- Specialty & Fine Chemicals

- Epoxidized Soybean Oil Market

Epoxidized Soybean Oil Market Size, Share, and Growth Forecast, 2026 - 2033

Epoxidized Soybean Oil Market By Raw Material (Soybean Oil, Hydrogen Peroxide, Others), Application (Plasticizers, Pigment Dispersion Agents, Others), End-user (Food & Beverages, Personal & Healthcare, Adhesives & Sealants, Others), and Regional Analysis for 2026 - 2033

Epoxidized Soybean Oil Market Size and Trends Analysis

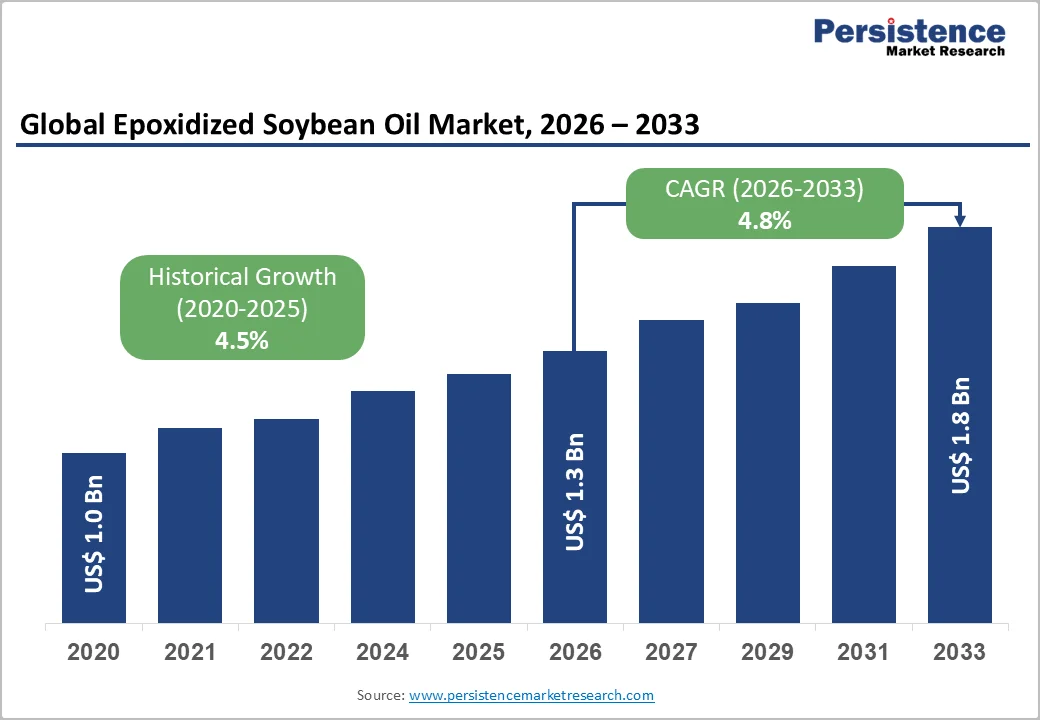

The global epoxidized soybean oil market size is likely to be valued at US$1.3 billion in 2026, and is expected to reach US$1.8 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by the increasing demand for eco-friendly and non-toxic plasticizers, rising adoption of bio-based stabilizers in flexible PVC, and stringent regulations on phthalate-based additives.

The move toward sustainable options in food & beverage and personal care packaging is accelerating the use of epoxidized soybean oil across industries. Market growth is further supported by advances in high-purity grades that offer improved heat and light stability, as well as the rising adoption of this green alternative in adhesives, sealants, and automotive applications.

Key Industry Highlights:

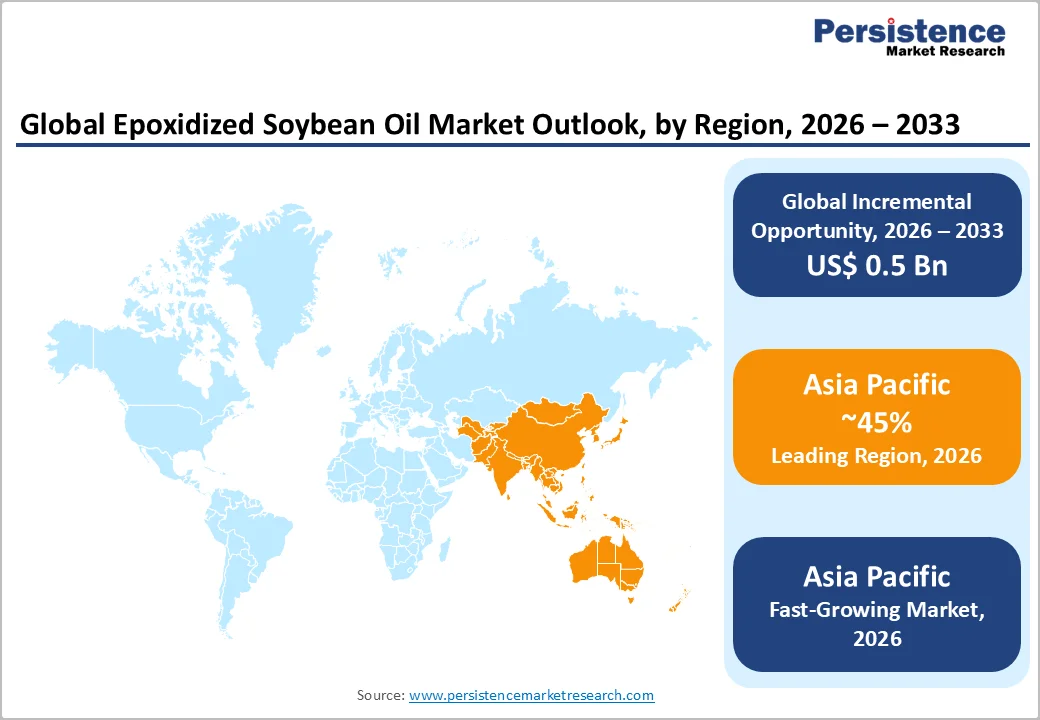

- Leading Region: Asia Pacific is expected to account for 45% of the market in 2026, driven by massive PVC production, strong demand for food packaging, and the expanding automotive sector in China.

- Dominant Raw Material: Soybean oil, likely to hold approximately 60% of the market share in 2026, due to its renewable nature and wide availability.

- Leading Application: Plasticizers, projected to account for over 40% of market revenue in 2026, are widely used in flexible PVC products, including films, cables, and flooring.

- Leading End-user: Food & beverages, expected to contribute nearly 35% of market revenue in 2026, due to regulatory approvals from the FDA and EU for direct food contact.

| Key Insights | Details |

|---|---|

| Epoxidized Soybean Oil Market Size (2026E) | US$1.3 Bn |

| Market Value Forecast (2033F) | US$1.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand for Eco-Friendly and Non-Toxic Plasticizers

The rising global demand for eco-friendly and non-toxic plasticizers is the primary driver of the epoxidized soybean oil market. Traditional phthalate-based plasticizers, widely used in PVC and other polymer applications, have faced increasing regulatory scrutiny due to potential health and environmental risks.

Concerns over reproductive toxicity, endocrine disruption, and chemical leaching have prompted governments worldwide, particularly in North America, Europe, and the Asia Pacific, to impose strict restrictions and guidelines on phthalate usage.

Manufacturers and end-users are increasingly shifting toward safer alternatives, with ESO emerging as a preferred solution. As a bio-based, non-toxic, and biodegradable plasticizer, ESO not only meets regulatory compliance but also aligns with growing consumer preferences for sustainable products.

Industries such as construction, packaging, automotive, medical devices, and consumer goods are adopting ESO to produce flexible PVC, coatings, adhesives, and films that are safer for human use and environmentally friendly. The trend toward green building materials, food-contact safe products, and low-VOC formulations further reinforces the adoption of ESO.

Its compatibility with the existing PVC processing technologies, along with the ability to improve thermal and mechanical properties, makes ESO a highly attractive option.

High Production and Raw Material Price Volatility

High production and raw material price volatility pose significant challenges to the epoxidized soybean oil (ESO) market, directly impacting profitability and long-term planning for manufacturers.

Since soybean oil accounts for a major portion of total production costs, fluctuations in soybean prices driven by climate conditions, global trade dynamics, and feedstock competition with food and biofuel industries create uncertainty in cost structures.

Any sharp increase in soybean prices immediately elevates ESO production expenses, making it difficult for producers to maintain stable pricing for downstream customers in plastics, coatings, adhesives, and food-contact applications.

The energy-intensive epoxidation process requires consistent access to hydrogen peroxide and other chemical inputs, which are also subject to global supply chain disruptions and pricing swings. Manufacturers operating without integrated sourcing face greater exposure to these fluctuations, leading to uneven margins.

Transportation and logistics costs further compound the issue, especially during periods of geopolitical tension or freight shortages. Price volatility not only affects manufacturers but also influences purchasing decisions among end users, who may temporarily reduce consumption or switch to alternative plasticizers when prices spike.

Advancements in High-Purity and Multifunctional ESO Grades

Advancements in high-purity and multifunctional epoxidized soybean oil (ESO) grades are significantly transforming market dynamics by expanding application potential across high-performance industries. Manufacturers are increasingly focusing on refining epoxidation processes to achieve superior oxirane content, lower acid values, and enhanced thermal stability.

These improvements result in ESO grades that deliver better plasticization efficiency, higher compatibility with a broader range of polymers, and reduced migration, key requirements for premium PVC products, medical materials, and flexible packaging.

Multifunctional ESO grades are also gaining traction as they offer dual benefits of plasticization and stabilization, enabling formulators to reduce the number of additives required and streamline product formulations.

These advanced grades demonstrate improved resistance to UV degradation, better mechanical strength, and enhanced barrier properties, making them ideal for use in automotive interiors, bio-based coatings, and sustainable adhesives. Innovations in purification technologies and catalyst systems are enabling the production of ultra-low-odor and food-contact-compliant ESO varieties.

Category-wise Analysis

Raw Material Insights

Soybean oil is expected to dominate the market, accounting for approximately 60% of the market share in 2026, due to its renewability, abundant availability, and cost-effectiveness. Its high unsaturated fatty acid content makes it ideal for efficient epoxidation, allowing manufacturers to achieve consistent quality during ESO production.

Stable supply chains in major producing countries such as the U.S., Brazil, and Argentina further support its widespread use across industrial applications. For example, PVC flooring and flexible packaging manufacturers frequently use ESO derived from soybean oil as a primary non-phthalate plasticizer, leveraging its biodegradability and regulatory acceptance to replace conventional plasticizers.

Hydrogen peroxide is likely to be the fastest-growing segment, driven by its ability to deliver high-efficiency epoxidation and superior oxirane content in ESO production. It enables cleaner reactions with fewer byproducts, aligning closely with global sustainability requirements and green-chemistry standards.

As manufacturers focus on high-purity, high-performance ESO grades for advanced PVC products and modern coating formulations, demand for hydrogen-peroxide-based processes continues to accelerate. For example, automotive coating manufacturers increasingly prefer ESO produced using hydrogen peroxide, as its higher oxirane value enhances crosslinking, resulting in superior strength and UV resistance in coating applications.

Application Insights

Plasticizers are projected to lead the market, holding over 40% share in 2026, driven by extensive use in flexible PVC films, cables, hoses, synthetic leather, and flooring. ESO improves flexibility, thermal stability, and durability, making it a preferred alternative to conventional phthalate plasticizers.

Its non-toxic profile and strong compatibility with PVC support its adoption in safer, sustainable product formulations. For example, manufacturers of PVC electrical cables increasingly use ESO as a secondary plasticizer to enhance heat resistance, reduce plasticizer migration, and extend cable life, ensuring improved performance and safety.

Fuel additives are likely to be the fastest-growing segment, as ESO offers excellent compatibility with biofuels and helps enhance lubricity in modern engines. As fuel standards tighten and renewable fuel blending increases, ESO is used to improve oxidation stability, reduce engine wear, and support cleaner combustion.

Its ability to function effectively in biodiesel blends strengthens its demand in transportation and industrial applications. For example, Biodiesel producers commonly add ESO-based additives to B20 and B30 fuel blends to improve lubricity and protect fuel injectors, ensuring smoother engine operation and reduced wear in commercial vehicle fleets.

End-user Insights

Food & beverages are expected to dominate, with nearly a 35% share in 2026, due to FDA and EU approvals that permit direct food-contact applications. ESO is increasingly replacing traditional phthalate-based plasticizers in applications such as PVC flooring, food packaging films, medical tubing, and wire & cable insulation.

Its non-toxic and migration-resistant nature enhances safety and regulatory compliance across food-related environments. For example, food packaging manufacturers use ESO-plasticized PVC films in meat wrap, dairy packaging, and bakery films, where improved flexibility and minimal chemical migration are essential for freshness and safety.

Adhesives & sealants represent the fastest-growing segment, due to rising demand for low-VOC, non-toxic, and sustainable formulations. Epoxidized soybean oil enhances flexibility, adhesion strength, and environmental compliance, making it ideal for construction, packaging, and automotive applications.

Its ability to improve chemical resistance and elasticity further supports its use in modern adhesive technologies. For example, construction companies use ESO-modified sealants for PVC flooring installation and flexible joint sealing, where added elasticity helps prevent cracking and ensures long-lasting performance.

Regional Insights

North America Epoxidized Soybean Oil Market Trends

North America is driven by strong demand for safer, bio-based plasticizers and stabilizers. One of the key trends is the rising replacement of traditional phthalate plasticizers, supported by strict regulatory scrutiny from agencies such as the EPA and FDA. As manufacturers seek compliant, non-toxic alternatives for PVC compounds, packaging materials, medical-grade products, and consumer goods, ESO is gaining significant traction across the region.

The expansion of domestic soybean processing and bio-based chemical production. Abundant soybean availability in the United States supports reliable, cost-effective feedstock sourcing, leading to increased investment in advanced epoxidation technologies.

These investments focus on improving product purity, enhancing epoxidation efficiency, and reducing carbon emissions during production, aligning with North America’s growing emphasis on sustainable industrial practices. Rising adoption of ESO in automotive interiors, building materials, and wire & cable applications is also contributing to market momentum.

Industries value ESO for its thermal stability, flexibility enhancement, and compatibility with PVC and biopolymers.

Europe Epoxidized Soybean Oil Market Trends

Europe is driven by strong regulatory support for bio-based and non-toxic additives, making the region one of the most quality-driven markets globally. A major trend is the accelerated shift away from traditional phthalate plasticizers, driven by strict EU chemical safety regulations that have significantly increased ESO adoption in PVC processing, packaging, flooring, wall coverings, and medical applications.

Manufacturers in Europe are prioritizing compliance, sustainability certifications, and food-contact approvals, all of which favor ESO as a safer and environmentally responsible alternative.

The rising integration of ESO in circular economy initiatives. As the EU pushes for recyclability and carbon-reduction targets, companies are incorporating bio-based materials to lower the environmental footprint of plastics and coatings. This is stimulating demand for ESO in biopolymer production, recycled PVC stabilization, and flexible packaging reformulations.

The automotive and construction industries are also contributing to market growth, as ESO-modified polymers enhance durability, thermal stability, and weather resistance—qualities essential for high-performance European manufacturing.

Asia Pacific Epoxidized Soybean Oil Market Trends

Asia Pacific is expected to lead the market with a 45% share and maintain its position as the fastest-growing region in 2026, driven primarily by China and India, fueled by rapid industrial growth and the rising use of bio-based additives across major end-user industries.

One of the major trends is the rising demand for environmentally friendly plasticizers, particularly in PVC-based products used in construction, flooring, automotive components, and flexible packaging. As governments in China, India, and Southeast Asia tighten regulations around phthalate-based plasticizers, manufacturers are shifting toward safer alternatives like ESO, accelerating its market penetration.

Regional production capacity is expanding as local manufacturers invest in advanced epoxidation technologies to improve processing efficiency, reduce energy use, and enhance product consistency.

This growth is further supported by abundant soybean availability in countries like China and India, enabling cost-effective raw material sourcing and stronger localized supply chains. Sustainability trends are also reshaping competition, with increasing demand for bio-based, non-toxic, and food-grade-compliant materials in packaging and consumer goods driving greater adoption of epoxidized soybean oil.

Competitive Landscape

The global epoxidized soybean oil market is highly competitive, with manufacturers emphasizing capacity expansion, cost efficiency, and sustainability. Key players such as CHS Inc., Nan Ya Plastics, and Adeka Corporation hold strong positions through integrated supply chains, large-scale facilities, and reliable soybean sourcing, ensuring production efficiency and supply consistency.

Industry trends show a shift toward environmentally responsible production, with expanded capacities and sustainability certifications, such as non-GMO, food-grade compliance, and eco-label approvals, meeting the growing demand for bio-based plasticizers and stabilizers, particularly in Asia Pacific and North America.

Key Industry Developments

- In December 2024, Valtris Specialty Chemicals promoted Plas-Chek and Lankroflex ESBO grades for flexible PVC, emphasizing food-safe, renewable, and Kosher-certified features across diverse uses.

- In February 2024, Galata Chemicals unveiled an advanced ESBO plasticizer with superior heat stability, targeting high-performance PVC applications.

Companies Covered in Epoxidized Soybean Oil Market

- CHS Inc.

- Nan Ya Plastics Corporation

- Adeka Corporation

- Cargill

- Valtris

- Galata Chemicals LLC

- Hairma Chemicals (GZ) Ltd.

- Shangdong Longkou Longda Chemical Industry Co., Ltd.

- Inbra Industries Quimicas, Ltd.

Frequently Asked Questions

The global epoxidized soybean oil market is projected to reach US$1.3 billion in 2026.

The increasing demand for eco-friendly and non-toxic plasticizers, along with regulations banning phthalates, are the primary growth drivers.

The epoxidized soybean oil market is expected to grow at a CAGR of 4.8% from 2026 to 2033.

Development of high-purity ESO for biodegradable lubricants and fuel additives presents the strongest opportunities.

CHS Inc., Nan Ya Plastics Corporation, Adeka Corporation, Cargill, and Valtris are the leading players.