- Home Appliances

- Smart Pillow Market

Smart Pillow Market Size, Share, Trends, and Growth Forecast 2026 - 2033

Smart Pillow Market by Product Type (Anti-snoring, Multifunctional, Others), Fill Material (Down and Feather, Cotton, Wool, Polyester, Foam, Others), Application (Residential, Commercial), Sales Channel (Online, Offline), Regional Analysis, 2026 - 2033

Smart Pillow Market Size and Trend Analysis

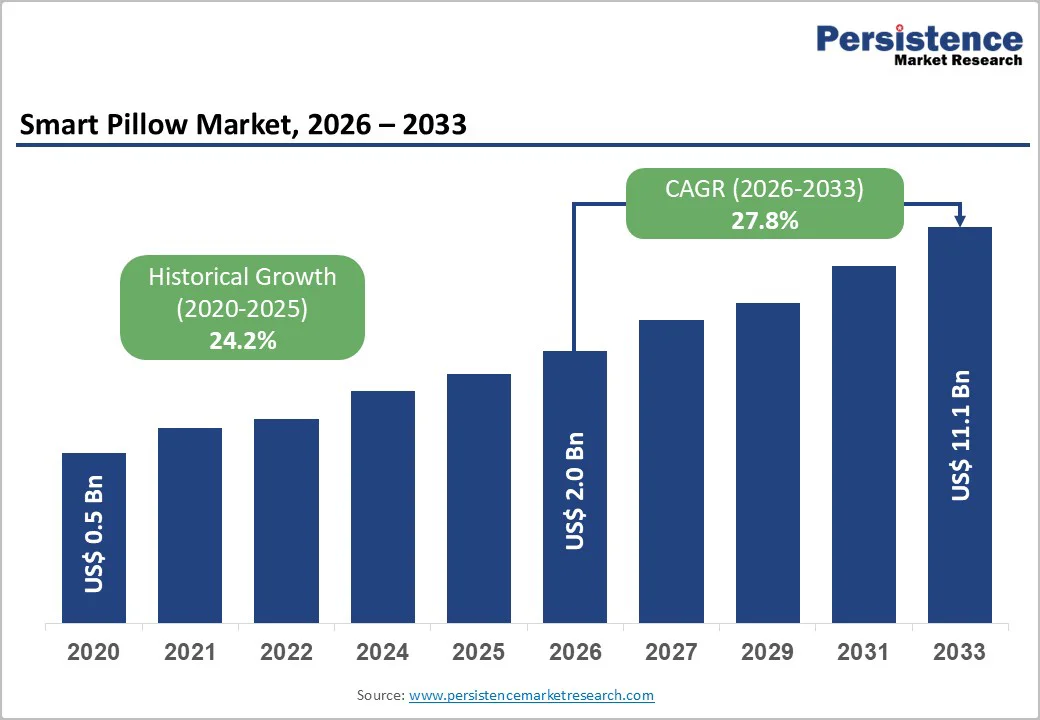

The global smart pillow market size is projected to grow from an estimated US$ 2.0 billion in 2026 to US$ 11.1 billion by 2033, reflecting a robust CAGR of 27.8% between 2026 and 2033. This expansion is largely driven by the increasing prevalence of sleep disorders worldwide, with authorities like the WHO and CDC highlighting insufficient sleep as a growing public health concern.

As a result, consumers are increasingly adopting technology-driven sleep solutions that go beyond conventional bedding, offering real-time monitoring and biofeedback to enhance sleep quality. Integration with smart home ecosystems through devices such as the Eight Sleep Pod or Nitetronic anti-snore pillows is further transforming pillows into advanced health-monitoring tools, fueling market growth.

Key Market Highlights:

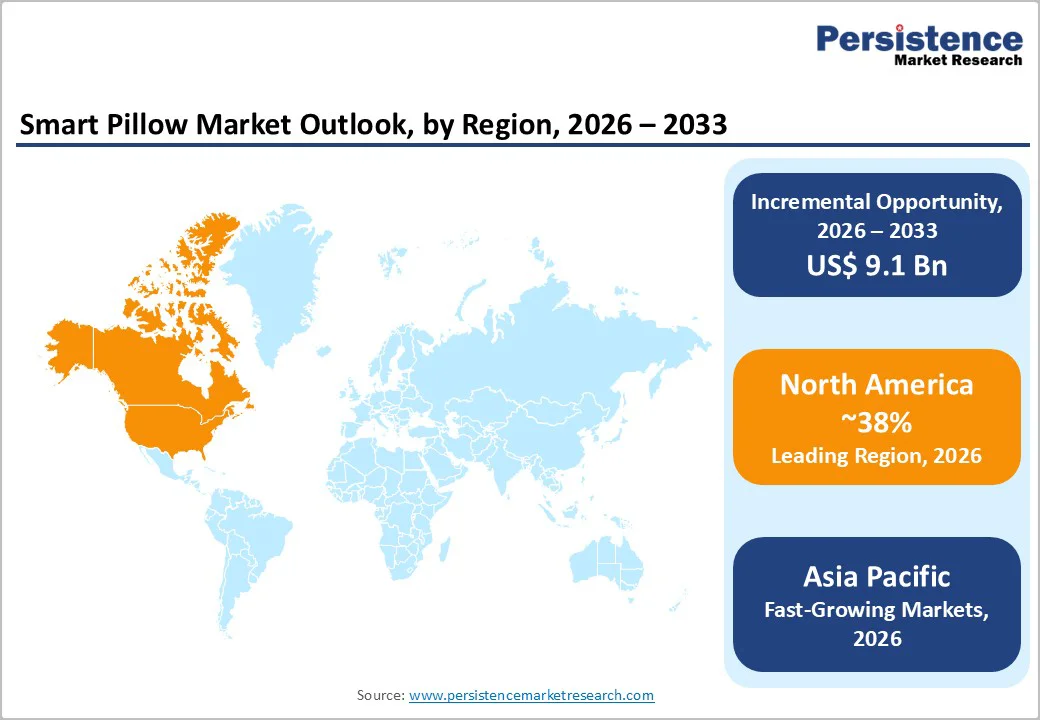

- Leading Region: North America dominates the smart pillow market with a 38% share, supported by high-tech adoption, widespread awareness of sleep health solutions, and a mature ecosystem of connected devices.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, holding a 32% share, driven by rising disposable incomes in China and India, rapid urbanization, and local manufacturing advantages that allow competitive pricing of smart pillows.

- Dominant Segment: The Residential application segment leads the market with a 72.1% share, as individual consumers increasingly invest in personal wellness, sleep optimization, and bedroom technology upgrades.

- Fastest Growing Segment: The Online sales channel is expanding most rapidly, accounting for 52.5% of the market, fueled by direct-to-consumer models, social media marketing, and risk-free home-trial policies for premium smart pillows.

- Key Opportunity: Securing FDA approval for diagnostic capabilities offers a significant opportunity to transform smart pillows from lifestyle gadgets into reimbursed medical devices, opening access to patients and insurance-funded sales.

| Key Insights | Details |

|---|---|

|

Smart Pillow Market Size (2026E) |

US$ 2.0 Billion |

|

Market Value Forecast (2033F) |

US$ 11.1 Billion |

|

Projected Growth CAGR (2026-2033) |

27.8% |

|

Historical Market Growth (2020-2025) |

24.2% |

Market Dynamics

Drivers - Rise in Global Prevalence of Sleep Disorders and Apnea Boosting Demand for Smart Pillows

The escalating incidence of sleep disorders, particularly Obstructive Sleep Apnea (OSA) and chronic insomnia, is a major catalyst for the smart pillow market. According to The Lancet Respiratory Medicine, nearly 1 billion people worldwide suffer from sleep apnea, with most cases going undiagnosed. As awareness increases, consumers are seeking non-invasive alternatives before resorting to CPAP machines or other medical interventions.

Smart pillows from companies such as Nitetronic and Smart Nora use airbag inflation to gently reposition the head and maintain open airways, directly addressing this need. The shift from traditional passive comfort to active health intervention is encouraging consumers to invest in premium sleep technology. This growing preference for data-driven sleep solutions is contributing to substantial year-over-year revenue growth in the sector.

Rapid Expansion of Smart Home Ecosystems Facilitating Integration of Connected Sleep Devices

The accelerated adoption of smart home technologies, particularly in North America and Europe, is creating a favorable environment for connected sleep products. Reports indicate that North America accounts for nearly 40% of global smart home consumer spending, highlighting the region’s readiness for integrated smart devices. As households become increasingly connected, consumers expect bedroom appliances to function seamlessly with platforms like Alexa or Google Home.

Multifunctional smartpillows that track sleep cycles, regulate temperature, and optimize wake-up times are emerging as essential components of the “IoT of Sleep.” Companies such as Xiaomi leverage this ecosystem approach, enabling smart pillows to synchronize with other smart home devices. This integration enhances convenience, delivers a comprehensive sleep experience, and strengthens the overall value proposition for consumers.

Restraints - High Product Cost and Affordability Challenges Limiting Mass Adoption of Smart Pillows

One of the primary barriers to mass adoption of smart pillows is their relatively high cost compared to standard bedding. While conventional memory foam or polyester pillows are generally available at affordable prices, many smart pillows equipped with sensors, heating elements, and AI connectivity often retail for $100 to $400, depending on features and brand. This price disparity limits accessibility, particularly for price-sensitive consumers in emerging markets, and confines adoption largely to high-income demographics in developed regions.

Economic pressures and rising inflation in 2024 and 2025 have further heightened consumer sensitivity toward discretionary spending. Consequently, manufacturers face challenges in penetrating mass-market retail channels without introducing lower-cost models or flexible pricing strategies, which can slow broader market growth despite increasing awareness of sleep health benefits.

Data Privacy and Security Concerns Acting as a Barrier to Consumer Confidence

The collection of sensitive biometric information, including heart rate, respiratory patterns, and sleep sounds, raises substantial privacy and security concerns. Smart pillows often rely on companion mobile apps and cloud connectivity to function effectively, which exposes user data to potential breaches and misuse.

In an era where consumers are increasingly vigilant about personal health data protection, fears of unauthorized access or surveillance can discourage adoption. Additionally, strict regulatory frameworks such as GDPR in Europe impose high compliance costs on manufacturers. Any high-profile data breach or security lapse could severely erode consumer trust in smart pillows and impede market growth.

Opportunity - Leveraging AI Integration and Medical-Grade Diagnostic Capabilities to Expand Market Potential

The convergence of consumer sleep technology with medical diagnostics presents a significant growth opportunity for smart pillow manufacturers. Companies like Eight Sleep are investing heavily in AI-powered "Sleep Agents" capable of detecting early signs of health conditions such as atrial fibrillation or sleep apnea patterns. These advanced features enable smart pillows to move beyond conventional sleep aids and position themselves as tools for proactive health monitoring.

By obtaining FDA clearance for diagnostic capabilities, manufacturers can transform smart pillows from lifestyle gadgets into medical-grade devices. This transition opens avenues for reimbursement through health insurance providers, expanding the potential customer base to patients prescribed these devices by healthcare professionals, rather than relying solely on tech-savvy consumers or wellness enthusiasts.

Expanding Commercial Applications in Hospitality and Wellness Sectors to Drive Revenue

The hospitality and wellness sectors offer a lucrative avenue for smart pillow adoption, particularly in luxury hotels, aviation, and wellness retreats. High-end hotel chains are increasingly differentiating their services through “Sleep Tourism,” promising scientifically optimized rest for guests. By partnering with hospitality brands, smart pillow companies can provide hands-on experiences, effectively creating a “try-before-you-buy” marketing channel.

Long-haul airlines also represent a niche but high-value market for smart pillows that incorporate features such as noise cancellation and temperature regulation. Offering enhanced comfort in business and first-class cabins, these products cater to affluent travelers seeking premium experiences. Expanding into these commercial markets allows manufacturers to diversify revenue streams and strengthen brand visibility among high-income and globally mobile consumers.

Category-wise Analysis

Product Type Insights

The anti-snoring segment holds a market share of 35.2%, making it a dominant product type in the global smart pillow market. Rising awareness of sleep disorders, including Obstructive Sleep Apnea (OSA), has prompted consumers to seek pillows that actively improve breathing patterns and reduce snoring. Products from brands such as Nitetronic and Smart Nora combine ergonomic design with sensor-driven technology to reposition the head and maintain open airways.

Beyond snoring reduction, these pillows appeal to health-conscious consumers looking for preventive solutions. The dual value of comfort and clinical benefit justifies the premium pricing and positions the anti-snoring category as a key revenue driver, influencing broader adoption trends within the smart pillow market.

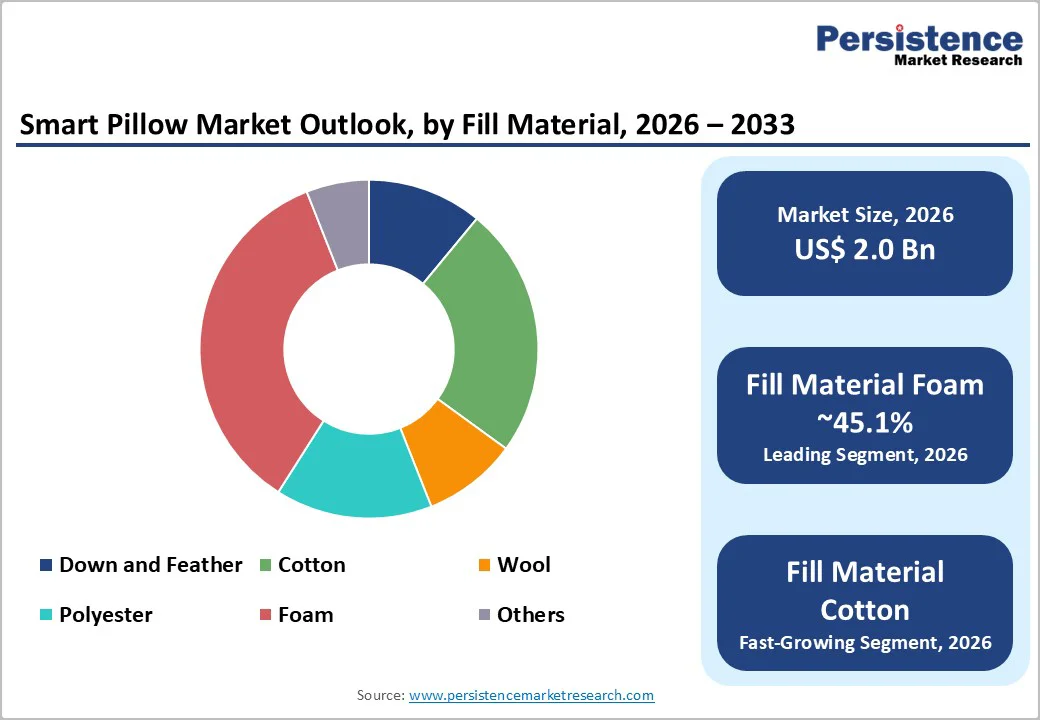

Fill Material Insights

Foam, particularly Memory Foam, commands a market share of 45.1%, establishing it as the leading fill material for smart pillows. Its high-density structure allows for integration of delicate electronic components, sensors, and airbags without compromising user comfort. This stability ensures accurate biometric readings for sleep tracking and other health-monitoring functionalities.

Unlike Down, Feather, or Cotton, which can shift and interfere with embedded sensors, memory foam provides a consistent and moldable base. Additionally, its hypoallergenic properties appeal to wellness-focused consumers. These advantages, combined with durability and comfort, make memory foam the material of choice for both multifunctional and health-oriented smart pillows.

Application Insights

The residential segment dominates the smart pillow market with a 72.1% share, reflecting strong adoption among individual consumers seeking better sleep at home. The rise of the “sleep economy” has positioned the bedroom as a personal wellness hub, where smart pillows act as key devices for improving sleep quality, productivity, and overall health.

Although commercial applications in hotels, hospitals, and wellness retreats are gaining traction, residential users remain the foundational driver of market growth. The ability to purchase directly through e-commerce and access trial offers has further encouraged adoption, making home use the central focus for manufacturers and shaping product design and marketing strategies.

Sales Channel Insights

The online sales channel represents 52.5% of market share, emerging as the fastest-growing route for smart pillow distribution. Brands like Eight Sleep and Nitetronic leverage direct-to-consumer strategies, social media campaigns, and digital education to communicate the features of complex smart pillows effectively.

Online channels also provide benefits such as trial periods, risk-free returns, and detailed product tutorials, helping consumers feel confident about purchasing premium-priced smart pillows. While offline retail remains important for tactile testing, the convenience and reach of online platforms continue to drive the majority of sales growth, reflecting a significant shift toward e-commerce in the smart pillow market.

Regional Insights

North America Smart Pillow Market Trends

North America, led by the United States, holds the largest market share of approximately 38% in the global smart pillow market. The region’s dominance is driven by a tech-savvy population with high disposable incomes and an established ecosystem of sleep technology innovators, such as Sleep Number Corporation and Eight Sleep. Awareness of sleep disorders, including sleep apnea, is high, prompting consumers to adopt preventive and wellness-oriented solutions.

A growing trend in “smart bedroom” integration, where pillows connect with home automation systems such as Apple HomeKit and Amazon Alexa, further drives demand. High connectivity preferences and multifunctional sleep solutions position North America as the most mature and profitable regional market for smart pillows.

Europe Smart Pillow Market Trends

Europe is a significant smart pillow market with a projected CAGR of 7.5% during the forecast period, reflecting steady growth fueled by wellness awareness and stringent regulatory standards. Countries such as Germany, the U.K., and France lead adoption, emphasizing privacy compliance under GDPR and sustainable, eco-friendly materials. Manufacturers like ADVANSA Marketing GmbH leverage these trends, highlighting environmentally responsible fill materials alongside advanced smart features.

The European sleep economy is also influenced by wellness tourism and an aging population seeking non-pharmaceutical solutions for insomnia. Bio-monitoring smart pillows that track health metrics appeal to health-conscious consumers, ensuring consistent demand and making Europe a specialized yet steadily expanding regional market.

Asia Pacific Smart Pillow Market Trends

Asia Pacific is projected to be the fastest-growing region, holding 32% market share, driven by rapid urbanization, rising disposable incomes, and an expanding middle class in countries like China, India, and Japan. The region benefits from being a manufacturing hub for global electronics, allowing companies such as Xiaomi and GioClavis Co. Ltd. to produce smart pillows at competitive price points.

Cultural factors, especially in Japan, where work-related stress and sleep deprivation are common, create a strong demand for high-tech relaxation and wellness products. The widespread availability of affordable IoT devices in Chinese households further accelerates adoption. These factors position the Asia Pacific as a high-potential region for growth, combining affordability, innovation, and urban consumer demand.

Competitive Landscape

The smart pillow market is moderately fragmented, featuring a mix of well-established bedding companies and agile tech startups. Large incumbents leverage their broad retail presence and brand recognition to integrate smart features into their products, targeting a wide consumer base. In contrast, smaller, specialized players focus on niche solutions addressing specific sleep issues, such as snoring or temperature regulation, often delivering high-efficacy and tailored experiences.

Market competition is heavily driven by innovation and R&D investments. Key differentiators include proprietary algorithms, AI-enabled sleep coaching, advanced sensors, and patent-protected technologies. Companies continually enhance functionality and user experience to maintain a competitive edge and capture growing demand.

Key Market Developments:

- In August 2025, Sleep secured US$ 100 Million in Series D funding to accelerate its AI roadmap, specifically developing a "Sleep Agent" to detect apnea and other medical conditions, signaling a major pivot toward medical-grade sleep tech.

- In July 2025, Sleep Number Corporation reported its Q2 2025 results, highlighting a strategic restructuring and cost-savings plan while emphasizing continued investment in its "Smart Bed" ecosystem to drive future profitability

- In November 2024, Smart Nora announced a partnership with Sunset Healthcare Solutions to distribute its contact-free snoring solution through Durable Medical Equipment (DME) providers, expanding its reach into the professional healthcare channel.

Companies Covered in Smart Pillow Market

- REM-Fit

- Smart Nora

- Moona

- Sleep Number Corporation

- Eight Sleep

- Xiaomi

- Nitetronic

- Sunrise Smart Pillow

- iSense Sleep

- GioClavis Co. Ltd.

- Sleepace

- Dreampad

- ADVANSA Marketing GmbH

- Tempur‑Sealy International

- Hollander Sleep Products

Frequently Asked Questions

The global smart pillow market is forecast to reach a value of US$ 11.1 Billion by the end of 2033.

Growth is primarily driven by the increasing prevalence of sleep disorders like insomnia and apnea, alongside the rapid expansion of smart home ecosystems.

Foam, particularly memory foam, holds the largest market share at 45.1%, due to its stability for housing sensors, ergonomic support, and hypoallergenic properties.

North America leads the market with a 38% share, supported by high consumer spending on health tech, a tech-savvy population, and the presence of major smart pillow manufacturers.

Integrating medical-grade diagnostics to detect conditions like sleep apnea and obtaining FDA clearance represents a major revenue opportunity for market players.

Key players include Sleep Number Corporation, Eight Sleep, Nitetronic, Smart Nora, Xiaomi, and Tempur-Sealy International.