- Home Appliances

- Smart Electric Heaters Market

Smart Electric Heaters Market Size, Share, and Growth Forecast 2026 - 2033

Smart Electric Heaters Market by Product Type (Smart Space Heaters, Smart Water Heaters, Smart Panel Heaters, Smart Infrared Heaters, Smart Baseboard Heaters, Smart Portable Heaters), by Distribution Channel (Online, Offline), by Application (Residential, Commercial), by Regional Analysis, 2026 - 2033

Smart Electric Heaters Market Size and Trend Analysis

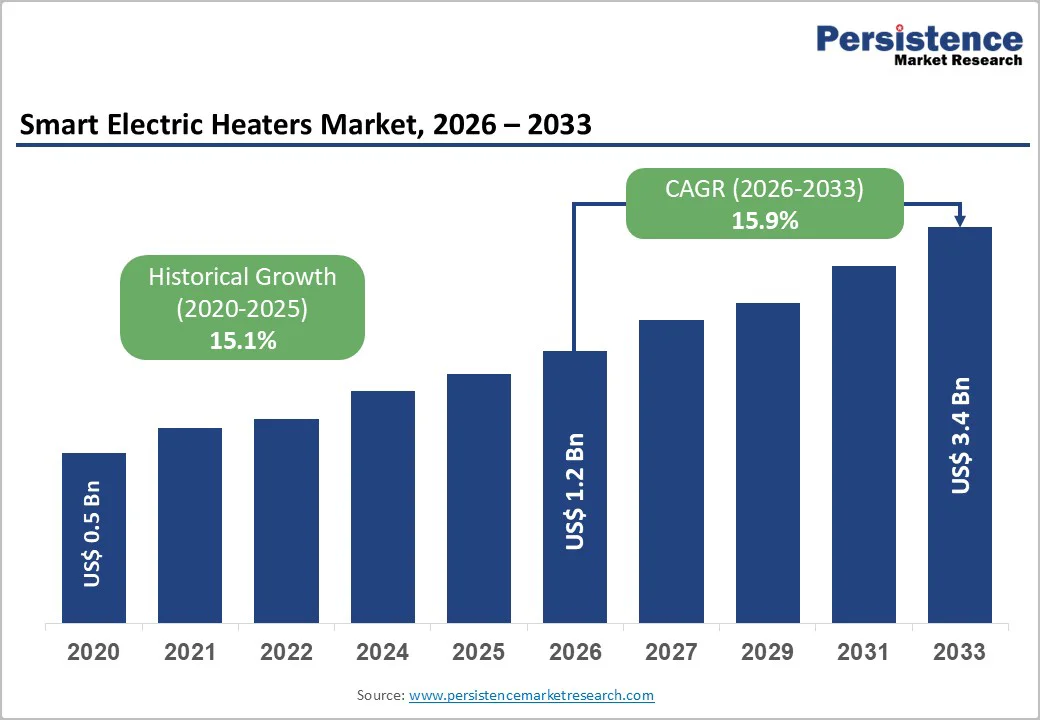

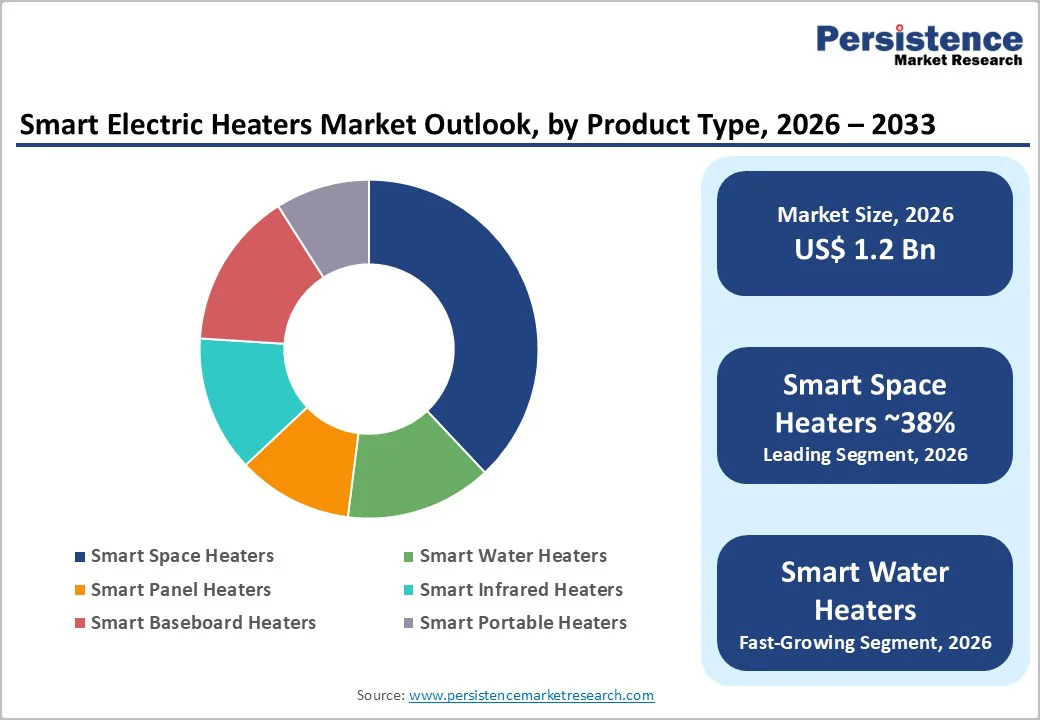

The global smart electric heaters market size is likely to be valued at US$ 1.2 Billion in 2026 and is expected to reach US$ 3.4 Billion by 2033, growing at a CAGR of 15.9% during the forecast period from 2026 and 2033.

The market expansion is primarily driven by escalating consumer demand for energy-efficient heating solutions amid rising electricity costs and heightened environmental consciousness. The proliferation of smart home ecosystems and IoT integration has fundamentally transformed the heating appliance industry, with advanced features such as Wi-Fi connectivity, programmable thermostats, and voice assistant compatibility becoming standard expectations among consumers.

Key Market Highlights

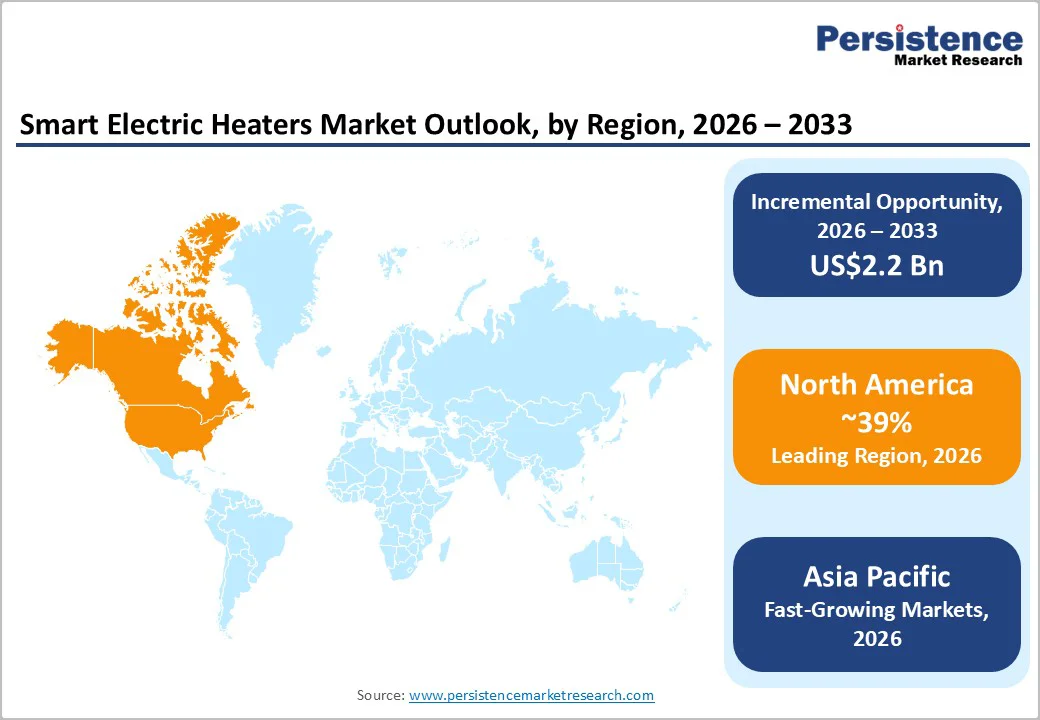

- Leading Region: North America maintains dominant market position with approximately 39% global share, driven by high smart home penetration, established regulatory frameworks supporting energy efficiency, and presence of major industry players advancing connected heating technologies.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market with CAGRs exceeding 18%, propelled by rapid urbanization in China, India, and ASEAN nations, rising disposable incomes, and accelerating smart home ecosystem adoption.

- Dominant Segment: Smart Space Heaters command approximately 38% market share within product type segmentation, reflecting versatile applicability, portable convenience, and advanced IoT integration capabilities valued by residential and commercial consumers.

- Fastest Growing Segment: Smart Water Heaters demonstrate rapid expansion driven by increasing demand for energy-efficient hot water solutions, IoT connectivity features, and integration with smart home platforms enabling remote monitoring and scheduling.

- Key Market Opportunity: Integration with utility demand-response programs and smart grid infrastructure presents substantial growth potential, enabling manufacturers to deliver grid-responsive heating solutions that provide bill credits while supporting renewable energy optimization.

| Key Insights | Details |

|---|---|

| Smart Electric Heaters Market Size (2026E) | US$ 1.2 Billion |

| Market Value Forecast (2033F) | US$ 3.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 15.9% |

| Historical Market Growth (2020 - 2025) | 15.1% |

Market Dynamics

Market Growth Drivers

Energy-efficient heating adoption accelerates as consumers seek cost savings, climate-friendly technologies, and advanced smart temperature optimization

The accelerating adoption of energy-efficient heating devices represents a primary catalyst for market expansion. According to the U.S. Energy Information Administration, residential water heating accounts for approximately 18% of total energy consumption in American homes, making it a crucial area for efficiency improvements. Smart electric heaters equipped with programmable thermostats, occupancy sensors, and adaptive learning algorithms enable precise temperature control and significant energy savings.

In 2025, Honeywell Home thermostat users achieve average savings of 22% on heating and 17% on cooling energy consumption when utilizing recommended scheduling features consistently. This substantial cost reduction potential, combined with growing consumer awareness of climate change implications, continues to drive purchasing decisions toward intelligent heating solutions that optimize energy usage without compromising comfort levels.

Smart electric heaters gain momentum through seamless IoT integration, enabling remote control, automation, and intelligent home energy management

The seamless integration of smart electric heaters with broader smart home ecosystems has emerged as a transformative growth driver. The global connected IoT devices reached approximately 18.5 billion in 2024, representing a 12% growth over the previous year, creating an expansive foundation for sophisticated energy management systems. Modern smart electric heaters leverage Wi-Fi connectivity, enabling remote control through smartphone applications, voice command compatibility with platforms including Amazon Alexa, Google Assistant, and Apple HomeKit.

The ABI Research indicates that smart thermostats will achieve over 45% adoption in Western European and North American households, with 67.2 million devices expected to ship globally by 2030. This connectivity revolution enables features such as automatic away modes, real-time energy tracking, and integration with utility demand-response programs, substantially enhancing the value proposition for consumers seeking comprehensive home automation solutions.

Market Restraints

Premium pricing, installation expenses, and infrastructure requirements limit widespread adoption of smart electric heaters in cost-sensitive markets

The premium pricing of smart electric heaters compared to conventional heating devices presents a significant barrier to mass market adoption. Advanced smart heating systems often cost substantially more than traditional alternatives, creating affordability challenges particularly in price-sensitive emerging markets. The requirement for professional installation in nearly half of thermostat purchases adds to the overall cost burden for consumers.

Furthermore, the need for compatible infrastructure including reliable Wi-Fi networks and updated electrical systems can compound initial investment requirements, potentially limiting market penetration among budget-conscious households and smaller commercial establishments seeking cost-effective heating solutions.

Data privacy risks, cybersecurity vulnerabilities, and inconsistent connectivity hinder consumer trust and adoption of connected heating devices

Data privacy and cybersecurity vulnerabilities associated with connected heating devices continue to impede market growth among security-conscious consumers. As smart electric heaters collect and transmit personal behavioral data regarding usage patterns, temperature preferences, and occupancy information, concerns regarding data protection have intensified.

Regulatory frameworks in the United States and Europe are evolving to address how smart devices communicate and store data, creating compliance complexities for manufacturers. Additionally, connectivity limitations in regions with inadequate internet infrastructure and the fragmented nature of smart home protocols create interoperability challenges that undermine consumer confidence in adopting connected heating technologies.

Market Opportunities

Smart heaters unlock new opportunities through demand-response participation, enabling grid stability, renewable energy use, and homeowner incentives

The growing implementation of utility-based demand-response programs presents substantial opportunities for smart electric heater manufacturers. Smart thermostats and connected heating devices serve as pivotal components for helping electrical grids manage peak loads, particularly as electrification of heating systems accelerates. Rheem Manufacturing Company has introduced Professional Prestige Smart Electric Water Heaters with built-in demand response capabilities, featuring CTA-2045 ports enabling seamless connection to utility programs.

Companies including Centrica and Glen Dimplex have launched trials demonstrating how smart storage heaters can function within virtual power plant platforms, storing renewable energy when abundant and releasing it during peak demand periods. This integration allows homeowners to potentially earn bill credits while contributing to grid stability, creating compelling value propositions that extend beyond individual energy savings to broader sustainability objectives.

Global electrification trends and fossil fuel phase-outs create strong growth potential for affordable, smart, energy-efficient heating technologies

The global transition toward electrification of residential heating, driven by decarbonization mandates and the phase-out of fossil fuel heating systems, creates expansive growth opportunities. The European Union's revised Energy Performance of Buildings Directive requires member states to plan for complete phase-out of fossil fuel boilers by 2040, with financial incentives for fossil fuel boilers discontinued from January 2025.

In China, heat-pump sales rose 12% in 2023, highlighting appetite for plug-and-play electric comfort solutions. The Asia Pacific smart home market is growing significantly with countries including China, India, Japan, and South Korea demonstrating increasing adoption of intelligent heating technologies. Manufacturers capable of delivering affordable, feature-rich smart heating solutions tailored to regional requirements can capture significant market share as governments worldwide implement policies supporting clean energy heating transitions.

Category-wise Insights

By Product Type Analysis

The Smart Space Heaters segment commands the dominant market position, accounting for approximately 38% of total market share. This leadership stems from the versatile functionality and broad applicability of smart space heaters across diverse residential and commercial environments. Portable smart space heaters have gained particular traction due to their ease of movement, plug-and-play usability, and minimal installation requirements, making them ideal for apartments, rental properties, and zone-specific heating applications. The segment benefits from substantial innovation in ceramic heating elements, infrared technology, and Wi-Fi-enabled controls that deliver precise temperature management, occupancy sensing, and remote access capabilities highly valued by modern consumers.

By Distribution Channel Analysis

The Offline distribution channel maintains market leadership with approximately 65% revenue share, reflecting consumer preferences for hands-on product experience when purchasing high-value home appliances. Physical retail channels including electronics stores, home improvement centers, and specialty appliance outlets offer critical advantages including product demonstrations, professional consultation, and immediate availability that build consumer confidence.

However, the Online segment is experiencing accelerated growth as e-commerce platforms provide convenience, competitive pricing, and extensive product selection. Digital retail advancements including virtual product displays, AI-enabled shopping assistants, and doorstep delivery services are progressively capturing market share, particularly among tech-savvy urban consumers. The channel landscape continues evolving toward omnichannel models that combine online research with offline purchase experiences.

By Application Analysis

The Residential segment dominates the application landscape, representing approximately 64% of market share, driven by escalating consumer demand for convenient, energy-efficient home heating solutions. Rising adoption of smart home technologies among homeowners seeking enhanced comfort, remote control capabilities, and reduced utility bills underpins this segment leadership. The U.S. Census Bureau data indicates that 42% of U.S. households reported electricity as their main space heating fuel in 2024, reflecting the growing transition toward electric heating in residential settings.

Features including programmable thermostats, occupancy sensors, and smart home ecosystem integration particularly resonate with residential consumers prioritizing convenience and cost savings. The commercial segment demonstrates promising growth potential as businesses leverage connected heating systems for centralized control, operational efficiency optimization, and sustainability compliance across office buildings, retail establishments, and hospitality facilities.

Regional Insights

North America Smart Electric Heaters Market Trends

North America leads the global smart electric heaters market with nearly 39% share, supported by early technology adoption, widespread smart home infrastructure, and strong consumer awareness of energy savings. The United States remains the largest contributor, with over 40% of homes using smart devices, strong ENERGY STAR-backed efficiency programs, and ongoing investments in home automation. Major players such as Honeywell and Rheem are driving innovation through AI-optimized heating, demand-response capabilities, and connected water heaters.

Favorable regulations, including utility rebates and DOE efficiency standards, continue accelerating adoption across residential and commercial segments. Canada shows strong future potential as colder regions increase reliance on efficient electric heating and government programs support electrification. A key emerging trend is the integration of smart heaters into virtual power plants (VPPs), enabling grid-responsive heating that supports renewable energy balancing and peak-load management, reshaping the overall market landscape.

Europe Smart Electric Heaters Market Trends

Europe holds around 20% of the global market and remains a high-value region driven by strict sustainability mandates and advanced energy-efficiency regulations. The updated Energy Performance of Buildings Directive (EU/2024/1275) sets zero-emission standards for new buildings and requires a phase-out of fossil fuel boilers by 2040, significantly boosting demand for electric and smart heating solutions. Germany leads adoption with strong renovation activity and widespread use of high-efficiency heating systems.

The United Kingdom is rapidly shifting toward low-emission technologies such as heat pumps and smart electric heaters, supported by government incentives and rebate schemes. France, through ADEME-backed programs, continues to push energy-efficient modernization. Spain is the region’s fastest-growing market, driven by rising urbanization, stronger internet access, and government-backed smart home subsidies. European consumers increasingly prefer electric heating, with smart room heaters projected to reach 30% household adoption, creating opportunities for IoT-enabled, eco-friendly solutions.

Asia Pacific Smart Electric Heaters Market Trends

Asia Pacific is the fastest-growing region, forecast to expand at a CAGR above 18% due to rapid urbanization, a rising middle class, and expanding smart home ecosystems across China, India, Japan, and ASEAN markets. China leads regional growth at around 11.6% CAGR through 2035, supported by strong demand for electric heating, large-scale residential construction, increasing heat pump adoption, and government-led energy-efficiency initiatives.

India is emerging as a major opportunity with a 10.8% CAGR, driven by rising heating needs in northern regions, increasing household incomes, and growing awareness of energy-efficient appliances. Brand initiatives, such as Panasonic Life Solutions’ IoT-enabled water heaters, highlight rising demand for smart, affordable heating. Japan remains a technology leader, especially in heat pumps and HVAC systems, with companies like Mitsubishi Electric expanding smart-connected product portfolios. Growing use of voice assistants, IoT platforms, and integrated home ecosystems is further accelerating adoption across diverse climates and consumer segments.

Competitive Landscape

Market Structure Analysis

The global smart electric heaters market is moderately fragmented, featuring established multinationals and regional specialists. Key players like Honeywell, Mitsubishi Electric, and Rheem dominate with diverse product lines and strong R&D investments. Technology differentiation is crucial, with a focus on IoT integration, AI optimization, and compatibility with smart home systems. Increased strategic acquisitions, such as A.O. Smith's purchase of Pureit from Unilever in 2024, highlight market consolidation. Emerging trends include energy-as-a-service, utility partnerships for demand-response programs, and subscription-based trials, allowing manufacturers to create recurring revenue and enhance consumer access to smart heating solutions.

Key Market Developments

- In January 2025: Resideo Technologies unveiled the Honeywell Home X2S smart thermostat at CES 2025, featuring Matter compatibility, ENERGY STAR certification, and pricing at US$79.99, delivering significant energy savings of 22% for heating and 17% for cooling applications.

- In November 2024: Dyson launched new Hot+Cool purifiers (HP2 De-NOx and HP1) in India featuring intelligent sensors, Air Multiplier technology, and MyDyson app connectivity for year-round heating, cooling, and air purification with voice control compatibility.

- In September 2024: Haier announced expansion of its Full Smart Energy Management system at IFA 2024, integrating AI-powered appliance control with real-time energy cost data through the hOn app platform, advancing sustainable smart living objectives.

Companies Covered in Smart Electric Heaters Market

- Honeywell International Inc.

- Zehnder Group

- Haier Electronics Group Co., Ltd.

- Mitsubishi Electric Corporation

- A.O. Smith

- Siemens AG

- Danfoss

- Rheem Manufacturing Company

- Glen Dimplex

- Panasonic Corporation

- LG Corporation

- Carrier Global Corporation

- Electrolux AB

- Dyson Ltd.

Frequently Asked Questions

The global Smart Electric Heaters Market is projected to reach US$ 3.4 Billion by 2033, expanding from US$ 1.2 Billion in 2026 at a CAGR of 15.9% during the forecast period 2026 - 2033.

Key demand drivers include rising consumer preference for energy-efficient heating solutions, integration with smart home ecosystems and IoT technology, escalating electricity costs prompting adoption of intelligent energy management, government regulations promoting energy efficiency, and the growing transition toward electrification of residential heating systems globally.

Smart Space Heaters dominate the market with approximately 38% share, driven by their versatile functionality across residential and commercial applications, portable convenience, advanced IoT integration capabilities, and features including Wi-Fi connectivity, programmable thermostats, and voice assistant compatibility.

North America maintains market leadership with approximately 28-29% global share, underpinned by high smart home penetration rates, robust regulatory frameworks supporting energy efficiency, presence of major industry players, and substantial consumer awareness regarding energy-saving benefits of connected heating technologies.

Key opportunities include expansion of utility demand-response program integration, accelerating electrification of heating systems amid fossil fuel phase-out mandates, growth in emerging markets particularly Asia Pacific, advancement of AI-enabled optimization features, and development of grid-responsive heating solutions supporting renewable energy utilization.

Key market players include Honeywell International Inc., Mitsubishi Electric Corporation, Rheem Manufacturing Company, Haier Electronics Group Co., Ltd., A.O. Smith, Siemens AG, Danfoss, Glen Dimplex, Panasonic Corporation, LG Corporation, Carrier Global Corporation, Dyson Ltd., and Electrolux AB, among others competing through technology differentiation and smart home ecosystem integration.