- Home Appliances

- Portable Bluetooth Speakers Market

Portable Bluetooth Speakers Market Size, Share, and Growth Forecast 2025 - 2032

Portable Bluetooth Speakers Market by Product Type (Mini Speakers, Standard Speakers, Large Speakers), End-use (Residential, Commercial), by Distribution Channel (Online, Offline), by Regional Analysis, 2025-2032

Portable Bluetooth Speakers Market Size and Trend Analysis

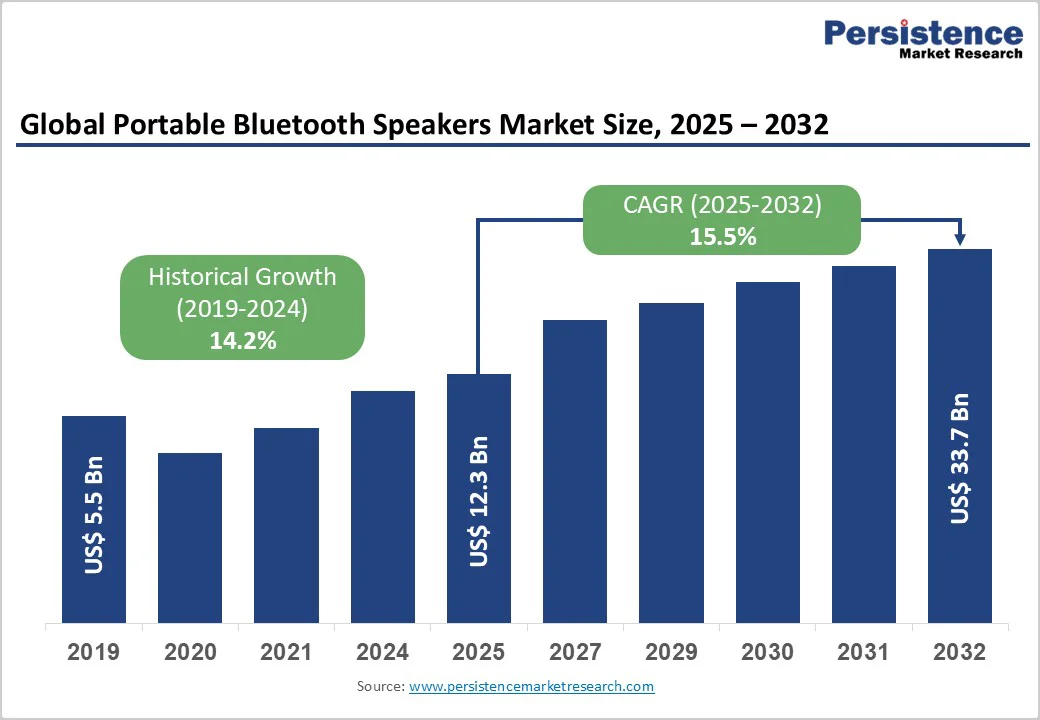

The global portable Bluetooth speakers market size is likely to value at US$ 12.3 billion in 2025 and is projected to reach US$ 33.7 billion, growing at a CAGR of 15.5% between 2025 and 2032. This remarkable expansion is primarily driven by the unprecedented rise in smartphone penetration and the explosive growth of music streaming platforms worldwide. With smartphone users reaching 4.88 billion globally in 2024, representing 60% of the world's population, and music streaming subscribers surpassing 818 million in 2024, consumers increasingly seek portable, high-quality wireless audio solutions to enhance their digital content consumption experience. Integrating advanced technologies, including Bluetooth 5.3, voice assistant compatibility with Amazon Alexa and Google Assistant, and enhanced battery life exceeding 16-30 hours has transformed portable bluetooth speakers from simple audio devices into multifunctional smart companions that seamlessly connect with modern digital ecosystems.

Key Industry Highlights:

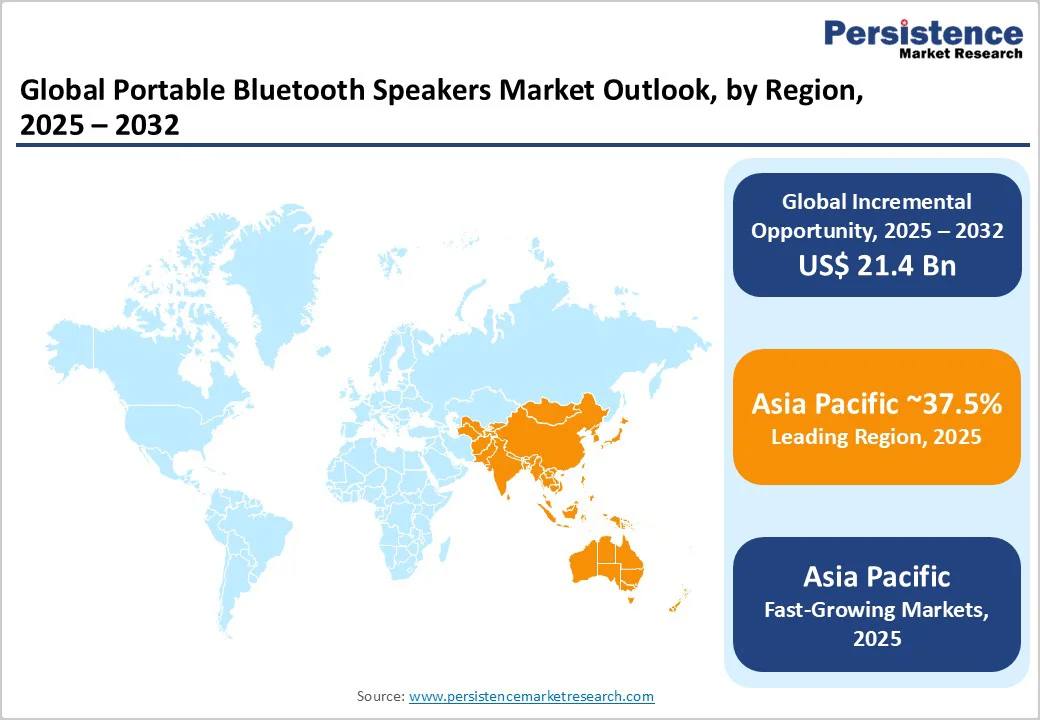

- Leading Region: Asia Pacific dominates the global portable Bluetooth speakers industry with a 37.5% market share in 2024, supported by vast consumer bases in China and India, booming e-commerce networks, and widespread smartphone adoption driving large-scale product demand.

- Fastest Growing Region: Asia Pacific also stands as the fastest-growing regional market, projected to surpass USD 11.28 billion by 2030, driven by India’s rapidly growing wireless speaker demand and widespread e-commerce adoption across emerging economies.

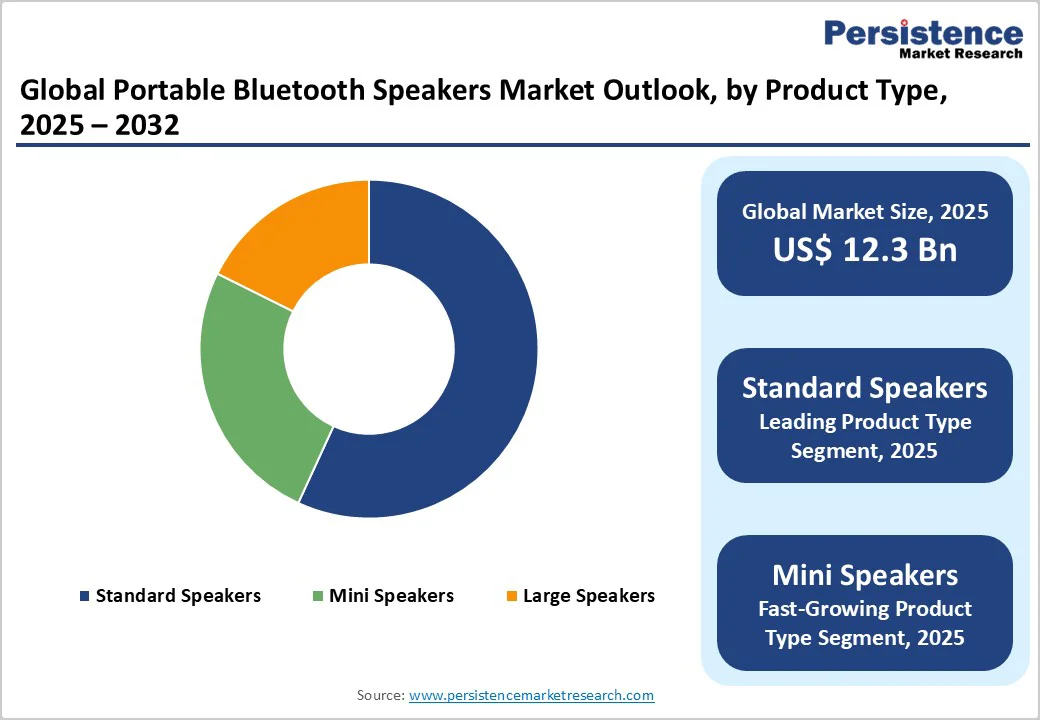

- Dominant Segment: In 2024, Standard Speakers accounted for about 58.7% of total market share, supported by strong consumer preference for mid-sized, feature-rich models combining power, portability, and durability across price tiers.

- Fastest Growing Application: The Commercial segment expanded steadily in 2024, contributing nearly 29% of total demand and projected to grow fastest at a 12.4% CAGR (2025–2032) due to increasing use in cafés, retail stores, and fitness spaces.

- Key Market Opportunity: Integration of AI voice assistants and smart home connectivity represents a major opportunity, as over 45% of European users now prefer Bluetooth speakers with hands-free control and smart interoperability.

| Key Insights | Details |

|---|---|

| Portable Bluetooth Speakers Market Size (2025E) | US$ 12.3 Bn |

| Market Value Forecast (2032F) | US$ 33.7 Bn |

| Projected Growth CAGR (2025-2032) | 15.5% |

| Historical Market Growth (2019-2024) | 14.2% |

Market Dynamics

Market Growth Drivers

Surge in Smartphone Penetration and Digital Content Consumption Propelling Market Expansion

The exponential rise in global smartphone adoption has become a major catalyst for the portable Bluetooth speakers market. As smartphone users reached 4.88 billion in 2024, representing over 60% of the world’s population, the demand for portable audio devices has surged. This number is projected to cross 5.28 billion by 2025 and 6.38 billion by 2029, creating a strong foundation for wireless audio consumption. Smartphones today serve as the central hub for music, podcasts, and entertainment, fueling the growing need for compact, high-fidelity Bluetooth speakers.

The proliferation of music streaming platforms like Spotify, Apple Music, and Amazon Music has accelerated this shift. Global streaming subscribers rose to 818 million in 2024, up 12% year-over-year, with Spotify alone holding a 32% market share. These platforms have revolutionized audio accessibility, motivating consumers to seek enhanced sound experiences through advanced portable Bluetooth speakers capable of delivering superior clarity, connectivity, and convenience across devices.

Growing Outdoor Recreation and Adventure Tourism Driving Demand for Durable Portable Audio Solutions

The rise in outdoor recreation and adventure tourism has significantly boosted the demand for rugged, weather-resistant Bluetooth speakers. Modern consumers increasingly favor models offering IPX4–IPX7 water resistance, with around 30% of Bluetooth speaker purchases in 2024 emphasizing waterproof features. The waterproof Bluetooth speaker segment, valued at USD 12 billion in 2023, is projected to reach USD 35.08 billion by 2029, reflecting a strong CAGR of 19.4%. This trend is closely tied to the expanding culture of outdoor activities and mobile entertainment preferences among youth and adventure travelers.

In regions like North America and Europe, outdoor tourism recorded over 1.1 billion trips in 2022 a 23% annual rise driving market momentum for durable audio solutions. Manufacturers are innovating with robust designs, extended 16–32-hour battery life, and shock-resistant materials. Leading brands such as JBL, Bose, and Sony are introducing IP67-rated speakers like the Boombox 3, SoundLink Flex, and SRS-XB100, which withstand dust, water submersion, and impact perfectly aligning with the needs of adventure enthusiasts.

Market Restraints

Intense Price Competition and Market Saturation Pressuring Profit Margins

The portable Bluetooth speakers market is increasingly challenged by fierce price competition and growing saturation, particularly across mature regions. The influx of cost-effective alternatives from Chinese and regional manufacturers has intensified pricing pressures, forcing premium brands such as Bose, JBL, Sony, and Apple to balance affordability with quality and innovation. Market analysis indicates over 50 active global players, with premium brands collectively holding around 35% of total market share reflecting high fragmentation and competitive overlap. This has led to shrinking profit margins and a continuous battle for brand differentiation through features, design, and sound performance.

Adding to this complexity is the rapid pace of technological evolution and short product life cycles that characterize the consumer electronics industry. Studies suggest nearly 40% of users replace their Bluetooth speakers within three years, often due to performance degradation or the introduction of newer models with enhanced connectivity, waterproofing, or smart integration. As a result, brands face constant pressure to innovate, manage production costs, and sustain profitability in an environment where price sensitivity and replacement frequency are both escalating.

Battery Life Limitations and Charging Infrastructure Constraints Hindering Extended Usage

Despite improvements in lithium-ion battery efficiency, battery life remains a key restraint limiting the extended usability of portable Bluetooth speakers. While premium models like JBL Boombox 3 and Marshall Emberton II promise playback times between 16 to 32 hours, real-world performance often falls short due to variable volume levels, environmental factors, and the use of advanced features. For instance, the Bose SoundLink Max offers around 20 hours of use, while Sony’s SRS-XB100 provides about 16 hours, yet both experience reduced runtime when employing high-volume playback, RGB lighting, or wireless pairing functionalities.

Moreover, dependence on USB-C charging though faster and more efficient still presents logistical challenges for travelers and outdoor users. Limited access to charging infrastructure, especially in remote or off-grid environments, can hinder continuous use, reducing convenience and reliability for consumers on the move. This constraint underscores the need for innovations in battery optimization, solar or kinetic charging systems, and energy-efficient speaker designs to overcome portability barriers in real-world usage scenarios.

Market Opportunities

Integration of Advanced AI Voice Assistants and Smart Home Ecosystem Connectivity Creating New Growth Avenues

The growing integration of AI-driven voice assistants within portable Bluetooth speakers is revolutionizing user interaction and expanding market potential. With global smart speaker shipments exceeding 87 million units in 2024 and the installed base of voice-enabled devices surpassing 320 million, consumer demand for seamless voice control continues to escalate. Platforms such as Amazon Alexa, Google Assistant, and Apple Siri have become integral to daily living, encouraging manufacturers to embed multi-assistant compatibility into portable models for greater versatility and convenience.

This convergence of smart technology is exemplified by products like JBL Authentics 300 and 500, which enable concurrent operation of Alexa and Google Assistant. Nearly 45% of European consumers now favor Bluetooth speakers offering voice-control features for hands-free operation supporting music playback, smart home management, and communication. As connectivity ecosystems mature, integrating AI assistants and IoT capabilities positions brands to capture premium value segments and foster long-term ecosystem engagement.

Expansion into Emerging Markets with Rising Middle-Class Populations and Digital Infrastructure Development

Rapid economic growth and expanding middle-class populations across emerging economies are unlocking substantial opportunities for portable Bluetooth speaker manufacturers. Markets in Asia Pacific, Latin America, the Middle East, and Africa are witnessing accelerated adoption driven by increasing disposable incomes, digital connectivity, and smartphone penetration. For instance, India’s wireless speaker market valued at USD 1.23 billion in 2024 is forecasted to reach USD 3.75 billion by 2032, reflecting a robust CAGR of 25.8%. Likewise, Saudi Arabia’s Bluetooth speaker market is expected to nearly double by 2030, fueled by over 90% smartphone and 99% internet penetration.

These developing regions present favorable demographic trends, including large youth populations, rising urbanization, and growing e-commerce access that simplifies product discovery and online purchasing. As consumers embrace premium audio experiences, global brands have an opportunity to localize their offerings focusing on affordable smart-enabled models and region-specific marketing to capture the accelerating demand in these digitally evolving markets.

Category-wise Insights

Product Type Analysis

The Standard Speakers segment leads the portable Bluetooth speaker market in 2025, holding about 58% share, driven by a balance between audio quality, portability, and pricing. Models such as JBL Flip 6 and Sony SRS-XB33 deliver 20–40W output, 12–24-hour battery life, and IPX5–IPX7 resistance, appealing to residential and outdoor users. Asia Pacific shows particularly strong demand for standard-sized speakers.

The Mini Speakers category, however, is the fastest-growing, favored for compactness and affordability. With 5–10W power output, lightweight designs, and Bluetooth 5.3 connectivity, these devices cater to travelers and young consumers. Innovation in micro-drivers, solar charging, and voice assistant integration supports its rapid expansion.

End-Use Analysis

The Residential segment dominates with around 71% share in 2025, reflecting rising smart home integration and the popularity of music streaming services like Spotify and Apple Music. Consumers seek Bluetooth speakers that sync with home systems, offer superior sound, and enhance interior aesthetics.

Meanwhile, the Commercial segment is the fastest-growing, driven by adoption in cafés, gyms, and hospitality spaces for ambiance and flexible audio setups. Businesses prefer speakers with durability, longer battery life, and multi-speaker pairing for better area coverage. The increasing focus on outdoor entertainment and energy-efficient wireless systems further fuels growth.

Distribution Channel Analysis

The Offline channel remains the market leader, accounting for roughly 62% of global sales in 2025, as consumers value in-store product trials, expert advice, and trusted retail experiences. Stores like Best Buy, Walmart, and Croma play key roles in driving sales through demos and bundled promotions.

However, the Online channel shows the fastest growth, expected to register a CAGR above 18%. Platforms such as Amazon and Alibaba offer broader selections, competitive pricing, and verified reviews. The convenience of doorstep delivery and expanding direct-to-consumer (D2C) websites enhance accessibility, making e-commerce the most dynamic sales avenue.

Regional Insights

North America Portable Bluetooth Speakers Market Trends

North America holds a 28.4% market share in 2024, continuing to lead the global portable Bluetooth speakers landscape. The U.S. dominates the region, driven by 77% smartphone penetration (251.7 million users), a mature music streaming ecosystem, and strong demand for feature-rich devices. American consumers favor models with Amazon Alexa and Google Assistant integration, multi-room audio, and rugged IP67-rated designs aligning with outdoor and recreational lifestyles.

Canada contributes notably through its sustainability-focused consumer base, encouraging brands like Sony and Marshall to adopt recycled materials. Meanwhile, Mexico represents the fastest-growing submarket, supported by a rising middle class, urbanization, and e-commerce growth. Regional sales momentum is reinforced by expanding retail networks and increasing cross-platform content streaming adoption, which continue to elevate demand for connected portable audio devices.

Europe Portable Bluetooth Speakers Market Trends

Europe accounts for 24.8% of the global market share in 2024, representing a mature yet innovation-driven region. The market is propelled by high disposable incomes, widespread smart home adoption, and a strong preference for audio quality and design aesthetics. Germany leads the region with high affinity for premium audio engineering and brands such as Bose, Sennheiser, and Bang & Olufsen. European consumers increasingly emphasize sustainability and eco-friendly materials, influencing production trends.

The United Kingdom and France maintain significant market shares, supported by strong smartphone penetration and vibrant tourism industries. The continent recorded 1.1 billion tourism trips in 2022, boosting sales of portable speakers as travel essentials. Southern European nations, including Spain and Italy, also exhibit rising demand linked to outdoor leisure culture. Europe’s premiumization and sustainable technology focus continue to shape competitive product differentiation.

Asia Pacific Portable Bluetooth Speakers Market Trends

Asia Pacific dominates the global landscape with a 37.5% market share in 2024, positioning it as both the leading and fastest-growing regional market. China drives the region’s strength as a manufacturing and consumption hub, supported by 782.8 million smartphone users and robust e-commerce ecosystems led by Alibaba, JD.com, and Pinduoduo. Local brands like Xiaomi, Huawei, and Edifier excel through affordable, feature-rich products that expand domestic accessibility.

India emerges as the fastest-growing submarket with a 25.8% CAGR (2026–2032), fueled by youth-driven adoption, online retail penetration, and strong brand loyalty toward boAt and Noise. Japan and South Korea sustain steady demand for high-end speakers, while Southeast Asian countries like Indonesia, Vietnam, and Thailand contribute dynamic growth due to urbanization and middle-class spending. Regional innovation, affordability, and large-scale consumer bases firmly anchor Asia Pacific’s global leadership.

Competitive Landscape

The portable Bluetooth speakers market features a moderately consolidated structure, defined by the coexistence of global premium brands and numerous regional players. Competition centers on sound quality, durability, battery performance, smart features, and price differentiation, spanning from entry-level to high-end segments. Leading manufacturers focus on technological innovation, integrating advanced Bluetooth connectivity, proprietary acoustic enhancement systems, and AI voice assistant compatibility to strengthen their market presence and sustain consumer loyalty.

The competitive intensity has increased significantly with the rise of regional value-driven manufacturers, particularly across emerging Asian markets. These brands emphasize affordability, strong online distribution, and feature-rich designs that rival premium products. In response, established players continue to invest in product diversification, strategic collaborations, and customer experience enhancements such as longer warranties and improved after-sales support to maintain their market advantage.

Key Market Developments

- In August 2024, Marshall launched the Emberton III and Willen II portable Bluetooth speakers in India, offering 32+ and 17+ hours of battery life, IP67 dust and water resistance, Bluetooth 5.3, and enhanced sound quality. They were priced at ?17,999 and ?12,499, respectively.

- In October 2024, Bose unveiled the second-generation SoundLink Flex portable Bluetooth speaker featuring upgraded Bluetooth 5.3 connectivity, support for AAC and AptX codecs, a customizable shortcut button, and Bose mobile app compatibility for enhanced performance and control.

- In 2024, JBL expanded its lineup with the Boombox 3, offering 29+ hours of playtime and IP67 protection, along with the Authentics 300 and 500 smart speakers supporting simultaneous operation of Amazon Alexa and Google Assistant.

Companies Covered in Portable Bluetooth Speakers Market

- Apple Inc.

- BoAt Bose Corporation

- Edifier

- Koninklijke Philips N.V.

- LG Electronics

- Logitech

- Marshall Group AB

- Panasonic Corporation

- Polk Audio

- Samsung Electronics

- Sennheiser Electronic SE & Co. KG

- Sony Corporation

- Harman International (JBL)

- Bang & Olufsen

- Ultimate Ears

- Anker Soundcore

- Xiaomi

- Amazon

- Sonos

- Tribit

- Beats by Dre

- Altec Lansing

Frequently Asked Questions

The global portable Bluetooth speakers market is valued at US$ 12.3 Bn in 2025 and projected to reach US$ 33.7 Bn by 2032, growing at a CAGR of 15.5%.

Growth is driven by rising smartphone penetration, booming music streaming usage, expanding outdoor recreation, smart home integration, and Bluetooth 5.3-enabled innovations.

The Standard Speakers segment dominates with around 58% market share in 2025, owing to balanced performance, portability, and mid-range pricing.

Asia Pacific leads with 37.54% market share in 2023, supported by large populations, smartphone growth, and thriving e-commerce ecosystems.

Integration of AI voice assistants and smart home connectivity offers major opportunities for product differentiation and user engagement.

Key players include Apple, Bose, Sony, JBL, Samsung, Marshall, Sennheiser, LG, Logitech, BoAt, Anker, Xiaomi, Edifier, UE, Bang & Olufsen, Amazon, Google, and Sonos.