-scale food manufacturers to provide customized soy-based protein solutions that meet specific nutritional targets.

Companies Covered in Roasted Soybean Market

- SunOpta Inc.

- KLC Farms Roasting Inc.

- N. L. Food Industries

- Mindals AGRO

- Bryant Grain Company

- Natural Products, Inc.

- Jabsons Foods

- Soyaam Food

- SR Foods

- Hillsboro Feed Company

- Others

Frequently Asked Questions

The global market is expected to be valued at approximately US$ 2.2 billion in 2026, reflecting a steady growth driven by health and nutrition trends.

The primary drivers include the escalating global demand for Plant-Based Protein snacks and the rising adoption of roasted soy as a high-quality bypass protein in the Animal Feed industry.

Asia Pacific is the leading region, commanding a 42% market share in 2025, supported by its massive production base and cultural affinity for soy-based diets.

A key opportunity lies in technological integration of precision roasting for tailored nutritional profiles.

Key market participants include SunOpta Inc., KLC Farms Roasting Inc., Natural Products, Inc., Jabsons Foods, and major agribusinesses like Cargill and ADM.