- Semiconductor Materials & Components

- Solid State Drive Market

Solid State Drive Market Size, Share, and Growth Forecast for 2026 - 2033

Solid State Drive Market by SSD Interface (SATA, SAS, PCIE and Other SSD Interface), Drive Storage (Under 500 GB, 500GB-1TB, 1TB-2TB, and Above 2TB) Application (Enterprise and Client), and Regional Analysis 2026 - 2033

Solid State Drive Market Share and Trends Analysis

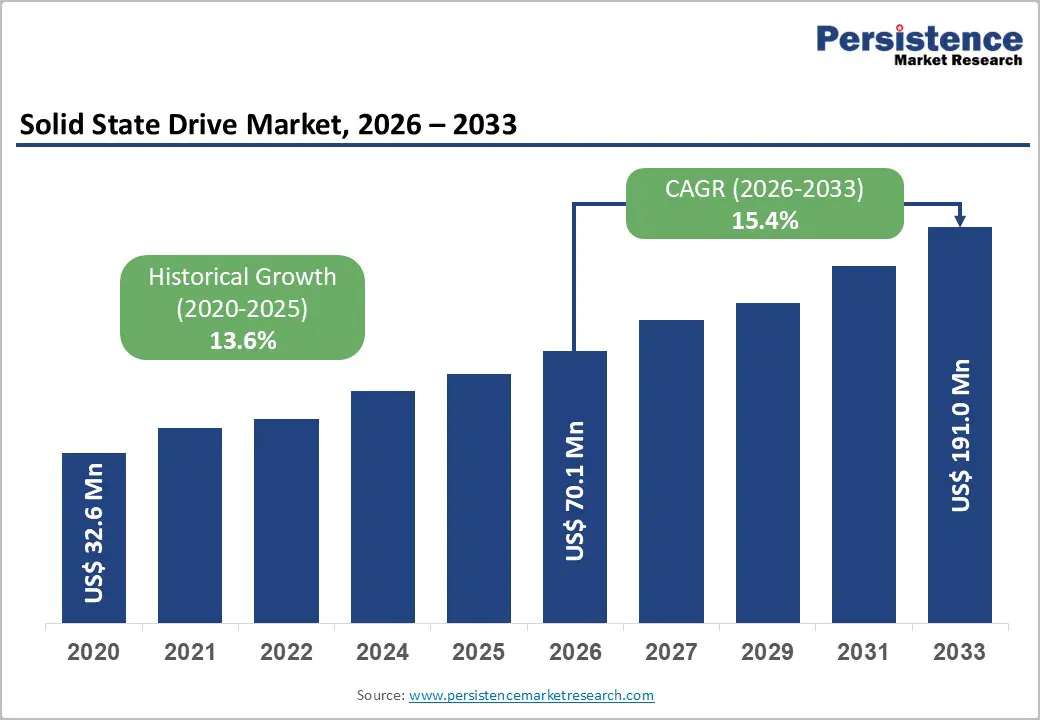

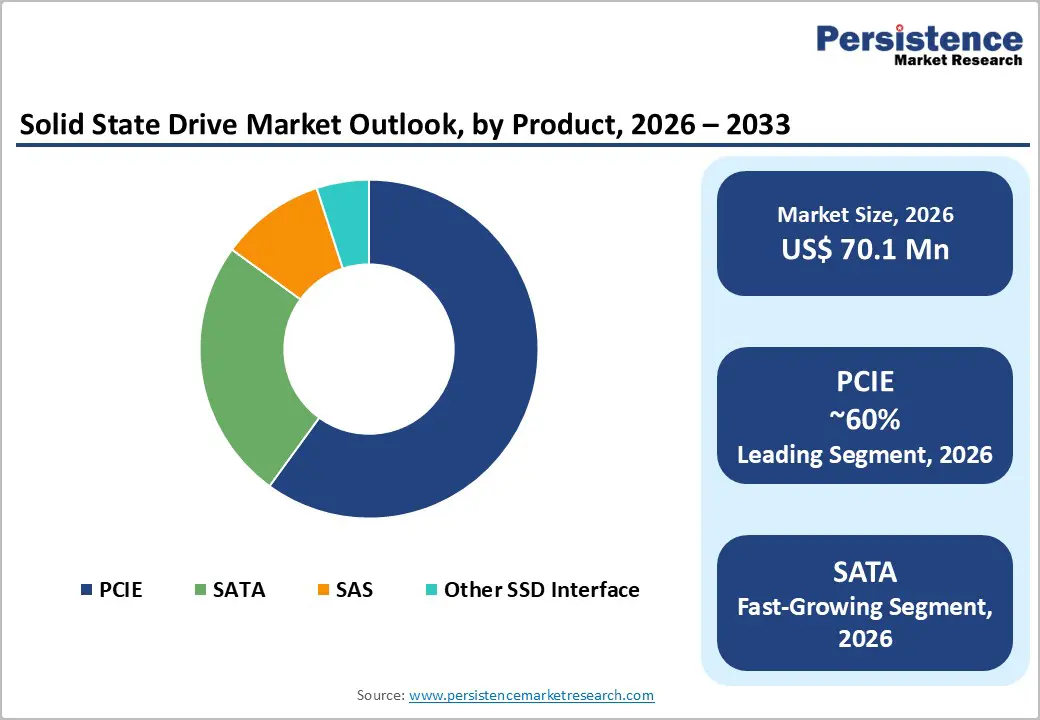

The global solid state drive market size is likely to be valued at US$ 70.1 million in 2026 and is projected to reach US$ 191.0 million by 2033, growing at a CAGR of 15.4 % between 2026 and 2033. This accelerated growth trajectory is driven by the exponential expansion of data center infrastructure supporting artificial intelligence workloads, cloud computing deployments, and edge computing applications, with hyperscale data centers commanding 53.8% of market share in 2024 and expanding at 22.5 % CAGR.

Key Industry Highlights:

- Leading Segment: PCIe interface segment dominates with over 60% of enterprise SSDs shipped in 2026 utilizing NVMe protocol, up from 36% in 2020, with PCIe 5.0 adoption projected to reach 38% in AI-centric deployments by 2025.

- Fastest Growing Segment: The enterprise application segment accounts for approximately 45% market share in 2024 and exhibits 16.2% CAGR through 2033, with data centers and servers expected to rise at 18.7% CAGR as Microsoft Azure and AWS each purchase over 500,000 SSDs per quarter.

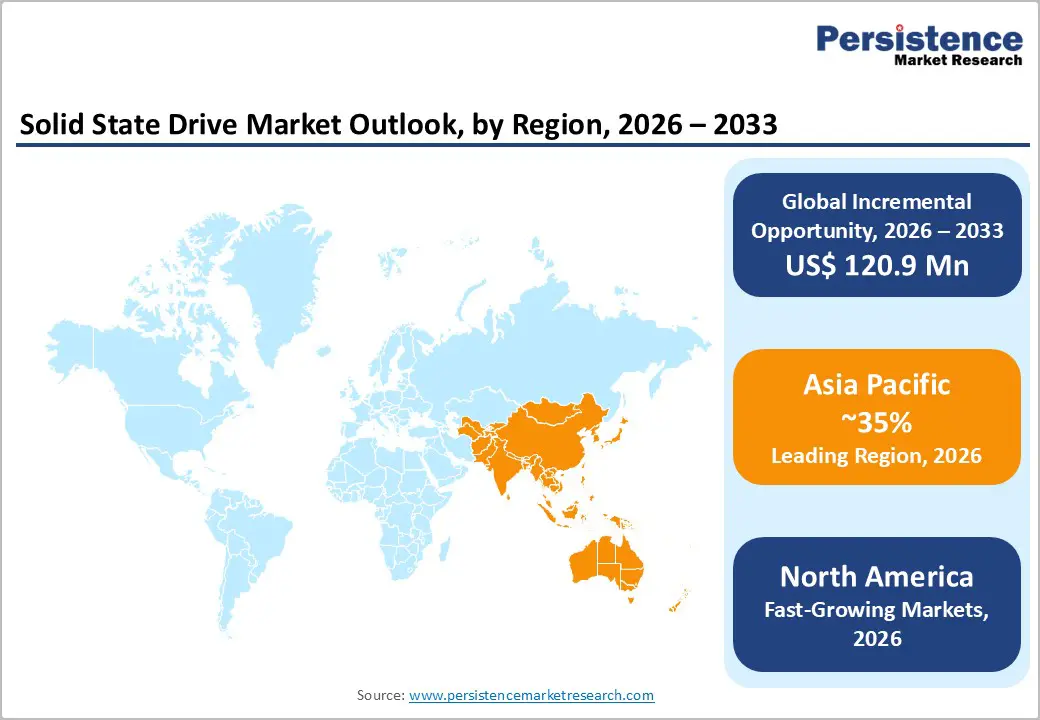

- Leading Region: Asia Pacific leads with 35% market share, driven by China, Japan, and South Korea's manufacturing capabilities and consumer electronics production, demonstrating the highest regional growth rate supported by IT infrastructure investments and digital transformation initiatives.

- NAND flash supply shortage represents a critical constraint with industry inventory lasting only until the first quarter of 2026 and prices surging 50 % in single-month periods, forcing PC OEMs to downgrade SSD specifications and prompting concerns of stock depletion by the second quarter of 2026.

- Opportunities: Samsung and Western Digital's partnership, announced in March 2022, focuses on standardizing Zoned Storage solutions, including ZNS SSDs that optimize data placement and reduce write amplification by 25 to 30 %, improving endurance and lowering total cost of ownership across enterprise applications.

| Key Insights | Details |

|---|---|

|

Solid State Drive Market Size (2026E) |

US$ 70.1 Mn |

|

Market Value Forecast (2033F) |

US$ 191.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

15.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

13.6% |

Market Dynamics Analysis

Drivers - Enterprise Data Center Expansion and AI Workload Proliferation

The solid state drive market is experiencing robust demand driven by hyperscale data center infrastructure investments supporting artificial intelligence training and inference workloads. Enterprise-level adoption in data centers represents a major growth catalyst, with workloads requiring high IOPS and low latency fueling expansion as Microsoft Azure and AWS each purchased more than 500,000 SSDs per quarter in 2025 to support AI inference clusters. AI model training operations demonstrate exceptional storage intensity, with GPT 4's 1.7 trillion parameters requiring 5.4 petabytes of SSD storage per training run, making power per terabyte a critical selection criterion as AI model parameters grow exponentially. Meta's AI research cluster utilizes custom SSD arrays delivering 14 million IOPS to handle trillion parameter model training, necessitating sustained read write speeds exceeding 3.5 gigabytes per second and pushing organizations toward PCIe 4.0 and 5.0 NVMe SSDs with sub-100-microsecond latencies.

PCIe Interface Technology Advancement and NVMe Protocol Migration

Technological evolution in SSD interface standards is fundamentally reshaping the Solid state Drive Market through performance improvements and protocol standardization. The aggressive adoption of NVMe Non-Volatile Memory Express protocol-based SSDs across hyperscale data centers reached over 80 % of enterprise SSD shipments in 2024 using NVMe rather than legacy SATA or SAS interfaces, demonstrating how storage performance transitioned from peripheral concern to core infrastructure competitiveness. PCIe 4.0 SSDs offering speeds up to 8 gigabytes per second dominate market deployment, with PCIe 5.0 interface adoption projected to reach 38 % in AI-centric storage deployments by 2025, enabling data transfer capabilities critical for demanding applications, including cloud computing, machine learning, and real-time analytics. Western Digital projects demand of 19,000 petabytes of NAND by 2029 for 5G enabled devices, highlighting flash memory's pivotal role in supporting next-generation connectivity and edge computing infrastructure.

Restraints - NAND Flash Supply Chain Constraints and Price Volatility

The solid state drive market experiences substantial challenges from NAND flash memory supply shortages and unprecedented price increases disrupting procurement strategies. The 2024 present global memory supply shortage, sometimes referenced as RAMmageddon, represents an ongoing period of supply constraints as major PC and notebook brands including Dell and Lenovo warned clients of imminent price hikes, with the memory market's supply demand imbalance worsening rapidly. Industry sources indicate memory module makers maintain inventory lasting only until first quarter of 2026, with some expected to experience stock depletion as early as March, while the scramble for NAND since the fourth quarter of 2024 has been described as the toughest in nearly a decade.

Opportunity - AI Enabled PC and Edge Device Storage Expansion

The solid state drive market presents substantial growth potential through integration with AI enabled personal computers and edge computing infrastructure. TrendForce observes that with increasing adoption of AI in PCs and edge devices in 2025, demand for high capacity, high performance SSDs will accelerate, positioning SSD module makers that focus on improving technical integration, channel strategies, and brand positioning to succeed in upcoming growth cycles. At the edge, 5G nodes with local flash sliced backhaul offer 38 % reduction in operational expenditure according to Ericsson, providing telecommunications operators immediate payback through reduced backhaul dependencies. Portable storage applications serving mobile workloads and Internet of Things deployments demonstrate steady growth momentum, while gaming segment expansion driven by faster load times and console upgrades exhibit growth rates exceeding 20 % CAGR through 2033.

Zoned Storage and Computational Storage Technology Convergence

Emerging data placement, processing, and fabrics technologies represent transformative opportunities for the Solid state Drive Market through enhanced efficiency and functionality. The adoption of NVMe over Fabrics NVMe allows PCIe based NVMe SSDs to be accessed over networks, enabling greater flexibility and scalability in data center environments as enterprises pursue disaggregated storage architectures. Samsung and Western Digital's collaboration announced in March 2022 to standardize next generation data placement, processing, and fabrics storage technologies focuses on Zoned Storage solutions including ZNS Zoned Namespaces SSDs that optimize data placement and reduce write amplification by 25 to 30 %, improving endurance and lowering total cost of ownership. This partnership through organizations such as Storage Networking Industry Association and Linux Foundation aims to define high level models and frameworks for Zoned Storage technologies, with initiatives expected to expand to include computational storage capabilities that offload processing tasks directly to storage devices, reducing CPU utilization and improving application performance across diverse workloads.

Category wise Analysis

By SSD Interface Insighst

The PCIe segment dominates the Solid state Drive Market and represents the fastest growing interface category, driven by superior performance characteristics and enterprise adoption. Over 60% of enterprise SSDs shipped in 2024 utilized NVMe protocol over PCIe interfaces rather than legacy SATA or SAS connections, reflecting dramatic protocol transition as storage performance became core to infrastructure competitiveness in AI model training and cloud native applications. PCIe 4.0 SSDs offering speeds up to 8 gigabytes per second are expected to dominate the market in coming years, with PCIe 5.0 adoption projected to reach 38 % in AI centric deployments by 2025 as enterprises prioritize solutions supporting faster boot times, improved application responsiveness, and enhanced multitasking capabilities. The segment benefits from backward compatibility enabling seamless integration with existing infrastructure while delivering 4x performance improvement over SATA interfaces, positioning PCIe NVMe as preferred choice for data hungry workloads across enterprise and high-end consumer applications.

By Application Insights

The enterprise segment accounts for approximately 45 % market share in 2024 and exhibits the highest growth trajectory at 16.16 % CAGR through 2033, propelled by data center modernization and AI infrastructure deployment. Enterprise data centers and servers are expected to rise at a modest CAGR through 2031, surpassing client device growth rates as hyperscale providers command 53.8 % of data center SSD market with their appetite shaping vendor roadmaps through custom firmware and telemetry requirements for fleet wide health analytics. Financial services data centers demand low latency flash for trading engines and in memory risk models, while colocation facilities offer pre cabled, high density racks optimized for SSD deployment, diversifying requirements across enterprise subsegments.

By Drive Storage

The 1TB to 2TB capacity segment emerges as the fastest growing category, driven by mainstream adoption across both enterprise and consumer applications. This capacity range represents optimal balance between cost per gigabyte and performance requirements, meeting needs for operating system installations, application libraries, and working data sets without excessive capital expenditure associated with ultra high-capacity units. Channel SSD shipments for 2024 reached 101 million units despite 14 % year over year decrease attributable to weak consumer electronics demand and notebook SSD attach rates reaching 100 %, indicating market maturation in traditional client segments. However, AI PC adoption and edge device proliferation are expected to accelerate demand for high capacity, high performance SSDs in 2025 and beyond, with SSD module makers focusing on improving technical integration and brand positioning to capture growth opportunities.

Regional Market Insights

North America Solid State Drive Market Share and Trends Analysis

North America maintains significant market presence driven by technological leadership and concentration of hyperscale data center operators including AWS, Microsoft Azure, and Google Cloud. The United States is a key driver of SSD demand due to strong presence of technology giants and rapid adoption of cloud computing, edge infrastructure, and AI applications fueling SSD utilization for faster, low latency data storage. Enterprise IT upgrades and investments in data centers boost SSD adoption across sectors including healthcare, retail, and manufacturing, with North America demonstrating leadership in innovation and early adoption of emerging technologies.

The region benefits from established semiconductor manufacturing capabilities and robust research and development ecosystems supporting advancement of 3D NAND architectures and PCIe 5.0 interface standards. Financial services firms concentrated in New York and major metropolitan areas deploy low latency SSDs for algorithmic trading platforms and real time risk analytics, creating specialized demand for enterprise grade solutions.

Europe Solid State Drive Market Share and Trends Analysis

Europe exhibits rapid growth as enterprises adopt SSDs for improved performance and storage efficiency across diverse industry verticals. Major economies including Germany, United Kingdom, France, and Spain demonstrate strong adoption driven by digital transformation initiatives, regulatory compliance requirements, and sustainability commitments emphasizing energy efficient data center operations. European data center operators prioritize total cost of ownership optimization through deployment of energy efficient SSDs offering lower power consumption compared to traditional hard disk drives, aligning with stringent environmental regulations and corporate sustainability targets.

The region benefits from regulatory harmonization across European Union member states facilitating cross border technology deployment and standardization of procurement specifications. However, Europe faces challenges from dependence on imported NAND flash memory components and limited domestic manufacturing capacity relative to Asia Pacific competitors. Colocation data center providers concentrated in Frankfurt, Amsterdam, London, and Paris invest in high density infrastructure optimized for SSD deployment, supporting cloud service providers and enterprise tenants requiring low latency storage.

Asia Pacific Solid State Drive Market Share and Trends Analysis

Asia Pacific dominates the global solid state drive market with approximately 35% share, driven by vast consumer electronics manufacturing hub, presence of major NAND flash memory producers, and burgeoning demand from client and enterprise sectors. Countries including China, Japan, and South Korea lead regional adoption, leveraging robust electronics manufacturing capabilities and high-volume PC and smartphone production that drives SSD integration across consumer devices.

China's expanding technology industry and manufacturing capabilities show significant growth potential, while Japan emphasizes innovation in storage technologies through companies including Kioxia Corporation advancing 3D NAND architectures. South Korea hosts major semiconductor manufacturers Samsung and SK hynix that collectively influence global NAND supply dynamics and technology roadmaps. The burgeoning middle-class population and increasing disposable incomes across Asia Pacific countries drive consumer demand for SSD equipped devices including laptops, gaming consoles, and smartphones.

Competitive Landscape

The global solid state drive market exhibits moderate to high consolidation, with leading manufacturers including Samsung Electronics, Western Digital, Kioxia Holdings, SK hynix, and Micron Technology collectively controlling substantial market share through vertical integration spanning NAND flash production, controller development, and firmware optimization. Samsung maintains global leadership with approximately 27.9 % market share in third quarter 2024 despite facing intensified competition from Micron, Kioxia, and Western Digital, which expanded revenue and market positions through aggressive pricing and technology differentiation.

Market leaders differentiate through vertical integration strategies securing NAND flash supply and enabling cost advantages, while simultaneously investing in next generation technologies including PCIe 5.0 interfaces, computational storage, and Zoned Namespace implementations. The competitive landscape reflects ongoing consolidation as established semiconductor manufacturers leverage economies of scale and manufacturing expertise to maintain barriers against new entrants, although specialized players target niche segments including industrial SSDs, embedded solutions, and ruggedized products for automotive and aerospace applications.

Strategic Developments:

- In June 2025, Kioxia announced the LC9 SSD with a capacity of 245.76 TB. Built on PCIe 5.0, it is the highest-capacity drive the company has released, designed for data-heavy applications in enterprise and hyperscale environments.

- In August 2025, SanDisk unveiled a 256 TB UltraQLC NVMe SSD. Using its BiCS8 QLC NAND technology, the drive is built for cloud and enterprise customers that need very high capacity with lower power use. Shipments are expected to begin in 2026.

- In November 2024, Micron Technology introduced the 6550 ION, a 60 TB solid state drive designed for data centers. It uses the E3.S form factor with PCIe Gen 5 support and can deliver 12 GB/s of throughput while using only 20 watts of power. The drive is aimed at large-scale workloads such as AI, content delivery, and cloud storage.

Companies Covered in Solid State Drive Market

- Teclast Electronics Co. Limited

- Intel Corporation

- Transcend Information Inc.

- Samsung Group

- Kingston Technology Corporation

- Micron Technology Inc.

- ADATA Technology Co. Ltd.

- Western Digital Corporation

- SK Hynix Inc.

- Seagate Technology LLC

- Other Key Players

Frequently Asked Questions

The global Solid State Drive Market size was valued at US$ 70.1 Million in 2026 and is projected to reach US$ 191.0 Million by 2033, growing at a CAGR of 15.4% during the forecast period.

Key growth drivers include enterprise data center expansion supporting AI workloads, with hyperscale providers commanding 53.8% market share and expanding at 22.5 % CAGR, alongside PCIe interface technology advancement with over 80 % of enterprise SSDs shipped in 2024 utilizing NVMe protocol compared to just 36% in 2020.

Significant opportunities include AI-enabled PC and edge device storage expansion, with TrendForce observing accelerating demand for high-capacity, high-performance SSDs in 2025 as AI adoption increases, while market data shows 30% of AI-focused organizations now allocate over 40 % of storage budgets to performance-assured SSD tiers.

Asia Pacific dominates the global market with approximately 35% share, driven by China, Japan, and South Korea's vast consumer electronics manufacturing capabilities, presence of major NAND flash memory producers, and burgeoning demand from client and enterprise sectors.

Leading companies include Samsung Group with approximately 27.9 % share, Western Digital Corporation, Micron Technology Inc. with 15.6 % share, Kioxia Holdings Corporation, and SK hynix Inc.