- Home Appliances

- Home Theater Audio Systems Market

Home Theater Audio Systems Market Size, Share, and Growth Forecast 2026 - 2033

Home Theater Audio Systems Market by Product Type (Home Theatre in A Box System, Sound Bar and Component System), by Distribution Channel (Offline and Online), and Channel Configuration (2.1 Channel, 5.1 Channel, 7.1 Channel and 9.1 Channel) and Regional Analysis for 2026 – 2033

Home Theater Audio Systems Market Size and Trend Analysis

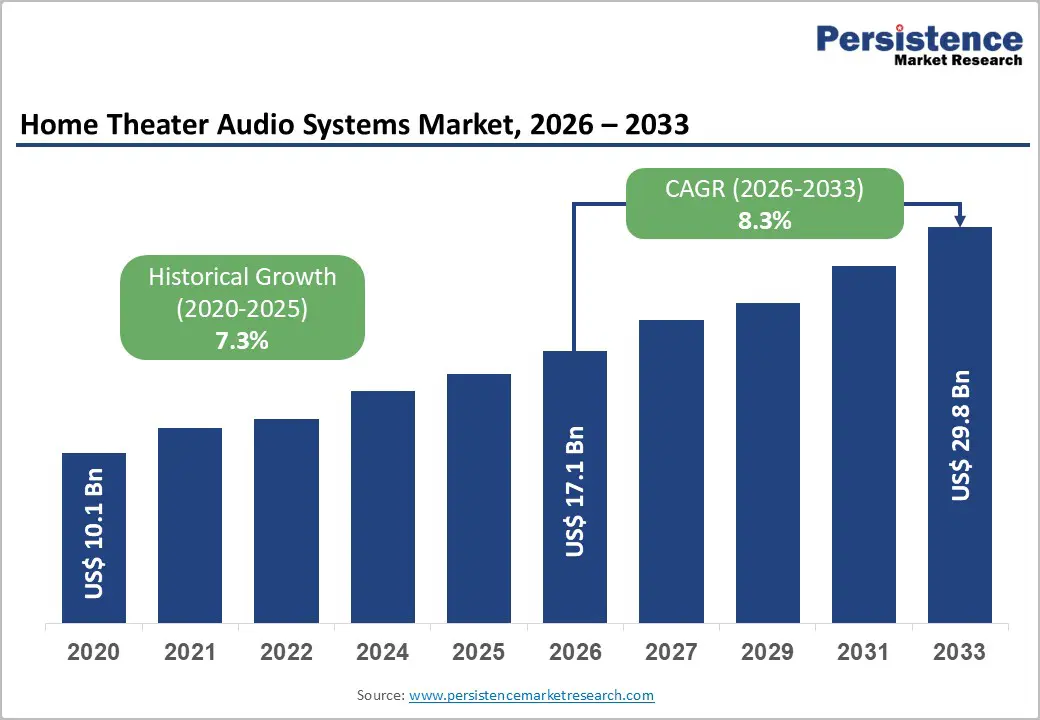

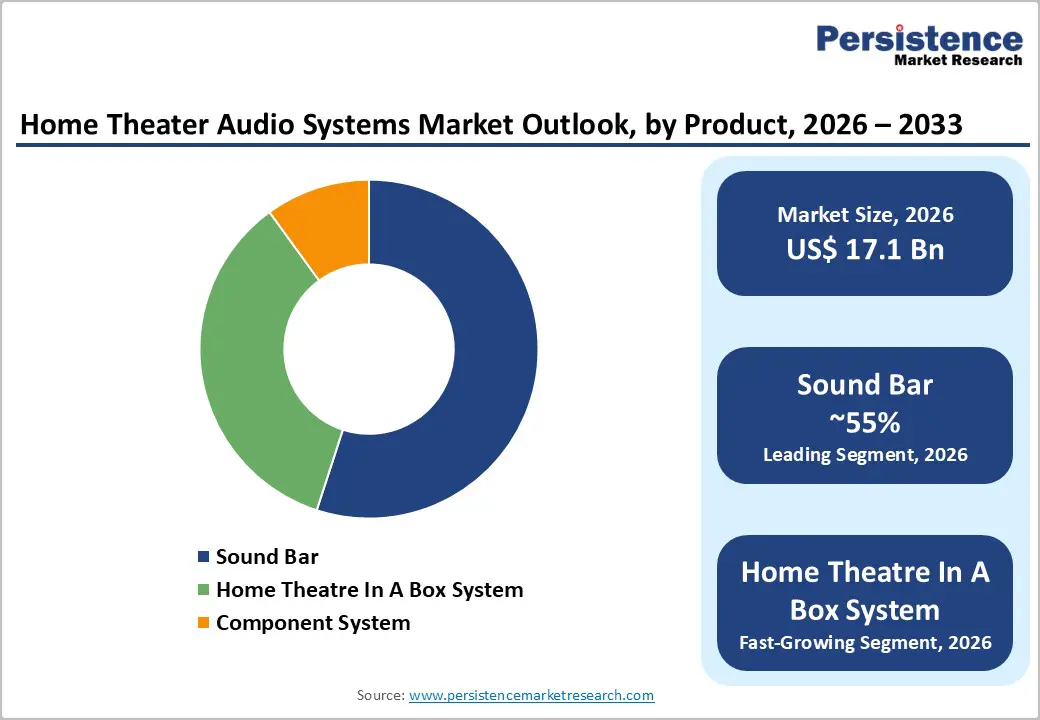

The global home theater audio systems market size was valued at US$ 17.1 Bn in 2026 and is projected to reach US$ 29.8 Bn by 2033, growing at a CAGR of 8.3% between 2026 and 2033. Strong consumer inclination toward premium in-home entertainment, along with rising availability of high-quality multichannel content from subscription streaming platforms, underpins this outlook. Growing household expenditure on audio-visual equipment classified under COICOP 09.1.1 (television sets, stereo systems, amplifiers, and speakers) is supported by international statistics frameworks, reflecting that a larger share of discretionary income is being allocated to such devices as ICT access deepens globally.

Key Market Highlights

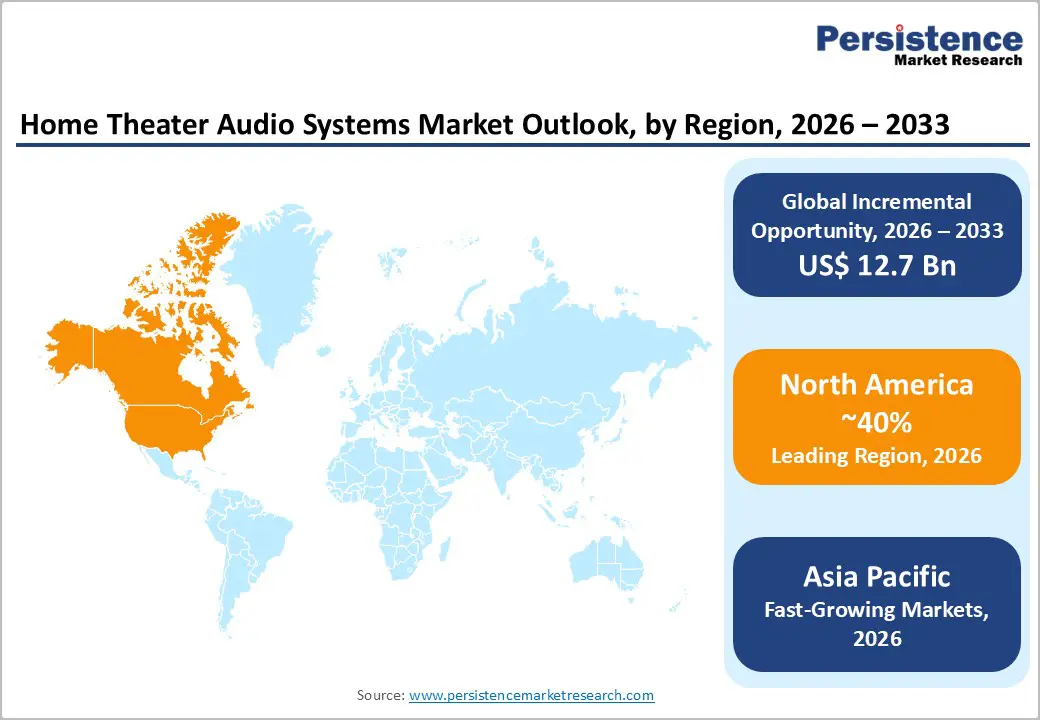

- Leading region: North America leads the Home Theater Audio Systems Market, supported by high streaming penetration, strong recorded music revenues above 40% of global total, and widespread suburban homes enabling adoption of 5.1 and higher?channel setups.

- Fastest growing region: Asia Pacific is the fastest?growing region, driven by rising middle?class incomes in China, India, and ASEAN, expanding ICT access, and large?scale local manufacturing that makes soundbars and 5.1 systems increasingly affordable.

- Dominant segment: Sound bars dominate the product landscape with an estimated share of around 55%, benefiting from simple installation, slim designs suited to flat?panel TVs, and rapid adoption of virtual surround and Dolby Atmos features in mainstream price bands.

- Fastest growing segment: Wireless and 5.1 channel configurations are emerging as the fastest?growing segments, as consumers seek immersive experiences without complex wiring, supported by streaming platforms standardizing multi?channel audio content.

- Key market opportunity: Integration of home theater audio systems into broader smart home and streaming ecosystems leveraging advanced sensing, room calibration, and voice control offers sizeable, long?term revenue potential for brands that can differentiate beyond hardware specifications.

| Key Insights | Details |

|---|---|

| Home Theater Audio Systems Market Size (2026E) | US$ 17.1 Bn |

| Market Value Forecast (2033F) | US$ 29.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 7.2% |

Market Dynamics

Market Growth Drivers

Rising streaming consumption and immersive content adoption

A key growth drive for the home theater audio systems market is the explosive growth of licensed music and video streaming, which is reshaping expectations for in-home sound quality. Global music industry data show that subscription streaming revenues have risen consistently, with streaming accounting for well over 60% of recorded music revenues and continuing to grow at single to double-digit rates annually, according to the IFPI Global Music Report series, where subscription streaming alone expanded by around 9.5% in 2024 and global recorded music revenues grew by 4.8% to roughly US$ 29.6 billion. As consumers spend over 20 hours per week listening to music across formats and over two-thirds of people use streaming services, demand for better playback hardware in the living room naturally increases.

Growing household ICT access and expenditure on audio-visual equipment

Another structural driver arises from the expanding base of households with multichannel television and rising ICT expenditure. International standards for ICT household statistics highlight that equipment for the reception, recording and reproduction of sound and picture, such as televisions, stereo systems, amplifiers, and speakers, forms a distinct category where expenditure is tracked as part of household ICT spending. As more households gain access to multichannel TV and high-speed broadband, the share of budgets devoted to AV equipment increases, reinforcing replacement and upgrade cycles toward higher value audio configurations. The proportion of households equipped with advanced televisions and set top boxes has grown steadily in both developed and emerging markets, while ICT household manuals emphasize multichannel TV and audio as core access indicators.

Market Restraints

Price sensitivity and competition from affordable alternatives

Despite robust demand, price sensitivity among mass?market consumers remains a notable restraint. Many households still consider multi?component home theater systems as discretionary purchases that must compete with other digital devices such as smartphones, tablets, and laptops, all of which also claim a share of ICT expenditure outlined in international classifications. In parallel, low?cost Bluetooth speakers and compact sound solutions provide “good?enough” audio for a portion of the market, diluting demand for higher?end multi?speaker packages. Households in lower income brackets or in regions with constrained purchasing power may prioritize single?device solutions or delay upgrades, limiting penetration of premium 5.1 or 7.1 channel systems. The presence of affordable alternatives at various price points, especially from regional brands and white?label manufacturers, can compress margins and slow value growth even when unit volumes increase.

Space constraints and installation complexity in urban dwellings

Another restraint is the practical challenge of installing full multi?speaker configurations in compact living spaces. Rapid urbanization has resulted in smaller apartments across major cities, leaving limited room for 7.1 or 9.1 channel setups that require optimal speaker placement to deliver their intended performance. International ICT access manuals note that device availability within households is conditioned by physical space and ease of use, with equipment expected to be in working condition and accessible to household members. Many consumers are deterred by perceived installation complexity, cable management issues, and the need for calibration to achieve surround sound, especially in rental homes where structural changes are restricted. This pushes some buyers toward simpler soundbars and 2.1 systems, restraining demand for larger component?based home theaters that could contribute more strongly to premium segment value growth.

Market Opportunities

Premium soundbars and wireless multi?channel solutions as fast?growing niches

A major opportunity for market participants lies in premium soundbars and wireless multi?channel systems that combine installation simplicity with immersive performance. Industry trends indicate that soundbars have already emerged as leading sub?segments in related home audio markets, often accounting for more than 50% share of home theater?type revenues as consumers favor sleek, space?saving designs with virtual surround capabilities. By integrating upward?firing drivers, dedicated subwoofers, and rear wireless speakers, manufacturers can deliver a near?5.1 or 7.1 experience without the complexity of full component systems, thus unlocking incremental demand in urban and rental housing. The synergy between the Home Theater Audio Systems Market and adjacent segments such as intelligent speakers and audio production equipment creates scope for technology transfer and bundled offerings that enhance perceived value.

Integration with smart home ecosystems and advanced sensing technologies

Another promising opportunity is deeper integration of home theater audio systems with broader smart home ecosystems, including televisions, voice assistants, and potentially advanced sensing hardware. The rise of connected devices, as documented in ICT usage frameworks, shows that households increasingly expect interoperability between entertainment, communication, and control devices. This opens avenues for systems that can automatically adjust sound profiling based on occupancy, content type, or even room acoustics, borrowing concepts from emerging sensing markets such as the Quantum Sensors Market where high?precision measurement is central to performance claims. While quantum sensing itself is still nascent in consumer audio, the narrative of precision, personalization, and adaptive response aligns well with premium home theater positioning. Companies that integrate multi?room audio, voice?activated controls, and low?latency wireless protocols into cohesive ecosystems with TVs, set?top boxes, and gaming consoles can differentiate beyond raw wattage or channel count, creating sticky platforms that drive attachment sales of additional speakers and accessories over the forecast period.

Category-wise Insights

Product Type Analysis

Within product types, sound bars are estimated to command the leading share of the Home Theater Audio Systems Market, accounting for roughly 55% of global revenues in recent years. Industry analyses of related home theatre systems highlight soundbars achieving around 55% share of the segment as early as 2024, driven by their compact form factor and ease of installation compared with traditional component systems. Consumers increasingly pair soundbars with large?screen smart TVs to compensate for the limited audio performance of ultra?thin panels, while integrated features like Dolby Atmos, wireless subwoofers, and HDMI eARC connectivity enhance appeal. The ability to deliver virtual surround sound without extensive wiring makes soundbars ideal for apartments and rental homes, reducing barriers associated with space and complexity.

Distribution Channel Outlook Analysis

In terms of distribution channels, offline retail is likely to retain a marginal lead, contributing an estimated 47% share of global home theater audio system sales, even as online channels grow rapidly. Evidence from closely related audio markets shows offline consumer?electronics stores holding about 46% market share because many consumers prefer to audition sound quality, especially bass performance, before purchase. Brick?and?mortar outlets offer dedicated demo rooms, sales staff guidance, and value?added services like installation and calibration, which are particularly relevant for multi?speaker systems. At the same time, the rise of e?commerce, supported by detailed product reviews, augmented?reality visualization, and flexible return policies, is steadily shifting a substantial portion of sales online, especially for soundbars and entry?level packages.

Channel Configuration Analysis

Across channel configurations, 5.1 channel systems are expected to maintain leadership, with an approximate global share in the range of 45% of configured home theater audio installations. The 5.1 layout comprising front left, right, center, two surround speakers, and a subwoofer has long been the de facto standard for DVD, Blu?ray, and many streaming titles, aligning with established content mastering practices and consumer familiarity. International audio?visual system frameworks from bodies such as the ITU have historically referenced multi?channel arrangements, including 5.1, as baseline configurations for surround sound services, supporting their continued relevance in households. While 2.1 systems dominate the entry level and 7.1 or 9.1 configurations are gaining traction among enthusiasts, 5.1 offers the optimal balance between immersion, hardware cost, and space requirements for mainstream buyers. The widespread availability of 5.1?encoded content on streaming platforms and physical media further reinforces this configuration’s dominance, encouraging consumers upgrading from stereo setups to adopt it as their first surround sound experience.

Regional Insights

North America

North America is a leading region in the Home Theater Audio Systems Market, underpinned by high broadband penetration, strong OTT subscription levels, and a culture of in?home entertainment. The U.S. and Canada together account for more than 40% of global recorded music revenues, with streaming commanding the majority share of that revenue base. As households spend more than 20 hours per week consuming music and significant additional time on video content, demand for high?performance home audio equipment naturally follows. Suburban housing patterns in the U.S., characterized by larger living spaces and dedicated media rooms, facilitate adoption of 5.1 and higher channel configurations, while soundbars gain traction in urban apartments where space is constrained.

The region also benefits from a strong innovation ecosystem, with leading brands such as Bose Corporation, Sony Corporation, SAMSUNG, and LG Electronics maintaining sizeable R&D footprints and launching Atmos?enabled bars and wireless surround packages tailored to North American preferences. Regulatory frameworks on energy efficiency and product safety are well defined, influencing design choices such as auto?standby functions and low?power wireless protocols, in line with ICT equipment guidelines for household devices.

Europe Home Theater Audio Systems Market Trends

In Europe, the home theater audio systems market is shaped by a combination of mature audio traditions, strong regulatory harmonization, and diverse housing stock across countries such as Germany, the U.K., France, and Spain. European consumers have historically maintained significant expenditure on audio?visual equipment, as evidenced by household budget classifications that single out stereo systems, amplifiers, and speakers as distinct spending categories. At the same time, the region’s recorded music revenues continue to grow, supported by high streaming penetration and strong adoption of licensed services, which incentivizes consumers to upgrade playback hardware for improved listening experiences.

Regulatory harmonization across the European Union, including directives on eco?design, recyclability, and hazardous substances, shapes product design and lifecycle considerations for home theater audio systems. Manufacturers must comply with uniform energy labeling and safety standards, which affects amplifier efficiency, standby consumption, and material selection. This environment encourages innovation in efficient Class?D amplification and durable, recyclable enclosures, providing differentiation opportunities for brands that position themselves around sustainability.

Asia Pacific Home Theater Audio Systems Market Trends

The Asia Pacific region represents the fastest?growing opportunity for the Home Theater Audio Systems Market, driven by rising disposable incomes, rapid urbanization, and expanding middle?class households in China, India, Japan, and ASEAN economies. Global ICT statistics underline a steady increase in household access to televisions, computers, and broadband across East and South Asia, reinforcing the foundation for adoption of advanced audio?visual equipment. In China and India, a surge in smartphone and streaming usage where up to 96% of respondents in some studies report using smartphones to listen to music has familiarized consumers with on?demand content and encouraged them to seek higher?quality listening experiences at home.

From a manufacturing perspective, Asia Pacific holds a critical cost and scale advantage, hosting major production bases for global brands such as SAMSUNG, LG Electronics, and Sony Corporation, as well as numerous OEM/ODM suppliers. The presence of vertically integrated supply chains for semiconductors, drivers, and enclosures allows competitive pricing and rapid feature upgrades aligned with global streaming trends. Governments in countries like China and India are also promoting domestic electronics manufacturing under various initiatives, which indirectly supports the regional availability and affordability of home theater audio systems.

Competitive Landscape

Market Structure Analysis

The competitive landscape of the Home Theater Audio Systems Market is moderately concentrated, with a cluster of global consumer electronics leaders and several specialized audio brands. Companies such as Bose Corporation, Sony Corporation, SAMSUNG, LG Electronics, and Panasonic Corporation leverage broad product portfolios and strong brand equity to anchor the premium and mid?range tiers, often bundling audio systems with televisions or offering ecosystem?based integration across devices. At the same time, specialist manufacturers like Bowers & Wilkins, Atlantic Technology, Definitive Technology, and GoldenEar focus on high?fidelity component systems and audiophile?grade speakers, differentiating through acoustic engineering, enclosure design, and proprietary tuning technologies.

Key Market Developments

- In May 2025, LG Electronics released the Alpha-Sound Q950 system featuring an AI chip that recalibrates beam width every minute; pilot sales in Seoul sold out on launch day.

- In April 2025, Sony issued a firmware update that adds Bluetooth LE Audio to its 2024 HT-A9000 bar, extending the product’s lifecycle.

- In March 2025, Samsung completed its USD 120 million purchase of WiSA Technologies to embed multichannel IP into 2026 TV system-on-chip roadmaps.

Companies Covered in Home Theater Audio Systems Market

- Bose Corporation

- LG Electronics.

- Panasonic Corporation

- Sony Corporation

- SAMSUNG

- Koninklijke Philips N.V.

- Bowers & Wilkins

- Atlantic Technology

- Definitive Technology

- dba GoldenEar

- Other Key Players

Frequently Asked Questions

The global Home Theater Audio Systems Market is estimated at US$ 17.1 Bn in 2026 and is projected to reach US$ 29.8 Bn by 2033, registering a CAGR of 8.3% over 2026–2033, supported by rising streaming consumption and higher household ICT spending on audio‑visual equipment.

Key demand drivers include rapid growth in licensed music and video streaming, with streaming commanding more than 60% of recorded music revenues, time spent listening to music exceeding 20 hours per week, and expanding household access to televisions and multichannel TV services that stimulate upgrades to immersive audio solutions.

By product type, sound bars lead the market with an estimated share of about 55%, owing to their slim design, easy installation, and ability to deliver virtual surround sound and Dolby Atmos experiences as companions to flat‑panel smart TVs and streaming platforms.

North America holds a leading position due to its large base of streaming subscribers, high recorded music revenues exceeding 40% of the global total, extensive broadband and smart TV penetration, and housing characteristics that support adoption of 5.1 and higher‑channel home theater configurations.

Major players include Bose Corporation, LG Electronics, Panasonic Corporation, Sony Corporation, and SAMSUNG.