- Food Ingredients & Additives

- Soybean Derivatives Market

Soybean Derivatives Market Size, Share, and Growth Forecast, 2026 - 2033

Soybean Derivatives Market by Product Type (Soy Meal, Soy Oil, Soy Protein, Soy Milk, Soy Nuts), Application (Food Industry, Feed Industry, Biodiesel), and Regional Analysis for 2026 - 2033

Soybean Derivatives Market Size and Trends Analysis

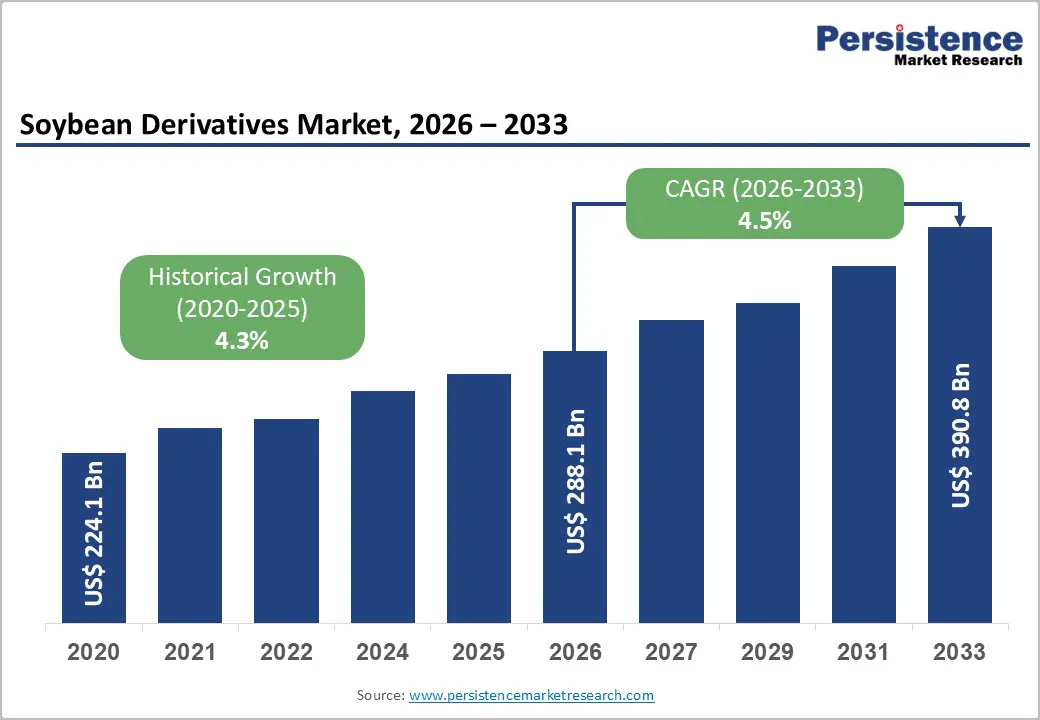

The global soybean derivatives market size is likely to be valued at US$288.1 billion in 2026 and is expected to reach US$390.8 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by the rising demand for soy meal as a high-protein animal feed amid increasing livestock and aquaculture production, particularly in emerging economies.

Soybean oil consumption is rising due to its widespread use in food processing, cooking, and biodiesel production, boosted by government mandates on renewable fuels. Growing demand for plant-based proteins such as soy protein, soy milk, and soy ingredients is driven by consumer preferences for sustainable nutrition, supported by population growth, urbanization, and global sustainability initiatives.

Key Industry Highlights:

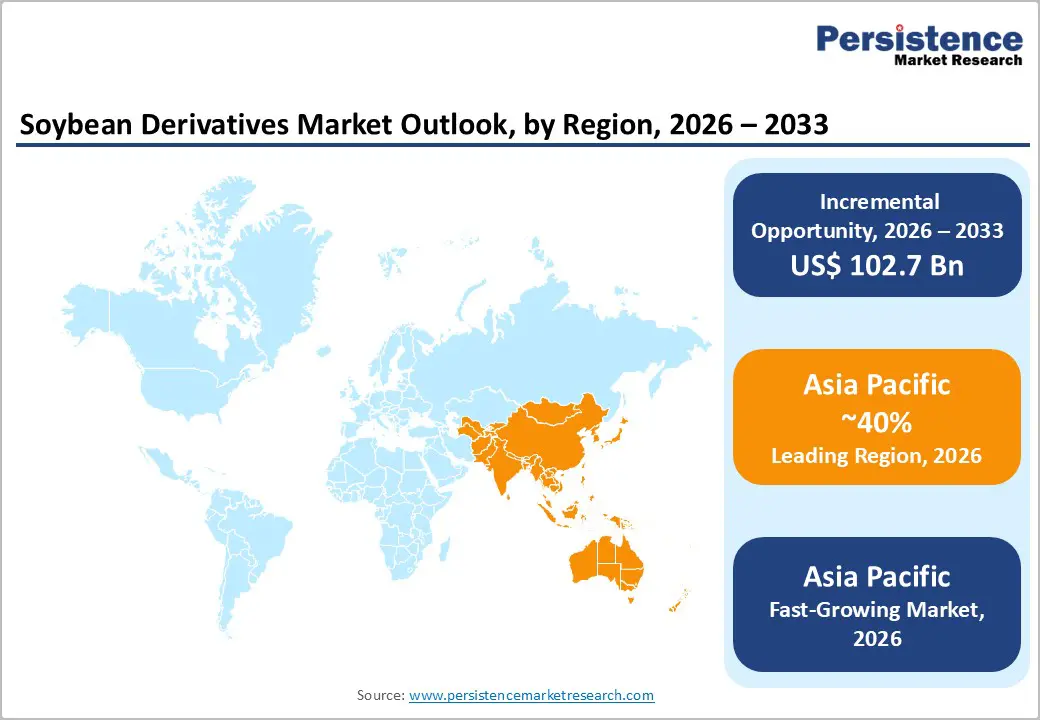

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for 40% market share in 2026, driven by strong livestock and aquaculture feed demand, rapid urbanization, expanding food processing industries, and increased regional processing capacity to reduce import dependence.

- Fastest-growing Region: North America is likely to be the fastest-growing region in the soybean derivatives in 2026, supported by strong crushing capacity, advanced biofuel production, regulatory support, and innovation in value-added soy proteins.

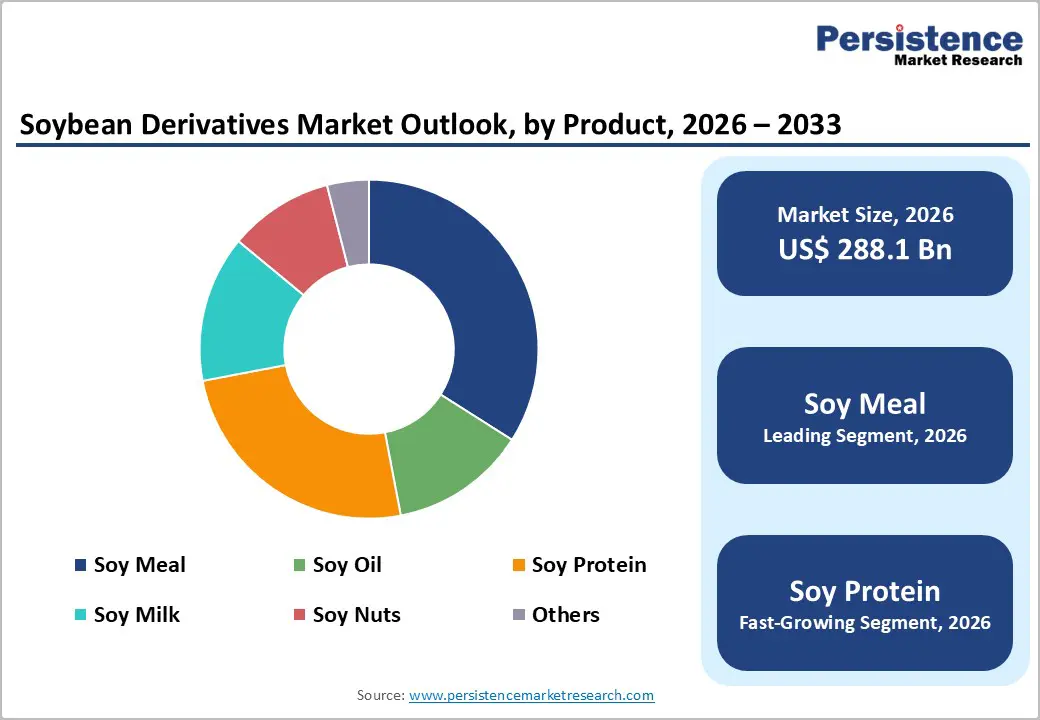

- Leading Product Type: Soy meal is projected to be the leading product type in 2026, accounting for 60% of revenue share, driven by its dominant use in animal feed across the livestock and aquaculture industries.

- Leading Distribution Channel: The feed industry is anticipated to be the leading application type, accounting for over 70% of revenue in 2026, supported by the widespread use of soy meal in global livestock and aquaculture feed.

| Key Insights | Details |

|---|---|

|

Soybean Derivatives Market Size (2026E) |

US$288.1 Bn |

|

Market Value Forecast (2033F) |

US$390.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Animal Feed Protein

Soy meal is widely preferred because of its balanced amino acid profile, high digestibility, and consistent supply, making it a cornerstone ingredient in poultry, swine, cattle, and fish feed formulations. Rapid population growth and rising incomes, especially in the Asia Pacific, Latin America, and parts of Africa, are increasing the consumption of meat, dairy, eggs, and seafood, which in turn drives large-scale livestock and aquaculture production. Producers seek to improve feed efficiency and animal productivity, and reliance on protein-rich feed ingredients such as soy meal continues to expand. The intensification of commercial farming systems and the shift from traditional feeding practices to compound and formulated feeds strengthen demand. Compared to alternative protein sources, soybean derivatives offer scalability, availability, and relatively stable pricing, reinforcing their dominance in feed applications.

The expansion of aquaculture and commercial livestock farming further amplifies protein demand, strengthening the role of soybean derivatives in feed applications. Aquaculture, one of the fastest-growing food production sectors, relies heavily on soy-based proteins as a sustainable alternative to fishmeal, supporting long-term soy meal consumption. Tightening regulations on animal health and feed quality are encouraging the use of nutritionally balanced and traceable feed ingredients, where soybean derivatives perform strongly. Feed manufacturers increasingly prioritize consistency, digestibility, and cost efficiency, all of which favor soy-based proteins over other plant or animal-derived alternatives. Advancements in feed formulation and processing technologies have improved the nutritional efficiency of soy meal, enabling higher inclusion rates without compromising animal performance.

Competition from Alternative Proteins and Oils

Protein alternatives such as rapeseed meal, sunflower meal, pea protein, canola meal, and emerging insect-based proteins are gaining traction, particularly in regions seeking to reduce dependence on soy imports. These alternatives are often promoted for their local availability, lower allergen perception, or suitability for specific feed formulations. In the edible oil segment, soybean oil faces strong competition from palm, sunflower, rapeseed, and coconut oils, which are preferred in certain geographies for pricing, taste, or functional properties. Volatility in soybean prices, driven by weather variability and trade policies, encourages buyers to switch to substitute ingredients when cost competitiveness shifts.

The impact of alternative proteins and oils is particularly evident in markets that emphasize sustainability and the diversification of protein sources. Plant-based food manufacturers are increasingly adopting pea, fava bean, and chickpea proteins to address consumer concerns related to soy allergies and genetically modified crops. In animal feed, improvements in processing technologies have enhanced the nutritional quality of non-soy meals, enabling partial substitution without compromising performance. Biofuel producers may shift toward other vegetable oils or waste-based feedstocks when soybean oil prices rise or policy incentives change. These competitive pressures limit pricing power for soybean derivatives and can slow demand growth in specific applications.

Emerging Demand in Plant-Based and Functional Foods

Rising awareness of health, wellness, and sustainable diets has driven a shift toward soy protein, soy milk, and other soy-based ingredients in food and beverage products. Soy protein isolates and concentrates are being incorporated into meat alternatives, protein bars, beverages, and bakery products to provide high-quality, plant-based protein. Functional soy ingredients, such as isoflavones, lecithin, and soy peptides, are gaining traction for their potential health benefits, including cardiovascular support, bone health, and hormonal balance, increasing adoption in nutraceuticals and fortified foods. This trend is particularly strong in North America, Europe, and the Asia Pacific, where consumers are seeking alternatives to animal-derived proteins and looking for cleaner, sustainable food sources. The shift is reinforced by regulatory support for nutrition labeling and consumer education about plant-based diets, driving innovation and product launches across retail and foodservice sectors.

The rise of flexitarian and vegan lifestyles is accelerating demand for versatile soy ingredients that can replace dairy and meat proteins without compromising texture or nutritional value. Food manufacturers are increasingly leveraging soy protein isolates, textured soy proteins, and soy-based emulsifiers to improve taste, functionality, and protein content in processed foods. Growing interest in personalized nutrition and functional foods is creating niche markets for soy-derived bioactive compounds that enhance immunity, digestive health, and metabolic function. Coupled with the scalability and global availability of soy derivatives, these factors provide ample growth opportunities for manufacturers to expand product portfolios and cater to evolving consumer preferences.

Category-wise Analysis

Product Type Insights

Soy meal is expected to lead the soybean derivatives market, accounting for approximately 60% of the revenue share in 2026, due to its critical role as a high-protein feed ingredient. It is extensively used in poultry, swine, cattle, and aquaculture feed, providing essential amino acids and digestible protein necessary for optimal growth and productivity. For example, in China, which is the world’s largest consumer of soy meal, poultry and aquaculture industries rely heavily on soy meal to meet protein requirements, reflecting its dominance in feed formulations. The established supply chain, large-scale crushing facilities, and consistent nutritional quality make soy meal a preferred choice for feed manufacturers, ensuring its continued leading role. Soy meal’s efficiency in improving feed conversion ratios and reducing production costs reinforces its widespread adoption across commercial livestock and aquaculture farms.

Soy protein is likely to be the fastest-growing segment, driven by increasing demand for plant-based proteins in human nutrition and functional foods. This segment includes soy protein isolates, concentrates, and textured proteins, which are widely used in meat alternatives, protein powders, dairy substitutes, and fortified food products. For example, Beyond Meat incorporates soy protein isolates in some of its plant-based products to mimic meat texture while providing high-quality protein. Rising health consciousness, flexitarian diets, and the trend toward sustainable and environmentally friendly protein sources are driving adoption. The nutritional benefits of soy protein, such as low saturated fat and high digestibility, enhance its appeal to consumers seeking healthy alternatives to animal proteins.

Application Insights

The feed industry is projected to lead, capturing around 70% of the total revenue share in 2026. Soy meal dominates feed formulations due to its high protein content and amino acid profile, essential for the growth and productivity of livestock, poultry, and aquaculture. For example, in Brazil, one of the top global exporters of soy meal, the feed industry heavily relies on soy meal for poultry and swine diets, ensuring a consistent protein supply for meat production. FAO data underscores soy meal's role as a primary source of dietary protein for animals, especially in intensive farming systems. The expansion of commercial livestock operations and aquaculture, particularly in Asia Pacific and Latin America, is increasing the soy meal demand. Feed manufacturers benefit from soy meal’s cost-effectiveness, year-round availability, and ease of formulation into compound feeds.

Biodiesel is likely to be the fastest-growing application, driven by increasing demand for renewable fuels and sustainability initiatives worldwide. Soybean oil is a key feedstock for biodiesel production, offering a renewable alternative to fossil fuels and aligning with government policies and blending mandates, such as the U.S. Renewable Fuel Standard (RFS). For example, Archer Daniels Midland Company (ADM) uses soybean oil to produce biodiesel, supporting energy diversification while adding value to the soybean supply chain. Rising environmental concerns, carbon-reduction targets, and incentives for renewable energy adoption are driving biodiesel production from soybean oil, accelerating segment growth. Technological advancements in biodiesel processing and the expansion of blending infrastructure are enabling higher uptake of soybean oil in renewable fuels.

Regional Insights

North America Soybean Derivatives Market Trends

North America is likely to be the fastest-growing region in the soybean derivatives in 2026, driven by advanced crushing capacity, technological innovation, and a strong focus on value-added products. The U.S., as the largest producer and exporter of soybeans, plays a central role in shaping regional market trends. Soy meal continues to dominate the feed industry, supplying protein-rich ingredients to poultry, swine, and cattle sectors, while soybean oil supports both food applications and renewable fuel production. Growing consumer awareness of plant-based diets and protein-enriched foods is stimulating demand for soy protein isolates and concentrates in food and beverage products. Sustainability initiatives and biofuel policies are influencing processing strategies, with producers optimizing operations to improve efficiency, reduce waste, and enhance traceability.

Archer Daniels Midland Company (ADM), a key player in North America, exemplifies these trends through its integrated soybean processing operations. For example, ADM has been expanding its production of soy protein isolates and soy-based functional ingredients, targeting both food and feed markets. The company is leveraging advanced processing technologies to meet growing demand for plant-based proteins and biofuels, positioning itself at the forefront of innovation. Regulatory support, such as the U.S. Renewable Fuel Standard (RFS), encourages the use of soybean oil in biodiesel, thereby increasing consumption of soybean derivatives. Research and development investments focus on specialty soy ingredients such as lecithin, soy peptides, and isoflavones, reflecting a shift from traditional uses toward higher-value functional foods and nutraceutical applications.

Europe Soybean Derivatives Market Trends

Europe is likely to be a significant market in 2026, driven by a combination of growing demand for animal feed protein, renewable energy mandates, and increasing adoption of plant-based food products. The feed industry remains the largest consumer of soybean derivatives, particularly soy meal, which is widely used in poultry, swine, and aquaculture feed formulations to meet strict protein requirements. Countries such as Germany, France, and the Netherlands have advanced livestock and aquaculture industries that rely on imported soy meal because local soybean cultivation is limited. The region is witnessing a surge in plant-based food consumption, with consumers seeking meat alternatives, dairy substitutes, and protein-enriched products.

European producers and feed manufacturers are investing in improved processing technologies to enhance nutritional quality. For example, Louis Dreyfus Company (LDC), a leading agribusiness player in Europe, exemplifies these market trends through its integrated soybean processing and trading operations. LDC supplies soy meal, soy oil, and soy protein ingredients to both feed and food industries, emphasizing sustainability and traceability throughout its supply chain. The company has invested in modern crushing facilities and partnerships to enhance efficiency, support renewable energy initiatives, and expand its portfolio of plant-based protein products. European biofuel policies promoting renewable energy have increased soybean oil usage for biodiesel production, while consumer demand for soy-based functional foods and nutraceuticals continues to rise.

Asia Pacific Soybean Derivatives Market Trends

The Asia Pacific region is likely to be the fastest-growing region in 2026, driven by a high demand for animal feed, a growing population, urbanization, and increasing consumption of plant-based proteins. Rapid growth in poultry, swine, and aquaculture industries is driving the need for protein-rich soy meal, while rising health awareness and dietary shifts are accelerating demand for soy protein isolates, soy milk, and other soy-based food products. Urbanization, increasing disposable incomes, and the expansion of processed food markets are fueling soy derivative consumption. Regional trends also include investment in local crushing and processing facilities to reduce import dependency and improve supply chain efficiency.

Governments are promoting sustainable agriculture and food security, encouraging the use of nutritionally balanced feed and plant-based proteins, which enhances soy derivatives' role across food, feed, and industrial applications. Wilmar International Limited, a major player in Asia Pacific, exemplifies these trends through its integrated soybean crushing and processing operations. For example, Wilmar supplies soy meal, soy oil, and soy protein ingredients across the region, catering to feed manufacturers, food processors, and biodiesel producers. The company invests in modern processing facilities, quality assurance, and sustainable sourcing programs to meet growing demand for protein-rich animal feed and plant-based food ingredients. Wilmar leverages its extensive distribution network to support both domestic consumption and exports.

Competitive Landscape

The global soybean derivatives market exhibits a moderately fragmented structure, driven by the presence of several large multinational agribusinesses alongside a mix of regional processors and niche specialists competing across product segments and geographies. Major players leverage extensive soybean crushing and processing infrastructure, integrated supply chains, and diversified portfolios spanning soy meal, soy oil, soy protein, and lecithin to serve feed, food, biodiesel, and industrial applications. Competitive pressures are shaped by rising demand for plant-based proteins, sustainability credentials, and cost efficiencies, prompting firms to innovate in areas such as non-GMO processing and specialty soy ingredients.

With key leaders including Archer Daniels Midland Company (ADM), Cargill, Bunge Limited, Louis Dreyfus Company, Wilmar International Limited, CHS Inc., AG Processing Inc., and DuPont Nutrition & Health, the competitive landscape balances scale with specialization. These players compete through product innovation, capacity expansion, vertical integration, strategic collaborations, and investments in technology to enhance the extraction yields, quality, and performance of soybean derivatives in diverse end uses. Strategic mergers, such as Bunge’s consolidation moves, and partnerships for supply stability underscore competitive tactics aimed at strengthening global reach and operational resilience.

Key Industry Developments:

- In April 2025, Bursa Malaysia Derivatives Exchange (BMD) launched the Bursa Malaysia DCE Soybean Oil Futures (FSOY), the first non-palm edible oil futures contract on the platform. Trading began on March 18, 2024, following an agreement with Dalian Commodity Exchange (DCE) to reference its soybean oil futures price for FSOY's cash settlement. This US$-denominated contract allows traders to hedge risks and arbitrage between soybean and palm oil on a single platform.

- In July 2024, Archer Daniels Midland Company (ADM) announced its provision of fully verified, segregated, and traceable soybean meal and oil to meet European customer demands under the EU Deforestation Regulation. Through its North American Resource™ program, ADM enrolled over 5,300 farmers across 15 states, covering 4.6 million acres for the 2024 season. Using advanced platforms such as FBN® Gradable and the TRACT sustainability measurement tool, the program ensured traceability from farm to final destination, supporting compliance with the new EU sustainability standards.

Companies Covered in Soybean Derivatives Market

- Archer Daniels Midland Company

- Bunge Limited

- Cargill, Incorporated

- Ag Processing Inc.

- Louis Dreyfus Company B.V.

- CHS Inc.

- Wilmar International Limited

- Fuji Oil Holdings Inc.

- The Scoular Company

- Nisshin OilliO Group, Ltd.

- Xinrui Group

- Devansoy Inc.

- Burcon NutraScience Corporation

- SLC Agricola

- Vicentin SAIC

- Viterra Limited

- Marubeni Corporation

- Amaggi Group

- Caramuru Alimentos S.A.

- Shandong Saigao Group Corporation

Frequently Asked Questions

The global soybean derivatives market is projected to reach US$288.1 billion in 2026.

The soybean derivatives market is driven by the growing demand for protein-rich animal feed, plant-based proteins, edible oils, and biofuels.

The soybean derivatives market is expected to grow at a CAGR of 4.5% from 2026 to 2033.

Key market opportunities lie in plant-based foods, animal feed, biodiesel, specialty soy ingredients, and sustainable, traceable supply chains.

Archer Daniels Midland Company, Bunge Limited, Cargill Incorporated, and Ag Processing Inc. are the leading players.